NRT - North European Oil Royalty Trust: Underperformance Cements My Thesis

2023-06-15 10:37:26 ET

Summary

- When I last wrote about NRT or the North European Oil Royalty Trust, I still rated the company a conservative "HOLD" due to some valuation issues.

- I now believe we're in for a significant drop in the dividend, which makes me even more cautious.

- Here's my updated thesis for NRT. While I do believe the company has upside, I also believe we should be careful at this time, and see potential for a decline.

Dear readers/followers,

In this article, we'll be looking at the North European Oil Royalty Trust ( NRT ) again. I know at least some of you have invested in this company, and are asking me for continued coverage on this company. I'm happy to provide such, even if at this time I am not invested in the business as such.

Since my last article, NRT has actually underperformed quite a bit. The company is flat, though if you include dividends, it's still up slightly over the S&P500. However, given that these dividends represent what I view as non-recurring incomes due to massively appealing trends, this is not something I view as indicative of the long-term performance of the business.

Seeking Alpha NRT (Seeking Alpha )

Instead, I'm sticking to my thesis for the company. Let me show you why that is as of June, and why my continued stance for NRT remains a firm "HOLD".

North European Oil Royalty Trust - Attractive technically, but problems exist

If you follow my work, the problems I see should not come as a surprise to you. Income investors love this company. Even today, the company technically yields 33.84%. This yield should imply the risk you're taking when investing in the business - and whenever a company reaches a yield like this, it's crucial that you understand underlying trends in the company, which I have been trying to explain for some time.

The decline in the monthly dividend has not yet come. Instead, we even got a small raise of 5% to $1.05 per share. Instead of being ecstatic about this though, I view this as a marked increase in the overall risk to the company. The company obviously saw a massive climb following this announcement, only to crash down back to earth from over $16/share to where it now trades at $12/share. Even if you got that quarterly dividend if you bought for the dividend alone here, you're still likely underwater.

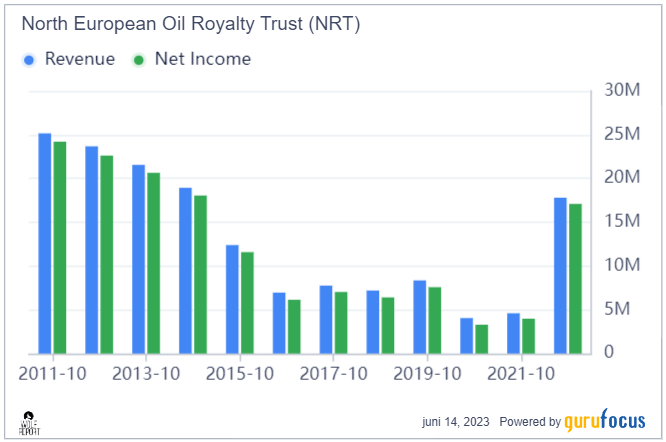

The company is one of the least-issuing companies I have ever covered in terms of financial information, color, and commentary. What we see is what we get. We have 6M23 results and these have seen total royalty income increase by triple digits in terms of percentage due to very strong comps during the last-year period. Net income for NRT is up 222%, with distribution up 225.4% YoY. The mistake is based on expecting this to continue as oil prices continue to decline where we currently are seeing nearly 1-year lows in overall crude futures. Those results are for the 6-month period, by the way.

Seeking Alpha Crude Futures (Seeking Alpha)

Remember, NRT is essentially correlated to crude inventories and pricing. When we're in a situation like this one, it comes as no surprise that the company is getting more for its product - and being a trust, it has rules about how to pay out profits. But we're reversing in terms of price/crude trends, and that means that people who expect the dividend to continue at this pace are deluding themselves. It won't if the company can't get the money for its product.

While increases are still triple-digit, I expect those to slow down markedly in the coming quarter. Here are the 2Q YoY numbers.

{kind=link}

I don't expect the same uptick for 3Q. We've already seen the first signs of things slowing down, as gas prices have declined significantly from the 1Q to the 2Q period. The company has commented on this as well, and I want you to take this in if you're interested in investing in the company - because this is essentially management warning you.

Given the actual quarter-over-quarter decline in gas prices from the first to the second fiscal quarters, the Trust received significantly more royalties than the amount attributable to the respective periods of gas sales and prices. This overpayment of royalties has resulted in a negative carry-over that will substantially offset the amount of royalties that will be paid to the Trust in the third fiscal quarter. Consequently, this reduction in royalty income is expected to substantially reduce quarter-over-quarter cash distributions to the unit owners for the third fiscal quarter.

