NDSN - Nordson Is Starting To Look Interesting

2023-05-29 10:00:00 ET

Summary

- Nordson has underperformed the market since I first covered the stock.

- After lowered guidance in Q1, the stock dropped over 10% and hasn't moved much since.

- Valuation looks attractive to consider starting a position.

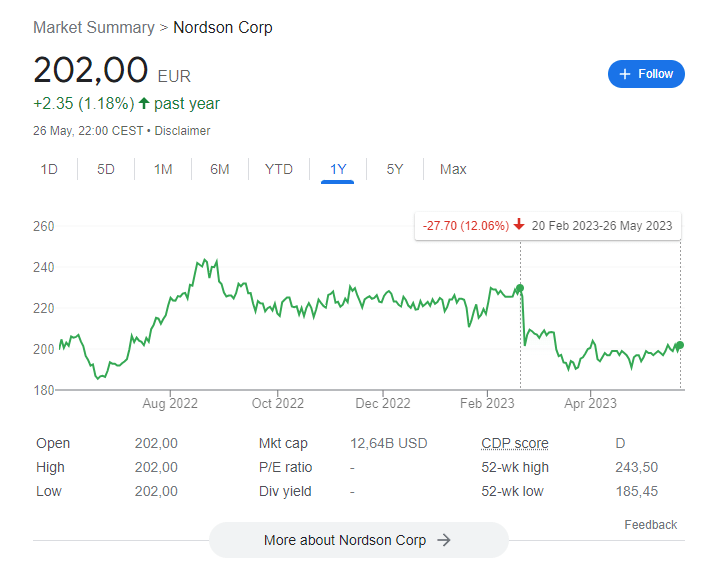

In January, I first published an article on Nordson ( NDSN ), highlighting the high quality of the business but also the high price and putting a hold rating on NDSN stock. After a disappointing Q1, shares plunged over 10% and the price hasn't moved much since then. The company also reported Q2 results last week. Let's see if the company is now a compelling investment after a tough first half of 2023.

{kind=link}

Nordson stock performance (Google)

Disappointing first quarter results?

First quarter results aligned with expectations and missed EPS by 1% and revenue by 2%. Overall revenues were flat, driven by 1% organic growth, 3% growth from M&A and a 4% forex headwind. Free cash flows increased and saw a strong cash conversion rate of 109% (compared to adjusted net income). The market got spooked by a lowered full-year 2023 guidance:

- Sales guidance lowered from $2,616-$2,772 to $2,590-$2,667

- Adjusted EPS guidance lowered from $8.75-$10.10 to $8.75-$9.5

Overall not a terrible quarter; a slightly lowered guidance on the high-end of the EPS guide shot the stock down over 10%.

Second quarter

Second quarter results beat the top (7%) and bottom line (2%). Once again, currency headwinds held growth down a bit, but EPS saw a healthy 18% jump. Free cash flow almost doubled from $84 million to $159 million and saw a strong 118% cash conversion. Q2 saw another update to the full-year guidance:

- Adjusted EPS was narrowed down from $8.75-$9.5 to $8.9-9.3

The market reacted neutrally toward the results.

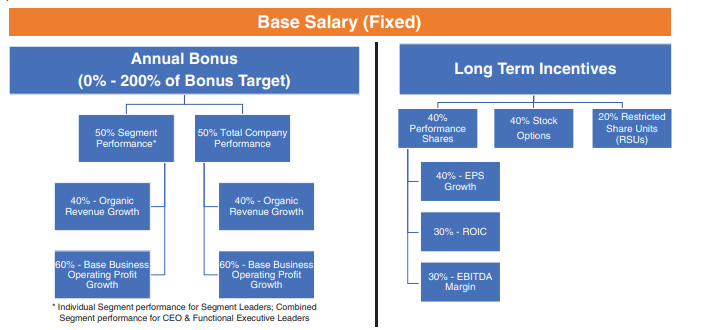

A textbook Compensation structure

It is vital to understand the compensation and ownership structure of a company. To do that, it's best to look into the Proxy statement . We can see that most management compensation is at risk, meaning it depends on business performance. 88% of CEO pay is at risk (76% from long-term compensation, 12% from short-term compensation and 12% base salary) and 77% for the average named executive officer (62% long-term, 15% short-term, 23% base salary). This is a good mix and we should always prefer pay for performance compensation.

