TTWO - Nordstern Capital - Embracer Group AB: I Am Accounting On Embracer

2023-05-11 01:45:00 ET

Summary

- Embracer Group is facing a streak of rough quarters.

- A group of short sellers fed their narrative to the Financial Times and the journalists fell for the ‘click bait’ arguments.

- The Financial Times article provided no argument to support the hypothesis.

- THQQF stock price leads to an enterprise value significantly lower than the sum of its parts, and the stock price can’t be wrong.

- I prefer Embracer Group’s strategy and am accounting on Embracer.

The following segment was excerpted from this fund letter.

Embracer Group ( OTC:THQQF )

(share price increased + 2% in 1Q 2023)

Embracer Group is facing a streak of rough quarters: a series of underperforming game releases, delays, reduced guidance, promised but yet-to-close partnership deals, and recently a series of short seller reports coupled with a Financial Times article that questioned Embracer Group’s business model, profitability, and accounting.

One page of a short seller’s playbook is called hit-and-run. Throw dirt and spin a damning narrative around a company to scare retail investors into selling, after which the short seller covers his position. Embracer Group was an easy target. The company has a large retail shareholder base, complicated financial statements, recent accounting changes, a unique business model, a declining stock price and negative sentiment. Kind of perfect.

A group of short sellers fed their narrative to the Financial Times and the journalists fell for the ‘click bait’ arguments. For instance, Embracer educates its investors to exclude contingent consideration to employees from adjusted profits. This is highly unusual and easy to call outrageous on a whim: employee salaries should not be treated as expenses? How ridiculous.

Before any quick judgement, however, let’s understand the facts. Embracer Group’s acquisition model is unique in that Embracer Group keeps managements and employees of acquired companies. In fact, Embracer offers large and long earn-out packages to former owners of said companies. These earn-outs will be settled in the future, partly in shares and/or partly in cash, if the acquired companies prove highly profitable. In some cases, Embracer Group issued the shares immediately, but subject to future clawback rights.

A common valuation metric is enterprise value (EV) divided by EBIT (EV/EBIT). Enterprise value equals share price times number of shares, plus debt, minus cash. To calculate Embracer Group’s enterprise value, one could count all potentially dilutive shares from earn-outs and increase Embracer Group’s debt by all potential future cash-payments from earn-outs. However, then it would be double-counting to subtract these same earn-out expenses from EBIT once more.

The newly adopted IFRS accounting rules require in some cases that Embracer Group treats former owners of purchased companies as employees. What essentially is reimbursement for selling the company must instead be treated as salary. In fact, for IFRS accounting rules it is not even essential that the owners indeed stay with Embracer Group, what counts is alone the language of the purchase contract.

A simplistic Gedankenexperiment to illustrate the core of the above:

- Assume that EG buys GG and EG will pay $10 per year over the next ten years to the owners of GG.

- If the former owners of GG part ways with EG, then the purchase price for GG is $100 and EG’s balance sheet debt is $100.

- If the former owners of GG instead stay with EG, then they become employees and the purchase price for GG is $0 and EG’s balance sheet debt is $0. EG’s profits, however, must be reduced by $10 over each of the next 10 years.

From a business owner’s point of view, these are two different methods of counting the same beans. Even if IFRS accounting rules were to require EG to deduct $10 from profits every year, would it not be legitimate to argue that for the benefit of standardization the $10 should be added back to ‘adjusted profits’ each year and instead the entire $100 should be added to debt?

In any event, if one claims that EG should not adjust profits for the $10 ‘salary’, then one must consider that EG’s enterprise value must be calculated using $0 debt. Short sellers, of course, might prefer to just drop half of the equation.

Embracer Group’s financial statements are complicated. This is a reality that won’t change so easily. In addition, the current quarterly filings cannot build upon an IFRS-based Annual Report. Embracer Group’s next annual filings will change that and allow for more clarity going forward. Nonetheless, with Embracer Group as with any other business, investors need to understand the ‘true’ economics of the business (Warren Buffett calls it ‘owner’s earnings’) and should adjust for ‘bizarro world accounting’, as one of my mentors likes to call it.

The Financial Times article not only drilled on accounting, but also indicated that Embracer Group’s acquisitions might not only have no synergies but might actually be worth far less than the sum of its parts. No argument is provided to support the hypothesis. Embracer Group’s acquisitions don’t change management, don’t change employees, don’t change the businesses. Why should these acquisitions be worth significantly less than stand-alone? The only argument seems to be: the stock price says so! Embracer Group’s stock price leads to an enterprise value significantly lower than the sum of its parts, and the stock price can’t be wrong, QED.

Let’s explore synergies. Let’s ask CEO Lars Wingefors: what if Embracer Group would do a deal with Netflix…

“We could make 10 or 20 games together with them, a number of TV series, a number of mobile games, a number of board games, we could do merchandising with them…Embracer could be the most important tool they could find to achieve their strategic goals. This goes for a company like Netflix, but there are many others like it.”

“With some patience it will be much clearer that actually Embracer makes total sense and that we are able to create more value out of the combined group than the individual pieces.”

