XLE - Northern Oil And Gas: Bigger Yield EPS Growth In '24 Monitoring The Chart

2024-01-19 14:47:51 ET

Summary

- Domestic oil prices have been volatile, but Northern Oil and Gas, Inc. remains undervalued with a high dividend yield.

- Northern Oil and Gas is the largest publicly traded non-operated E&P and has assets in North Dakota, Pennsylvania, and the Permian Basin.

- Despite a recent earnings miss, the company's EBITDA and dividend have increased, and analysts expect earnings and dividends to continue rising.

- I outline key price levels to watch ahead of Q4 results due out in February.

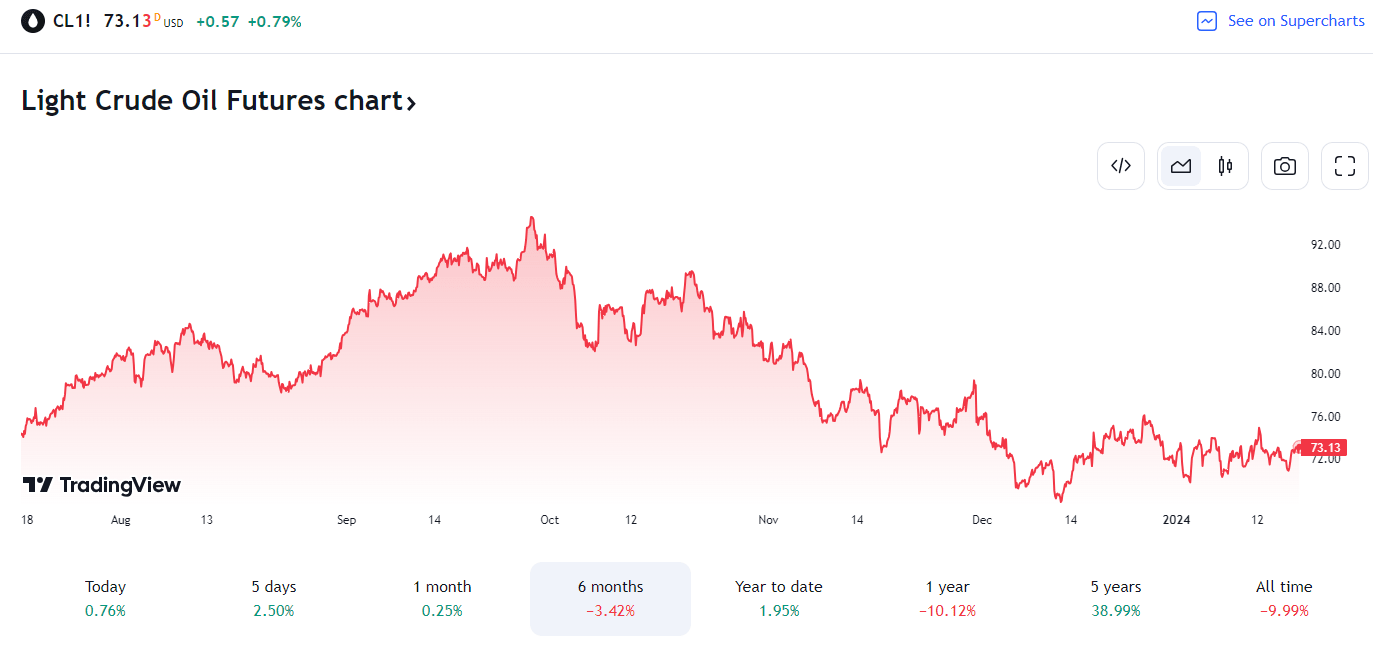

Domestic oil prices (CL1:COM) have been volatile over the past year. Recently, though, a trading range has developed between the upper $60s and mid-$70s. Amid geopolitical tensions in the Red Sea, disrupting the transportation of crude oil, WTI has been conspicuously quiet at significantly lower prices compared to what was seen in September and October.

Amid ebbing oil and gas prices, I reiterate my buy rating on Northern Oil and Gas, Inc. (NOG). I see this U.S.-based E&P name as undervalued, with a sustainable and high dividend yield.

