NDSN - Nordson Has A Challenging Year Ahead Of Them

2023-10-18 13:34:56 ET

Summary

- Nordson Corporation is experiencing the effects of the global economic slowdown and geopolitical risks, particularly with China within the electronics and medical fluid components.

- Management expects medical fluids to improve in 1h24 while electronics will begin recovering in 2h24.

- Revenue is expected to grow 0-2% for FY23 and can potentially experience similar effects throughout 2024.

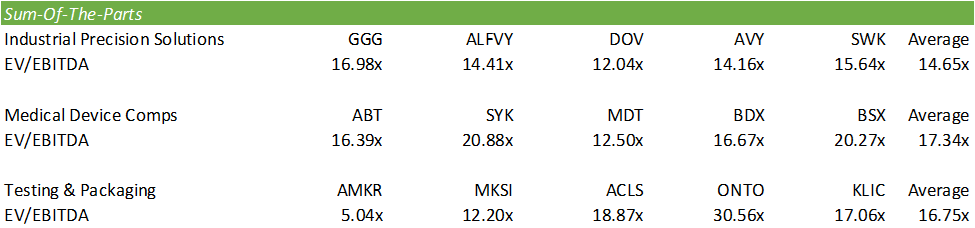

Nordson Corporation ( NDSN ) is currently feeling the effects of the global economic slowdown in conjunction with the geopolitical risks posed by trade and supply chain challenges, primarily with China. Despite having the ability to follow the customer if capacity were to be relocated out of China or expanded outside of China, there are still economic growth risks in the electronics space that must not be overlooked. With one quarter of reporting left in the fiscal year, management is anticipating a mere 0-2% topline growth with the bottom-line narrowing to $8.90-$9.05/share. Using a SOTP (sum of the parts) model, I provide a target EV/EBITDA multiple of 15.69x and a SELL recommendation with a price target of $205.60/share.

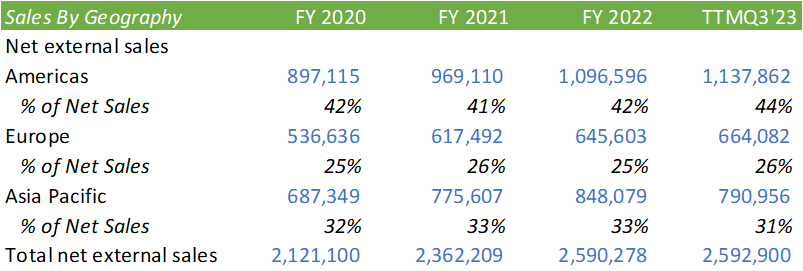

Nordson is currently feeling the beginning of the rippling effects of the global economic slump as we enter a more challenging market. On a geographic basis, APAC organic sales declined -9.7% q3'23 with Americas experiencing a 3.2% increase and EUR a 4.3% increase. Though Nordson doesn't break out China-specific sales, management does suggest a significant portion does come from the region.

{kind=link}

Though it's challenging to tell just how much trade with China will affect future earnings, this might be the beginning of a long-term trend as the US and China decouple supply chains. Per data from OEC.World :

In August 2023, the decrease in China's year-by-year exports to the United States was explained primarily by a decrease in product exports in Computers ($-478M or -10.4%), Other Plastic Products ($-184M or -16.8%), and Centrifuges ($-135M or -40.4%).

Management is in the camp that this is a short-term cyclical trend and should last 4-5 quarters.

The cyclical downturn of demand in the semiconductor market will anniversary in the second quarter of fiscal 2024, which aligns with the historic downcycles lasting approximately four to five quarters.

