NDSN - Nordson Corporation: Still Not A Bargain

2023-03-17 14:03:12 ET

Summary

- Nordson Corporation reported mixed results with a slightly growing topline, but especially the guidance was a huge disappointment for market participants.

- The company completed the acquisition of CyberOptics for $380 million in November 2022.

- In my opinion, Nordson Corporation is fairly valued right now, although we can make the case for a higher intrinsic value and the stock trading for a 20% discount.

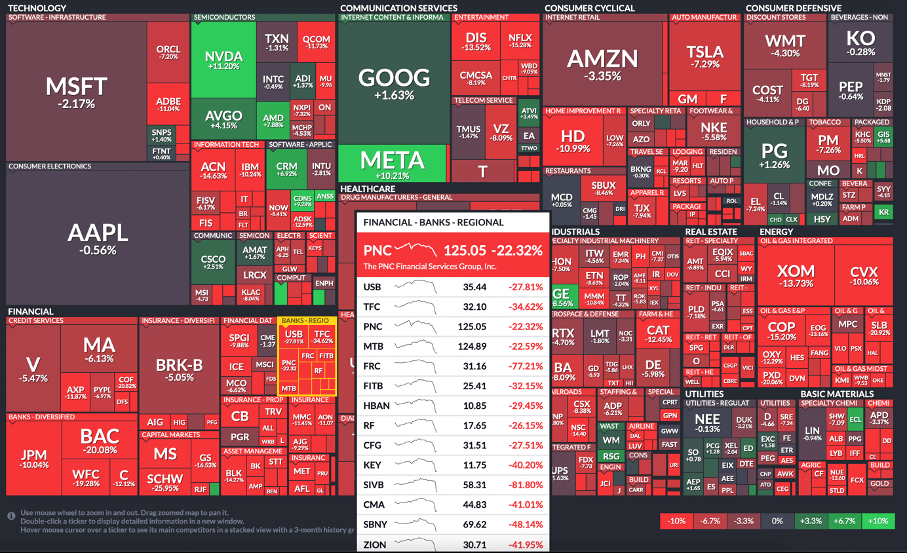

When looking at the performance in the last few weeks, the S&P 500 ( SPY ) did not perform great and lost about 7% since its temporary high in early February 2023. Not only did the banks perform horribly in the last few weeks, but the regional banks tanked, losing in some cases 50% or more of their previous market capitalization.

Performance S&P 500 companies last month (Finviz)

{kind=link}

Nordson Corporation ( NDSN ) also underperformed the S&P 500 in the last few weeks, as the stock lost about 18% of its value and is trading now about 24% below its previous all-time high. Nevertheless, I do not see Nordson Corporation as a bargain. It is actually trading for a similar price as 10 months earlier when my last article was published in May 2022. In the following article, I will take a closer look at Nordson to determine if and when it could be a good investment in the coming quarters.

