NESRF - Northern Star Resources: Solid Reserve Replacement In FY2023

2023-09-16 06:26:48 ET

Summary

- Northern Star finished the year with ~20.2 million ounces of gold reserves and ~57.4 million ounces of resources, with resource growth offsetting its slight decline in reserves.

- Importantly, the company maintained its conservative metals price assumptions to calculate resources and reserves and added ounces at KCGM, a key pillar for future growth.

- In this update, we'll dig into the FY2023 Reserve/Resource update and see whether the stock is offering an adequate margin of safety to place it in a low-risk buy zone.

Just over two months ago, I wrote on Northern Star Resources (NESRF), noting that while the company had a solid FY2023 (despite its slight miss on its guidance mid-point), there wasn't nearly enough of a margin to justify paying over US$8.20 for the stock. Since then, the gold price has mostly treaded water, but the stock has been hit quite hard, suffering an 18% drawdown at its August lows, slightly underperforming the Gold Miners Index (GDX) from a drawdown standpoint. I would attribute this underperformance to some mean reversion following outperformance relative to its million-ounce producer peers since its September 2022 lows, with Northern Star up ~60%, outperforming nearly all of its peers except for Evolution Mining (CAHPF) which remains up over 100% from its 2022 lows.

In this update, we'll dig into the company's year-end reserve & resource update and whether the stock's relative value has improved following its sharp correction.

{kind=link}

All figures are in United States Dollars unless otherwise noted at an exchange rate of 0.65 AUD/USD.

