NESRF - Northern Star Resources: Limited Margin Of Safety At Current Levels

2024-01-04 07:51:05 ET

Summary

- Northern Star had a softer fiscal Q1 2024 report due to planned maintenance and lower grades/recoveries at KCGM but remains on track to deliver into FY2024 guidance.

- On a positive note, we should see margin improvement sequentially and year-over-year as the year progresses, with a stronger gold price and higher grade feed from Golden Pike North (KCGM).

- In this update we'll dig into the fiscal Q1 2024 results, recent developments, and where the stock's updated buy zone lies.

Northern Star Resources (NESRF) has been one of the best-performing miners over the past eighteen months since I highlighted the stock as attractive below US$5.60 in mid-2022 , with the stock gaining over 65% vs. a ~15% gain for the Gold Miners Index (GDX). This outperformance can be attributed to its aggressive buyback program and robust forward outlook with the company green-lighting its KCGM Mill Expansion (19% IRR at a conservative ~$1,700/oz gold price assumption). Notably, the company has also made significant progress at its Thunderbox and Pogo mines, delivering at/above nameplate capacity from a milling standpoint following plant expansions at both assets. In this update we'll dig into the fiscal Q1 2024 results, recent developments, and where the stock's updated buy zone lies:

KCGM Super Pit - Company Website

{kind=link}

All figures are in United States Dollars at a 0.65 AUD/USD rate unless otherwise noted with an A$ in front of the dollar figure.

Q3 Production & Sales

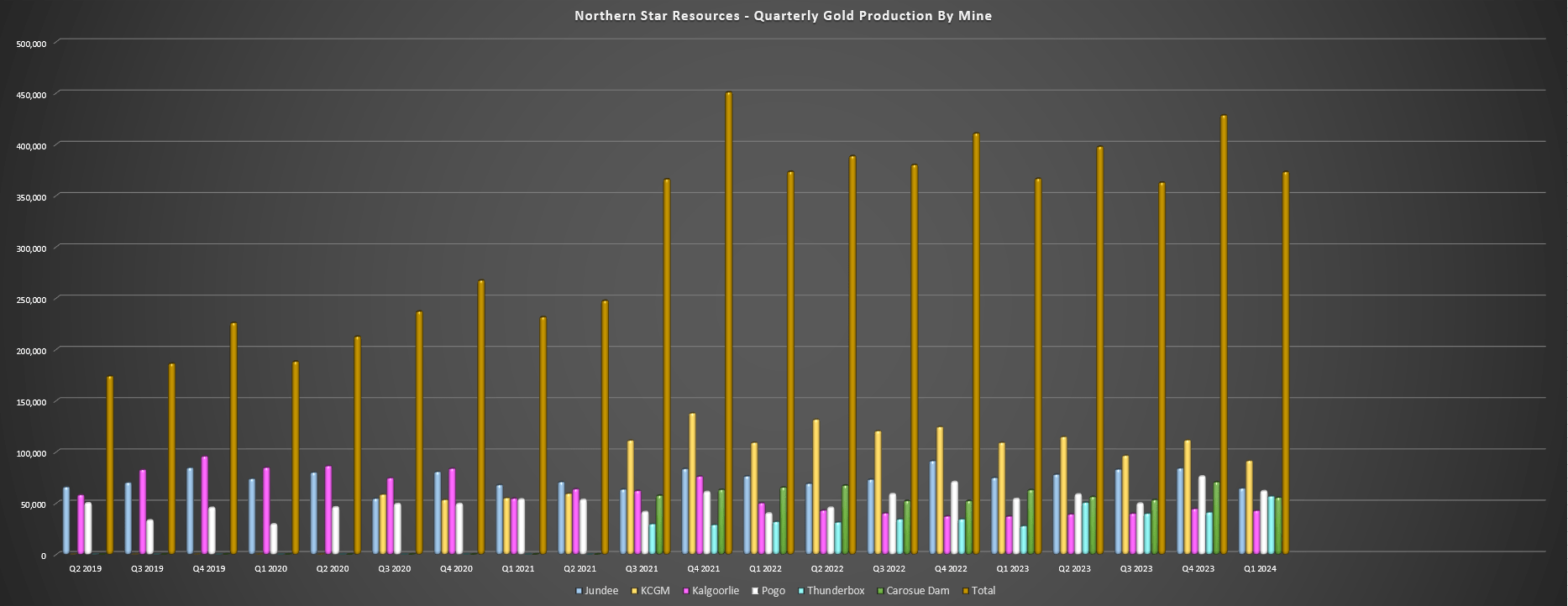

Northern Star Resources ("Northern Star") released its fiscal Q1 2024 results in mid-October, reporting quarterly production of ~373,300 ounces of gold, a 2% increase from the year-ago period. The solid performance was despite lower grades and recoveries at its flagship KCGM Mine in Western Australia, lower production at Jundee with an unplanned crushing circuit event (since resolved), and less access to high-grade areas at Carosue Dam which affected production levels here as well. This was helped by the company's Thunderbox/Bronzewing Operations (part of its Yandal Production Center) putting up a strong quarter with production of ~56,900 ounces (Q1 2023: ~27,900 ounces), driven by significantly higher throughput following its plant expansion, and slightly higher head grades in the period (1.5 grams per tonne of gold vs. 1.4 grams per tonne of gold).

