NBNKF - Nordea: Cautious Ahead Of Full-Year Results

2024-01-03 01:54:59 ET

Summary

- Boosted by consecutive quarters of outperformance, Nordea has started 2024 on a high.

- From here, though, the P&L outlook gets a lot more challenging.

- At the current premium to book, I see no reason to move off the sidelines.

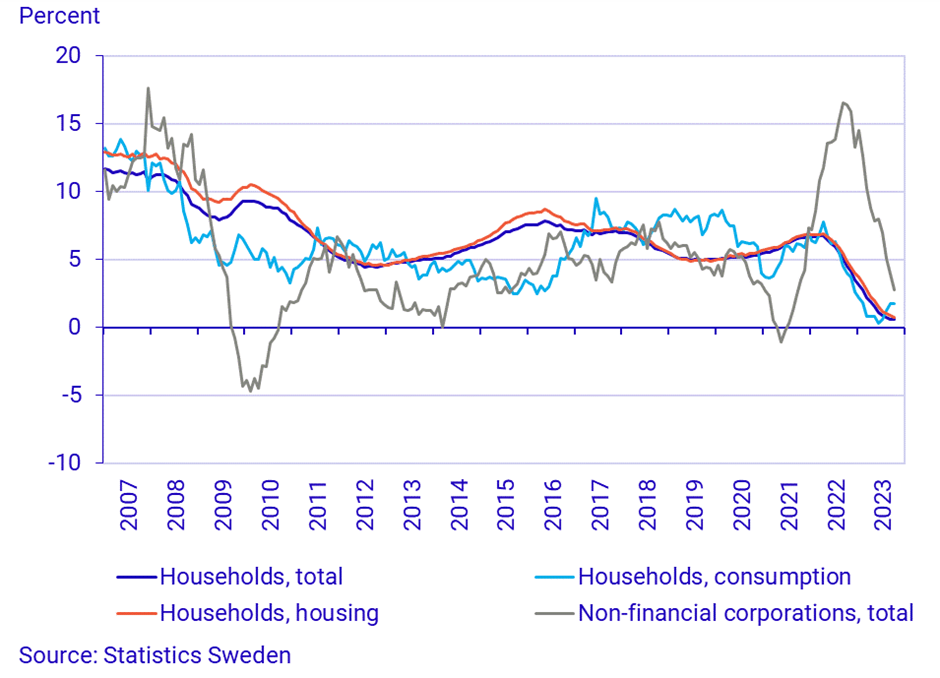

Nordea (NRDBY), the leading Nordic bank, has had its share of underperforming years in the past, but under CEO Vang-Jensen, profitability is back on track. Yet, the path back to a peer-level return on equity profile will be complicated by a challenged near-term backdrop for banks. For one, the lagged impact of a series of rate hikes in the Nordics has yet to fully work through the system – per recent Swedish data , mortgage balances and corporate lending are slowing down and, in some instances, already contracting.

Nordea may be the pick of the large banks, but the source of its strength, corporate loan demand, is fading quicker than other categories; in tandem, Nordea may suffer disproportionately relative to its peers. Deposit retention isn’t going much better in an environment of household-led deposit outflows. Nordea’s higher Euro-denominated deposit base as well (forward curves imply more Euro rate cuts than for the Nordics) also means it will be going up against more net interest margin pressures ahead. Having re-rated in recent months, the stock isn’t cheap either at the current premium to tangible book. Net, I would steer clear ahead of next month’s full-year update.

Guidance Bar Raised on ‘Higher for Longer’ Expectations

It’s been consecutive quarters now that Nordea has outpaced guidance and consensus expectations. That said, the size of its beats and raises are narrowing – a result of slowing net interest income expansion. Still, management kept full-year guidance numbers unchanged at a “comfortably above” 15% return on equity - despite potential post-Q4 headwinds.