WTI Crude Oil: Rangebound Around $70

{kind=link}

According to Bank of America Global Research, Northern Oil and Gas is the largest publicly traded non-operated E&P. Its net production reflects a broad array of working interests in a series of oil and gas properties where it partners with operators and takes a cut of well-level revenues for a proportional amount of capital operating costs. It has assets in North Dakota, Pennsylvania, and the Permian Basin.

The Minnesota-based $3.4 billion market cap Oil and Gas Exploration and Production industry company within the Energy sector trades at a low 4.9 forward non-GAAP price-to-earnings ratio and pays a high 4.7% dividend yield as of January 17, 2024. Ahead of earnings due out next month, shares trade with a moderate 35% implied volatility percentage, while short interest on the stock is high at 12.0%.

Back in November, NOG reported a disappointing set of quarterly results. Q3 non-GAAP EPS of $1.73 missed the Wall Street consensus forecast of $1.79 while GAAP EPS verified at just $0.27, a sharp $1.47 shortfall compared to estimates. Its oil and gas sales summed to $512 million, a 4% decline from year-ago levels, though that was a modest beat. On the plus side, the management team reported record quarterly oil production of more than 102,000 Boe per day.

The firm’s EBITDA was actually healthy at $386 million as a result of the hefty production volume and a new focus on the Permian after recent acquisitions . 2023 was updated to be in the $790 million to $820 million range. Also, sanguine was a 5% increase in its dividend, lifting the already-high yield. Still, analysts at BofA recently downgraded the domestic driller, citing geopolitical concerns and uncertain OPEC policy, leading to rangebound oil prices.

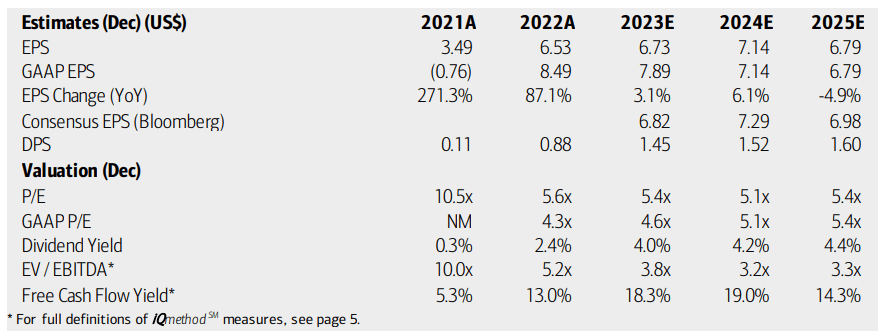

On valuation , analysts at BofA see earnings rising by 6% this year after just a 3% EPS increase in 2023. We will know the final numbers when the Q4 report is released next month ( expected February 23rd). Per-share profits are then expected to dip in 2025. The current consensus outlook, per Seeking Alpha, shows a similar earnings growth trajectory.

Dividends, meanwhile, are expected to continue rising, and I would point out that the higher payout is backed up by a remarkably high free cash flow yield that should sustain even if oil holds in the $70s. With a forward earnings multiple in the mid-single digits and an EV/EBITDA ratio that’s about one-third that of the S&P 500 (SP500), the value case remains strong.