Gold Reserves & Resources

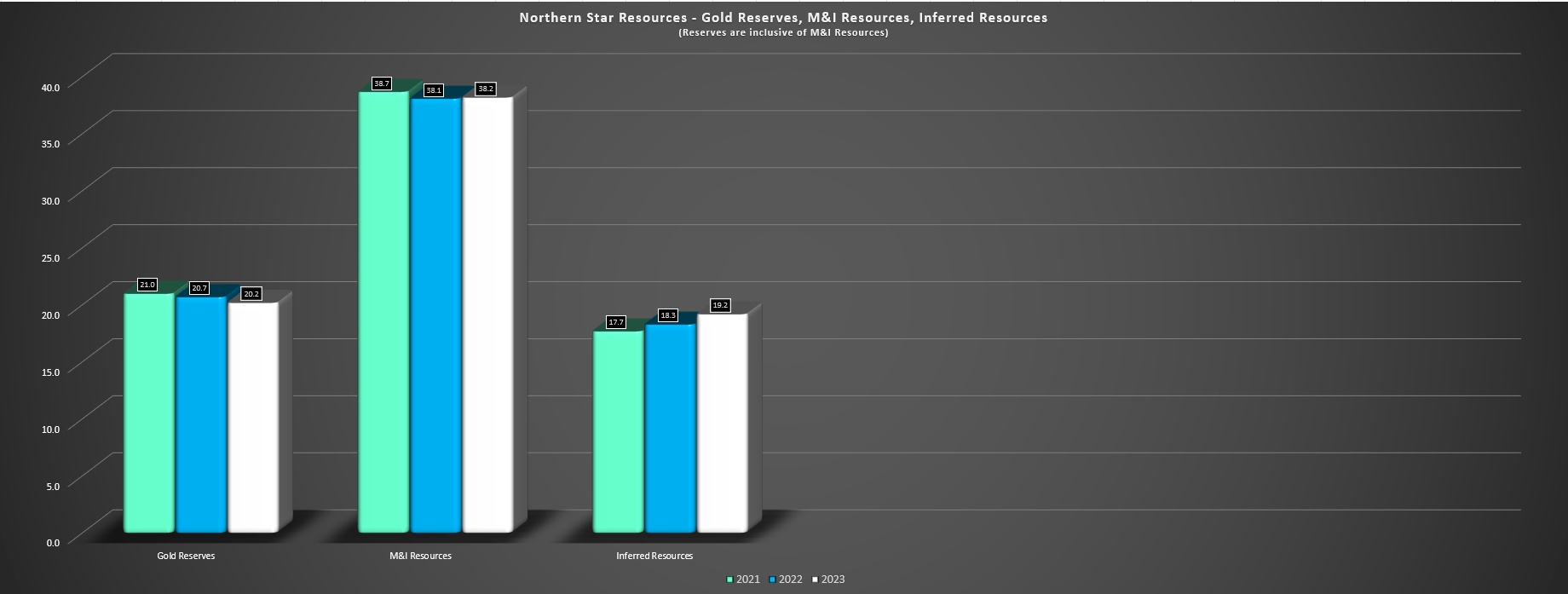

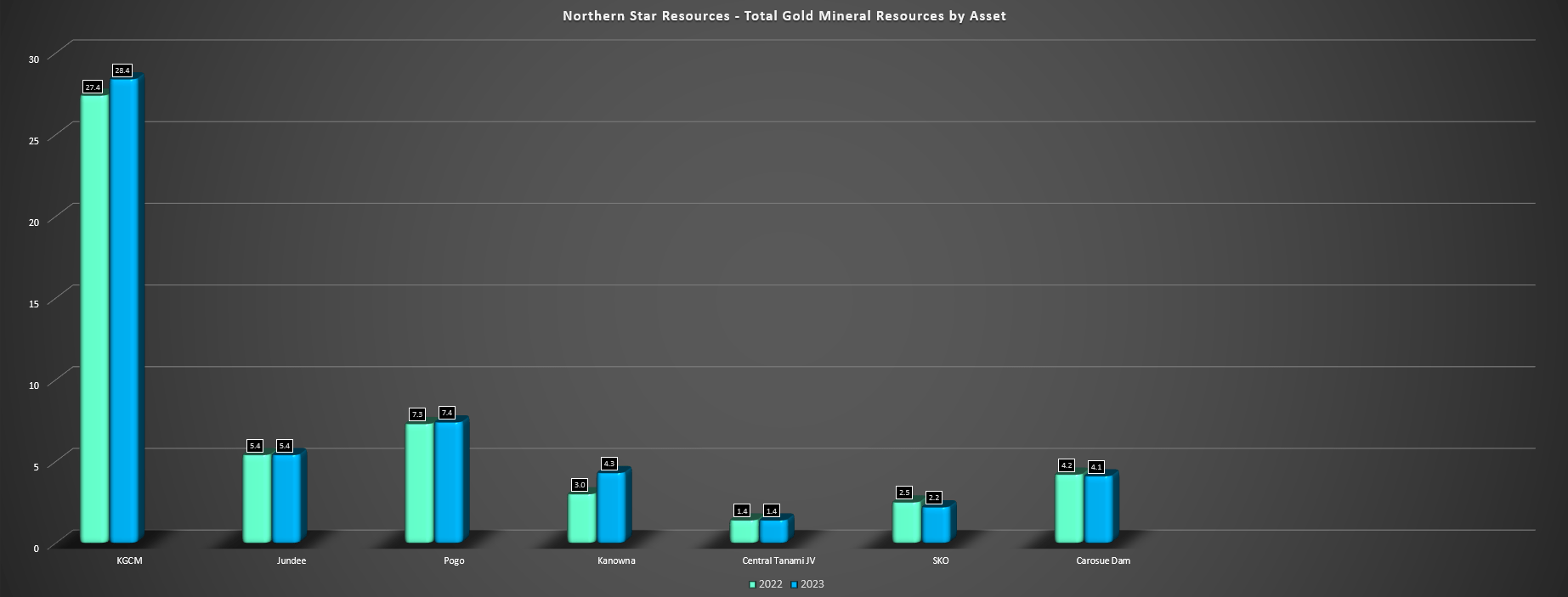

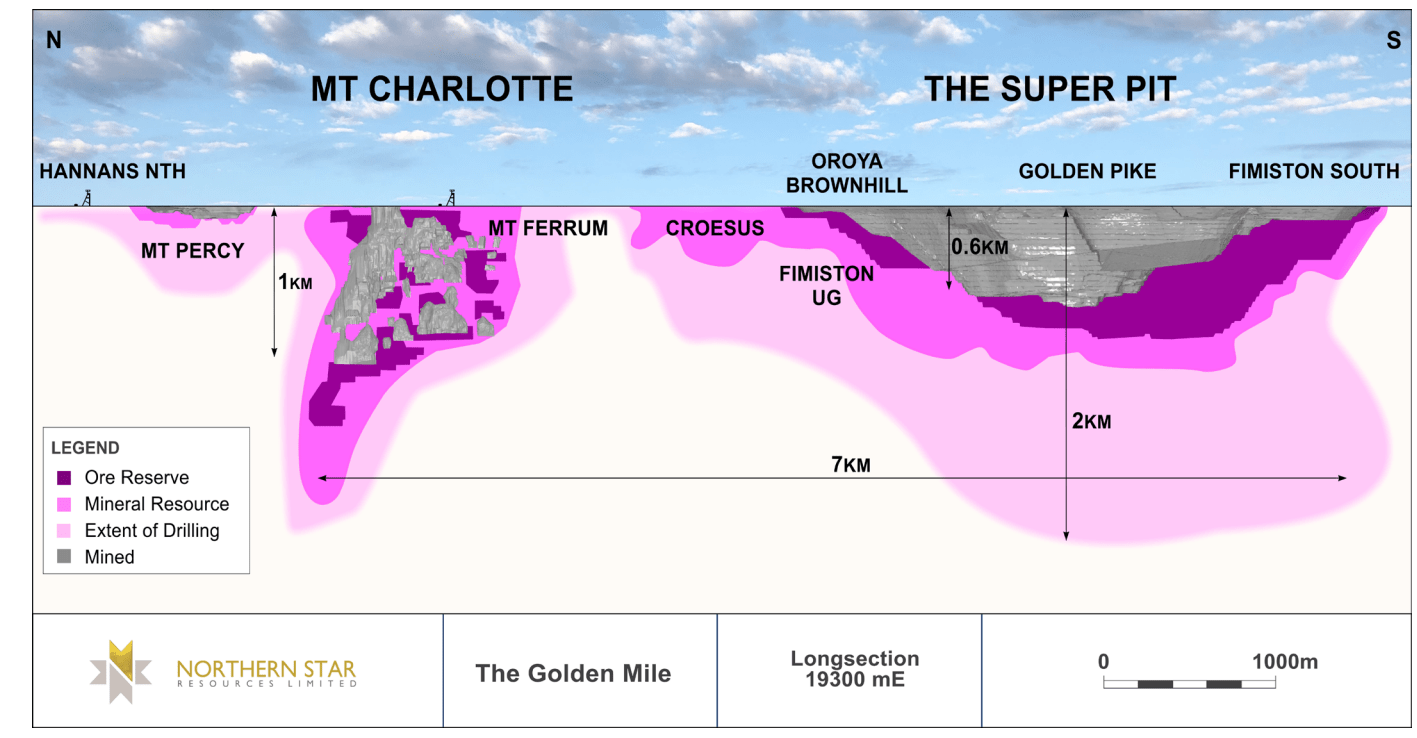

Northern Star Resources ("Northern Star") released its FY2023 Reserve & Resource statement last month, reporting total gold reserves of ~20.2 million ounces and total resources of ~57.4 million ounces (inclusive of reserves). This translated to a 2% decline in reserves from the year-ago period (~20.7 million ounces), offset by a 2% increase in total resources, with the bulk of resource growth coming from the inferred category. Meanwhile, at the company's flagship operation, KCGM, total resources increased by 1.0 million ounces to ~28.4 million ounces (~564 million tonnes at 1.6 grams per tonne of gold), supporting the recent decision to more than double annual processing throughput to 27 million tonnes per annum by FY2029 with the recently approved Fimiston Mill Expansion.

