NOG - Northern Oil and Gas: Big Company Revenue Small Company Flexibility

2023-06-15 15:17:16 ET

Summary

- Their business model consisting of non-operating interests in upstream provides the revenue without the headaches.

- A proven and well-executed strategy of acquisition clearly shows the foresight of management.

- Their flexibility in capital allocation allows them the ability to shift capital at the proverbial "drop of a hat" to the area that can provide maximum return.

Northern Oil and Gas ( NOG ) has the large company feel in their cash flow and revenue return, but the small company flexibility to solidly execute on their plans and return maximum value to their bottom line.

Their business model of investing in non-operating interests in upstream helps to allow them that tremendous flexibility, and furthermore allows them to cherry-pick their wells with precision for the best returns.

In this article, we'll explore the company and its metrics, and by the end, I believe you'll see why I think it's an excellent add for the dividend investor.

Company Overview

Northern Oil and Gas, Inc., an independent energy company, engaged in the acquisition, exploration, exploitation, development, and production of crude oil and natural gas properties in the United States. The company has "a primary strategy of investing in non-operated minority working and mineral interests in oil and gas properties, with a core area of focus in the premier basins within the United States."

The company is purely in the upstream sector and primarily holds interests in the Williston Basin, the Appalachian Basin, and the Permian Basin in the United States. The company is based in Minnetonka, Minnesota.

Operations

Northern Oil and Gas holds positions in some of the most prolific shale plays in North America. Commodity production for the company is split as follows - 52% in the Williston Base with approximately 181,200 net acres, 35% in the Permian Basin with approximately 30,000 net acres, and 13% in the Marcellus Shale with about 59,200 net acres. These positions are in the states of Texas, New Mexico, North Dakota, South Dakota, Montana, and Pennsylvania.

The company currently has approximately 9,400 gross wells on approximately 260,000 net acres. Producing the oil from these wells and acreage are approximately 100 different operators. As of Q1 2023 , out of all these positions being operated in, the company's commodity split is approximately 62% crude oil and 38% gas. Lastly, the company produces approximately 87.4k barrels of oil equivalent per day.

It's important for investors to note that Northern Oil and Gas does not drill wells or operate rigs. The company acquires fractional working interests in drilling units. This allows the company to control capital expenditures higher and lower. Northern Oil and Gas is actually a pretty small company (only 33 employees) despite its impressive reach and working interests. Investors should note the company's size and position as this is a very scalable business model.

Revenue

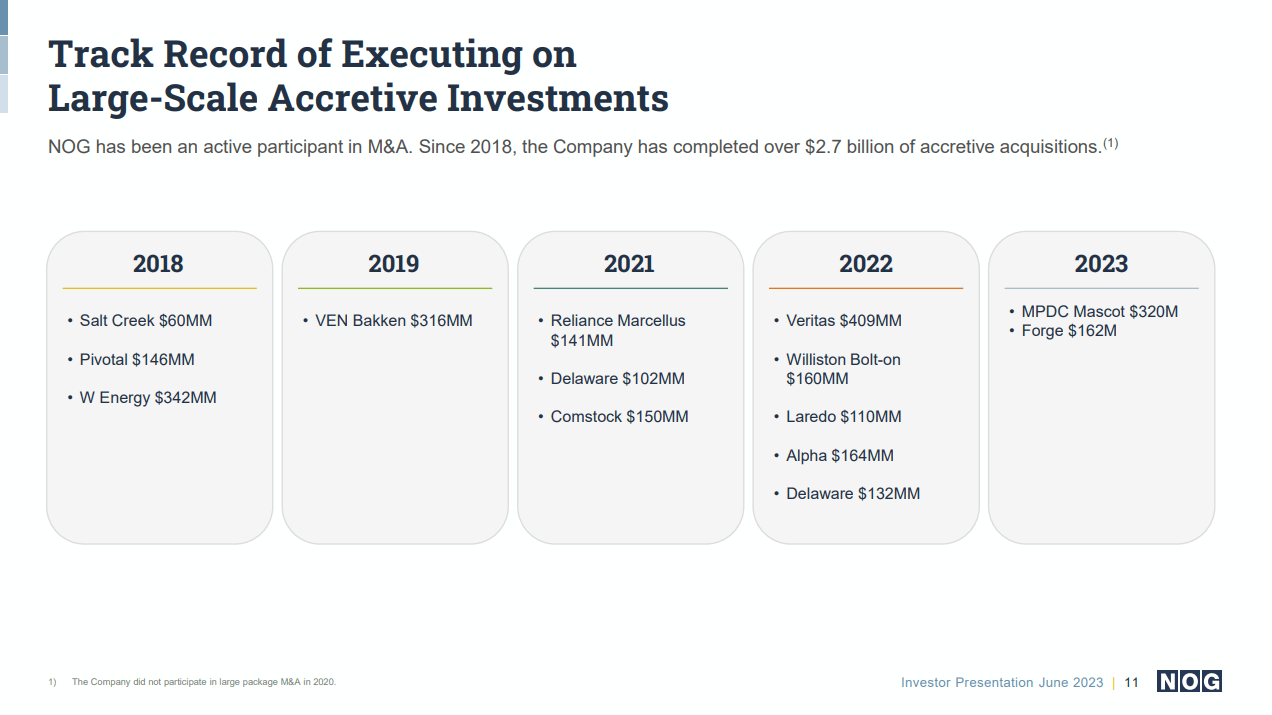

NOG has done a fantastic job of increasing their topline revenue over time due to their aggressive acquisition plan. Let's take a look at exactly how much they've acquired over the last several years:

{kind=link}

These acquisitions have driven cash flow up since 2018. Now their free cash flow reads lower and lower, but that's simply a result of CapEx. See the charts below. They've increased CapEx significantly to continue to purchase more interest in wells, and it's clearly paying off in the cash flow department.

Debt

NOG has issued some debt to finance their acquisitions, and according to their latest 10-Q , they currently have senior notes at a whopping 8.125% interest rate, a revolving credit facility at FFR + 50 bp, and convertible notes at 3.625%.

Normally I'm not a fan of convertible notes, but I actually believe their stock price is likely to rise and as such they can probably get out from under the $500M in debt. The shares will cost them in dividends, but it's probably a better interest rate than they could get today based on their senior notes rate.

They recently made fairly large repayments towards their debt, and it's mentioned in their latest investor presentation that part of their capital allocation focus is debt repayment.

At present, they have no problems paying their interest with an interest coverage ratio of 15x, and with a focus toward paying down their debt, it seems like they have plenty of runway to expand financing to continue to acquire more interest in new wells.

Returning Value To Shareholders

They've been issuing shares to fundraise from the equity markets and help acquire more wells, however, that can't go on forever. I'm not a fan of share dilution, and as their dividend rises it'll become more and more difficult to do so.

The big question for them is if the share issues return in excess of the dividends paid. So far that has clearly worked out for them, but the strong dividend increases can curb that.

{kind=link}

A lot of their recent earnings call focused on the dividend. There's a quote in there that I liked, and highlights some of their capital flexibility (emphasis added by author):

And so, we really try to be very, very careful and methodical about this. That's why we've really stuck to a base dividend. We do believe we have a path to grow it over time, as well as to leave enough meat on the bone and enough excess cash flow to allocate it to things that are going to drive that dividend growth in a solid fashion over that long term period.

Last Earnings Call Analysis

Company leadership reported a strong start to the year that included strong consistent results with record adjusted EBITDA and record oil and total volumes. The leadership team emphasized opportunities for growth and access to the best properties across multiple basins.

The company has made significant progress with its operating partners as a superior capital provider for oil and gas asset co-development and has implemented a multi-pronged approach to capital allocation, including a share repurchase program, repurchasing debt securities at discounts, and increasing cash dividends for common stockholders.

The earnings conference call discussed the importance of scale in the oil drilling industry and how it affects operations, sourcing, and ancillary costs. Smaller private companies often struggle to borrow equipment and source materials on the spot, while larger companies have greater resources and financial backing. The call also touched on the benefits operators see in terms of tangible advantages, such as not having to put down deposits to secure supplies.

There was also a notable increase in the number of proposals, including those for well proposals, in the first quarter, with 200 gross proposals. A participant's question focused on cost inflation, particularly in the Bakken region, which the executives addressed by noting that they had budgeted for a cost inflation rate and acknowledged a steadier cost environment in the Permian region.

The company is optimistic about the levels of activity in the regions, expecting production to remain consistent to slightly higher in the coming quarter, with a significant increase in the third quarter due to the first wave of Mascot wells coming online. The company's service providers and operators remain confident in navigating challenges in the volatile industry, with a focus on steady growth in production and maintaining strong partnerships.

Final Analysis

Northern Oil and Gas has an impressive reach and core position for the size of the company. The company has a solid non-operating business model, and the scalability of the company should be incredibly attractive to investors. The method of non-operated acquisitions and disciplined capital allocation approach should also catch investors' eyes.

Lastly, investors should take note of the flexibility of the company - with around 100 different operating partners the company can be disciplined in who operates in what acreage, build or deplete reserves according to price swings, and is actively hedging commodities and deliverables in the futures market to mitigate any risk exposure to commodity price swings.