NOG: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

{kind=link}

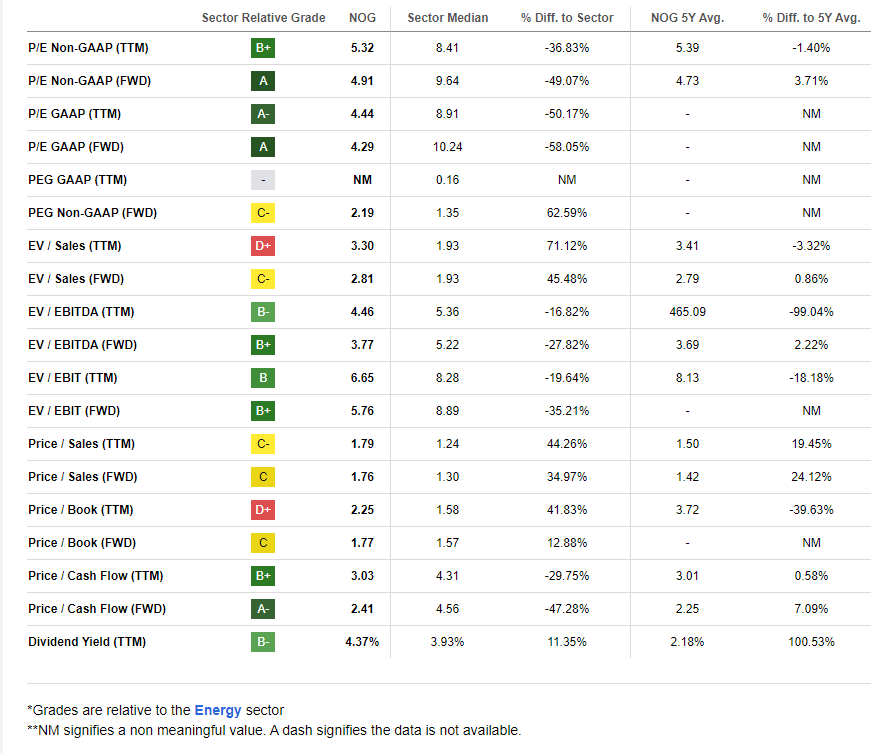

If we assume normalized forward operating EPS near $7.20 and apply an earnings multiple of 6, between the sector median and the company’s 5-year average, then the stock should trade near $43. I assert a higher P/E is warranted due to the firm’s impressive free cash flow ("FCF") and depressed EV/EBITDA multiple.

NOG: A Very Low Valuation

{kind=link}

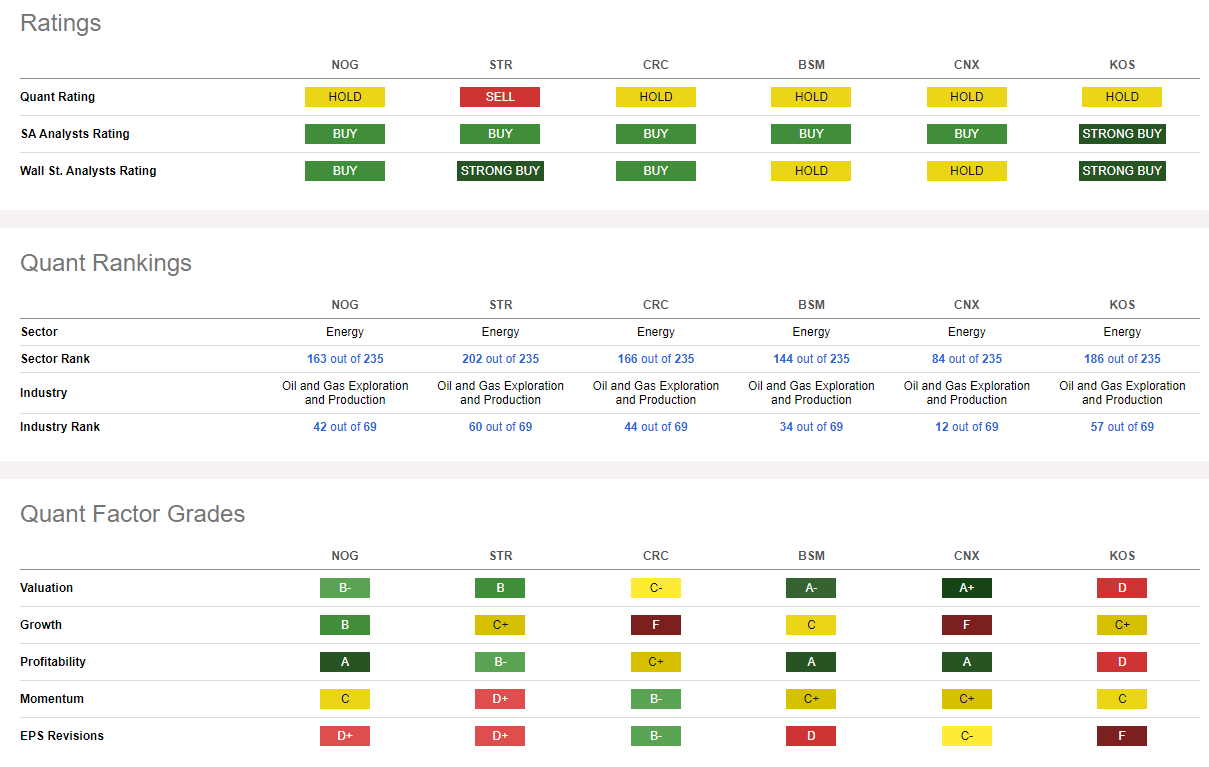

Compared to its peers , NOG sports a favorable valuation rating with an above-average growth outlook. Profitability trends continue to look strong, despite the recent hiccup in share-price momentum – I will detail key price levels to watch later in the article. Underscored by the recent BofA downgrade and after the EPS miss, there have been more EPS downgrades than upgrades lately.

