NAT - Nordic American Tankers Limited: Sailing Into A Storm

2023-08-04 10:43:54 ET

Summary

- Nordic American Tankers Limited (NAT) faces challenges due to its aging fleet, limited cash reserves, and potential difficulties in managing and repaying its debt.

- The company's high Debt to Free Cash Flow ratio and premium valuation suggest a disconnect between market valuation and underlying fundamentals.

- Shorting NAT may serve as a hedge against long positions in better-positioned companies in the industry due to its potential underperformance.

Nordic American Tankers Limited ( NAT ) has been navigating the waters of the oil tanker market for many years. With a strong track record and a wealth of experience, this industry titan has weathered many a storm while consistently maintaining a dividend. However, several indicators suggest that the company's journey may become more challenging relative to it's better capitalized peers and we are placing a Sell rating on the stock.

{kind=link}

Author and NAT

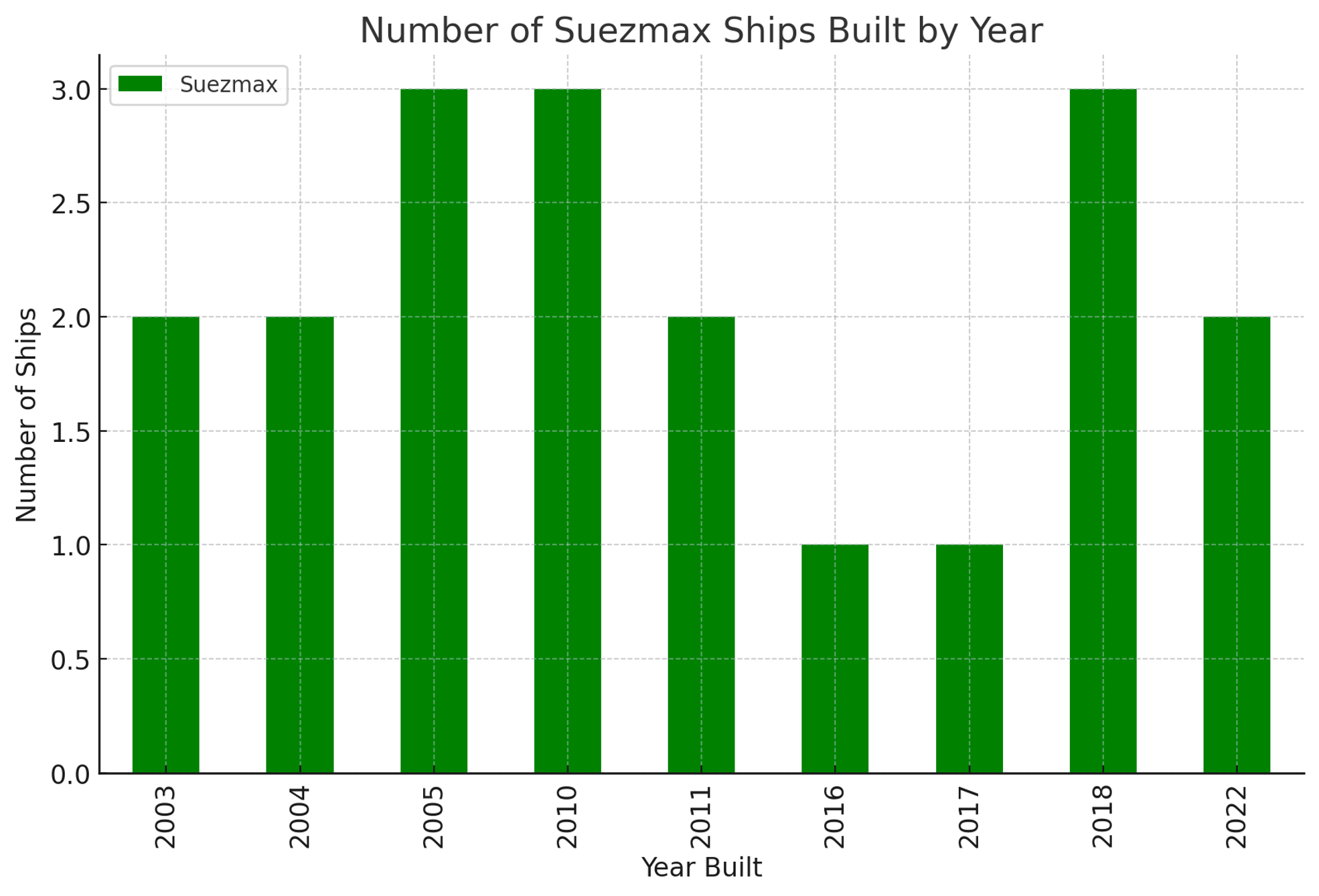

Aging Fleet

Despite the forecast for substantial revenue growth and the broader market trends signaling continuous growth, NAT faces significant headwinds. A significant concern is the ageing fleet, with 36% of their vessels nearing the end of their operational lifespan. While their DWT (dead-weight tonnage) weighted average ship was built in Feb. 2011, they do have seven "Sunset Fleet" vessels, built between 2003 and 2005. Given the typical tanker lifespan of 20-30 years, these ships are likely to retire or be sold within the next 3-5 years, if not sooner. This prediction is substantiated by the company's recent sale of a suezmax for $21 million in September of last year .

NAT prides itself on its strategy of maintaining and expanding a homogeneous and top-quality fleet. However, the imminent retirement of a significant portion of their fleet, coupled with the company's limited cash reserves ($56 million) and cash from operations ($84 million TTM), paints a concerning picture. Further complicating matters is the continuous rise in overall tanker prices despite higher interest rates. NAT is limited in their ability to expand and maintain the size of their current fleet without substantial changes. Given these financial constraints and market conditions, NAT's fleet expansion may hit rough seas.

