NBNKF - Nordea Bank: What's Good And What's Not

2023-03-09 14:40:42 ET

Summary

- Nordea's NII trajectory looks comforting enough, and it should help mitigate cost pressures linked to inflation.

- We like Nordea’s management, and their expertise is reflected in the progression of some key metrics.

- Some of Nordea’s key focus markets are likely to slow, and asset quality may deteriorate.

- Nordea doesn’t offer much value, and the charts look overbought.

Introduction

Nordea Bank Abp ( NRDBY ) is the largest player in the Nordics banking market and operates four key segments- personal banking, large corporates & institutions, business banking, and asset & wealth management. The bank has a vast household customer base of 10m, and a corporate customer base of 0.6m; these focus segments are serviced through 320 odd branches & call centers, spread across the Nordics area.

At this juncture, we have a neutral opinion on the ADR of Nordea Bank. This article will focus on both the good and bad facets of pursuing an investment in Nordea at this juncture.

What’s Good?

In a hawkish rate environment, most banks’ NII profiles tend to flourish, and Nordea is no exception. Even if the impact of deposit betas could weigh more heavily on Nordea’s interest expenses this year, the overall NII profile of Nordea is still expected to be rather resilient through FY24. Also note that structurally Nordea has been well-positioned with its funding costs which are well below the Nordic and European averages.

Annual Report

All in all, Nordea management expects higher policy rates to boost Nordea’s incremental NII by EUR 1200-1700m, with over 85% of the benefits coming through in FY23 itself.

FY22 Presentation

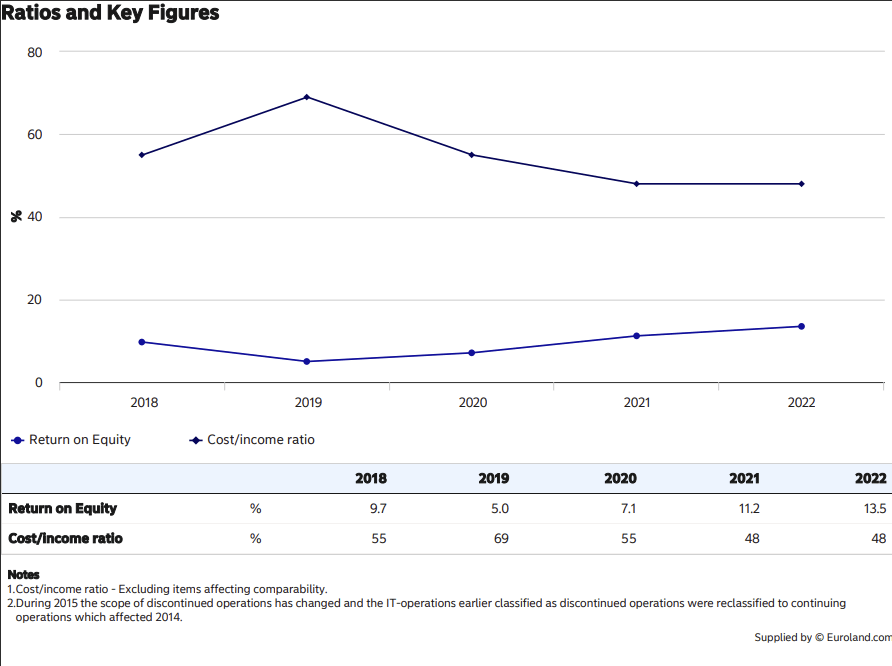

Nonetheless, the alluring NII sub-plot provides a solid foundation for Nordea to get closer to its 2025 cost-to-income (OPEX as a function of NII and non-interest income) target of 45-47%. The cost-to-income ratio is a fitting metric to gauge management efficiency in the banking sector. As noted in the image below, there's been a marked improvement in this ratio over the last 4 years (last year it came in at 47.5%). Likewise, even Nordea's ROE has trended up impressively over the years, and in FY22 the bank managed to hit its >13% ROE target ahead of schedule (they were looking to achieve this by 2025). In FY23, management thinks this could exceed 13% once again.

{kind=link}

Investors should note that Nordea will likely see a 5% increase in its cost base this year, but some component of the cost increase is linked to management pre-empting regulatory requirements and getting ahead of the curve by deepening its risk management processes. Areas like financial crime prevention are likely to gain traction in the periods ahead, and it’s comforting to note that Nordea is one step ahead.

Nordea also offers a lot of qualities that should appeal to income investors. It has been paying dividends for 13 years now, and recently the dividend was hiked by an impressive 16%, well above the historical hike of 7.4%, and the typical banking median hike of 7.4%. In effect, you’re staring at a rock-solid yield of close to 7%, which could come in very handy during drawdowns!