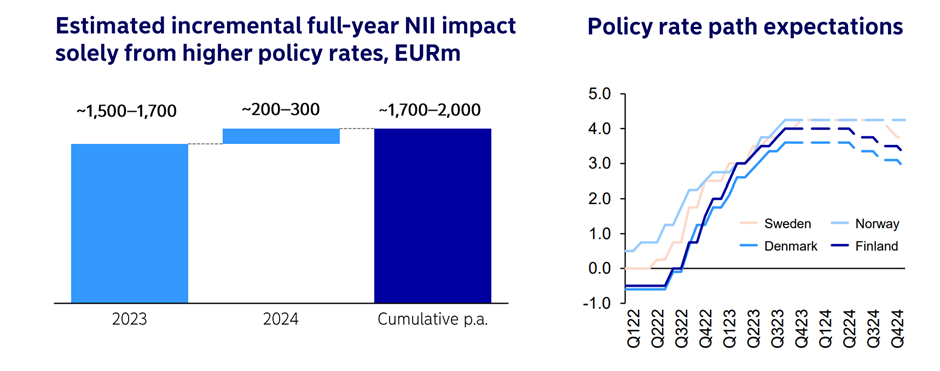

The more interesting update, in my view, was Nordea’s sensitivity guidance showing an expected rate-driven boost to net interest income at +EUR1.5bn to EUR1.7bn (up from +EUR1.2bn to EUR1.6bn prior). Also notable is that management has rolled this benefit into 2024, albeit by a smaller EUR200m - EUR300m (up from EUR100m to EUR200m prior).

{kind=link}

While positive at first blush, the issue here is that this update depends on interest rates remaining ‘higher for longer’ – a view that seems outdated in light of the Fed’s recent pivot (three cuts in the 2024 dot plot vs six implied by markets currently) and its implications for reaction function s across the Nordics and European Union. In the likely event we see the latter central banks follow up with more cuts this year, expect more downside than upside for Nordea’s net interest income path.

{kind=link}

Monthly Banking Data Signals Growing Margin Pressure

Relative to the more optimistic 2024 net interest income update provided in Q3, the monthly system data out of Sweden paints a more challenging outlook for Nordea. For context, the bank had already posted sequential deposit and loan contractions last quarter – a result of its exposure to a deteriorating corporate segment.

Monthly reports show more of the same, with the system as a whole seeing deposit outflows, particularly on the household side. Corporate deposits are still roughly down high-single-digits % YoY. Perhaps the more worrying signal was corporate loans, a segment that Nordea over indexes to, posting another month-on-month decline.

{kind=link}

Given Nordea is going up against a relatively high guidance bar, the poor quarter-to-date data doesn’t bode well for Q4 and beyond. And with limited rate upside now that the Riksbank is likely done with its hiking cycle, there isn’t a lot of room to protect net interest margins either. So, while Nordea outperformed on strong corporate loan demand earlier this year, a reversal in 2024 would expose the bank to a more challenging volume outlook than peers. Until guidance numbers are rebased in line with forward curves in Q4 (slightly lower rates across the Nordics and Eurozone), I would be cautious about underwriting earnings resilience.