Northern Star Resources - Gold Reserves, M&I Resources, Inferred Resources - Company Filings, Author's Chart

{kind=link}

Digging into the company's gold reserves, M&I resources, and inferred resources closer, we can see that total reserves have declined moderately since FY2021, but this can partially be attributed to the divestment of non-core assets like Kundana and Paulsens and a moderate decline in reserves at its Jundee and Carosue Dam operations. Fortunately, this has been more than offset by reserve growth at Pogo (Alaska), KCGM, Thunderbox/Bronzewing, and South Kalgoorlie. However, as noted, resources were up year-over-year with growth at nearly all operations, with a maiden resource at Red Hill (large porphyry intrusion) leading to growth at Kanowna Belle and KCGM seeing resource growth from Mt. Charlotte and Fimiston North. The former has pushed Mt. Charlotte's resource base to an impressive ~3.5 million ounces (58 million tonnes at 1.9 grams per tonne of gold), with a reserve base of ~1.2 million ounces at 2.0 grams per tonne of gold at Mt. Charlotte.

{kind=link}

Looking at the progression in reserves asset by asset, we can see that Kanowna Belle has one of the smaller reserve bases at ~730,000 ounces, and declined from ~800,000 ounces in the year-ago period. However, we saw meaningful resource growth at this asset helped by exploration success at Joplin (300 meters from its underground infrastructure at Velvet) and, as noted previously, the company also announced a maiden resource of ~1.2 million ounces at Red Hill, a low-grade deposit amenable to bulk mining just 3.5 kilometers east of its Kanowna Belle Plant (22 kilometers from Fimiston). Highlight intercepts at this asset include 191.0 meters at 1.1 grams per tonne of gold, and 161.9 meters at 2.8 grams per tonne of gold. And elsewhere at South Kalgoorlie, reserves also declined year-over-year, but the company has made a discouraging discovery, Hercules, located 20 kilometers west of the HBJ deposit. It's still early days here, but results are solid with intercepts including 21 meters at 3.0 grams per tonne of gold and 16.7 meters at 3.6 grams per tonne of gold.

Northern Star - Total Mineral Resources by Asset - Company Filings, Author's Chart

{kind=link}

Moving over to Yandal, this is another relatively small reserve base (~3.8 million ounces combined at Jundee and Thunderbox), but there's reason to be optimistic here as well. For starters, the company increased its resource base at its Wonder Project to ~920,000 ounces at 2.9 grams per tonne of gold (25 kilometers south of the Thunderbox Plant), and Wonder West, North and Golden Wonder remain open at depth, with highlight intercepts of 17.7 meters at 3.3 grams per tonne of gold, 24.6 meters at 4.5 grams per tonne of gold, 16.7 meters at 3.6 grams per tonne of gold, and 14.7 meters at 4.7 grams per tonne of gold. In addition, Northern Star has intersected new mineralization on the Bannockburn Shear Zone (north of its Bannockburn Open Pit), suggesting the potential for reserve growth here as well southwest of Thunderbox.