Another area of concern is NAT's dividend payments, which stand at a hefty $52.1 million. While shareholders appreciate the company's focus on providing dividends, the company may need to consider a reduction in its payout ratio and dividends to stay afloat. The sale of older ships in exchange for newer (and fewer) tankers could be on the horizon, a move that could further strain their finances.

Free Cash Flow

Taking a look at FCF over the last few quarters can paint a picture of the ability for Nordic American to increase their Free Cash Flow through their ability to control costs and Capital expenditures. I'm calculating FCF in the manner below:

Free Cash Flow ((FCF))=Operating Cash Flow?Capital Expenditures

| Period Ending | Cash from Operations | Capital Expenditures | Free Cash Flow |

|---|---|---|---|

| Mar 2023 | |||

| $51.1 | |||

| $-0.2 | |||

| $50.9 | |||

| Dec 2022 | |||

| $40.5 | |||

| $-5.2 | |||

| $35.3 | |||

| Sep 2022 | |||

| $-2.4 | |||

| $-0.4 | |||

| $-2.8 | |||

| Jun 2022 | |||

| $-5.3 | |||

| $-72.3 | |||

| $-77.6 |

(As a note all of the above values are in millions)

The Cash Flow from Operations for Q1 2023 was $51.1 million and for Q4 2022 was $24.1 million, with relatively low capital expenditures of $0.217 million and $5.116 million respectively. This resulted in a significant positive FCF of $75 million over the past two quarters.

However, it's important to consider the larger capital expenditures in Q3 and Q2 2022. These large purchases of two new ships resulted in negative FCFs of $-74.7 million and $-22.8 million for these quarters. Bringing FCF over those four quarters to $5.8 million dollars.

While the recent positive FCF is encouraging, it's critical to contextualize these figures within the broader framework of NAT's business model. As a shipping company operating in a capital-intensive industry, NAT must periodically invest heavily in new vessels to maintain and grow its fleet. These investments, while resulting in short-term cash outflows, are designed to increase the company's capacity and, consequently, its future cash inflows.

It's important to note that a significant portion of NAT's fleet comprises older vessels that will eventually need to be replaced over the next few years. As such, these necessary investments will continue to impact the company's FCF in the future and we believe this places them in a weaker position relative to those with newer fleets such as STNG .