Northern Star - Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

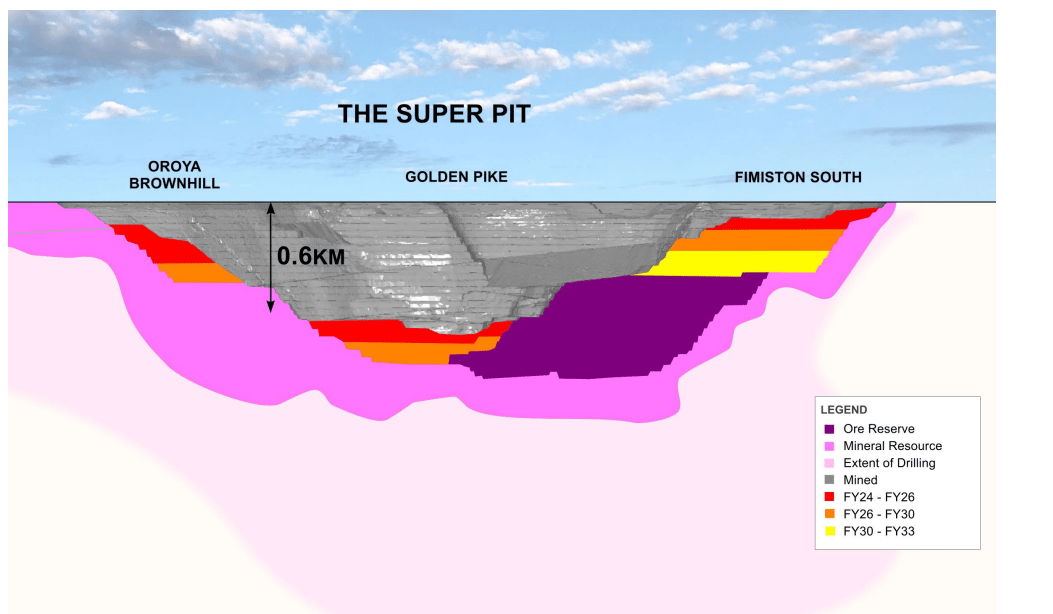

Digging into the operations a little closer, KCGM produced ~91,500 ounces (Q1 2023: ~109,200 ounces) which translated to a 16% decline year-over-year, affected by lower recoveries (one-off event according to the company) and lower throughput (~2.92 million tonnes vs. ~3.23 million tonnes). However, underground ore mined increased materially to ~519,400 tonnes (+32% year-over-year, offset by less access to high-grade areas at Mt. Charlotte), and the company continues to make solid progress on the Super Pit's East Wall remediation which is expected to be completed by year-end. Importantly, this will provide access to high-grade ounces from Golden Pike North (~1.2 million ounces at 1.8 grams per tonne of gold), with grades here more than 30% above KCGM's average reserve grade of ~1.3 grams per tonne of gold.

KCGM Super Pit - Company Website

{kind=link}

Moving over to the company's Carosue Dam Mine, we saw lower throughput at lower grades (~964,000 tonnes at 1.9 grams per tonne of gold) with reduced access to high-grade areas with lower grades from Kirari Underground and a mill shut that impacted mill throughput in the period. On a positive note, high-grade feed will ramp up from the Porphyry Underground at Carosue Dam where production has begun, and although KCGM had a soft Q1, we will see a better Q2 with improved recovery rates and higher throughput following major planned maintenance completed in the quarter. Finally, while production is up year-over-year at its Kalgoorlie Operations (~42,800 ounces vs. ~37,300 ounces), this wasn't enough to offset lower output at Carosue Dam and KCGM, which resulted in ~183,000 ounces sold at costs of A$1,844/oz vs. ~215,000 ounces at costs of A$1,762/oz from its Kalgoorlie Production Center in the year-ago period.

Looking at the company's Yandal Operations, Jundee had a tougher quarter with production down 14% year-over-year to ~64,600 ounces related to lower throughput and lower grades in the period. This was attributed to lower grades in line with mine sequencing and the unplanned crushing circuit event that led to twelve days of downtime and resulted in the production of high-grade ounces being pushed into fiscal Q2 2024. Fortunately, Thunderbox/Bronzewing had a massive quarter with ~1.37 million tonnes processed despite a planned mill shut (~501,000 tonnes in August which is in line with ~6.0 million tonne per annum nameplate capacity), and this helped its Yandal Center to enjoy higher sales year-over-year with ~124,600 ounces sold at A$1,949/oz costs vs. ~102,600 ounces at A$1,584/oz in the year-ago period. And while costs were higher, this was largely related to increased sustaining capital (A$39 million vs. A$25 million).

