NAT - Nordic American Tankers: Remain Constructive On Shares

Summary

- NAT owns a fleet of 19 Suezmax tankers.

- NAT's fleet continues to benefit from Russian oil disruptions and low global fleet growth, which has allowed tanker rates to stay 'higher for longer'.

- NAT is scheduled to pay $0.15 / share in dividends for Q4/2022. With strong profitability expected in 2023, NAT could continue to pay elevated dividends for many quarters.

I recently wrote a positive update on Teekay Tankers Ltd. ( TNK ), as Russian oil disruptions have caused tanker rates to stay elevated while full shipyards mean the situation can extend for years. The same fundamental drivers for Teekay also drive Nordic American Tankers ( NAT ), as they both primarily operate in the spot tanker market.

If tanker rates can maintain at Q4 levels for the rest of 2023, I believe we could see $0.79 / share in EPS for NAT, the best performance in almost a decade. I remain constructive on shares trading at less than 6x P/E.

Brief Overview Of Nordic American

Nordic American Tankers own a fleet of 19 fairly interchangeable Suezmax oil tankers that are mostly chartered in the spot market. NAT's business model is simple: it tries to keep operating costs low, with 2022 vessel operating expenses ~$8k / day. When tanker markets tighten, NAT can earn large windfall profits.

Great End To 2022

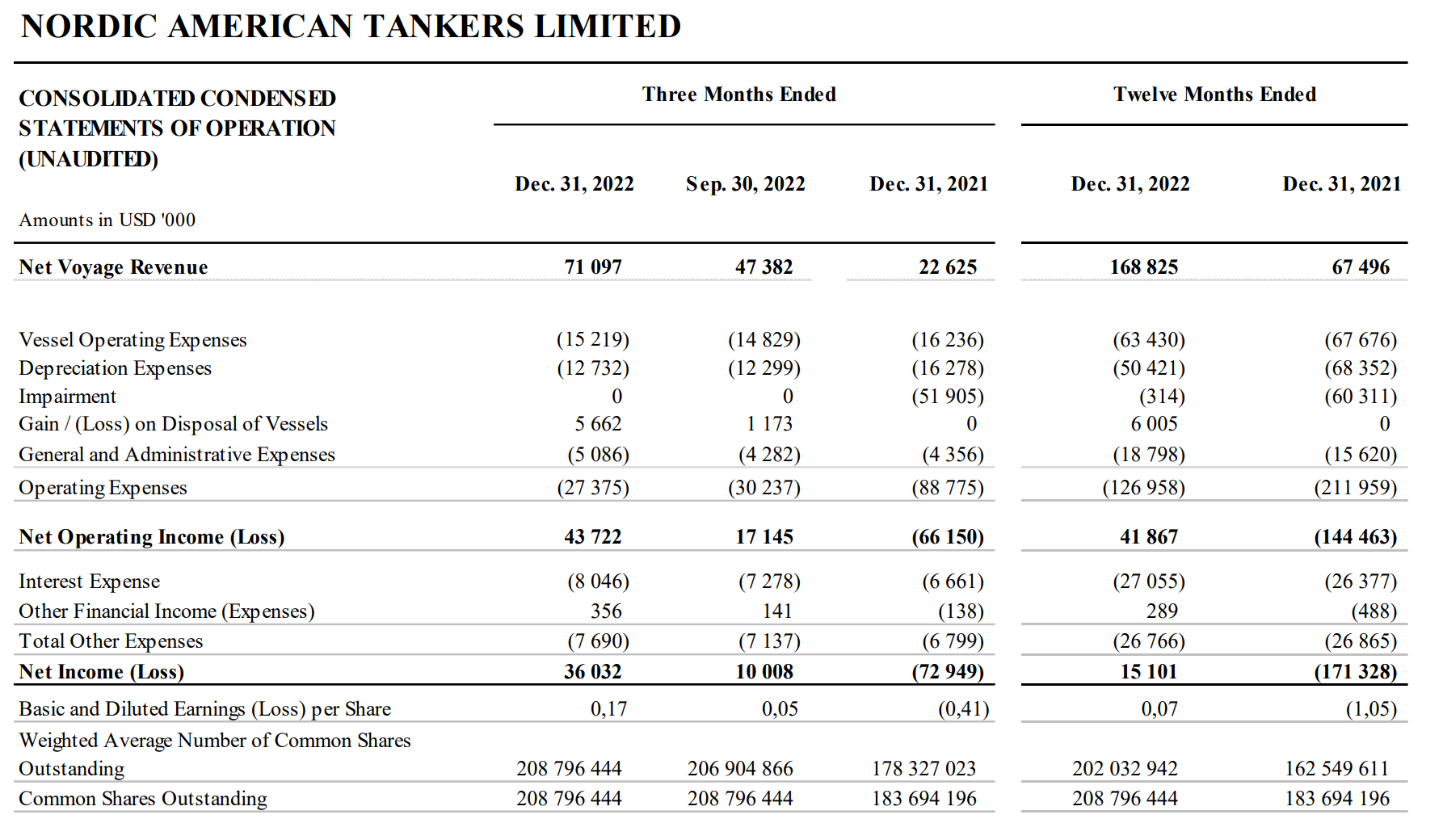

On February 27th, 2023, Nordic American reported their fiscal fourth quarter results, showing a sharp improvement in financial performance. For the 3 months ended December 31, 2022, NAT recorded revenues of $71.1 million (+215% YoY) and diluted EPS of $0.17 (vs. $0.41 loss in Q4/21) (Figure 1).

Figure 1 - NAT Q4/2022 financial summary (NAT Q4/2022 press release)

{kind=link}

Q4 results were a large improvement against Q3, as NAT saw time charter equivalent ("TCE") rates of $57k / day for spot vessels and $49k / day for the fleet versus $28k / day in Q3. In fact, Q4 results for NAT actually missed analyst estimates , which called for $83.5 million in revenue and $0.21 in earnings.

This miss was mostly because the bulk of Nordic American's 2022 drydockings (maintenance work on vessels) occurred in the fourth quarter and negatively affected revenues. With voyage revenues of $71.1 million and total TCE (including chartered vessels) of $49k / day, I estimate NAT's fleet only operated ~85% of the available days in the fourth quarter versus normal operating rates of ~90-95%.