Current Valuation

{kind=link}

Seeking Alpha

Seeking Alpha

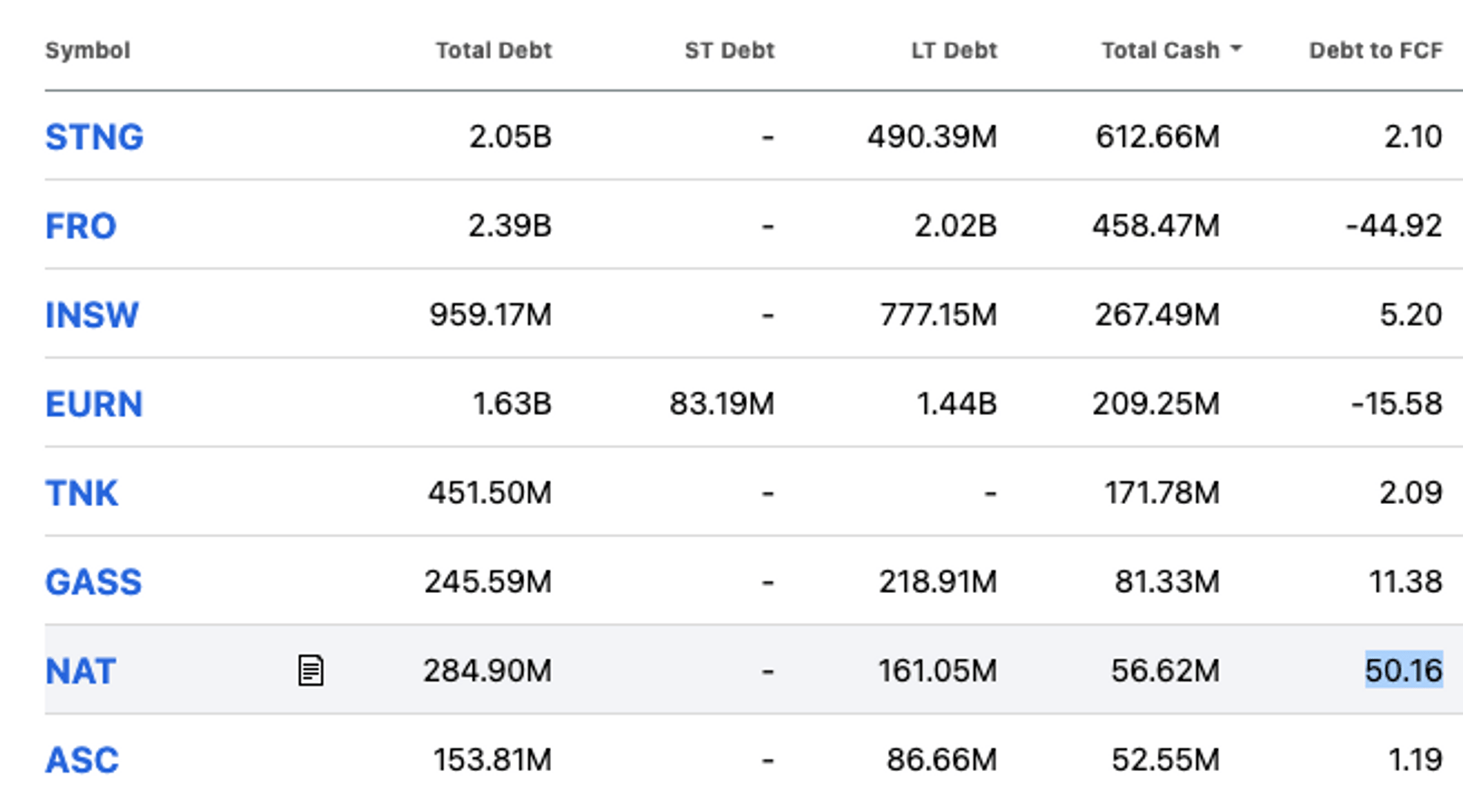

The financial health of a company is often gauged by examining its debt levels relative to its free cash flow, a measure of how much cash a company generates after accounting for capital expenditures. NAT's Debt to TTM FCF ratio stands at a staggering 50.16x. While there is a caveat to be made here has over the TTM NAT does have a large Capex expense and if they do not make any further large Capital purchases this ratio will drop to dramatically. This high ratio indicates a heavy debt burden and suggests potential difficulties in managing and repaying its debt if they maintain large Capex purchases.