Pogo Mine Quarterly Production & AISC - Company Filings, Author's Chart

{kind=link}

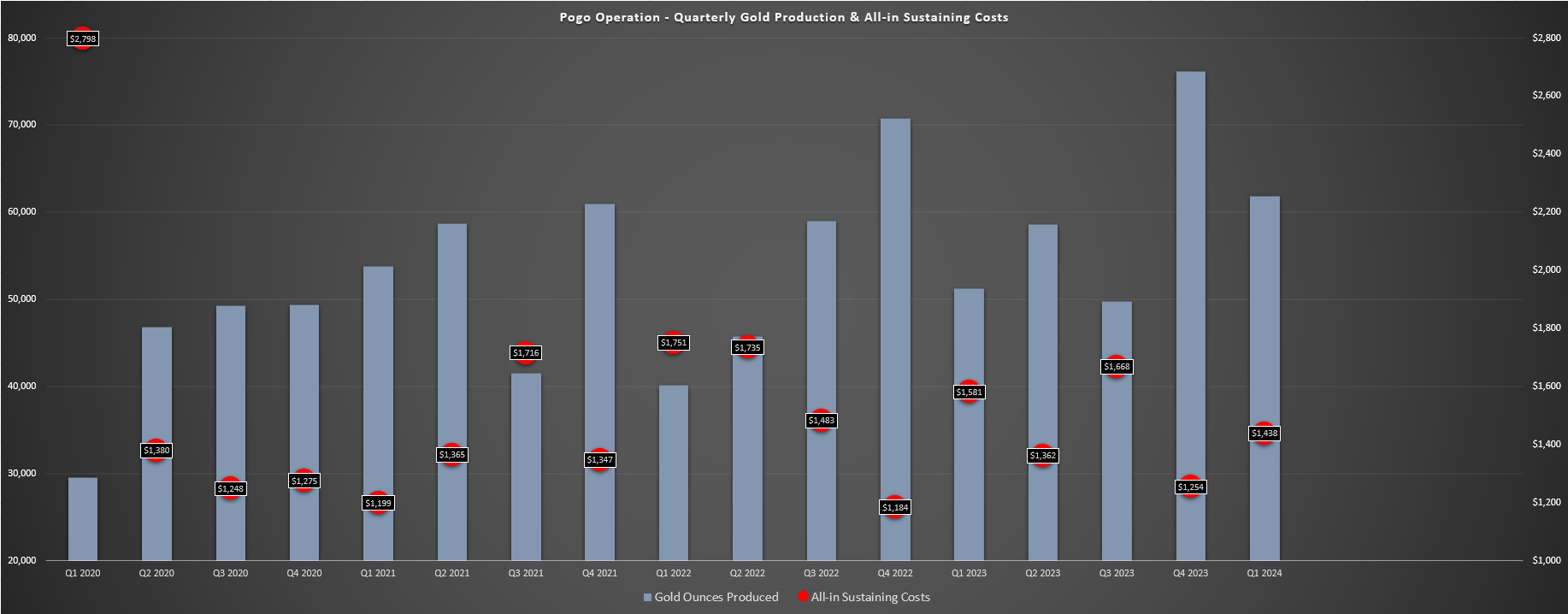

Last but not least, the company's Pogo Mine in Alaska had a better quarter year-over-year with ~61,600 ounces produced at all-in sustaining costs of $1,438/oz vs. ~54,300 ounces produced at costs of $1,581/oz. The higher production was thanks to higher throughput rates (~326,300 tonnes milled) at higher grades of 6.9 grams per tonne of gold (Q1 2023: 6.1 grams per tonne of gold), with the solid throughput rates just shy of nameplate (~1.3 million tonnes per annum) despite planned a major planned mill shut. Meanwhile, mine development continues to improve with an average monthly rate of 1,851 meters from five jumbos, improving from 1,562 meters in the year-ago period. This solid performance despite grades well below reserve grades (stope ore represented just 67% of total ore) allowed the operation to generate a net mine cash flow of A$25 million, up from [-] A$15 million in Q1 2023.