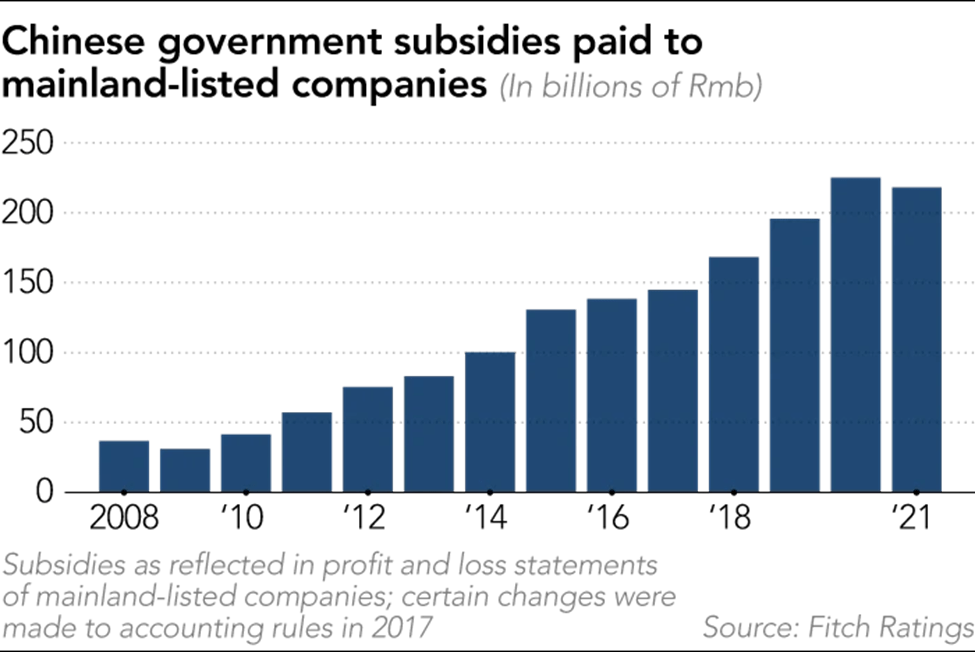

Electronics and medical fluid components might be major challenges for Nordson in China as the CCP seeks to insource electronics manufacturing. The development of electronics and medical devices are both being heavily subsidized for future growth in China, posing a threat to foreign operators. This may affect both Nordson and their clients within China.

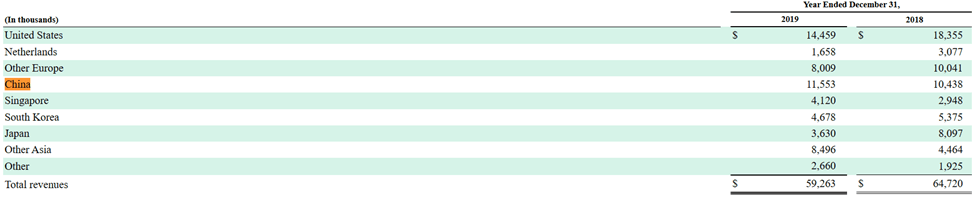

One of Nordson's major acquisitions in recent years was CyberOptics. CyberOptics is in the OSAT business and competes in an industry that predominantly resides in China. Reviewing pre-acquisition filings of CyberOptics, nearly 20% of revenue had derived from China.

{kind=link}

Because Nordson does not break out these figures, it's challenging to say whether these operations are still standing. On a relative basis, assuming CyberOptics sales have not grown in China, revenue in China for the OSAT business accounts for under 1% of total sales.

As for medical devices, China accounts for ~20% of the global market. According to Deloitte , China's regulatory authority has created policies to favor domestic manufacturers by providing subsidies and tax credits.

{kind=link}

Time will tell whether this leads to a long-term secular decline in Nordson's Chinese presence or is just a cyclical effect as a result of worsening economic conditions in China. Given the current trade restrictions on some electronics as enacted by the Biden administration, China may further seek to bolster their domestically manufactured devices. If this does occur, Nordson has the capabilities to move operations to regions their clients relocate to. As of q3'23, 75% of the revenue generated by the electronics business came from APAC with a substantial portion from China.

Overall, Nordson expects medical fluid components to begin recovering in 1h24 and electronics to begin recovering in 2h24. Management was adamant in maintaining their $3,000mm 2025 revenue target with 30%+ EBITDA margin.

Nordson did experience strong growth in their polymers business and has a strong runway as recycled polymers becomes a bigger focus in the EU, whether through government mandates or actionable business decisions. Nordson designs and manufactures the systems to execute this process. Please read my analysis on LyondellBasell ( LYB ) for a more detailed analysis on the polymer industry.

{kind=link}

Overall margin compression has been trending over the course of the last year but still elevated when compared to 2020 & 2021 figures.

