NESRF - Northern Star Resources: Time To Book Some Profits

Summary

- Northern Star Resources has enjoyed a massive rally since September, up more than 85% from its lows in less than 80 trading days.

- This strong recovery is attributed to it being dirt-cheap while it hung out below US$5.00 per share at less than 0.80x P/NAV and the impressive rally we've seen in gold.

- So, while the company has a very strong H2 2023 ahead with back-end weighted production, I don't see any way to justify chasing the stock here above US$8.25.

Just over four months ago, I wrote on Northern Star Resources ( NESRF ), noting that while the company saw a slight miss in FY2022, this already looked priced into the stock after a more than 60% decline. Since then, the stock has been up more than 50%, lagging behind Evolution Mining ( CAHPF ), which has doubled, but it is impressive compared to many other sectors that have treaded water or declined on a trailing four-month basis. However, while I expect much stronger results in fiscal Q2/fiscal Q3 2023, the stock is getting extended short-term, suggesting that chasing the stock above US$8.30 is risky. Let's take a closer look below:

Unless otherwise noted, all figures are in Australian Dollars (), and all exchange rates are based on $0.70 AUD/USD . Northern Star trades significant volume daily on the Australian Stock Exchange (NST.ASX) but trades very limited volume on the OTC Market. Therefore, the best way to trade the stock is on the Australian Stock Exchange. There is a significant risk to buying on the OTC due to wide bid/ask spreads, low liquidity, and no guarantee of future liquidity.