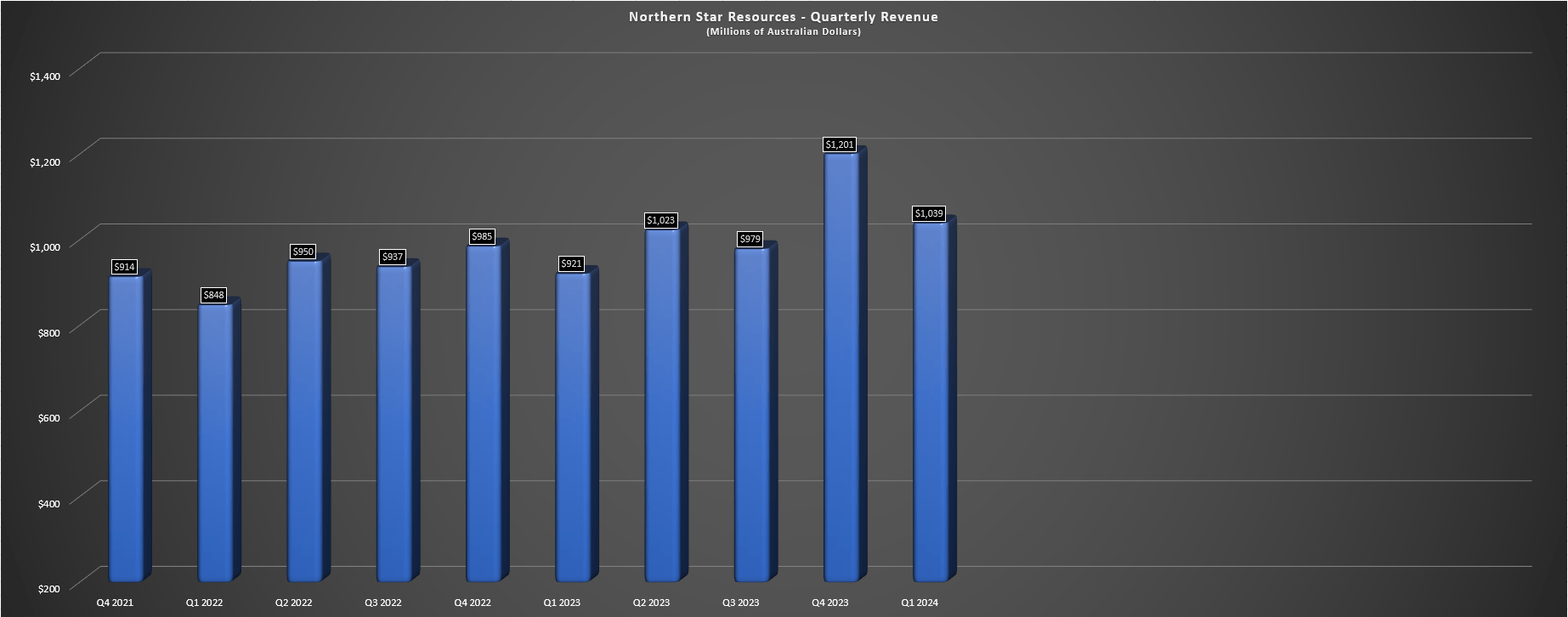

Northern Star Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

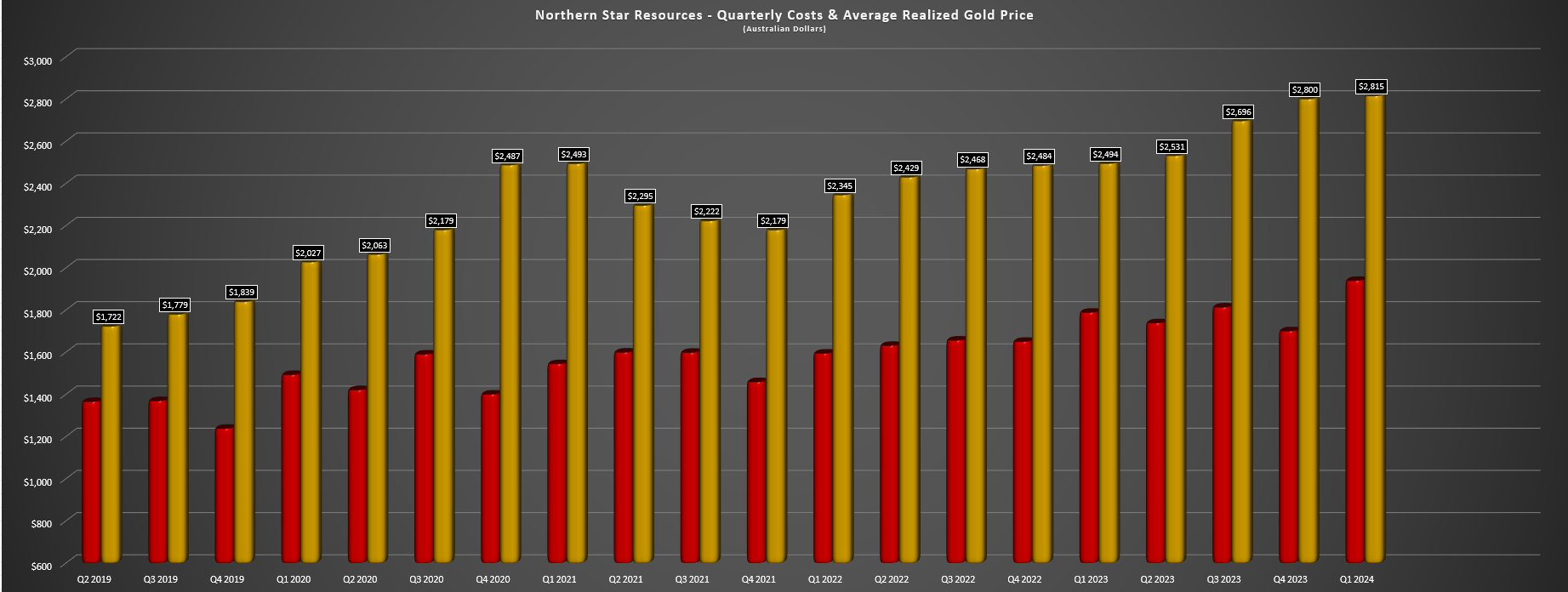

Unfortunately, while this was a decent start to what will be a second-half weighted year (FY2024 guidance of ~1.67 million ounces at mid-point), revenue was up only 13% due to continued delivery into hedges. This resulted in an average realized gold price of just A$2,815/oz [US$1,830/oz] which was well below the sector average of ~US$1,920/oz, and Northern Star added 330,000 ounces of hedges in the period at ~US$2,150/oz. The increase in hedges has increased its hedge position to ~1.68 million ounces at ~US$1,900/oz over the forward four-year period, amounting to over 20% of total production. Overall, I don't mind the hedging strategy given the significant growth capital related to its KCGM Mill Expansion (13 million to 27 million tonnes per annum), which will ultimately make this a top-5 gold by the end of the decade with production of ~900,000 ounces per year, similar to what Agnico Eagle ( AEM ) is targeting from Detour Lake/Canadian Malartic once optimized.

