NDSN - Nordson: Great Business But Too Expensive To Buy Here

Summary

- Nordson is a leader in the precision technology industry.

- The company has a well-balanced customer base between five diverse end markets.

- The company is of high quality, but future returns do not look attractive.

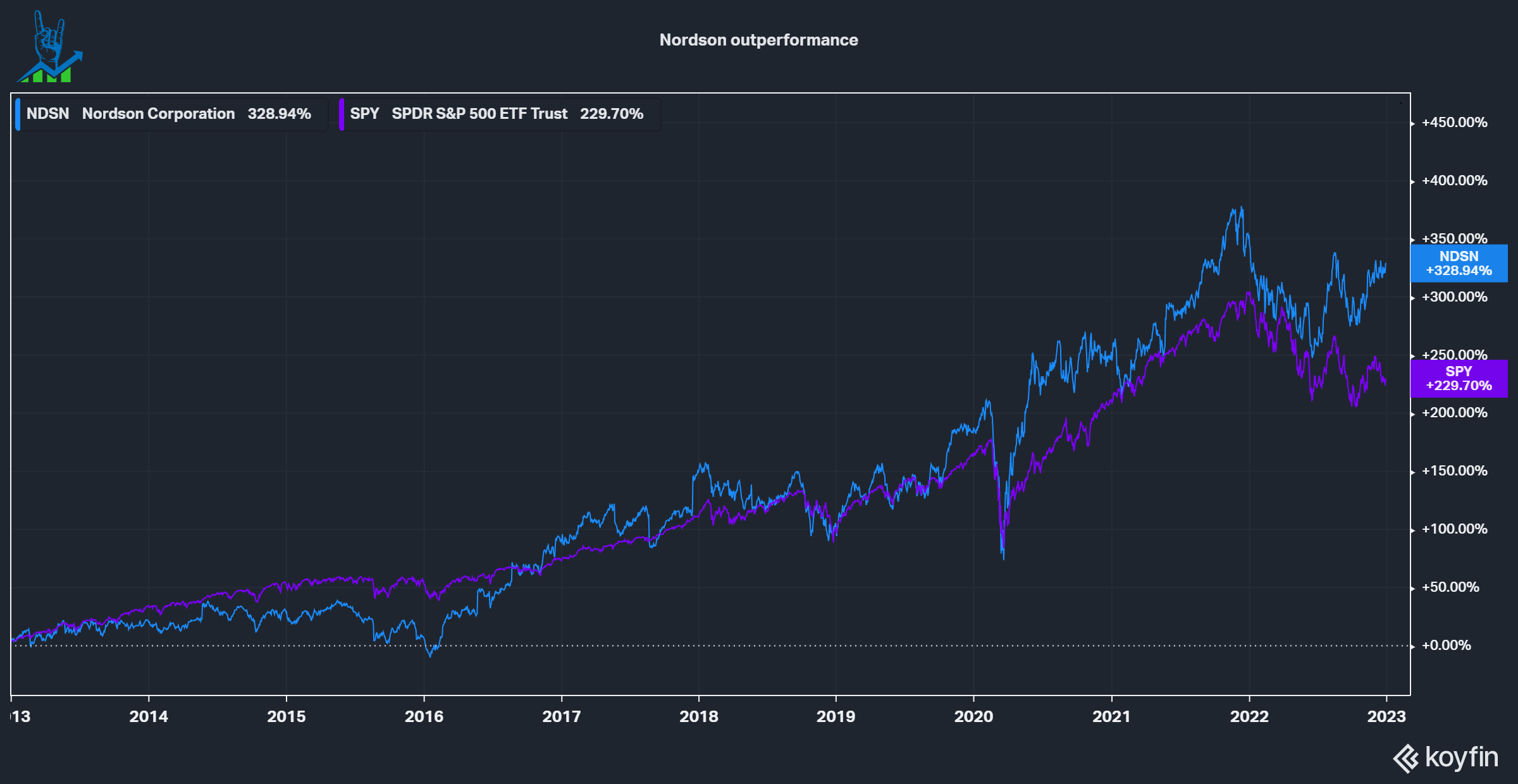

Nordson (NDSN) is an industrial company focused on precision technology that comfortably beat the S&P 500 over the last decade. Nordson is said to be a high-quality business, so let's see if it can hold up to its name and maybe even present an attractive investment opportunity at current levels.