In contrast, International Seaways, Inc. ( INSW ), another player in the oil tanker industry, has a significantly lower Debt to FCF ratio of 5.2, implying a far more manageable debt load. Furthermore, INSW operates a slightly newer and much larger fleet, positioning it better for future growth and success in the industry. The stark difference between the financial health of NAT and INSW highlights the challenges NAT may face in the coming years.

{kind=link}

Seeking Alpha

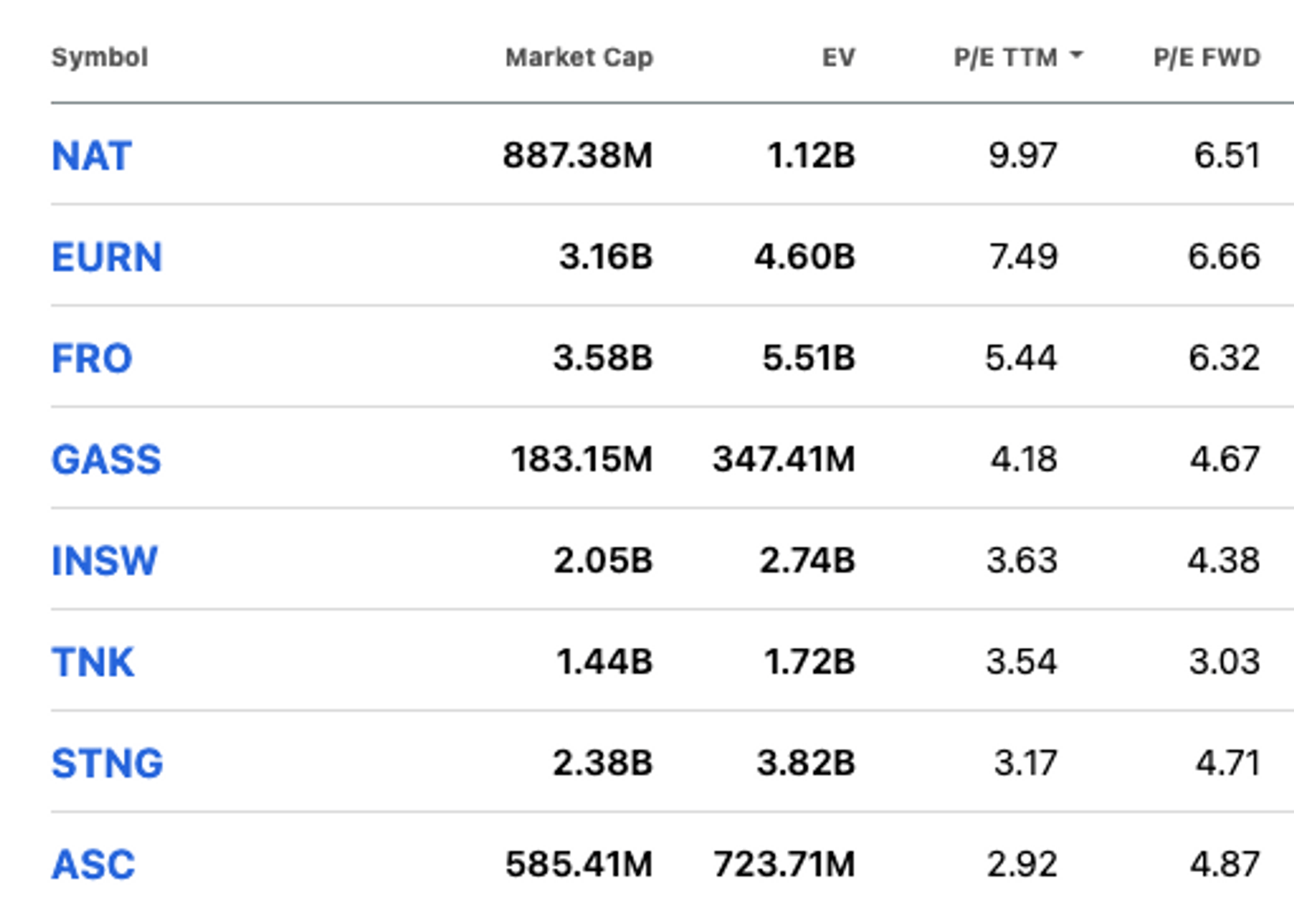

NAT's valuation also gives cause for concern. Despite the looming challenges, the market appears to be valuing NAT at a premium. Its forward Price-to-Earnings (P/E) ratio is 6.51, which is higher than the industry average of around 5. The P/E ratio is a valuation ratio and is used to compare a company's current share price to its earnings per share ((EPS)). A high P/E ratio could indicate that a company's stock is over-valued, or else that investors are expecting high growth rates in the future. The fact that NAT's P/E ratio is higher than the industry average, despite its aging fleet and high Debt to FCF ratio, may suggest a disconnect between market valuation and the underlying fundamentals.

Despite the challenges facing NAT, the overall gas tanker space shows strong potential due to a global undersupply and limited growth rate of the tanker fleet. However, other players in the industry may be better equipped to capitalize on these opportunities. NAT's high Debt to Free Cash Flow ratio and its premium valuation, coupled with its aging fleet and financial constraints, make it a less attractive option compared to its competitors which puts it in a unique position to be used in a short-leg for a spread trade.

Despite the optimistic outlook for the industry, a bearish view on NAT seems warranted. Its focus on providing dividends to shareholders could potentially be driving a disconnect in its stock price relative to others in the space. Thus, a short position on NAT could serve as a hedge against long positions in other, better-positioned companies in the industry.

{kind=link}

Shares Issued vs Share Price (Author)

Risks

Shorting Nordic American Tankers Limited ( NAT ), like any other stock, carries inherent risks that investors must thoroughly understand before proceeding with such a move. A central risk in shorting NAT arises from the potential supply constraints in the oil tanker market due to slowing fleet growth and a globally low supply of both oil and ships. This scenario could lead to a tightening of tanker capacity, and in such a supply-constrained market, freight rates might see a substantial hike. This could, in turn, boost revenues for NAT, potentially leading to better-than-expected financial performance. As global oil demand recovers in the post-pandemic world, these freight rates could surge further or maintain their current elevated levels, driving NAT's stock price up.