Costs & Margins

Moving over to costs and margins, Northern Star's performance was a little weaker than I expected with all-in sustaining costs of A$1,939/oz [US$1,260/oz] vs. A$1,788/oz [US$1,162/oz] in the year-ago period. However, most producers in the sector have continued to be impacted by inflationary pressures, there continues to be a shortage of skilled labor in Western Australia which is affecting labor costs, and sustaining capital was slightly higher in the period at A$87 million. On a positive note, Northern Star is aiming for costs of A$1,760/oz at the mid-point in FY2024 or ~US$1,150/oz and these costs are in line with its million-ounce producer peer group with room to improve over the long term. This is because the company is aiming to bring costs below US$1,100/oz at Pogo longer-term (currently dragging up its overall costs), and pulling costs at KCGM closer to US$1,000/oz with a much higher denominator.

Northern Star Quarterly AISC & Realized Gold Price - Company Filings, Author's Chart

{kind=link}

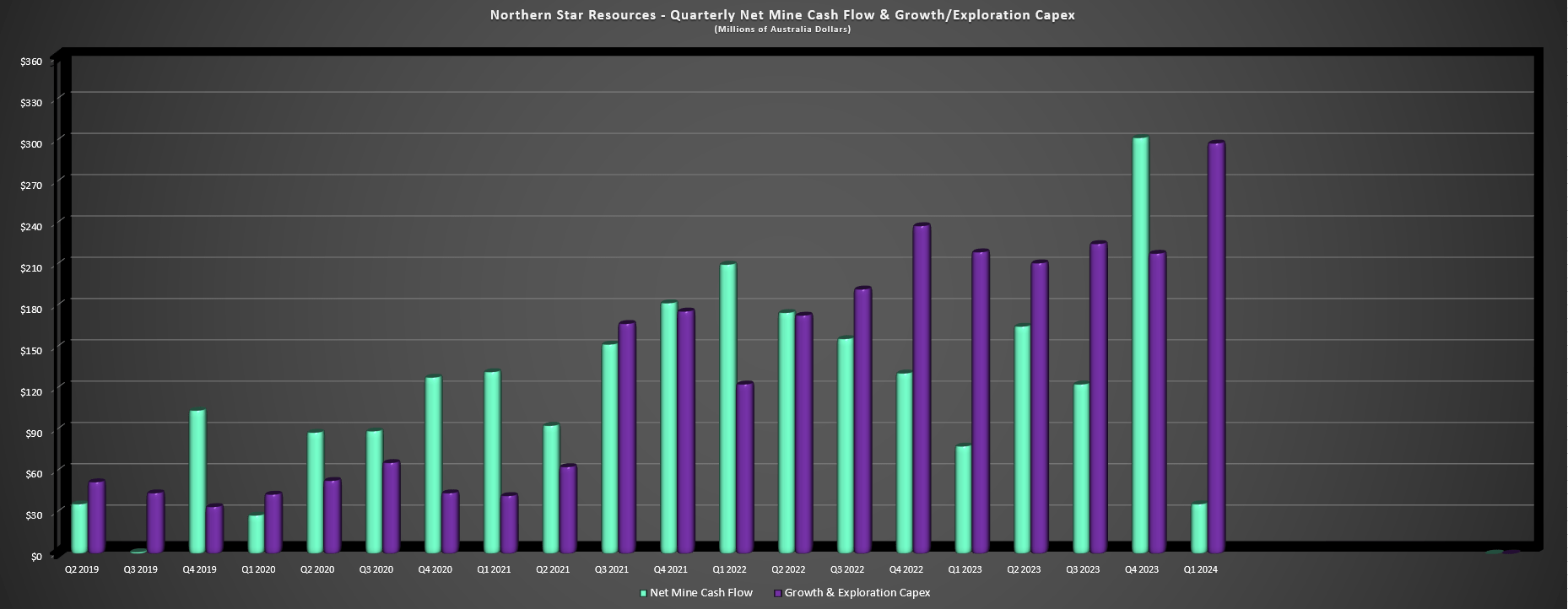

Looking at the company's margin performance, AISC margins improved to A$876/oz, a significant increase from A$706/oz in the year-ago period. This was entirely driven by the higher realized gold price in the period, and Northern Star should see margin improvement in fiscal Q2 with a stronger gold price and lower costs across its portfolio following a busy quarter of maintenance in fiscal Q1 2024. However, despite the higher costs in the period, Northern Star still generated A$36 million in net mine cash flow after A$219 million in growth capital spend (mostly related to KCGM), and ended the quarter with A$185 million in net cash. Meanwhile, its liquidity position sits at A$2.0+ billion, giving it lots of flexibility to complete major growth at KCGM which was estimated at A$1.5 billion mainly split over the next three years (FY2024 through FY2026).