{kind=link}

What is Precision Technology?

Precision Technology is an undefined term that usually means that something is precise. Nordson divides its operations into three divisions that serve five end markets:

- The Industrial Precision Solutions division accounts for 51% of revenues and is the focus of Nordson. The division consists of Adhesives, Industrial Coating Systems, Management & Control Solutions and Polymer Processing Systems. To sum it up, it is predominantly packaging and other processes happening towards the end of an industrial manufacturing process.

- The Medical Fluid Solutions division accounts for 27% of revenues. The division also focuses Fluid Management and other products focusing on storing or transferring medical equipment.

- The Advanced Technology Solutions division accounts for 22% of revenues. The division consists of Electronic Processing, Test and Inspection Systems.

We see that Nordson focuses on machines, parts and consumables geared toward the last stages of industrial manufacturing processes like packaging, testing and inspection. This results in a high percentage of recurring sales (51% of revenue is Parts and Consumables, with the remaining 49% being System sales), the holy grail of any investment. Recurring revenues increase the certainty that a company (and analysts) can forecast the business and reduce the need always to sell new products. Ideally, you want to have a smaller percentage of system sales, requiring a higher rate of recurring sales. Nordson is pretty close to that setup.

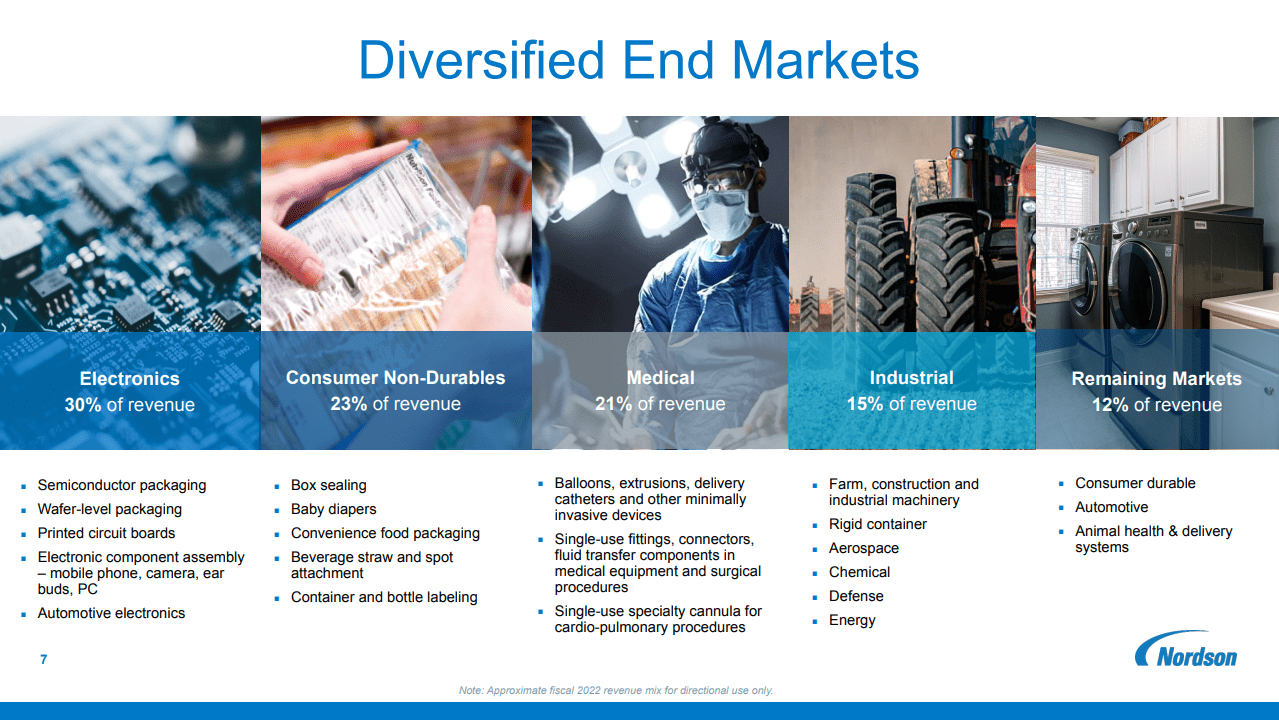