“We have built the largest capacity of games development in the industry and we have one of the largest portfolio of IPs.” - Lars Wingefors

Nordstern Capital believes that Embracer Group should be worth at least the sum of its parts. In fact, we believe it is probable that Embracer Group’s various parts can profit from each other’s knowledge, contacts, experience, IPs, resources, and all kinds of things. However, regardless of any soft synergies, there lies major power in the sheer scale of the combined group.

Embracer Group’s scale makes the group attractive for partnerships with leading platforms, game engines, and media houses. Transmedia is the perfect strategy to further build and enhance Embracer Group’s IP values together with those partners in a structured and efficient way. In addition, such partnerships could provide predictable cashflows and help to maximize risk adjusted returns.

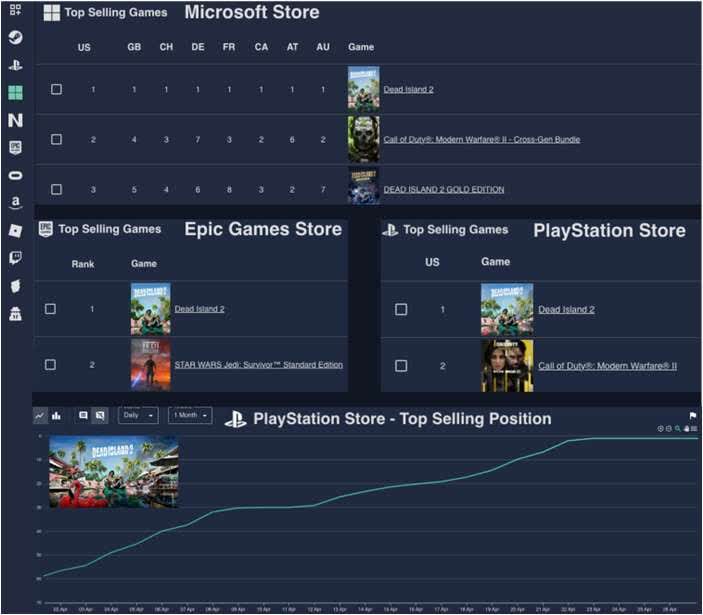

One powerful IP is Dead Island. The recently released AAA-sequel Dead Island 2 is currently topping the US video game sales charts and disproving the often-voiced opinion that mid-size AAA games will be crowded out by big budget megahits.

The CMA report issued in conjunction with the decision to block the Activision ( ATVI ) takeover by Microsoft ( MSFT ) reveals that some games now have budgets of over $1bn. The budget for Dead Island 2 was 20 times smaller. Embracer Group is the developer, publisher, physical distributor, and IP owner. From a return-on-investment perspective

Dead Island 2: #1 on Xbox, PS, Epic. (Database provided by Lakrix (@Lakrixx))

{kind=link}

I prefer Embracer Group’s strategy.

That said, Embracer Group is undertaking a few larger budget productions as well. However, the development of the next Tomb Raider game is paid for by Amazon. Embracer Group received $45m for the early game development so far and will receive payments from Amazon ( AMZN ) for another 10-12 more milestones. It is rumored that TakeTwo ( TTWO ) is pumping $2bn of its own capital into the next GTA6 game. From a cashflow perspective I prefer Embracer Group’s strategy.

Cash flows will be strong in the coming quarters. More money from Amazon, cash from other strategic partnership deals, normalization of Asmodee’s working capital, significant Dead Island 2 revenue, etc. In addition, many upcoming game releases are from studios that traditionally deliver higher-ROI projects, while recent underperformers in the group will likely receive reduced reinvestment.

Embracer Group will probably use the excess cash to reduce debt in the near term. However, Nordstern Capital would not be surprised if a share buyback program is on the agenda, at the very latest at the next Annual Meeting.

I am accounting on Embracer.

DisclaimerThis report is based on the views and opinions of Dr. Johannes Arnold, which are subject to change at any time without notice. The information contained in this report is intended for informational purposes only and is qualified in its entirety by the more detailed information contained in the offering memorandum of Nordstern Capital, LP (the “Offering Memorandum”). This report is not an offer to sell or a solicitation of an offer to purchase any investment product, which can only be made by the Offering Memorandum. An investment in the Partnership involves significant investment considerations and risks which are described in the Offering Memorandum. The material presented herein, which is provided for the exclusive use of the person who has been authorized to receive it, is for your private information and shall not be used by the recipient except in connection with its investment in the Partnership. Nordstern Capital Investors, LLC is soliciting no action based upon it. It is based upon information which we consider reliable, but neither Nordstern Capital Investors, LLC nor any of its managers or employees represents that it is accurate or complete, and it should not be relied upon as such. Performance information presented herein is historic and should not be taken as any indication of future performance. Among other things, growth of assets under management of Nordstern Capital, LP may adversely affect its investment performance. Also, future investments will be made under different economic conditions and may be made in different securities using different investment strategies. The comparison of the Partnership's performance to a single market index is imperfect because the Partnership's portfolio may include the use of margin trading and other leverage and is not as diversified as the Standard and Poor's 500 Index or other indices. Due to the differences between the Partnership's investment strategy and the methodology used to compute most indices, we caution potential investors that no indices are directly comparable to the results of the Partnership. Statements made herein that are not attributed to a third-party source reflect the views, beliefs and opinions of Nordstern Capital Investors, LLC and should not be taken as factual statements. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Nordstern Capital - Embracer Group AB: I Am Accounting On Embracer