(Source: NRT, 2Q23 Press Release, Emphasis from Author)

I have seen commentary that implies they're investing because they're hoping for the distribution to stay the same way. My only comment to those investors is that they do not understand this company's business model. They're simply a funnel for whatever money comes their way from sales. When there is less money, less royalties will be paid.

Looking at this company from a fundamental perspective gives us some very distorted numbers, to say the least. Due to its operating model and structure, the company has a net margin of 97.46%, an RoA of over 400%, and a ROCE of 6720%. I don't need to tell you that we can't use such numbers to estimate whether the company has good profitability or not. The company is simply a play on commodity pricing and should be bought as an income investment when there is a weakness to exploit - in a good way. Previously to this oil/crude high, the company had been in revenue and net decline for several years.

{kind=link}

The question is when these trends normalize, and how violently the company will go down when they do - or even before. There's also the simple fact that the company's underlying assets have a lifespan and a limited one. Even with 11 years or more still in the bag, I see some longer-term worries here.

So, I repeat what I said in my previous article. It's not a bad business - just a risky overall play that I wouldn't put capital in unless I saw it as undervalued. It's not undervalued today - I view NRT as currently overvalued. Don't let shorter-term returns like 3-year graphs fool you either. Take a look at what the company has delivered over longer timeframes. It confirms the old adage that if it's too good to be true, it usually is.

I said before, and back in April that I don't expect company share prices to materially improve. The underlying fundamentals simply are not there. This has been confirmed - shares are up less than 0.5% without dividends, and we're staring down the barrel of more softness in commodities like oil- at least for now.

The valuation remains a very tricky prospect, to put it mildly.

NRT Valuation - Let's avoid the obvious pitfalls in the sector

Anytime a company gives you a 33% yield is time to be extremely cautious. Instead, we should expect a normalized yield closer to 6-9% for this company in the longer term. Such a yield is not bad, per se - but it also happens to be a yield we can get from a dozen companies with investment-grade credit and far better safeties than this particular business. What I'm saying here is that NRT is a good investment - but it's not "safe", and there are companies that offer similar yields that are much safer.

Even if I don't expect normalization on the geopolitical level, here meaning Ukraine and Russia, this doesn't go a long way towards making me positive to this investment.

We can expect NRT to still give you income - but that income, as I see it, does not represent a favorable risk/reward when you compare to what else is available on the market at this time. Because the company hasn't really moved from my last valuation, and I in my thesis apply long-term trends and assumptions, you can expect me to not change my price target massively. I still want to discount this company by around 40% to get any sort of appealing price, but I'm also keeping the small bump I made to my PT. Even if we expect crude prices to normalize, I do think we're a long way from going back to the sub-$40s we saw over a year ago.

The reason is the continued exception of Russian crude and continued issues on the global scale - as well as gas. Europe is taking steps further and further towards self-sufficiency. I now view it as extremely likely that at a time when Russia is trying to turn the taps back on, Europe is going to be fairly self-sufficient from Russia in that - because that's what we've been forced to do.

In my latest article, I bumped my PT to $10/share. The share price target represents around 4-5x normalized sales numbers, which is what I'd want to be paying for this company - the sales multiple is the closest thing to a comparison we have. Most of the other multiples make very little sense. With that said, this still comes with the risk associated with nano-cap, which the company remains. But as long as there's life in the company's wells and assets, I can see my way to actually giving this company a positive target as long as it drops low enough.

The fact that this company is undercovered and underappreciated is confirmed by the utter failure of institutions to make a market-beating 80%+ RoR in less than 3 years by buying NRT. However, in order to do that, you would have to have bought NRT at a cheap price and have bought it above other investments which have yielded market-beating returns.

I didn't cover NRT at the time when it was extremely cheap - but if I had, given the valuation, I would probably have called it a "HOLD" (Russia was different back at the time, and few could imagine the conflict that is currently going on). So I'm not saying that I would have done anything differently at that time, though I now have my eyes opened to the company and what it's capable of.

Low valuation and upside. That's what it'll take for me to invest here. And as of 2Q, I'm raising my finger in warning to you, because the company is literally telling us to expect a lower distributable income in 3Q.

So, you have been warned. I'm not changing my thesis by much, and here it is.

Thesis

My thesis for NRT is as follows:

- The company is an interesting play on a specific EU gas/Oil/sulfur asset in Germany. It's not without its general appeal, but I would say that there's too much risk to go fishing here, despite some improvement in price.

- As of June, I'm saying that the company is still too overvalued to make it an attractive "BUY", but I am giving it a continued, clear target.

- I would remain at an updated $10/share PT to stay conservative, making this a very risky play given the correlation to energy prices.

- I consider NRT a "HOLD" here and would wait.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fulfills one of my criteria at this time, I call it a "HOLD".

For further details see:

North European Oil Royalty Trust: Underperformance Cements My Thesis