{kind=link}

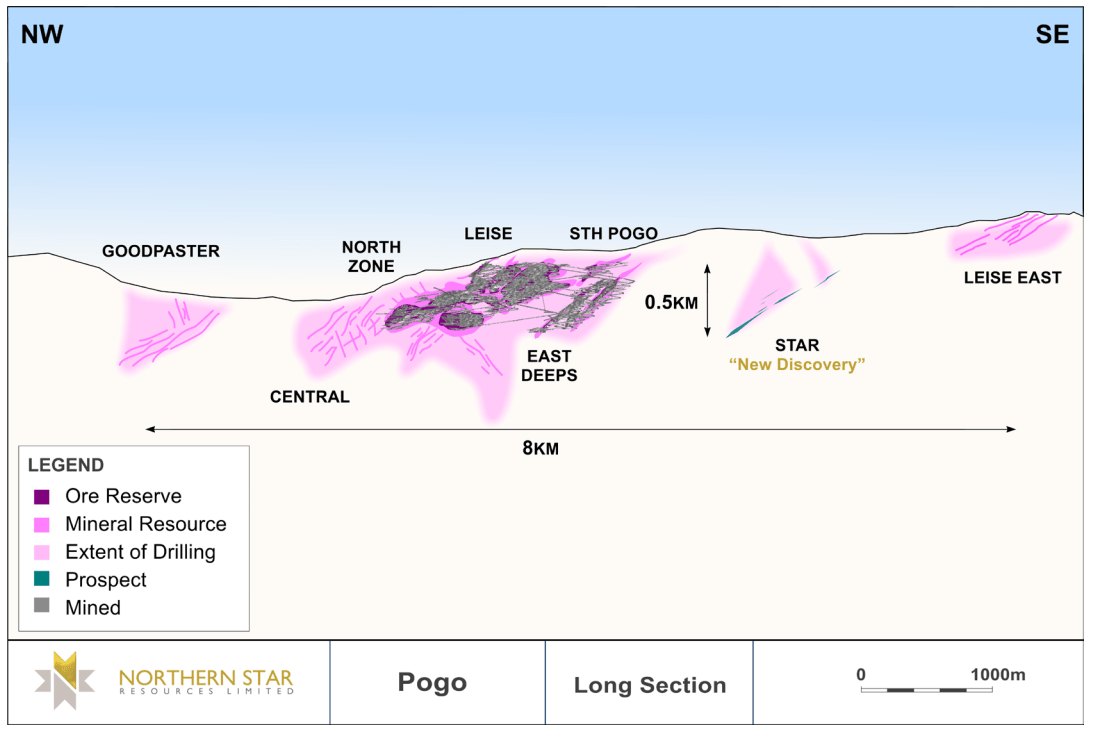

Finally, when it comes to Pogo, gold reserves fell to ~1.6 million ounces at slightly higher grades (8.6 grams per tonne of gold), and the ~6.6 million tonne reserve base might be a cause of concern to some, suggesting just a five-year mine life assuming a ~1.3 million tonne per annum throughput rate. However, it's important to note that this is a mine that had just ~5.1 million tonnes of reserves (~2.3 million ounces) at year-end 2010, and has enjoyed solid reserve replacement despite depletion of more than 2.5 million ounces. It's also worth noting that drilling at Pogo by impacted by labor availability, which slightly impacted resource and reserve growth in the period. Still, the company recently made a new discovery at Star (1.3 kilometers south of Pogo mine infrastructure), with the Star vein being taced over a 150 meter and 500 meter dip and open in all directions. Highlight intercepts include 4.9 meters at 15.8 grams per tonne of gold, 6.9 meters at 13.2 grams per tonne of gold, and 9.7 meters of 52.9 grams per tonne of gold, all well above the mine's average reserve grade.

Plus, in addition to near-mine upside like Star, the company has a solid resource base at Goodpaster, with a maiden resource announced last year of ~1.1 million ounces at 10.3 grams per tonne of gold. So, while Pogo's 5-year mine life based on solely reserves may seem low, it's important to note that this is backed up by significant resources, with Pogo's total resource base continuing to grow and sitting at ~7.4 million ounces (~5.8 million ounces outside reserves). Hence, between the new Star discovery, the North Zone, and Goodpaster, this is a mine that could be producing until 2040 even if this might not appear to be the case based on solely its current reserve base (~6.6 million tonnes at 8.6 grams per tonne of gold).

{kind=link}

To summarize, while reserves were down year-over-year, it was a positive year overall for Northern Star, with growth in total resources to ~57.4 million ounces, and with the company reporting growth at key assets like Pogo, Kanowna, KCGM while holding the line at Jundee, Carosue Dam, and Thunderbox. And it's certainly encouraging to see the most significant of these assets creeping towards the ~30 million ounce resource mark on resources and just shy of 13 million ounces for resources given that KCGM should be a ~900,000-ounce per annum operation by FY2029, and a 12.0+ million ounce and growing reserve base gives it a solid base to work from to sustain this production profile until past 2040 when factoring in additional reserve replacement.