Results

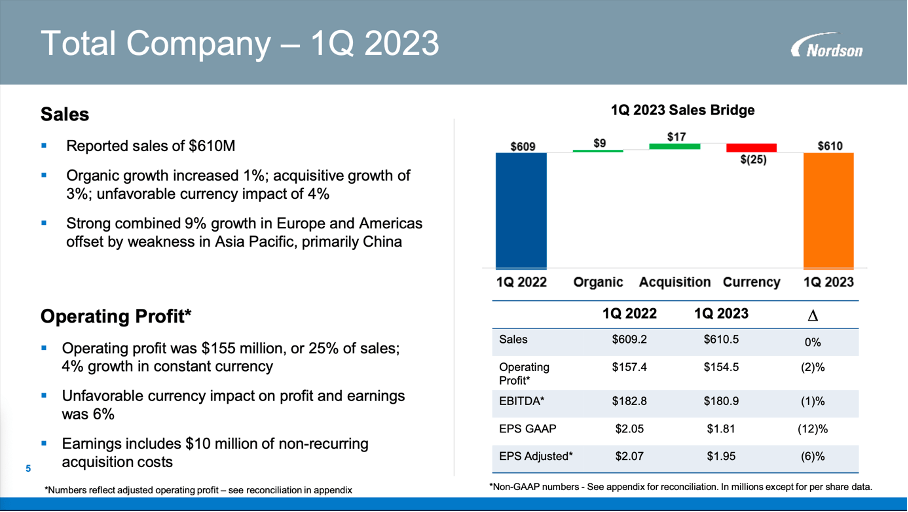

When looking at the last quarterly results Nordson Corporation released about four weeks ago, the market was deeply disappointed as the company missed on earnings per share as well as revenue. And the following trading day the stock declined from $246 to $211 - a 14% loss in a single trading day.

And at least when looking at the results, the decline seems like an overreaction, although results were not great. Sales could increase slightly from $609.2 million in Q1/22 to $610.5 million in Q1/23 - an increase of 0.2%. And while the top line could still increase, operating profit declined from $155.9 million in Q1/22 to $144.2 million in Q1/23 - a decrease of 7.5% year-over-year. And diluted earnings per share also declined 11.7% from $2.05 in the same quarter last year to $1.81 this quarter. And finally, adjusted earnings per share declined 5.8% year-over-year from $2.07 in Q1/22 to $1.95 in Q1/23.

Nordson Corporation Q1/23 Presentation

{kind=link}

When looking at the three different segments, two of them had to report declining sales. Industrial Precision Solutions declined from $324 million in Q1/22 to $312 million in Q1/23 and Medical and fluid solutions saw revenue decline from $159 million in the same quarter last year to $154 million this quarter. Only Advanced Technology Solutions was able to report increasing revenue from $126 million to $145 million - this stemmed mostly from acquisitions (we will get to that) while organic growth was 4.6%. Overall, organic sales growth was 1.4% while currency effects had a negative impact of 4.0% on the top line.

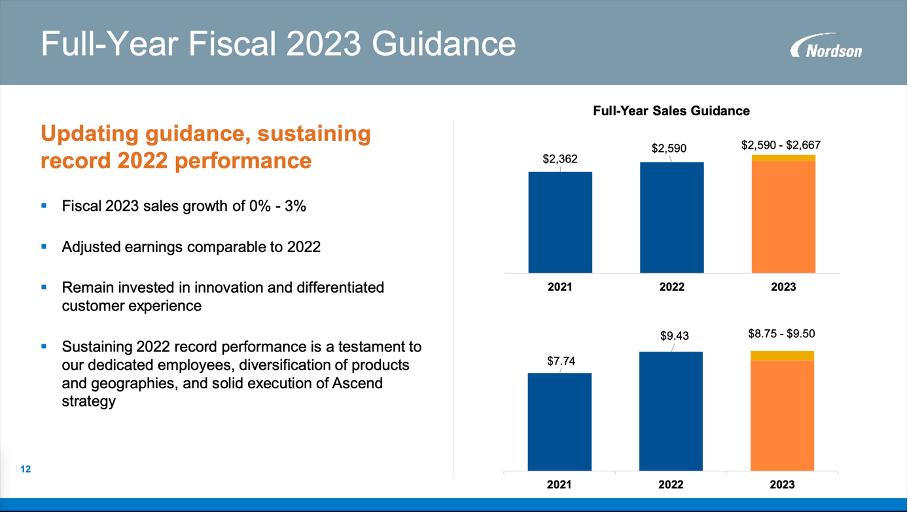

Updated Guidance

While the stock declining about 14% in a single trading day might seem like an overreaction when looking at the quarterly results, the reason for the disappointment was probably the updated guidance. For fiscal 2023, Nordson Corporation is now expecting sales to grow in a range between 0% and 3% and is targeting a range between $2,590 million and $2,667 million. Adjusted diluted earnings per share are expected to be in a range of $8.75 to $9.50 per share - compared to a diluted EPS of $8.81 in 2022, reflecting a range from a slight decline of 1% to about 8% growth.

