NRDBY - Nordea: Not Enough To Like About It Here

2023-06-06 04:05:14 ET

Summary

- I have a good understanding of when a Scandinavian financial institution is at a good valuation, and I've written about the company a few times in the past.

- Nordea can be considered attractive at the right price, with plenty to like about the company if you can buy it at a double-digit valuation.

- My choices in the sector remain Handelsbanken and Swedbank, which represent the majority of my investments in the Scandinavian financial sector.

Dear readers/followers,

I would say that generally speaking, I have a good grasp of when a Scandinavian financial institution, such as a bank, is at a good valuation. When it's buyable, but moreover, when it is not. That's why in the last article, I actually gave you a "HOLD" rating for Nordea ( OTCPK:NRDBY ). I hold a small stake in the bank - my choices in the sector are Handelsbanken ( OTCPK:SVNLF ) and Swedbank ( OTCPK:SWDBF ), which represent the lion's share of my investments in this sector in Scandinavia.

But Nordea can nonetheless be considered to be attractive at the right price. I gave you an overview of the bank last time I wrote about the company, and the stance I held has held true if we look at the RoR until about today.

Seeking Alpha Nordea (Seeking Alpha)

So, let's see based on these results, why Nordea is attractive or not at this particular time.

Nordea - Plenty to like, even if we're not at bottom-level valuations for the company

So, Nordea is a good bank - Nordic as opposed to some of the other Swedish-centric banks I follow and write about. Swedbank and Handelsbanken are way more Swedish-focused, while Nordea has some focus on Finland as well, with its headquarters actually in Finland now as well. 11 million customers, and 1,400 offices around the world means that it has better representation across the various geographies than others Swedish banks does. With its shareholding no longer tied to Sampo ( OTCPK:SAXPY ) as well, ownership is focused mostly on SEB funds and other institutional owners. Not necessarily a drawback either.

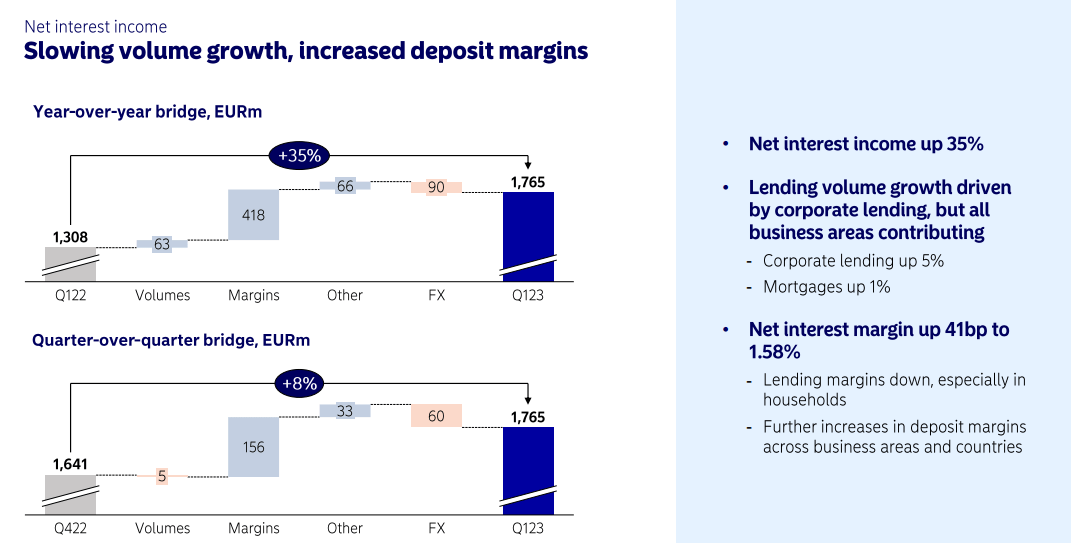

First-quarter results were good, as they were with most banks across Scandinavia. Net interest income was up strongly, offsetting any drop-off in fee/commission-based income, with a YoY operating profit improvement of close to 35%, meaning almost €1.5B per quarter.