Gold Reserves vs. Peers

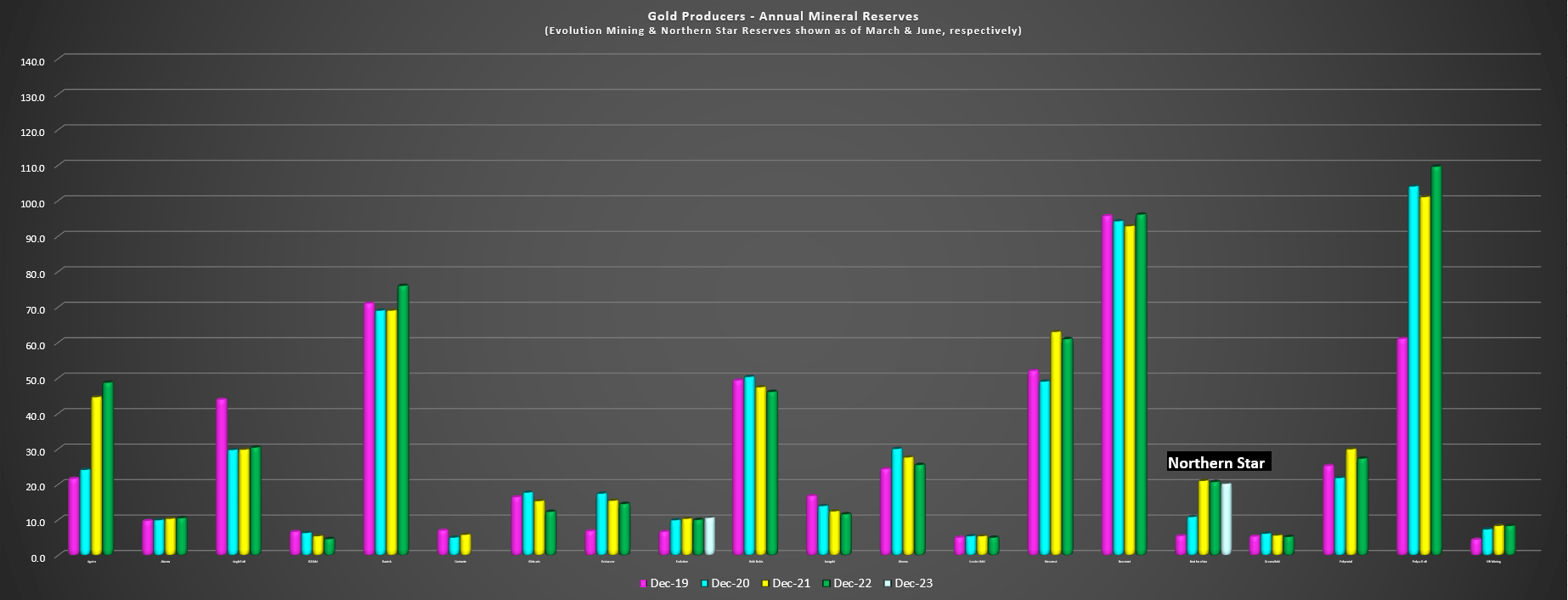

Digging into Northern Star's reserve growth vs. peers, we can see that the company has done a solid job mostly holding the line on reserves since FY2021 following its merger with Saracen Minerals. This is in line with the average for larger gold producers that haven't completed major acquisitions in the period, and it's actually better than many producers that have seen reserve declines like Gold Fields ( GFI ) and OceanaGold ( OCANF ). In fact, Northern Star is ranked 7th for largest reserve bases sector-wide at ~20.2 million ounces and ranks well against similar sized peers from a production standpoint like Kinross Gold ( KGC ) and Endeavour Mining ( EDVMF ) with ~25 million ounces at ~15 million ounces, respectively.