The short-term compensation or annual bonus is paid in cash and (depending on which NEO) is based on 40% organic revenue growth and 60% base business operating profit. I like these criteria because they do not incentivize management to make bad acquisitions to meet their targets.

The long-term incentives are paid in 40% performance shares, 40% stock options and 20% RSUs. Stock options and RSUs do not have special criteria, but the performance shares are tied to EPS growth (40%), ROIC (30%) and EBITDA margin (30%). In 2021 the company switched its long-term compensation from total shareholder return benchmarked against the S&P 900 to these metrics, a great change! Management is aligned to prioritize profitable growth with a high return on invested capital. My only criticism is the lack of a cash flow metric (EBITDA is a proxy for cash flow, but I'd like Operating or Free Cash Flow instead).

Lastly, it is essential to know if there is insider ownership. While the management team owns under 1% of the equity, around 9% of the shares outstanding are with the Nord Foundation and Nord family members.

{kind=link}

Nordson Compensation structure (Nordson Proxy)

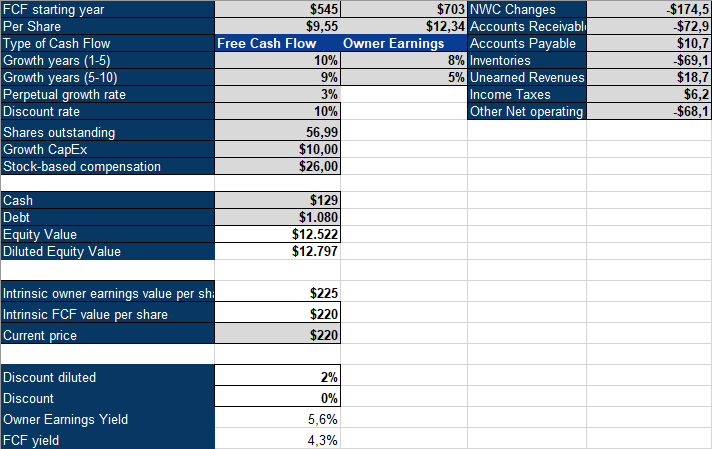

Price is starting to get attractive

Let's value Nordson using An inverse DCF model and multiples. Below you can see my inverse DCF model. I use traditional Free cash flow and Owner Earnings (Free cash flow - SBC +/- changes in NWC + growth capEx). We can see that free cash flow was suppressed quite a bit by changes in NWC and if we adjust for it, we get $703 million in owner earnings. Using a 10% discount rate, Nordson would have to grow its owner earnings by 8% for the next five years, followed by 5% growth for the next five years. This seems reasonable if we consider that Nordson guides for 7% revenue CAGR and 10% EBITDA CAGR until 2020-2025. Nordson expects its Industrial Precision Solutions segment to grow at 3%+ over the long term, while Medical Fluids and Advanced Technology Solutions should grow at 5%+ over the long term. These aren't exceptionally high organic growth rates, but Nordson has a history of accretive M&A and increasing the company's margin profile. The valuation doesn't look demanding for a proven company.