Nordson Corporation Q1/23 Presentation

{kind=link}

The huge problem - and reason for disappointment - was the lowering of the guidance as Nordson Corporation had expected sales growth to be as high as 7% in a previous guidance and the top end of the EPS range was $10.10 instead of only $9.50.

CyberOptics Acquisition

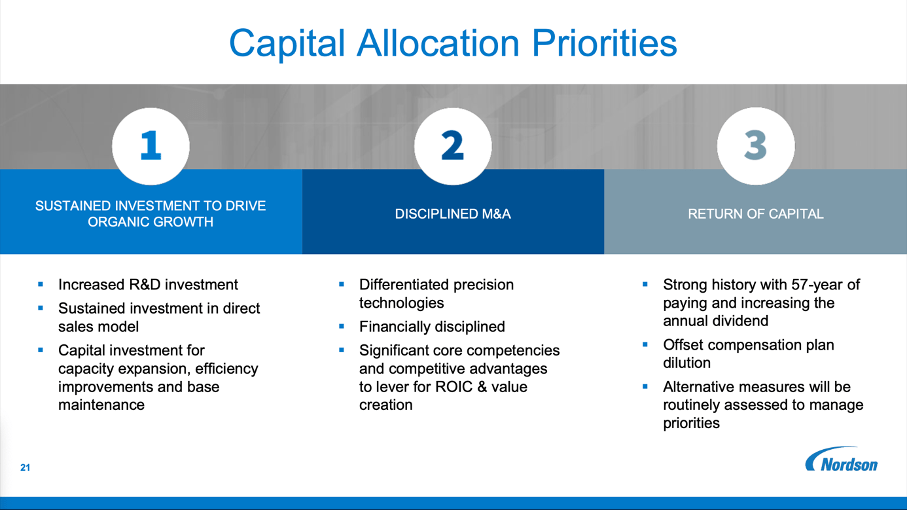

One of the three major capital allocation strategies of Nordson Corporation is merger and acquisitions.

Nordson Corporation Investor Presentation

{kind=link}

And in August 2022, Nordson Corporation announced its intention to acquire CyberOptics and on November 3, 2022, the acquisition was completed . The company was acquired for $54 per share, resulting in an acquisition price of $380 million. CyberOptics is a leading global developer and manufacturer of high-precision 3D sensing technology solutions, and its portfolio is consisting of high-precision inspection and metrology sensors and systems. The company has about 200 employees and generates about $100 million in annual revenue and is now part of Nordson Corporation's Test & Inspection Division.

And of course, the acquisition had an impact on the balance sheet. In my last article, I wrote that we should not worry about the balance sheet - and that is still the case, although the balance sheet got a little worse. On January 31, 2023, Nordson Corporation had $2,107 million in goodwill and compared to total assets of $4,237 million, 50% of total assets are now goodwill, which is certainly a problem (in my last article it was 48%) and this increases the risk for goodwill impairments (at least in theory). The company also has now $421 million in short-term debt and $595 million in long-term debt, resulting in $1,016 million in total debt. Compared to a total equity of $2,447 million, we get a debt-equity ratio of 0.42 (compared to 0.36 in my last article). And when comparing the total debt to the operating income of $702 million in fiscal 2022, it would take less than 1.5 years to repay the outstanding debt.

Determining an Intrinsic Value

In my last article, I described Nordson Corporation as fairly valued and in this article, I would back up the "Hold" rating again as in my opinion not much has changed, and we can determine a similar intrinsic value for Nordson Corporation as about 10 months earlier.

When looking at the valuation multiples Nordson Corporation is trading for, we see a similar picture as in our last article. Right now, Nordson Corporation is trading for a P/E ratio of 24 and a price-free-cash-flow ratio of 25.4. Both ratios are neither cheap nor extremely expensive. And both are more or less in line with the company's 10-year average P/ E ratio of 25.56 and 10-year average P/FCF ratio of 23.71.