Tanker Rates Remain High Into 2023

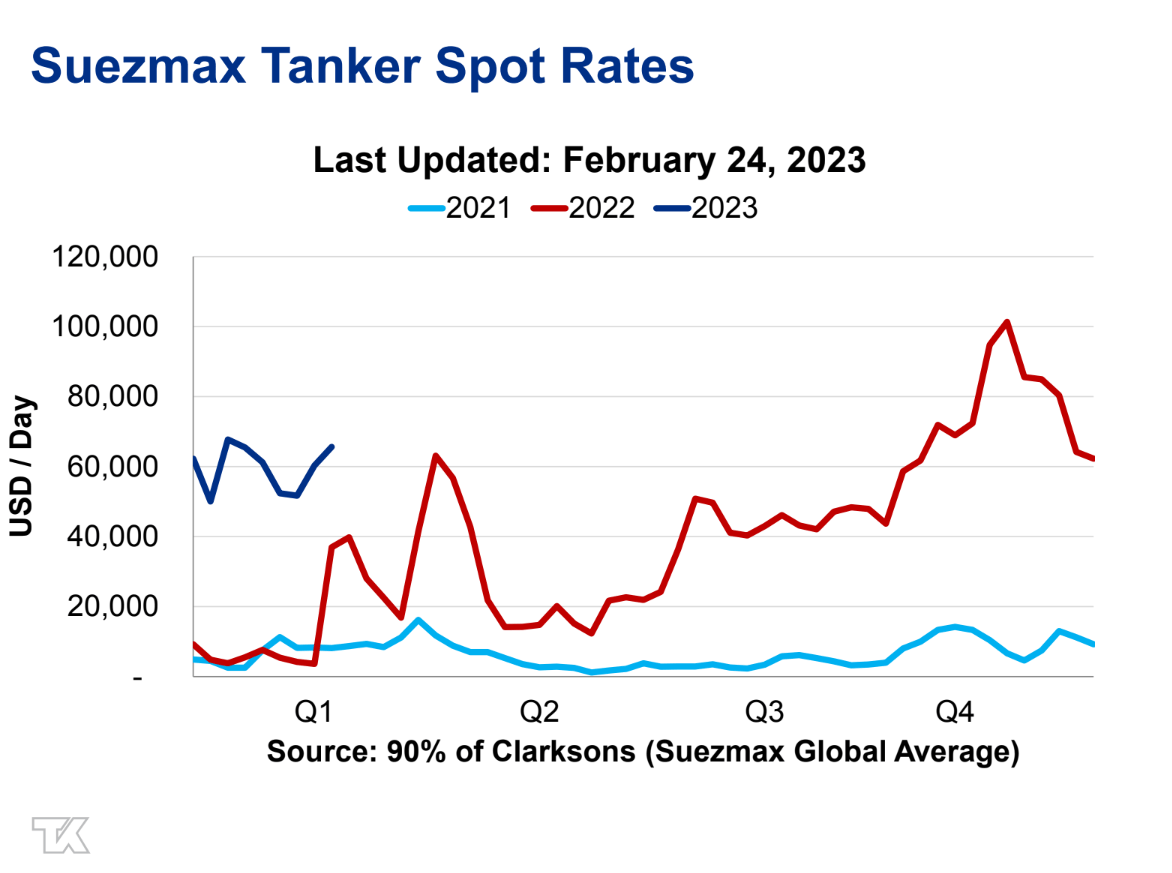

Revisiting my bullish thesis on NAT, it appears tanker rates are set to stay higher for longer, as I laid out in my prior article . While NAT's Q4 spot rates of $57k were fantastic, the company is seeing even strong rates so far in 2023, with 72% of spot voyages having been booked at an average TCE of $61k / day.

This is consistent with the trend seen from the market data that Teekay Tankers graciously provides for free on a weekly basis (Figure 2).

Figure 2 - Suezmax tanker rates remain elevated (Teekay Market Insights)