Another significant factor to consider is that NAT pays substantial dividends, and when you short a stock that pays a high dividend, you are responsible for paying that dividend to the lender from whom you borrowed the shares. These dividend payments could accumulate to a substantial amount over time, decreasing potential profits from the short sale, or even leading to losses if the stock price doesn't decline as anticipated. It's crucial to stay vigilant, monitor market trends, and be prepared to adapt as necessary.

In order to reduce risks associated with shorting a high dividend paying stock such as NAT investors can utilize a variety of strategies. One common approach is to use options contracts to limit potential losses. Put options give investors the right to sell a stock at a certain price before a certain date, effectively setting a limit on the potential loss from a short position and reducing the need to pay the lender dividends. If the stock price rises above this level, the investor can simply let the option expire worthless and close out the short position at a manageable loss.

Another strategy is to maintain a diverse portfolio to mitigate the risk associated with any single investment. If an investor shorts NAT while also holding long positions in other stocks or asset classes, losses from the NAT short position could potentially be offset by gains elsewhere in the portfolio. This diversification can help to smooth out returns and reduce the overall risk level of the portfolio.

Conclusion

In conclusion, while NAT has traditionally been a mainstay in the oil tanker industry, its aging fleet, high Debt to FCF ratio, and premium valuation relative to its peers suggest that the company could face significant headwinds. As NAT charts its course for the future, investors will need to closely monitor these factors. The industry's currents are ever-changing, and only the most adaptable companies will be able to successfully navigate these waters I believe NAT is a sell relative to the rest of the oil ship fleets and is a clear under performer at current prices despite their high dividend yield.

For further details see:

Nordic American Tankers Limited: Sailing Into A Storm