Competitor Analysis

{kind=link}

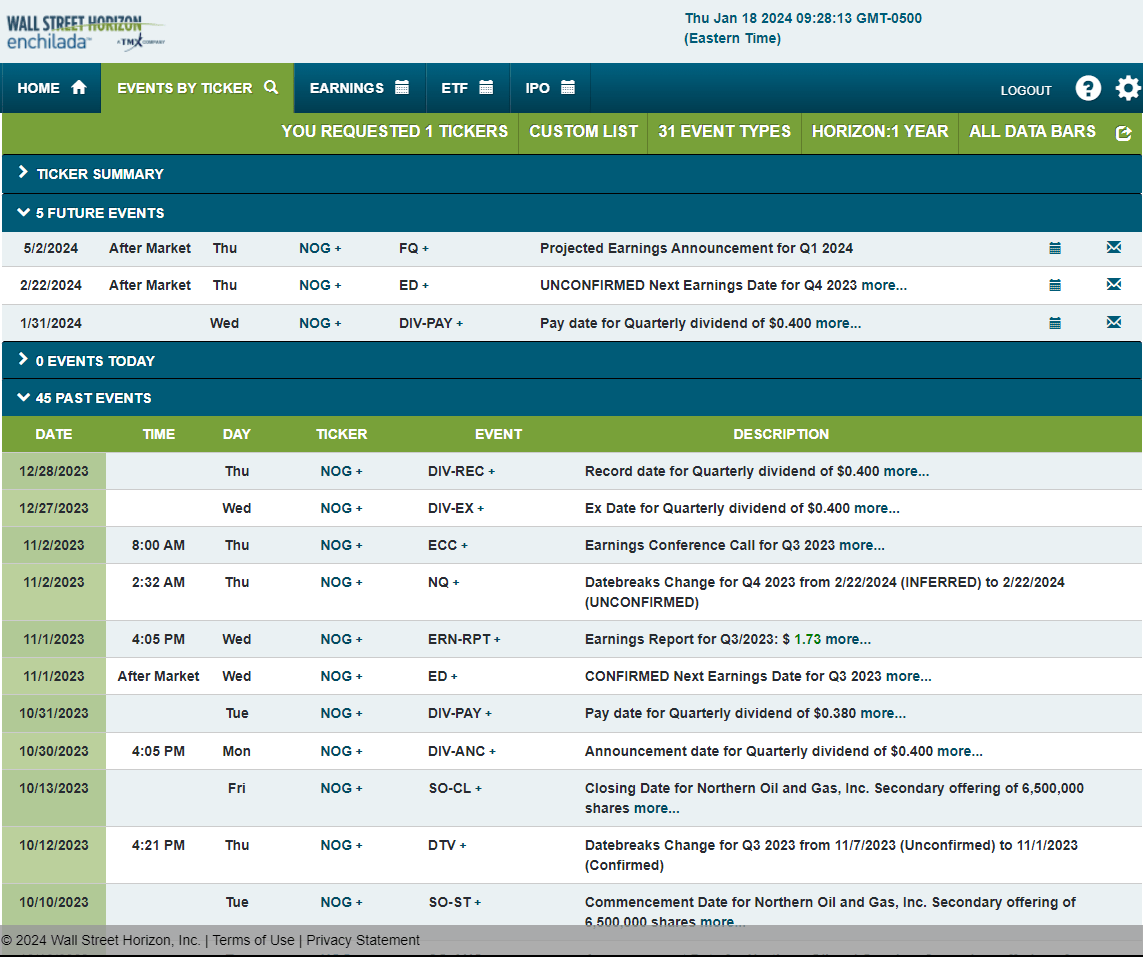

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4, 2023 earnings date of Thursday, February 22 AMC. The stock has a dividend pay date on Wednesday, January 31. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