What’s Not

Even though Nordea finances various market segments, the subdued prospects of one segment, in particular-mortgages, will reflect heavily on the bank's loan growth potential (Mortgage accounts for 48% of total loans, 3x higher than the next biggest segment).

FY22 Presentation

Excess monetary tightening in some of Nordea’s key regional markets has taken the wind out of the sails of the mortgage part of the loan book. In Q4, Nordea’s mortgage volumes only grew by 2% YoY, and this is unlikely to improve, with management expecting a 1-2% cadence through FY23.

Even though Nordea offers exposure to all the Nordic markets, the economic developments in Denmark and Sweden have a more pronounced effect on the bank, as those two regions jointly account for around ~60% of the total operating income of the bank. Both regions are staring at fairly underwhelming outlooks in the near term. Sweden is looking at a 2% decline in real GDP for 2023, whilst Denmark could witness a decline of 0.5% for the same period.

An important component of Swedish net worth - housing - is in a slump with home prices expected to make a peak-to-trough decline of 20% this year. With limited incentive to construct, Nordea expects housing starts in Sweden to drop by 63% through FY25, from the 68000 levels seen at the end of FY21. One also ought to be mindful of the debt servicing ability of the Swedish populace as hiring plans dim. Unemployment is poised to increase from 7% to 8.5% by the end of FY21 whilst the household financial savings level is already in negative territory.

Nordea

In Denmark, Nordea’s export-oriented clients will likely have limited incentive to invest (and take on more credit), as there’s been a drop in export values and freight rates compared to what we saw 12-18 months ago.

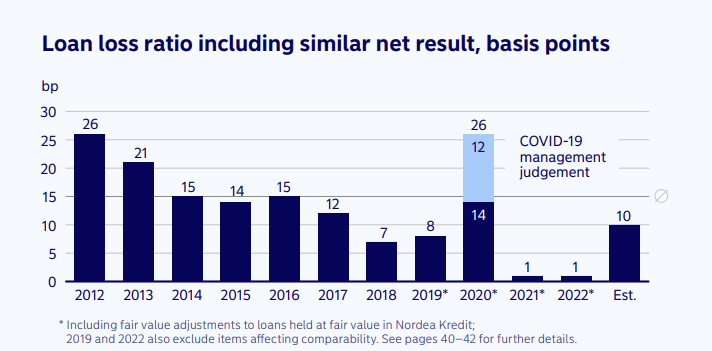

Considering the tricky macros in Nordea’s key markets, it is no surprise to discover that after two subdued years, the net loan loss ratio (net loan losses as a function of the carrying amount of loans) in FY23 could rise to 10bps.

{kind=link}

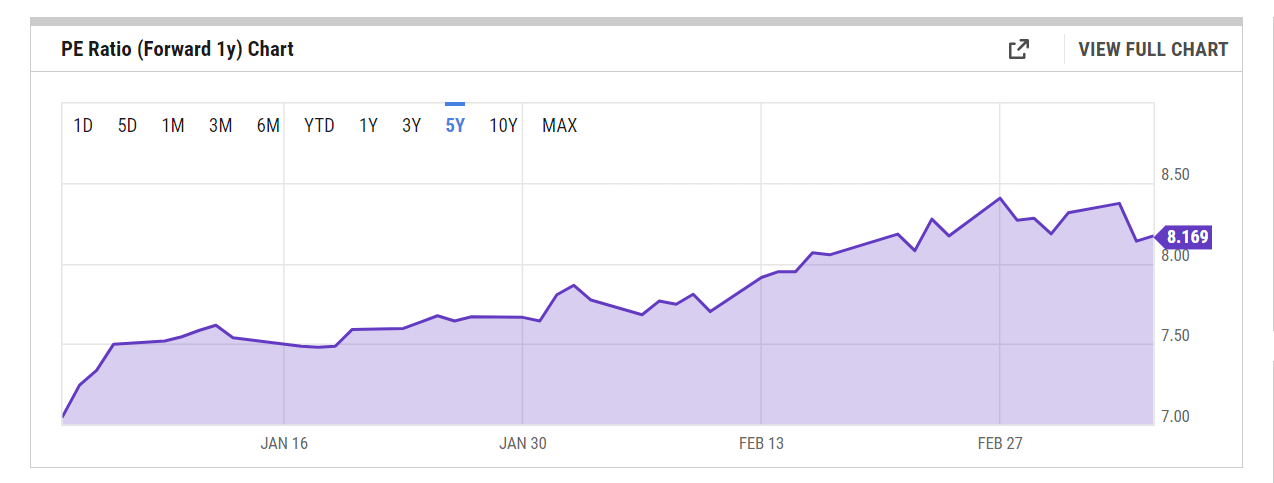

Then, according to consensus estimates for FY24, Nordea will likely only deliver subdued annual earnings growth of just 1.2% . Considering that underwhelming figure, the valuations do feel a bit dear, more so, as it exceeds the historical average. Based on the FY24 numbers, on a forward P/E basis, NRDBY trades at a figure of 8.2x, ~5% higher than the mean of 7.8 x.