Nordson is currently in the process of issuing $850mm of debt in pursuit of acquiring ARAG Group, bringing net debt up from $695mm as of q2'23 to $1,545mm. This will more than double Nordson's leverage ratio from 0.88x to 1.95x, which is still relatively low. The new issuance is a combination of $500mm in 5.80% notes due in 2033 and $350mm in 5.60% notes due in 2028. The addition of these notes will increase interest expense from 5.25% to 5.50%. Though that doesn't equate to a huge increase, it will lead to some bottom-line compression assuming an additional $20-30mm in revenue for FY23, as management suggested. ARAG will provide some EBITDA margin accretion with their high-30% range; however, this may only be a drop in the bucket when considering the scale of total operations.

Valuation

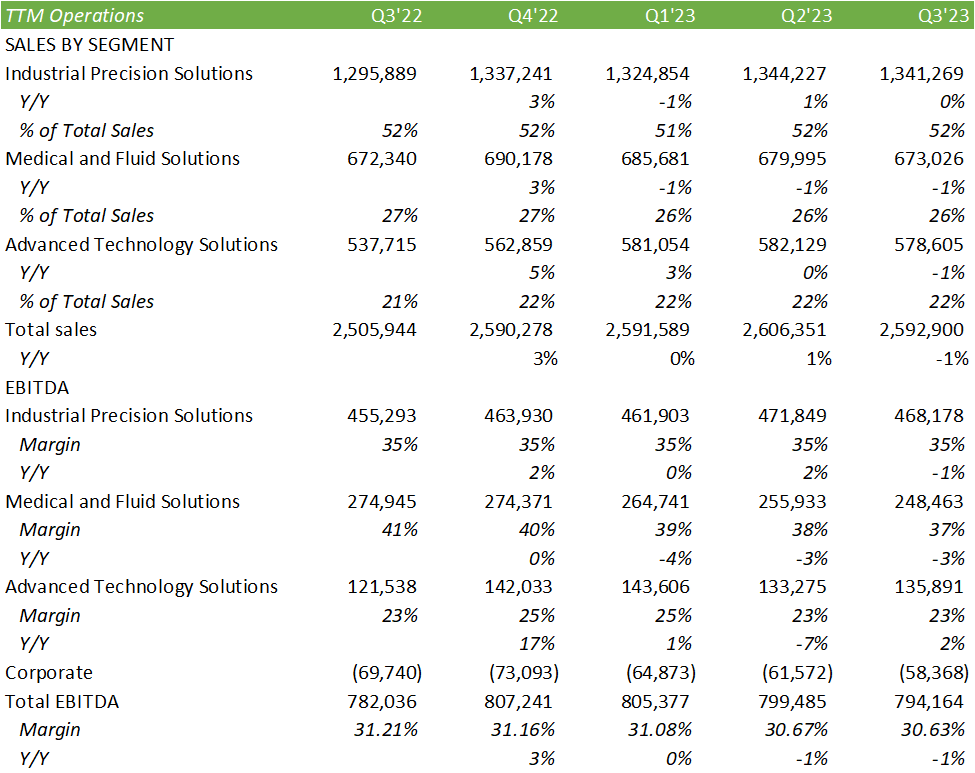

Given Nordson's diverse business, I believe a SOTP analysis is prudent. Breaking out their three segments, Industrial Precision Solutions, Medical & Fluid Solutions, and Advanced Technology Solutions and their respective weights to EBITDA, I came up with a target FY23 EV/EBITDA multiple of 15.69x for a price target of $205.60/share, an -8% downside to the current trading price. NDSN currently trades at 17x FY23 EV/EBITDA for a FCF yield of 4%. I believe this SELL recommendation is appropriate given the current macro challenges, geopolitical risks in APAC, and flat growth expectations for the duration of the year. Despite these near-term challenges, I do believe Nordson is a well-run organization and will make a great candidate for a future buying opportunity at a more appealing price.

Corporate Reports SeekingAlpha

{kind=link}

My final note on Nordson is that insiders have been selling a good portion of their holdings over the last few months. Though this is likely a result of their stock compensation, insiders selling stock can also be seen as a signal.

{kind=link}

For further details see:

Nordson Has A Challenging Year Ahead Of Them