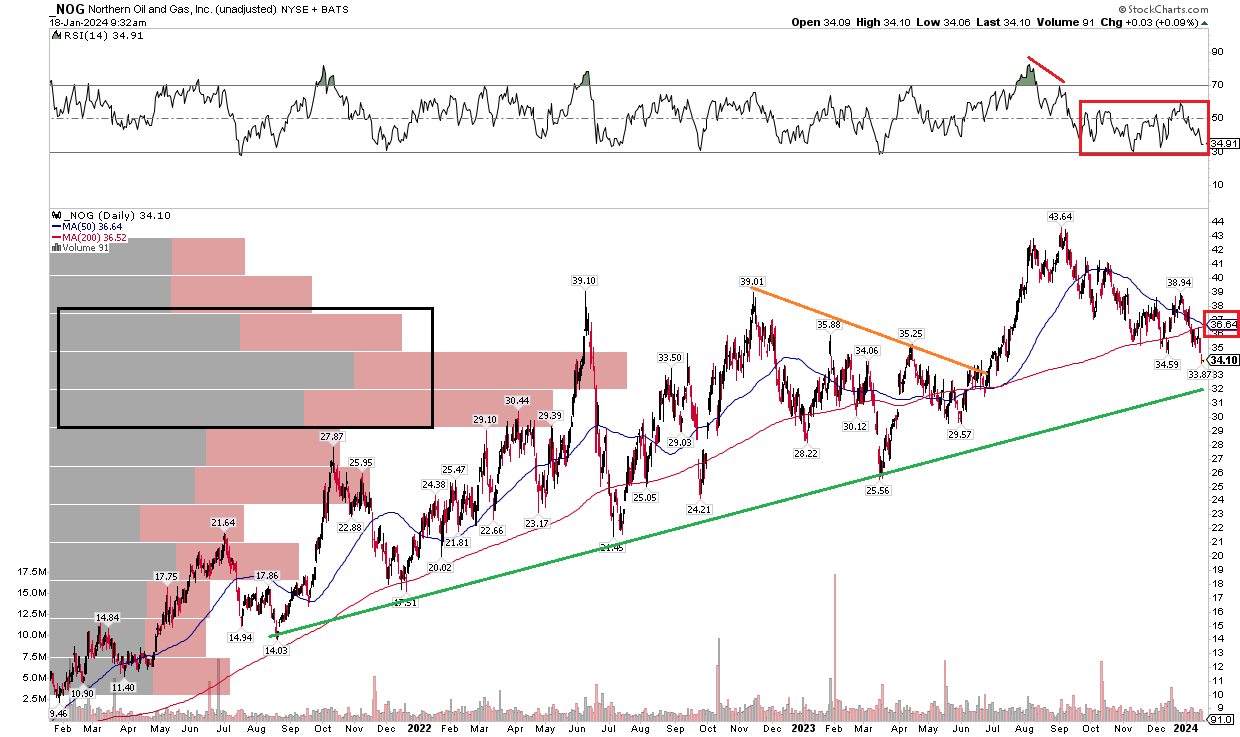

With an attractive valuation amid a troubled oil market, Northern Oil and Gas has a generally positive chart. Shares remain in a solid uptrend that dates back years, and key support is seen in the low $30s. Moreover, the breakout point from the middle of last year is also in that range, making this current pullback to support all the more critical for the bulls to defend. What is a concern in my technical eye is a weak trend in the RSI momentum oscillator at the top of the chart – it's ranging between 30 and 60, a notoriously bearish characteristic.

Still, there is an ample amount of shares traded down to about $29. That should result in some buying demand if we see the stock fall further. Another weak point is seen when analyzing NOG’s short-term 50-day moving average and its longer-term 200-day moving average. A death cross appears imminent, which suggests near-term momentum has turned softer. Nevertheless, zooming out is helpful in this case, and NOG’s uptrend is something that should be seen as a bullish sign. I see support at $32 and $29 while $44 is resistance.

Overall, buying the dip in NOG here appears as a favorable risk/reward play.

NOG: Broad Uptrend, But Near-Term RSI Concerns, Under 200dma

{kind=link}

The Bottom Line

I reiterate my buy rating on Northern Oil and Gas, Inc. shares. I see the stock as undervalued while the technical set-up, though mixed, suggests a long-term uptrend is in place ahead of earnings next month.

For further details see:

Northern Oil And Gas: Bigger Yield, EPS Growth In '24, Monitoring The Chart