Furthermore, Nordson has a very diversified customer base, spread across five end markets between 12 and 30 percent of total revenues. In the picture below, you can also get a better picture of Nordson's different product offerings.

{kind=link}

Growing organically

Nordson is operating in relatively stable industries due to its high mix of recurring revenues. In the table below, I compiled some numbers based on 2022 regarding the different segments (expected growth rates/CAGR are taken from management). For the most part, Nordson doesn't expect any extraordinary organic growth in its business and expects the organic growth in all its divisions to be between 3-5% with some potential upside. An organic growth rate of 3-5% does not excite me, so they must either trade at a high FCF yield or grow earnings by other means.

| Revenue |

| EBITDA margin |

| Expected CAGR |

| % of total revenues |

| Industrial Precision |

| $1337 million |

| 35% |

| 3+% |

| 51% |

| Medical Fluids |

| $690 million |

| 40% |

| 5+% |

| 27% |

| Advanced Technology |

| $563 million |

| 25% |

| 5+% |

| 22% |

Growth through M&A

Due to the lacking organic growth, Nordson occasionally acquires companies to add to its portfolio. Throughout the last decade, the company spent a total of $1.66 billion cash on acquisitions, which accounts for a very modest 12.6% of the Free Cash flow the company generated in the same period. It's common knowledge that Mergers and Acquisitions are a risky endeavor for companies, with the common knowledge being that between 70-90% of M&A destroy value . Therefore, a company that does strategic M&A needs to show a good framework and discipline in its approach. I want to see the following aspects of such a strategy:

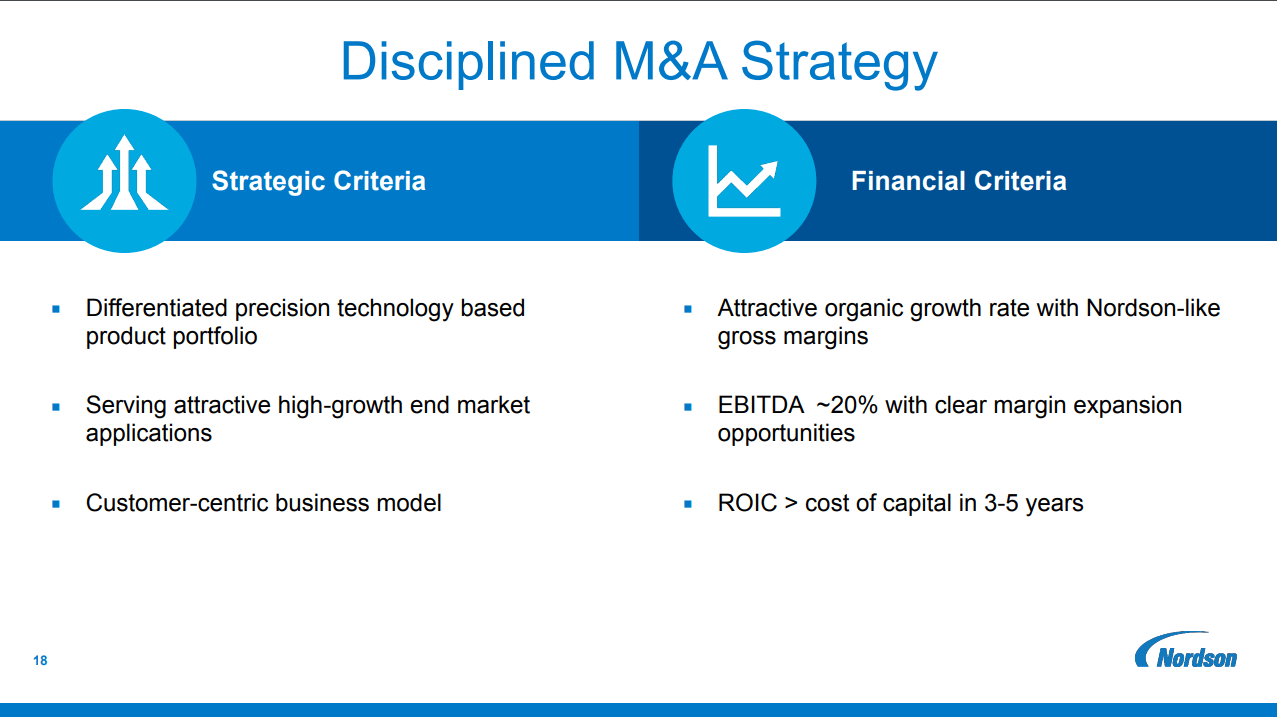

- A strategic fit into the business model. This can be gaining market share in existing business lines, entering adjacent businesses or cost synergies. I don't like to see totally unrelated businesses being acquired; that often backfires due to the lack of existing knowledge in those areas. Nordson addresses this point and points towards a product portfolio within Nordson's circle of competence and in high-growth end markets.

- Integrating new businesses is always critical; if two business cultures clash, it often leads to failure. Nordson addresses this by requiring a customer-centric business model, as Nordson has with its Ascend Strategy .

- A big contributor to why most M&A destroy value is a focus on revenue growth. That is why I want to see a focus on the profitability of the business. Nordson addresses the margins and requires at least a 20% EBITDA margin with the potential for improvement. Furthermore, they need the ROIC to be above the cost of capital in 3-5 years. This last part is a bit generous, in my opinion, because a good company should always generate returns above its cost of capital.

- Lastly, the price paid matters a lot and often is a significant contributor to value destruction. Although Nordson doesn't explicitly talk about a hurdle rate or preferred multiple for acquisitions, based on the last additions (mid to high teens EV/EBITDA), the company seems to buy around its own multiple. Not great, but it also doesn't seem like overpaying.