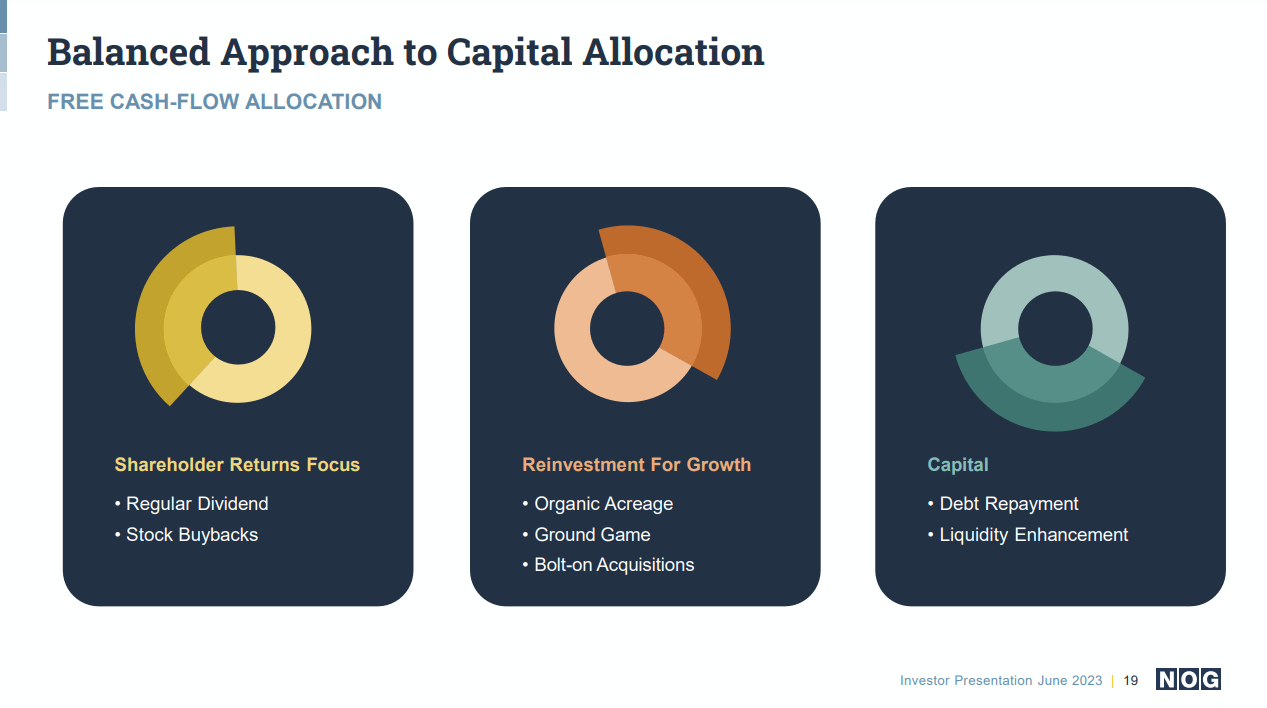

In the category of flexibility as well as their capital allocation:

{kind=link}

NOG has shown that not only does it have the ability to be very flexible with their capital, but they also have the wherewithal to actually implement and execute on their plans. They have shown the ability to strategically shift that capital between debt repayments, share buybacks, and capex to bring the maximum return to the company. This isn't something you see often in larger and more ponderous companies.

While investors should be extremely bullish about the company, Northern Oil and Gas is, however, a pure-play upstream company. Being a pure-play upstream company leaves the company susceptible to negative effects associated with drops in commodity prices.

With half of the information being spread on financial talk shows and financial news outlets indicating a recession is possible, investors should be aware of the risks in the company's business operations. In the event of a recession and the resulting global crude oil oversupply and weakened demand commodity prices would inevitably drop. And in the event of commodity price drops, there will inevitably be a slowdown in drilling activity and production - ultimately declining revenue for Northern Oil and Gas.

Overall, investors should strongly consider Northern Oil and Gas as the company's lean, disciplined, and flexible non-operating business model is incredibly solid. Northern's company structure is also very scalable, something that not a lot of oil and gas companies can boast.

With a healthy production mix between oil and gas and the company having core positions in the heart of the most prolific shale plays in North America, Northern Oil and Gas is well-positioned for future growth. While pure exposure to the upstream market does make for commodity price swing risks, the hedging strategy in the futures markets should mitigate any major concerns for investors.

Conclusion

Taking everything into account - their current portfolio designed around non-operating upstream interests, flexible capital spending strategy, strong commitment to return of value to shareholders, as well as a proven ability to acquire cash flow generating assets - I have to give Northern Oil and Gas a buy recommendation.

They are an excellent prospect for the dividend-focused investor looking to add upstream exposure in their portfolio.

About this article:

When I research stocks, I start with a "bird's eye view" of the target company. Many of the things I went through in this article are what I'll look at first.

When this bird's eye view is complete, I'll decide if I want to avoid the company for the time being or if it's a potential candidate for investment. This article that you are reading is the result of my bird's eye view examination.

It is designed to be an overall, high-level view of the company that you can read to determine if this company is something that you might consider as a candidate for investment. It is not possible to report everything about a company in the space of a single article, nor is it possible for me as an author to learn every detail about a company in the amount of time allotted to write an article.

You should not take my final conclusion on the company as your sole recommendation for investment, and you should conduct further in-depth research on your own to come to your final conclusions.

As a result of this, my "buy" recommendations come with an asterisk. And that asterisk is that this is only a high-level examination, and in-depth research that can take many hours, or days, of your time is still required. This is why my articles are short and to the point, with no fluff or filler. Just the facts that you need to know to move forward.

For further details see:

Northern Oil and Gas: Big Company Revenue, Small Company Flexibility