{kind=link}

Financial Forecast Robust For 2023

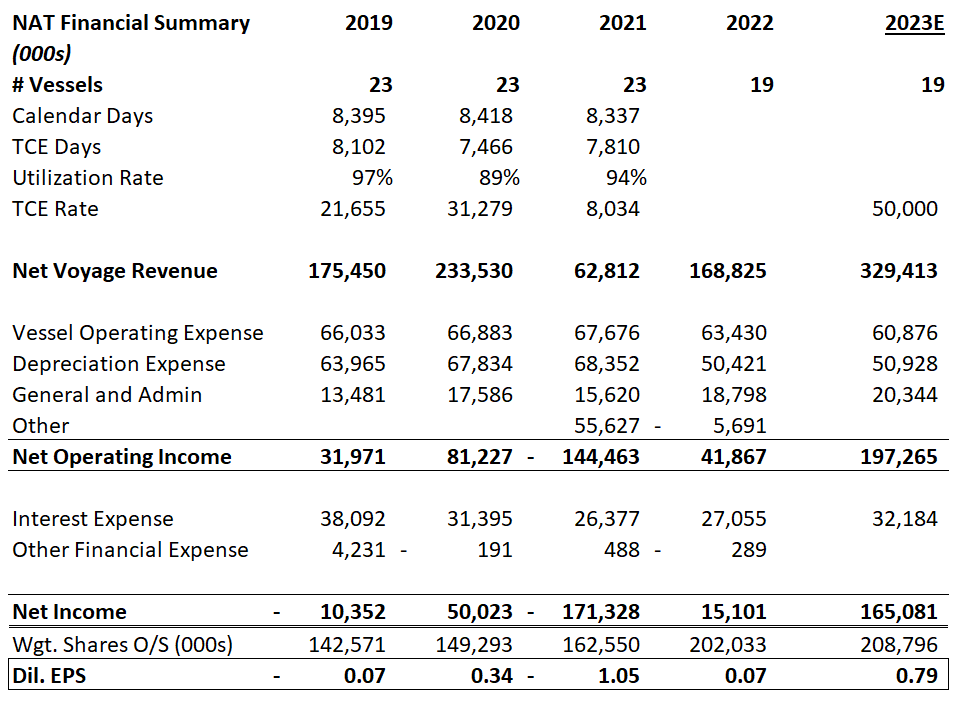

In fact, if we model $50k / day TCE for NAT's fleet, similar to Q4/2022 levels, we can see NAT generating $329 million in net voyage revenues and $165 million in net income for 2023, or $0.79 / share in EPS (Figure 3).

{kind=link}

This level of profitability will be the highest in years and would surpass the windfall profits that NAT earned in 2020 due to oil falling into negative territory.

Trading at only $4.43 / share as of February 28, NAT appears to be valued at sub 6x P/E on my 2023 earnings estimates.

Are Tanker Rates Sustainable?

The key question for investors is whether the current level of windfall profits is sustainable. In the past, high tanker rates incentivized shipowners to place lots of newbuild orders, which would swamp the market all at once and crash the tanker rate. However, the current tanker cycle appears to be fundamentally different. According to Nordic American, there were only 14 vessels (2% of worldwide fleet of 573 vessels) in the order books, with 6 scheduled for delivery in 2023 and 5 deliveries in 2024.

Global fleet growth is expected to be muted for the next 2-3 years because shipyards are currently full building containerships and LNG carriers that were ordered in response to extraordinary rates in those markets.

Therefore, with the Russian oil ban potentially lasting for many years and tight supply growth, we could see a multi-year period of elevated tanker rates.

Insiders Continue To Buy

It is no surprise then that insiders continue to buy shares of Nordic American, seemingly at every opportunity they can. On February 28th, 2023, NAT reported that board member Alexander Hansson bought an additional 75,000 shares, bringing his total to 2.08 million shares.

A few months ago, Chairman and CEO Herbjorn Hansson bought 100,000 shares. Since the beginning of 2022, the father and son duo have bought close to 1 million shares on the open markets. This is about as strong a vote of confidence as one can see in the investment business.

Rewarding Investors With Dividend Increase

Concurrent with the fourth quarter report, NAT also announced a $0.15 / share quarterly dividend to be paid to investors as of March 14. This is an increase from $0.05 / share paid last quarter.

As a reminder, during windfall years like 2020, NAT rewards investors with very high dividend payments (Figure 4).

Figure 4 - NAT reward investors with windfall dividends (NAT Q2/2020 report)

Risks To Bullish View

While 'higher for longer' tanker rates remain my base case, investors need to keep in mind that high inflation may push the global economy into recession in 2023, which could dent crude oil demand. If OPEC+ responds to weak oil demand with production cuts, then tanker demand and rates could be negatively affected.

There is also a risk that flush with cash, Nordic American management could do foolish things such as order multiple newbuilds at the top of the cycle. For now, NAT has been prudent and have used the high tanker rates to offload some of its older vessels, reducing its fleet to 19 ships from 23 ships last year. However, we have also seen NAT take delivery of 2 new vessels in 2022 and management have said publicly they plan to order more. When NAT decides to order more ships will be something investors need to watch for.

Investors need to remember that the tanker business is highly cyclical, so sometime in the next year or two, investors will need to sell when the future looks impossibly bright and NAT may be gushing cash. Fortunately, I think we still have a few good quarters left.

Conclusion

My 'higher for longer' tanker rate thesis continues to play out and NAT is a prime beneficiary as most of its vessels are chartered on the spot market. If tanker rates can maintain at Q4 levels for the rest of 2023, I believe we could see $0.79 / share in EPS for NAT. I remain constructive on shares trading at less than 6x P/E.

For further details see:

Nordic American Tankers: Remain Constructive On Shares