NBNKF - Nordea Bank: Slow Rise In Rates Is Better Than Fast

2023-06-22 04:32:51 ET

Summary

- Nordea is not seeing immense loan growth, but NIM is great thanks to what we identified as a favourable duration gap.

- Growth could have been more were it not for some deposit hedges.

- There was some pressure on the very bottom line due to taxes on their Swedish lending book in order to impose some risk-related costs.

- While we like Nordea, we think DNB is a more interesting pick due to the MobilePay angle.

Nordea ( NRDBY )( NBNKF ) is a pan-Nordic bank that has put in some phenomenal result YoY, and its loan book is pretty safe. But Sweden has been a bit of a problem for it both on the organic business side and also on the regulatory side. We also have a better Nordic banking pick in DNB Bank ( DNBBY ). While you must do your own due diligence , withholding taxes should be much more favourable with a Norwegian pick over a Finnish pick at 25%. Moreover, we believe there is a much more pronounced value angle due to their stake in one of the most essential banking and ID platforms in Norway. So while Nordea is solid, it's uninteresting compared to DNB.

Q1 2023 Nordea Results

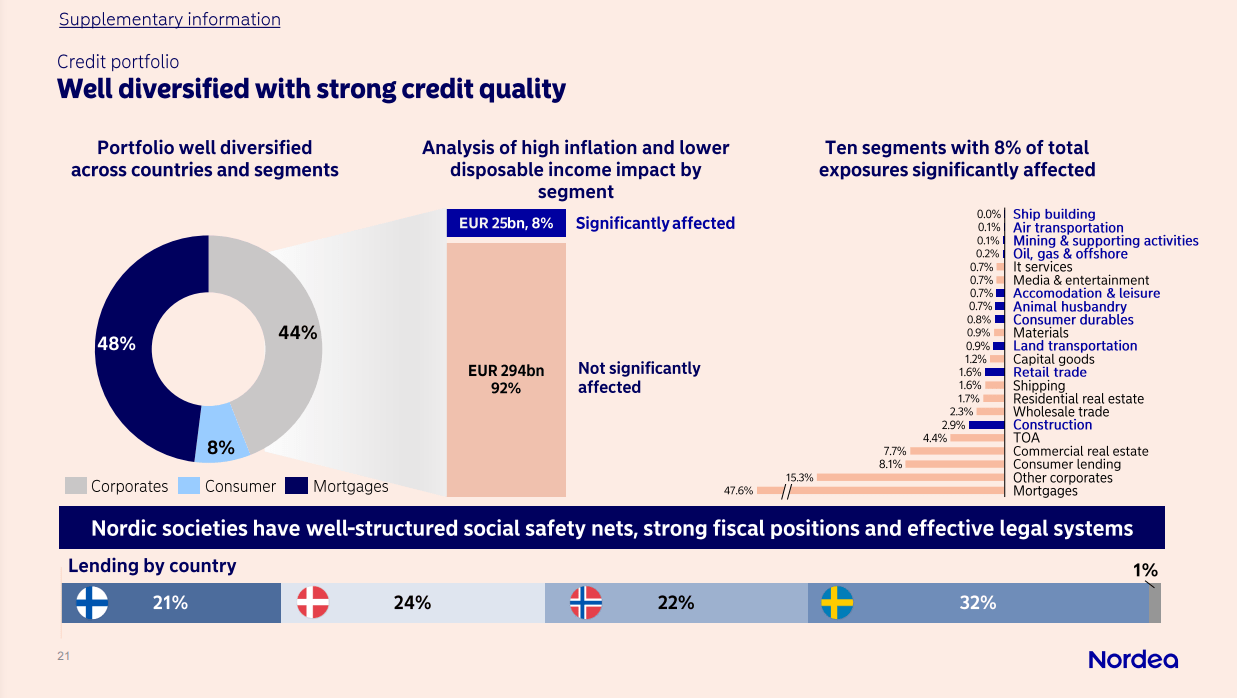

Let's start looking at the credit portfolio in terms of exposures.

{kind=link}

We agree with how Nordea has divvied up the industries into more and less exposed buckets. Ultimately, the commercial loans do not look concerning, and the large exposure to mortgages is also not a major concern all thanks to the differentiated rate regime in Nordic countries. While the US is being aggressive in its rate hikes, the Nordic countries, with Sweden somewhat of an exception, are going much slower. A slow rise in rates is a lot better for banking institutions because it firstly precludes issues around bank assets and bank solvency on interest rate risks as we've seen in regional banking in the US. Moreover, it allows the spread between deposit rates and lending rates to be better managed.