Northern Star Net Mine Cash Flow & Growth/Exploration Capex - Company Filings, Author's Chart

{kind=link}

Recent Developments

As for recent developments, gold price strength has continued since the end of fiscal Q1 2024, pointing to likely margin improvement both sequentially and year-over-year. In fact, the gold price has spent a record six weeks above the pivotal $2,000/oz level, closed at a new all-time yearly high for 2023, and it appears that prior resistance at $1,800/oz to $1,850/oz has now become new support, with this being near the floor for the metal last year. Overall, this is a very positive development for the sector and certainly Northern Star, and should contribute to stronger cash flow generation despite headwinds from the competitive labor market in Western Australia where the company produces most of its gold.

{kind=link}

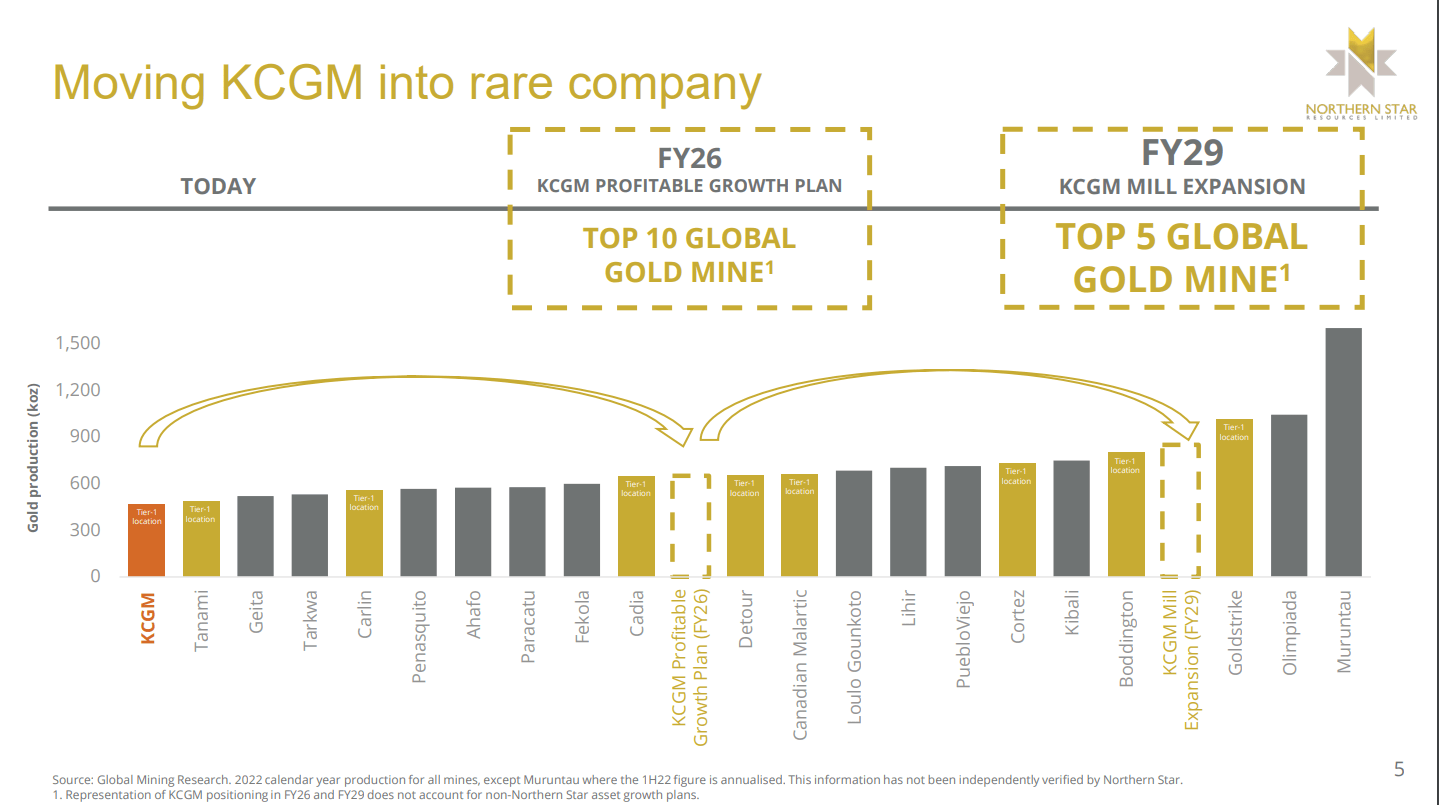

As for share buybacks and M&A, the company took advantage of prices below US$8.00 to buy back additional shares in the period and noted that it will continue to be opportunistic when it comes to share repurchases. As for M&A, Northern Star shared that the assets that may be divested as part of the Newcrest deal were the same ones that the suitor also likes, suggesting a low likelihood of scooping up an asset as part of what's likely to portfolio optimization by the world's largest gold producer. Meanwhile, the company noted that it's focused on the "value it can get out of its current portfolio" without worrying about external opportunities, which makes sense given the significant lift in production expected from KCGM that will turn this into a world-class asset, well ahead of Cadia, Fekola, and Paracatu for annual production by FY2027.