Gold Producers - Annual Mineral Reserves - Company Filings, Author's Chart

{kind=link}

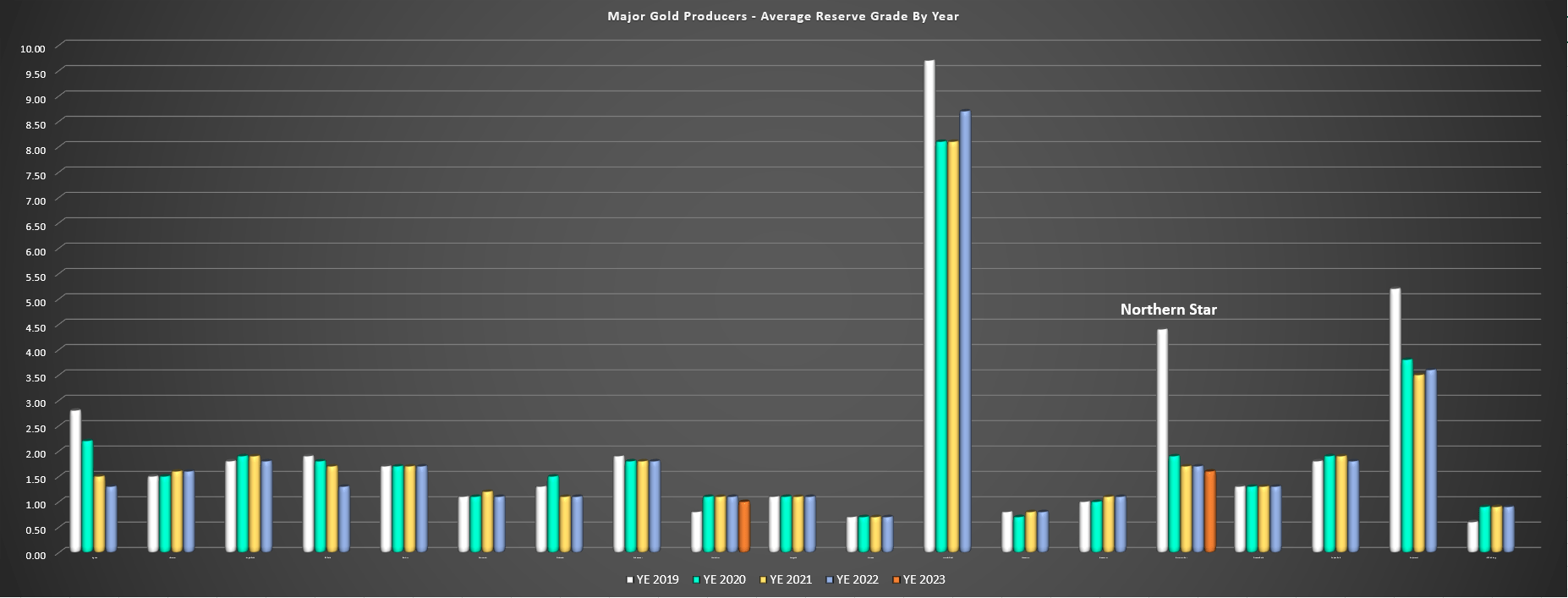

When it comes to reserve grade, Northern Star also stands out, and the addition of high-grade reserves at Mt. Charlotte helped the company to maintain its above-average reserve grade of 1.6 grams per tonne of gold. This is above the large producer peer average of ~1.4 grams per tonne of gold when excluding a major anomaly Lundin Gold ( LUGDF ) at 8.7 grams per tonne of gold, and also above the median reserve grade for this sub set of the producer universe. And when it comes to its largest peers, Northern Star is also ahead, with the three largest producers having an average reserve grade of ~1.3 grams per tonne of gold when factoring in the lower grade reserves added from the pending Newcrest acquisition. Just as importantly, the company has maintained relatively conservative gold price assumptions to calculate reserves, with a $1,400/oz reserve price assumption at Pogo and ~$1,200/oz at its Australian operations (0.65 AUD/USD exchange rate).