And when trying to determine an intrinsic value for Nordson Corporation by using a discount cash flow calculation, we can use similar assumptions as in our last article. As a basis for our calculation, we can once again take the free cash flow of the last four quarters, which was $470.2 million. In my last article, I calculated with a growth rate of 6% from now till perpetuity and when taking 57.8 million outstanding shares and a 10% discount rate we get an intrinsic value of $203.37 for Nordson Corporation.

Nordson Corporation Investor Presentation

{kind=link}

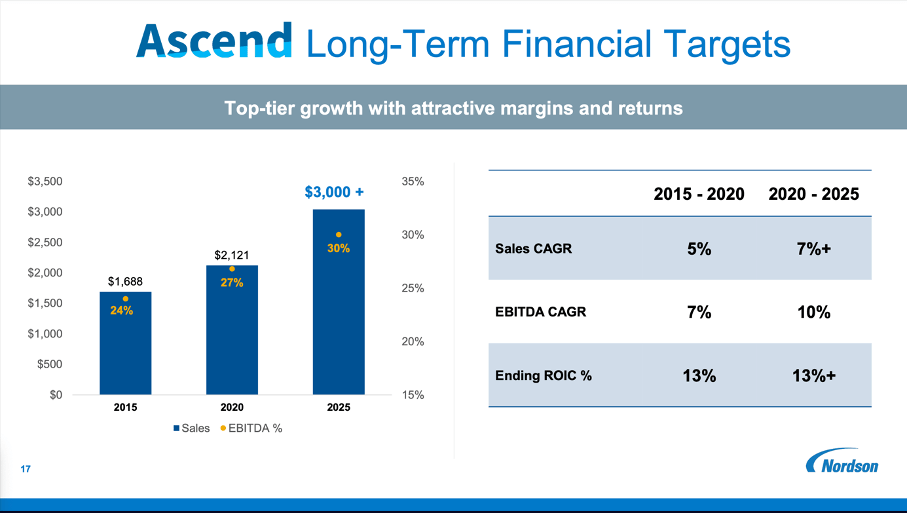

Of course, we can make the argument that 6% growth for the next 5 or 10 years might be too pessimistic as the long-term financial targets of management are at least 10% growth and the growth rates in the past have also been higher.

| EPS CAGR | Since 1980 | Since 1992 | Since 2000 | Since 2010 |

|---|---|---|---|---|

| 10.36% | ||||

| 9.96% | ||||

| 11.34% | ||||

| 11.22% |

In the chart above, I tried to pick dates from the last forty years to show the growth over the long run but avoided years which appeared to be extreme outliers. And I think it is safe to say that Nordson Corporation was able to grow in the low double digits in the last few decades and based on that numbers we can make the argument that we should calculate with a higher growth rate than 6%. When assuming 8% growth for the next ten years instead, we get an intrinsic value of $234.33 for Nordson Corporation and the stock would be trading for a discount of 12%. We could even be more optimistic and assume 10% growth for the next ten years, which would lead to an intrinsic value of $269.93 for the stock, and in this case, we could call Nordson Corporation a bargain.

However, we also must take into account that we could be at the eve of a global recession and should maybe not calculate with such optimistic assumptions but rather calculate with a declining free cash flow in the next few quarters. And when looking at the stock performance during the last recessions, Nordson Corporation usually declined steeper than 23%. Especially in the early 1980s, the stock declined almost 60%, and during the Great Financial Crisis, the stock declined 74%.

In my opinion, Nordson Corporation is fairly valued and certainly not the worst investment one can make right now. But it is also not a bargain or a stock for which we can assume impressive outperformance in the years to come.

Conclusion

In my opinion, Nordson Corporation is still fairly valued and can be seen as a "Hold". And while one can make the argument for a higher intrinsic value - when using higher growth assumptions (that might seem reasonable when looking at the past performance) we should not ignore the high risk of a recession in the coming quarters, which will lead to a lower free cash flow and probably a declining stock price.

For further details see:

Nordson Corporation: Still Not A Bargain