KCGM Mill Expansion vs. Other Major Gold Assets - Company Website

{kind=link}

Valuation

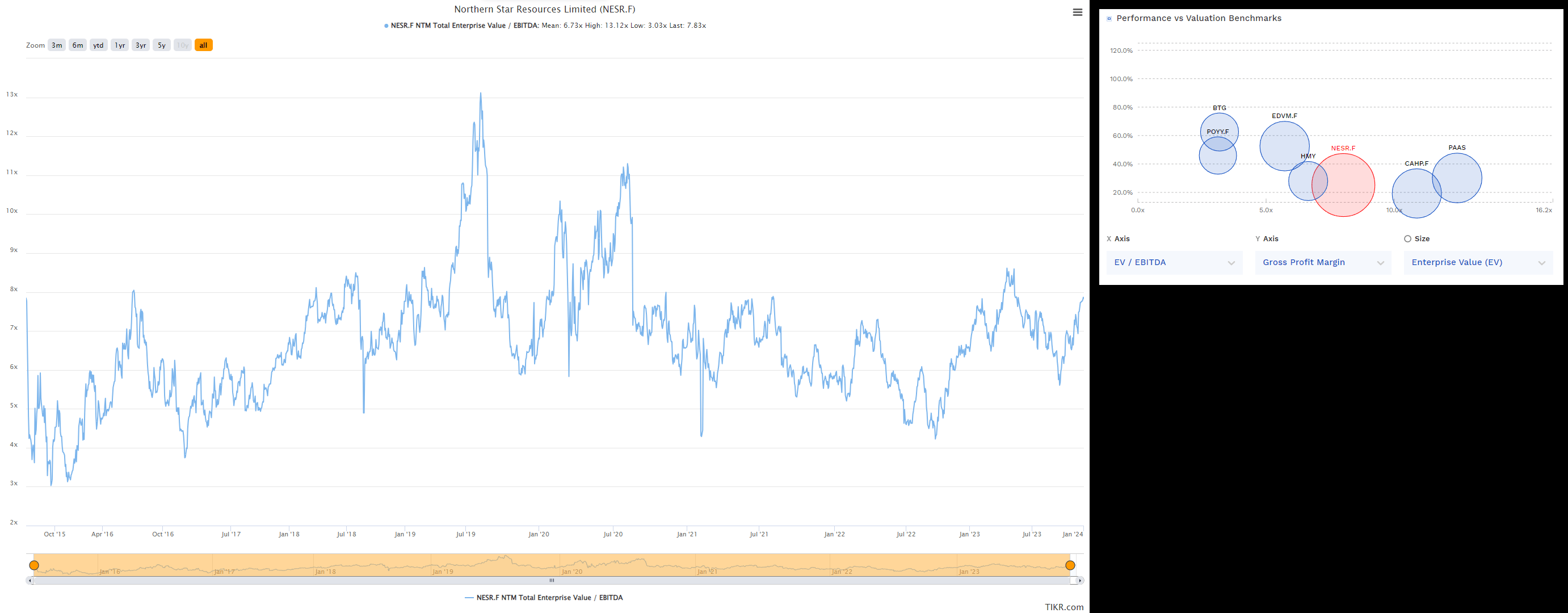

Based on ~1,160 million shares and a share price of US$9.20, Northern Star trades at a market cap of ~$10.7 billion and an enterprise value of ~$10.6 billion, making it the highest capitalization producer in the 1.0 million to 2.0 million ounce producer space. The company also trades at one of the higher multiples sector-wide, valued at ~$525/oz on gold reserves and ~8.0x forward EV/EBITDA, a similar valuation to Agnico Eagle which is a larger, more diversified, and higher-margin gold producer with over 10 mines across multiple jurisdictions. Finally, Northern Star continues to trade at a premium on a P/NAV basis, sitting at ~1.14x P/NAV vs. an estimated net asset value of ~$9.4 billion. This premium to its peer group is partially justified by its solely Tier-1 jurisdictional profile and solid forward outlook with its gold production set to increase meaningfully at KCGM later this decade.