Major Gold Producers - Average Reserve Grade by Year - Company Filings, Author's Chart

{kind=link}

Let's take a look at Northern Star's valuation to see if the stock is sitting at an attractive buy point:

Valuation

Based on ~1.15 billion shares and a share price of US$7.20, Northern Star trades at a market cap of ~$8.3 billion and an enterprise value of ~$8.1 billion. This places it ahead of names like Kinross and AngloGold Ashanti ( AU ) which are much larger producers based on their guidance of ~2.1 and ~2.5 million ounces, respectively. However, while Northern Star may be smaller (~1.67 million ounces) with less diversification, the company is unique in that it's one of the only producers solely operating out of Tier-1 jurisdictions. In addition, the company operates one of the most impressive assets globally in KCGM (~500,000 ounces per annum growing to ~900,000 ounces per annum by the end of the decade), and has a more attractive cost profile, targeting all-in sustaining costs [AISC] below US$1,200/oz in FY2024. So, although it may be smaller, it screens well on quality relative to Kinross and AngloGold, with Tier-1 jurisdiction producers with above average grade reserves and below average costs typically trading at a premium valuation.

That being said, this will be another expensive year from an investment standpoint, with growth capital likely to come in above $800 million, suggesting Northern Star will likely generate less than $300 million in free cash flow this year. And while the company screens better from a P/FCF standpoint vs. peers in FY2026 once it grows production to ~2.0 million ounces, the stock currently trades at ~28x forward free cash flow, a significant premium to peers like Agnico Eagle ( AEM ) at ~20x forward free cash flow, but with Agnico being larger, more diversified, and also offering growth with one of the sector's best development pipelines. So, while I continue to see Northern Star Resources as one of the sector's top-10 producers from a quality standpoint, it's difficult to justify paying up for the stock from a valuation standpoint, especially in a market where investors are not paying up for future growth and more focused on current cash flow.

Obviously, I could be wrong, and Northern Star could continue to outperform its peer group and make a run at the US$9.50 level over the next 12 months. However, for businesses with depleting assets that lack pricing power, I prefer to buy at a deep discount to fair value or pass entirely. And while Northern Star may be very reasonably valued when considering its long-term potential (~2.0 million ounces at sub US$1,200/oz AISC), I continue to see several more attractive bets elsewhere in the sector currently. One example is B2Gold ( BTG ), which has transformed its jurisdictional profile with a high-grade operation in Nunavut, Canada, and currently trades at just ~6.25x FY2025 free cash flow estimates, a fraction of Northern Star's FY2024 and FY2025 P/FCF multiples. So, if I were looking to put new capital to work in the sector, I see B2Gold below US$3.05 as a lower-risk buying opportunity.

Summary

Northern Star had a solid year in FY2023, maintaining solid cost control in a jurisdiction that continues to struggle from a labor tightness standpoint. This helped the company to generate over $230 million in free cash flow despite a tough fiscal H1 2023 (lower gold prices), and the company also took advantage of its share price weakness to buy back ~1% of its outstanding shares (~15.5 million shares repurchase in FY2023). Finally, the company made a Final Investment Decision on the KCGM Mill Expansion, setting this asset up to be one of the largest gold mines globally by the end of the decade, which should help Northern Star to maintain its premium multiple. And supporting this growth, reserves remained steady at over 20.2 million ounces, with over 28.0 million ounces of resources at KCGM, its flagship asset and a key pillar for its future growth.

However, with Northern Star sitting over 65% from its September 2022 lows, the stock has significantly outperformed its peer group, and this made its relative value less attractive than peers. This is especially true given that Northern Star's free cash flow generation will be strained short-term because of elevated growth capital, and the company continues to have elevated hedges relative to peers (~440,000 ounces below US$1,800/oz in FY2024), meaning that gold price strength will matter less regarding providing upside surprises. Hence, while I see Northern Star as a solid buy-the-dip candidate, I would only become interested at US$6.15 or lower where its relative value setup would improve vs. million-ounce producer peers.

For further details see:

Northern Star Resources: Solid Reserve Replacement In FY2023