{kind=link}

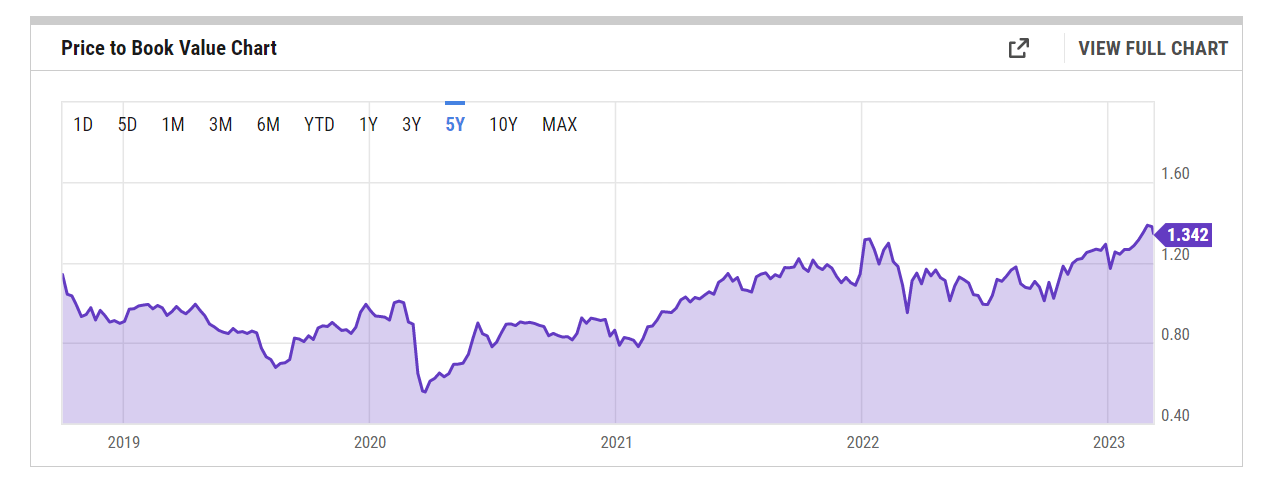

Even on a price-to-book value basis, the narrative does not change; if anything, things look a lot more daunting when you consider that traditionally, this is a stock that has mostly always traded below book value (0.98x). Currently, the premium over the P/BV mean is quite significant at 35% !

{kind=link}

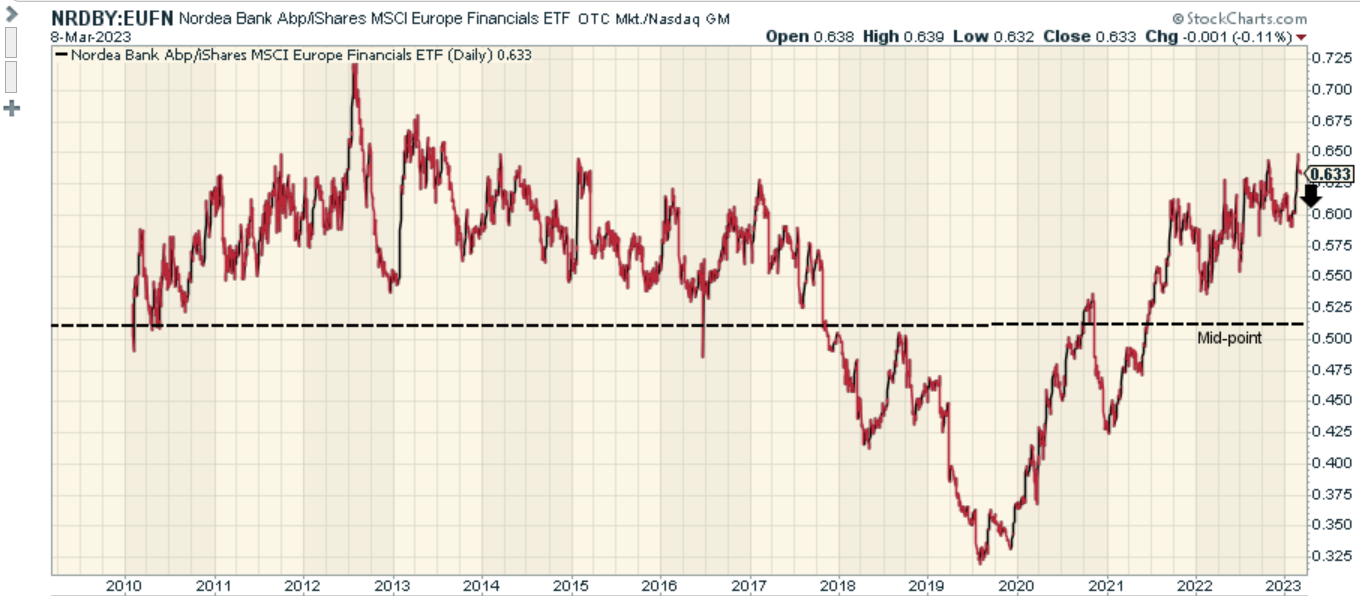

Then, if one looks at a ratio measuring the relative strength of the Nordea stock and a portfolio of European financial stocks, we can see that this ratio looks overbought, trading well above the mid-point of its life-long range. This may prompt investors to rotate out of Nordea and move into other companies which offer better value.