On the lending side, corporate lending was up the most at 5%, mortgages up 1%, and deposits up 5%. Even AUM was up 1% sequentially, delivering a very positive picture overall.

The bank saw an improved cost-to-income ratio at 43%, a very strong credit quality. Loan losses weren't as low as Handelsbanken, amounting to around €20M for the quarter, but well below the judgment buffer of nearly €600M that the bank has prepared for provisioning.

RoE was at 17.1%, with EPS up almost 50% YoY - superb results. The company improved the dividend to €0.8/share, coupling this with a new buyback program, and a CET1-ratio of 15.7%. This is lower compared to most of its Scandinavian peers, but still significantly above the regulatory requirements as they currently stand.

As with most mature banks, which is the case in Scandinavia, because this is a very mature market run essentially by 4-5 incumbent banks, growth is slow. Volume growth at this time is even slower, so any improvements here are coming from margins - not from volume.

{kind=link}

When commissions and fee-based incomes are down, the company can instead focus on incomes like card, and interest-based income - and these are up significantly. High customer activity resulted in a significant YoY increase in net fair value results. As with most banks, KYC/AML investments continue, with a 4% YoY increase in spending, mostly from costs, IT/risk, and with lower regulatory investments and positive FX.

Nordea, again like its peers, is doubling down on quality and reports a very strong credit quality. Impaired loans, known as stage 3 loans, are less than 1%.

Nordea IR (Nordea IR)

Because there are no credit issues, because income is up, and because the bank is seeing no direct weakness, the company has deployed more toward buybacks. It continues to operate at a very strong capital position, although, on a YoY basis, dividend accruals, buybacks, IFRS charges, and other things have dragged this down from 16.4% to 15.7%, which means that it goes in the other direction compared to most banks.

Personal banking income increases hail from interest income, lending generally, and deposit incomes. Total income was up 22%. Margin pressures on mortgages continue to be significant, with strong competition for mortgages on a broad basis. Business banking also saw similar volume increases, and C/I ratios are now less than 39% for the bank in the business segment - absolutely superb.

Nordea does have an asset management arm as well, though its nowhere as significant as in larger, more global banks. Still, that asset management arm did deliver good results, by which I mean a 19% YoY improvement due to interest incomes from deposit margins - not necessarily performance. Lending in private banking was up as well, as were deposits in the segment. The bank, across the board, manages C/I of less than 40% in every segment except in personal banking, which is at 44%.

Nordea has long had a target of a 13% or above RoE and a company-wide C/I ratio of 45-47%. As you can see, Nordea is currently outperforming to this set of targets, a definite positive here. Both Nordea customers and Nordea investors have the right, with the last quarter, to be pleased with their performance.

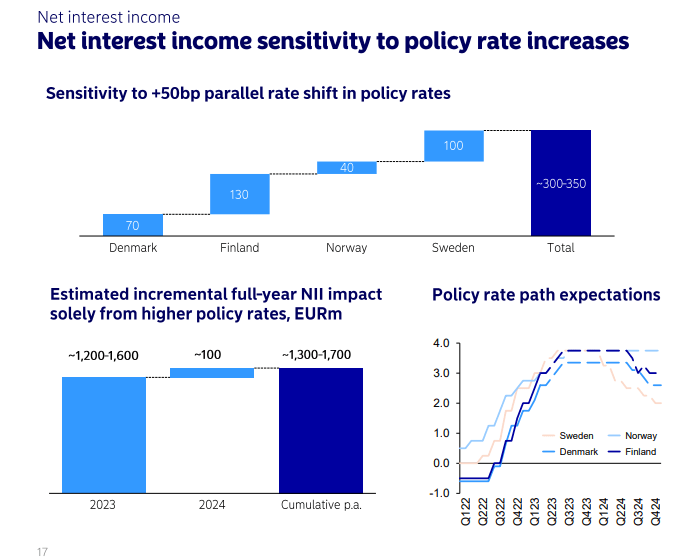

The company remains somewhat heavily exposed to interest rate increases. A 50 bps increase in the interest rate across its geographies results in the following parallel shift.