{kind=link}

The Efficiency Lever

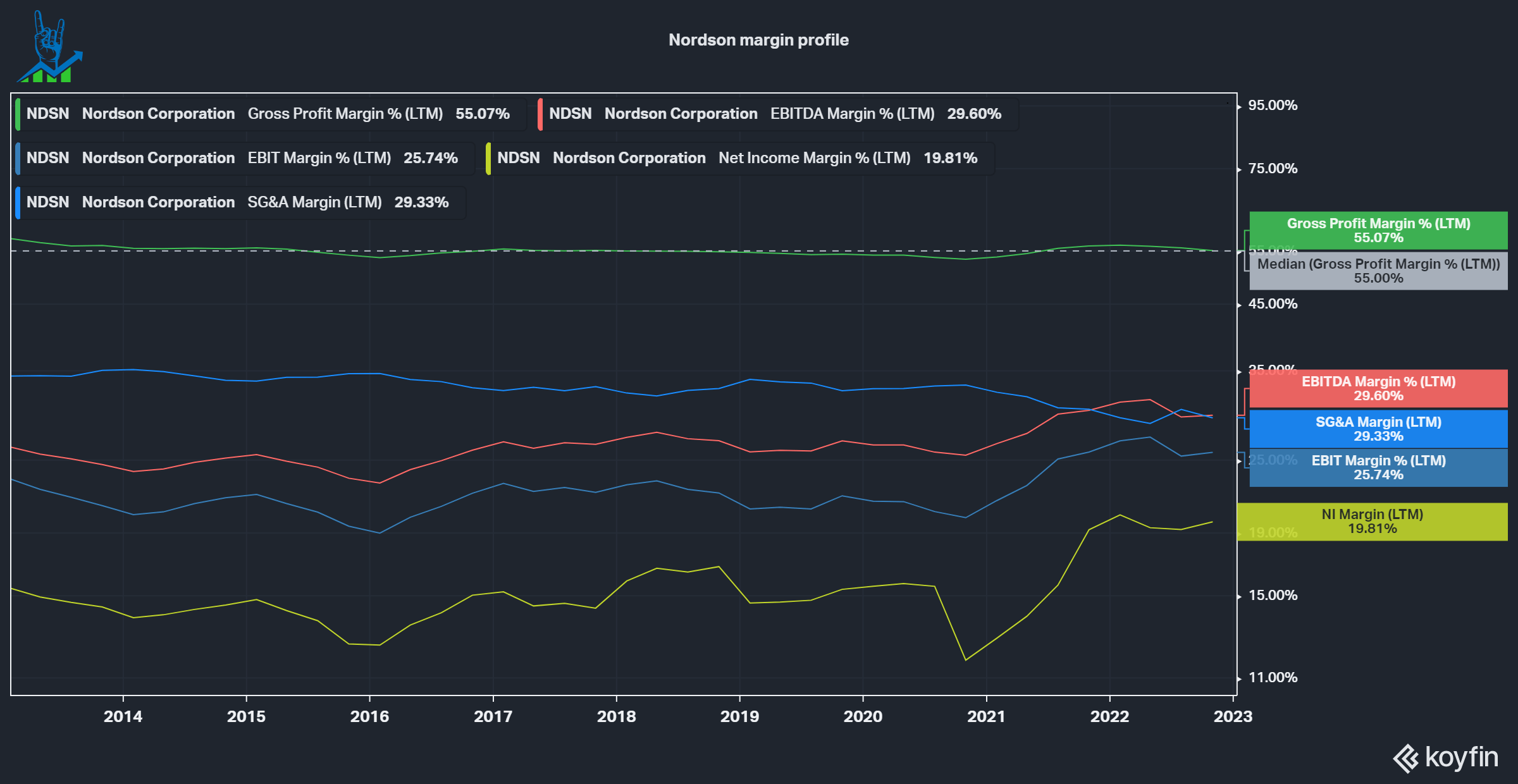

The last lever the company has to pull is margin improvements because it's about earnings growth, not revenue growth. The graphs below show that gross margins have remained steady at 55%, while profit margins are trending upwards. A great metric to track that gets too little attention is the SG&A margin, which represents the bulk of the company's costs. We can see that the SG&A margin gradually declined from 35% to 29%, which coincides with profit margins increasing by roughly 5-6%. The company still has room to grow its margins, but it won't be too meaningful. Additionally, we can look at the efficiency of Nordson's reinvestment by looking at the spread between ROIC and WACC , which is at a healthy 8%. We aim for at least 2%; otherwise, the company is destroying shareholder value.

Nordson's margin profile (Koyfin)

{kind=link}

A quality business trading above fair value

To value Nordson, I have done an Inverse DCF analysis with a 10% discount rate/required rate of return, a 3% perpetual growth rate and the assumption that the share count will be reduced by 1% annually through buybacks following the past decade. According to the model, Nordson needs to grow FCF at 12% in the first five years, followed by 10% in the following five years. Management guided with a medium-term (20-25) outlook of 7+% sales growth and 10% EBITDA growth, so we can assume that FCF should also be around the 10% mark. At this price, I do not see great returns coming toward Nordson. The company would need to deploy significantly more money to M&A than its historic 10% of FCF to grow fast enough to justify its stretched valuation.

Nordson Inverse DCF model (Authors Model)

For further details see:

Nordson: Great Business, But Too Expensive To Buy Here