Attractive Capital Returns but Mind the Sustainability

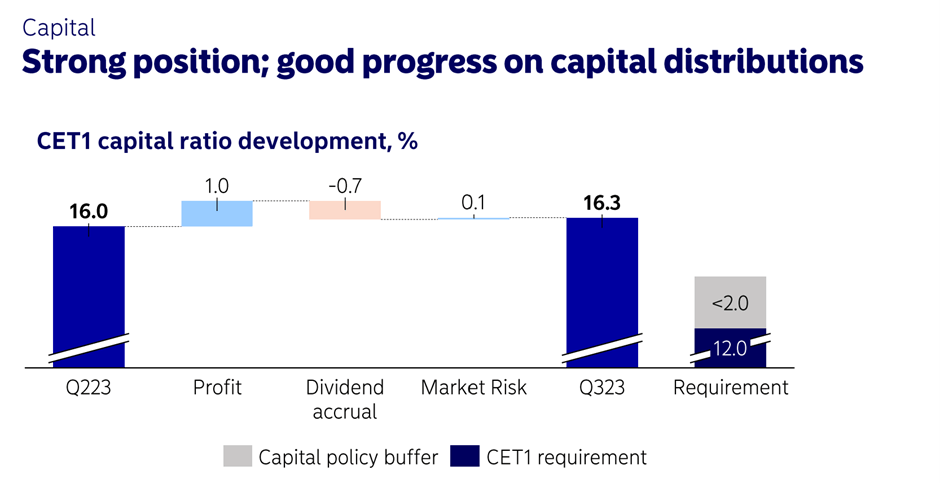

With a tougher outlook on the horizon, Nordea’s robust capital position stands out. Its tier-1 equity buffer stands well above current regulatory requirements, and even after a projected increase later next year, the bank is more than adequately capitalized. Thus, the capital return, comprising a hefty high-single-digit % dividend and a further EUR1bn of buybacks (currently in progress), seems well-supported.

{kind=link}

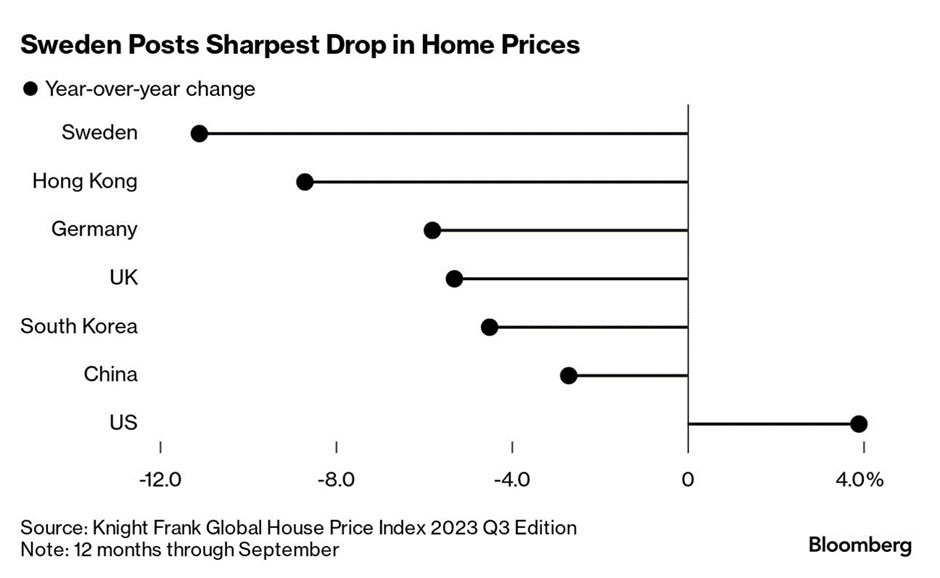

From here, though, I see more downside than upside to overall yields, which, per Nordea’s last mid-term strategy update , hinges on profitable growth. Even if management pulls off its increased operational efficiency targets, lower net interest income leaves less room to return capital to shareholders in the strategy period. Plus, we’ve yet to see the full impact of loan losses hit financials, particularly with housing markets starting to roll over in Sweden. Either way, expect next month’s full-year result announcement to come with a much-needed reset, in turn posing downside risk to consensus expectations.

{kind=link}

Cautious Ahead of Full-Year Results

Nordea stock may have rallied into year-end but the Nordic banking environment isn’t getting any easier from here. Rate cuts are on the horizon, and if the monthly Swedish banking system updates are anything to go by, the sector could be in for some headwinds on both the lending and deposit sides. Having benefited the most from corporate lending this year, Nordea is particularly exposed as the tailwind reverses. All in all, the Q3 guidance upgrade seems a tad optimistic heading, and ahead of full-year results next month, I would be cautious about the potential downside. In the meantime, the stock does offer attractive returns of capital (high-single-digits % dividend yield; low-teens including buybacks), though balanced against the prospect of lower returns on capital, I don’t see compelling value here.

For further details see:

Nordea: Cautious Ahead Of Full-Year Results