{kind=link}

You can see the policy path expectations above. This comes to an NII impact from policy increases to drive €1.2-€1.6B for the year, with the actual pass-through varying between both account types and countries. As NII increases, wholesale funding costs and hedging costs will obviously be increasing as a net result, but in the end, that's weighed up by volumes and asset pricing trends.

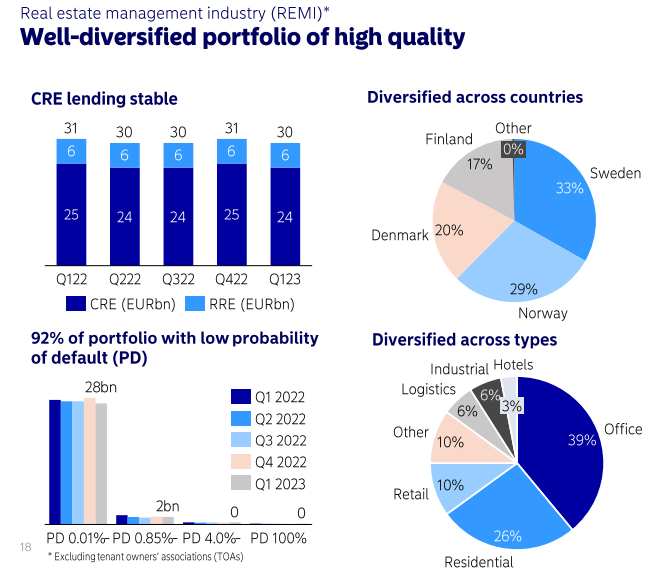

Nordea also has a real estate management industry segment, or REMI, where we find CRE lending, and the mix looks like this currently.

{kind=link}

It's a very good mix, and even with RE risk, 92% of the exposure is towards low-risk customers in 1Q23. Only 2% of the actual lending portfolio is towards what the bank would consider higher-risk, with much of the portfolio consisting of high-quality central and modern resi and office properties. Underwriting standards for Nordea are focused on cash flows and existing customers - doors to new lending are not closed, but requirements here are very strict. Vacancy rates are higher than in some office REITs in the US, but they're still not bad, at a 93.5% vacancy rate, with an average interest-coverage ratio of 5.8x. LTV vary, coming to about 53% as of 1Q23, lower in Sweden at below 50%, but higher in Denmark at 56%. Not something I consider massively worrying here either.