{kind=link}

Nordson Inverse DCF (Authors model)

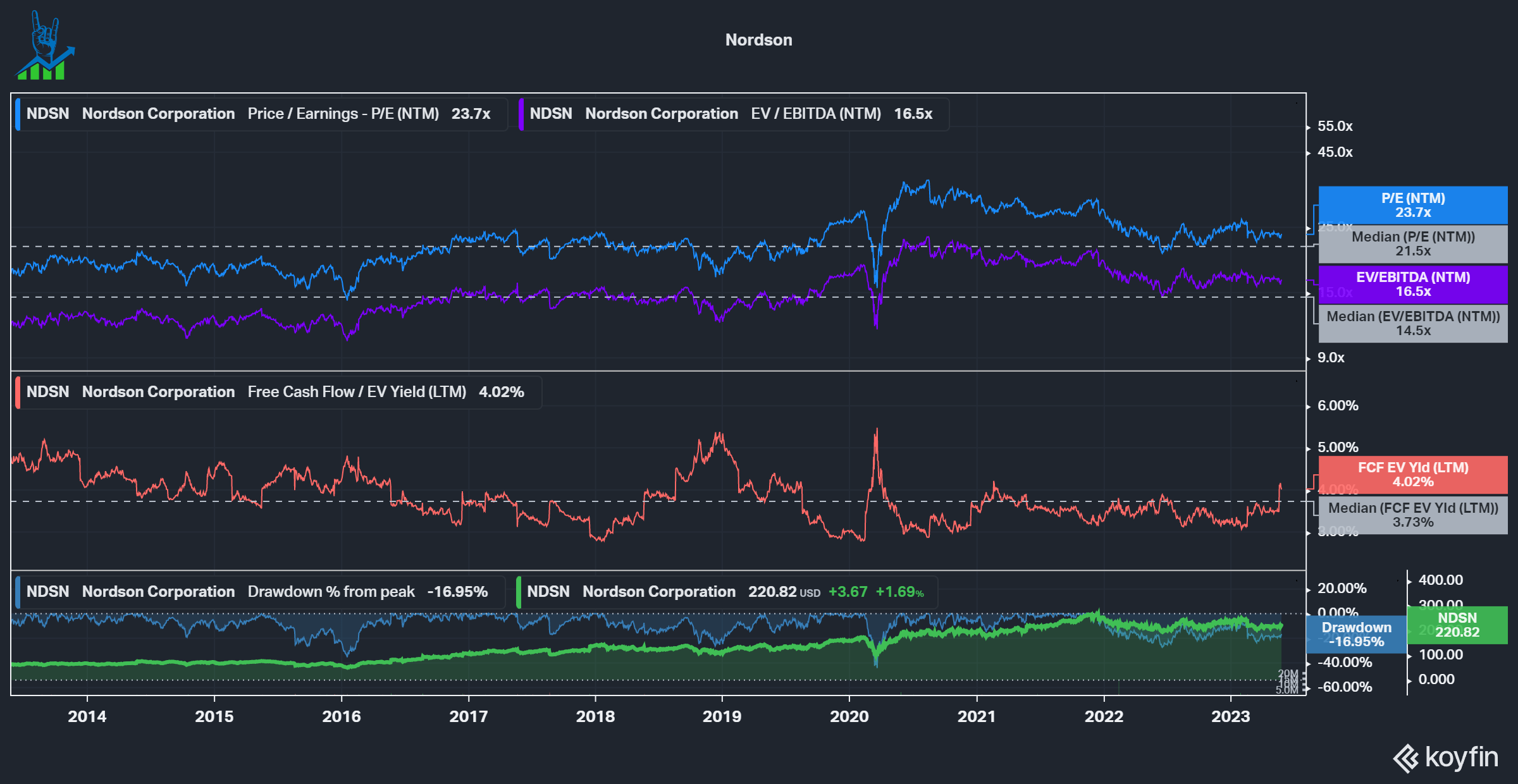

On a multiple basis, we can see that PE and EV/EBITDA are slightly elevated compared to the last decade, but most of the valuation premium it had in 2020-2022 is gone. The FCF yield is above the 10-year median.

{kind=link}

Nordson valuation multiples (Koyfin)

Overall, Nordson is not a screaming buy at these levels, but it might be a good starting point to accumulate shares in a high-quality compounder.

For further details see:

Nordson Is Starting To Look Interesting