{kind=link}

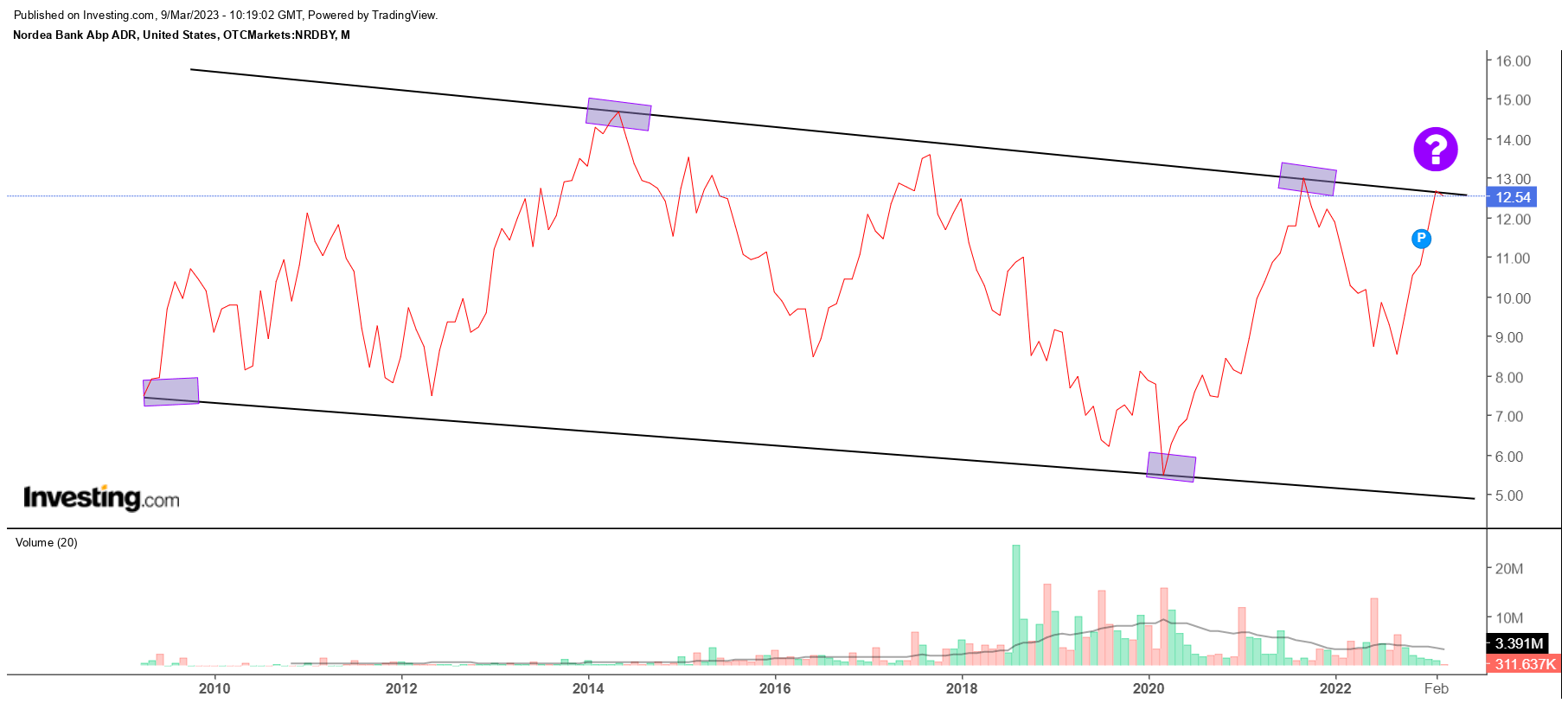

Finally, if you look at the price imprints on Nordea’s long-term chart, it’s not hard to miss the crucial pivot points that have come about every now and then. Unfortunately, NRDBY has recently just hit the upper boundary of its channel. we think it would be unwise to deploy your resources at this juncture as the stock appears to have hit another pivot point.

{kind=link}

To conclude, Nordea Bank is a HOLD.

For further details see:

Nordea Bank: What's Good, And What's Not