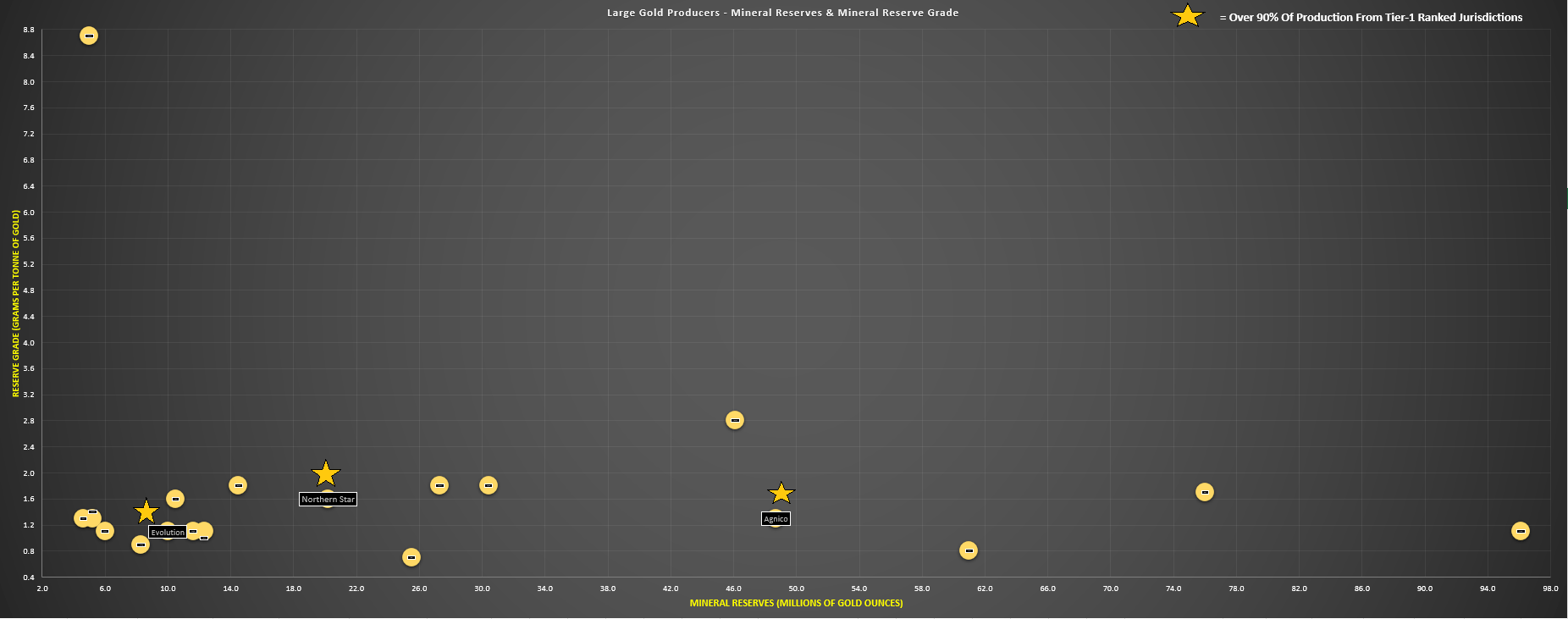

Northern Star Enterprise Value, Margins, EV/EBITDA Multiple vs. Peers - FinBox, TIKR Producers With Over 90% Of Production From Tier-1 Jurisdictions (Reserves/Reserve Grade) - Company Filings, Author's Chart

{kind=link}

{kind=link}

Looking at Northern Star's current forward EV/EBITDA multiple of ~8.0x, we can see that this is a premium to its average multiple of ~6.7x since the end of the secular bear market in gold in 2015, and its highest EV/EBITDA multiple since the stock's peak in April 2023. And while this premium valuation doesn't mean that the stock can't continue to march higher, I prefer to buy at a deep discount to fair value for cyclical stocks or pass entirely. And even using what I believe to be fair multiples of 10.0x cash flow and 1.25x P/NAV and a 65/35 weighting (P/NAV vs. P/CF), I see a fair value for Northern Star of US$10.50 and an ideal buy zone of US$7.40 or lower (given that I require a minimum 30% discount to fair value to justify starting new positions in Tier-1 jurisdiction producers). Hence, although Northern Star may benefit from a higher gold price, I don't see nearly enough margin of safety to pay up for the stock at current levels.

Obviously, waiting for a pullback of this magnitude may be an opportunity cost, and there's no guarantee that the stock will pull back to provide an entry below its 200-day moving average. That said, there are several other bets that are more attractive from a relative value standpoint elsewhere in the market, with one being Argonaut Gold ( ARNGF ), a Tier-1 jurisdiction producer (currently in the process of divesting Tier-2 assets), trading at ~0.40x P/NAV and less than 2x FY2024 P/CF estimates with its core operations in Canada/Nevada. Therefore, if I were looking to put capital to work in the sector, I see this as a more attractive reward/risk opportunity, especially with the stock being one of the most out-of-favor names in the sector today.

Summary

Northern Star reiterated that it's on track to deliver annual guidance of 1.6 to 1.75 million ounces after a slow start to the year (mostly related to planned mill shuts, lower recoveries at KCGM, and a crushing circuit event + mine sequencing at Jundee), and has pulled its costs well below the industry average with successful plant expansions at Pogo and Thunderbox. Meanwhile, the company has a much better fiscal Q2 and H2 2024 on deck as it benefits from better grades from Golden Pike North. That said, the stock has had a strong run relative to peers and I don't see nearly enough margin of safety at US$9.20. So, while I see Northern Star as a top-10 producer given its superior jurisdictional profile and portfolio of strong assets, I continue to see more attractive bets elsewhere in the sector, like Argonaut Gold.

For further details see:

Northern Star Resources: Limited Margin Of Safety At Current Levels