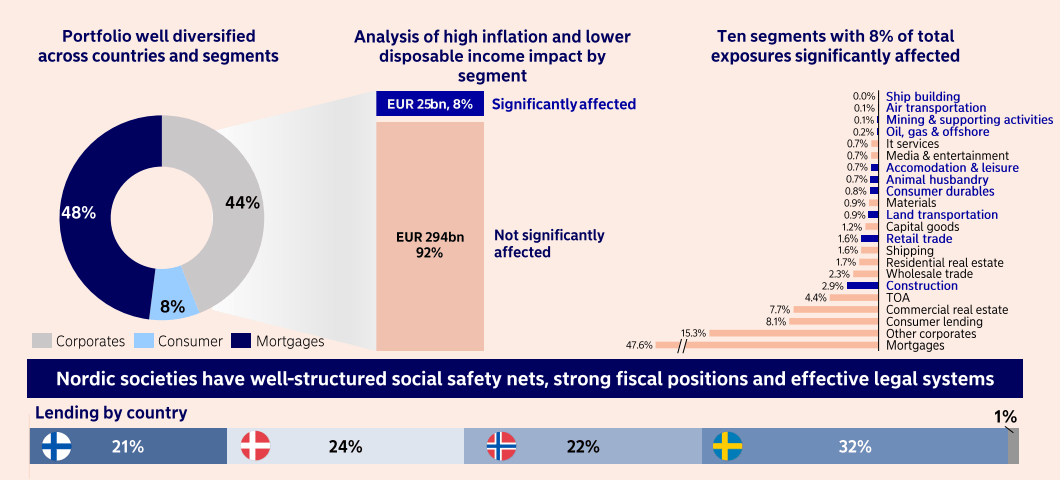

Investing in Nordic real estate is never a bad idea, as I see it, nor the banks that run it. The characteristics are chronic underbuilding, which puts a high floor on the value of virtually anything that's out there.

{kind=link}

That's why, in addition to investing in stocks in the Nordics that cover RE, I also invest in things like actual property, if I can find a good combination of cash flow, price, and returns as well as an appealing geography.

However, all of these are just smaller points. The bigger point I'm making is that Nordea did very well and deserves your attention at this particular time.

Here's the valuation takeaway from the company at this particular time.

Nordea - The valuation

I've previously said that Nordea has a bit of a character of underperformance. A long-term investment in Nordea has not been a good idea for much of the past 10-20 years. My target for this bank has, for a long time, been a conservative 80-90 PT range, with my latest target at 85 SEK/share for the native, by which I mean Swedish (Finnish can be said to be native here).

For the past 18 or so years, the company has averaged 2.6% CAGR - and I don't see that improving meaningfully in the near future. The company currently trades at 110 SEK. The covered calls of which I spoke in my last article which I wrote against my position have delivered ITM at 120 SEK strike. Guess what happened after I sold those?

The company dropped back down. As I wrote in that article, I wanted them to expire ITM - so this was a great little addition to my income, at an effective share price of almost 126, less than 2 SEK below the high it reached before dropping.

I could increase my PT for Nordea here, but I'm not going to - not meaningfully. I could see my way to increase, based on excellent results, the PT to around 90 SEK/share, but this would still see the company at a high valuation. Most analysts consider the company fairly valued at this particular time, at least of those I follow. S&P Global have 15 analysts following the company coming in at a range of 95 to 135 SEK/share, averaging around 118 SEK/share. I view that as being too high for what the bank offers. At that price, the company yields about 6% in dividends. Handelsbanken is better, higher yield, and is also significantly cheaper, explains why I am buying Handelsbanken rather than Nordea at this time.

Nordea typically commands a 10-year average LTM price to BV/share of 1.18x-1.2x - no more than that. The latest is 1.2x - with a record high of 1.7x and a record low of 0.56x. This shows you about where you want to get in with Nordea, and that certainly is not today - it would be more interesting if it dipped below that 1.15x, and better even at a share price in the double digits for the SEK ticker.

All banks here are currently outperforming. This is an environment that is made for banks to outperform, with strong interest rates and a good property market, despite the risks and volatility we currently see, with one of the major players currently in trouble.

In the end, Nordea remains a "HOLD" here. I'm adding Handelsbanken, but I'm not adding Nordea here, and I would only add Nordea if it dropped below 90 SEK/share.

Thesis

- Nordea is a sector-leading sort of banking play in the Nordic region, with a presence across one of the most attractive banking regions in the world due to its incumbent status. The bank is well-capitalized and has an almost-un dislodgeable position in the market. It has an attractive yield and good growth prospects.

- However, it's all about valuation - and I don't see a good valuation here. in terms of Book value, earnings, and other relevant multiples, Nordea shows all the signs of being slightly above its standard valuation trend, calling for me to give it a "HOLD".

- That is what I am doing. PT is 90 SEK/share, and I'm at a "HOLD" here, as of June of 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

Nordea: Not Enough To Like About It Here