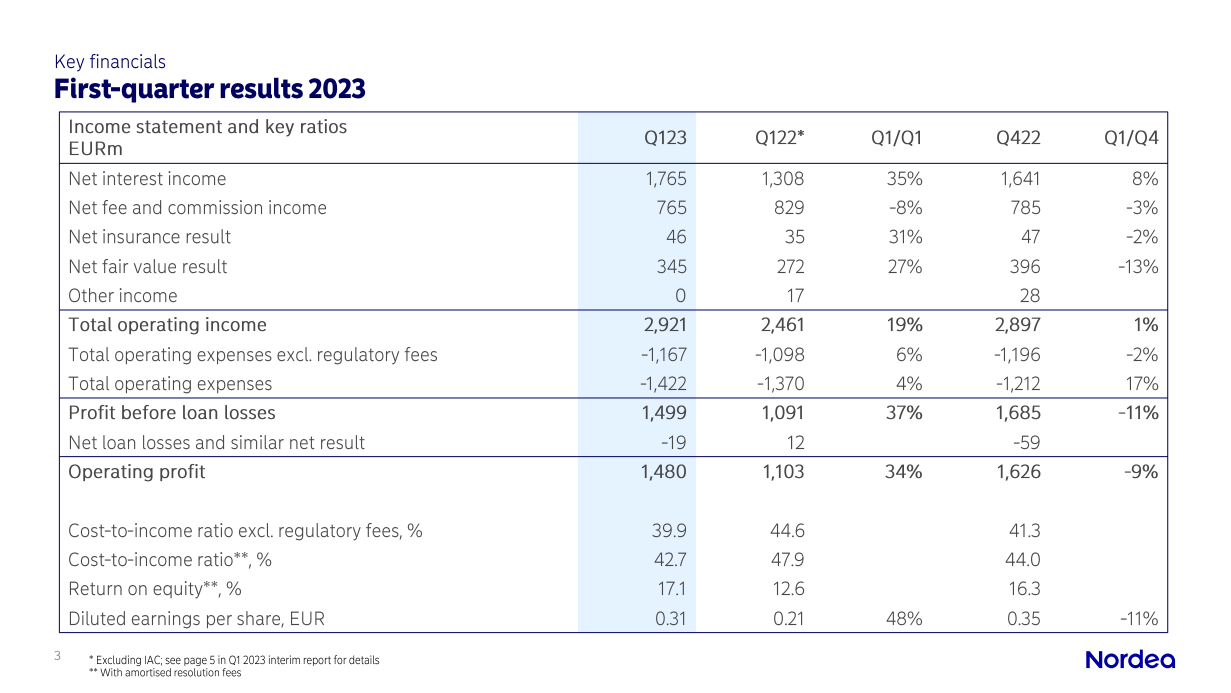

In our previous coverage of Nordea we pointed out that there was going to be a lot of rollover into higher rate plans due to the maturity structure on the asset side. A nicer duration gap than some competitors on top of a slower rate rise which leads to lower deposit beta has been a major boost for Nordea's NI which has rocketed YoY.

{kind=link}

Loan volumes have been up in the mid-single digits which is not aggressive, and the pressure that higher rates and inflation puts on markets like real estate is consistent with this. Again, it's the NIM that has been driving the growth in rates.

We should note that while SG&A was controlled and while growing net interest income managed to grow income YoY, increases in taxes imposed on the asset book in Sweden have grown regulatory fees substantially and actually caused net income declines on a quarterly basis, despite the fact that NI grew sequentially as well. This tax is being imposed by the Swedish government on large financial institutions to create a bit of a false equity hit in order to force them to manage their risk and growth more responsibly. It is not good for shareholders as seen clearly in the net income evolution.

Finally, we note the fee and commission income. Nordea is a full service bank and does all sorts of things like asset management and investment banking. Market volatility has not helped these divisions, and generally weaker economic conditions with less interest in Nordic markets won't help the picture. This part of the business is down, but the lending and deposit business is ultimately more important.

Bottom Line

Nordea is a pretty good pick, and we admire the quarterly results, but there's better value out there in those regions that shouldn't hurt dividend intakes as much for US investors. We're talking about DNB, which we covered here for your reference. The business case is pretty similar to Nordea except it is more levered to deposit and lending as opposed to Nordea, which is more skewed to commission and fee based income. This is already a first positive. But the main reason we prefer DNB is because of the value angle from its major stake in MobilePay, which is a payment and ID portal that is essential for things like paying your taxes and generally accessing government portals and your bank account. It has other businesses in it like Vipps which is like Venmo except even more dominant in its own market. We think that about 10% of market cap can be accounted for by the MobilePay stake. For large businesses like these that's an important source of margin. With recovery in private markets to come eventually and with these businesses being major growers, that margin of safety could become more pronounced. Overall, DNB is our preferred pick, also because we prefer the more pronounced Norwegian focus which is the richest and safest economy up north.

For further details see:

Nordea Bank: Slow Rise In Rates Is Better Than Fast