Fiscal Q1 Results & Fiscal Q2 Outlook

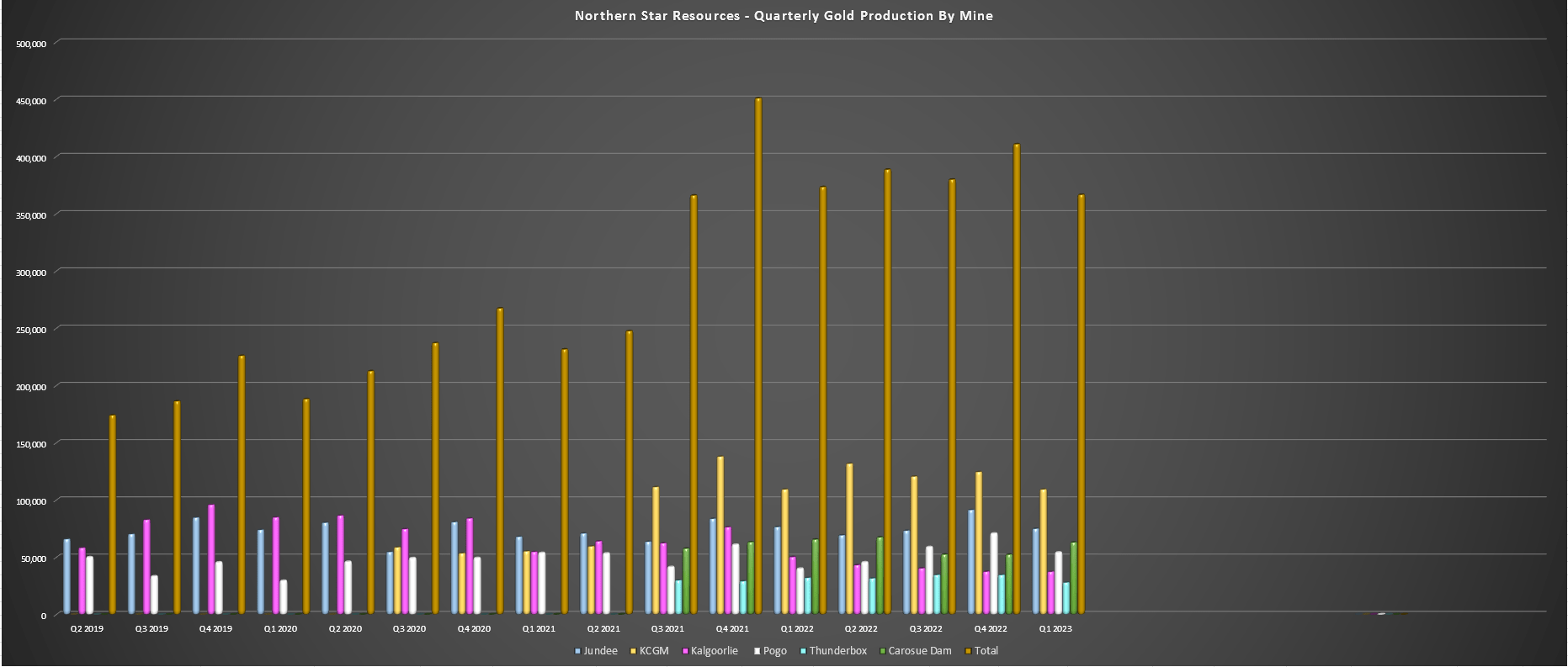

Northern Star released its fiscal Q1 results (calendar year Q3) in November, reporting quarterly production of ~366,600 ounces of gold at all-in-sustaining costs [AISC] of A$1,788/oz [US$1,251/oz]. This was a 2% decline from the year-ago period, driven by lower output from Jundee and its Kalgoorlie Operations, plus a slight dip in production at Thunderbox. Fortunately, Pogo picked up some of the slack in the period, with the operation now running at an annualized rate of ~1.3 million tonnes per day, with ~319,000 tonnes processed in fiscal Q1 at an average grade of 6.1 grams per tonne of gold. Given the higher denominator, unit costs improved materially, dropping from $1,700/oz+ to $1,581/oz despite inflationary pressures.

Northern Star - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

On the surface, the fiscal Q1 production results might have looked a bit disappointing, coming in at just 22.6% of the company's annual guidance mid-point (1.62 million ounces). However, it's important to note that the company had a major maintenance shutdown in fiscal Q1 at its largest KCGM operation that impacted plant throughput, and the company has guided to production being back-end weighted this year. Plus, not only was KCGM expected to benefit from higher grade ounces in fiscal Q2 (October to December 2022 quarter that's being reported this month), and we'll see higher throughput from Thunderbox with the mill expansion complete plus higher grades at Pogo in H2-2023. Hence, production should progressively improve throughout the year.

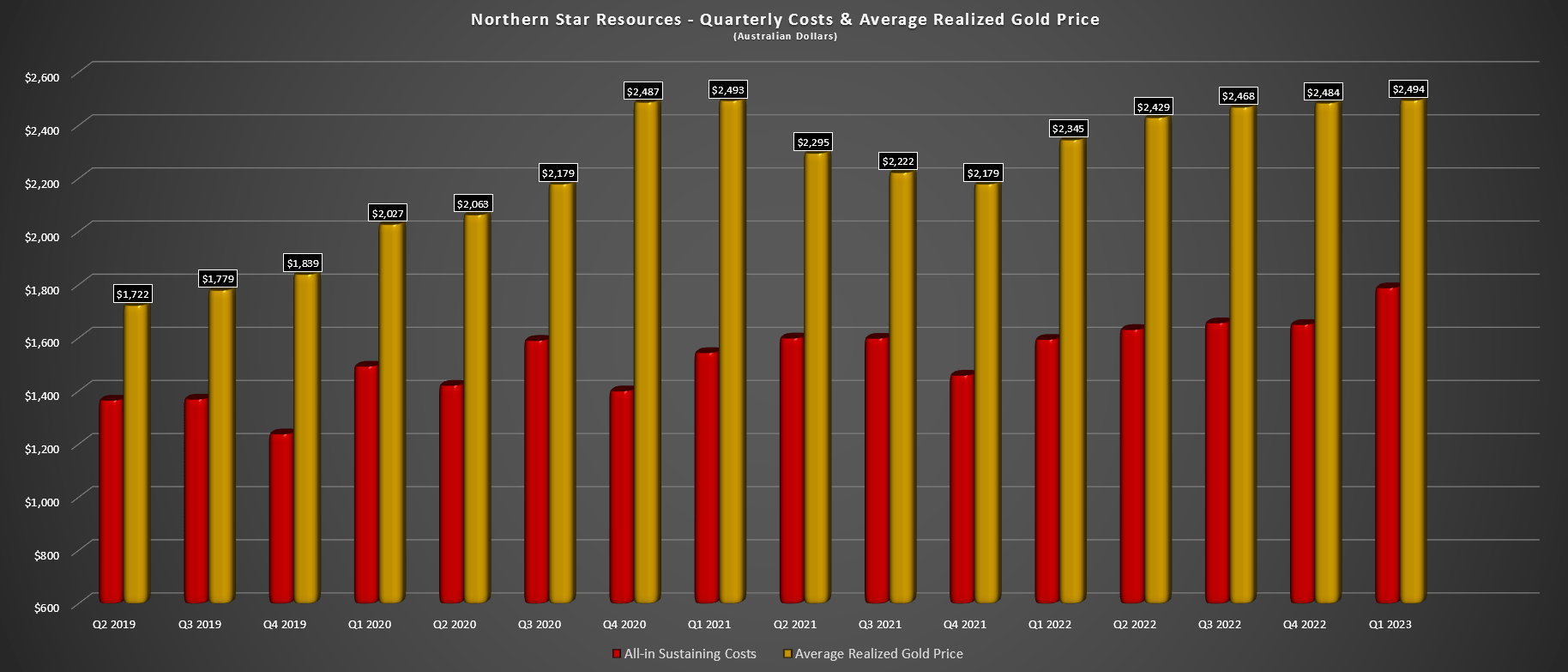

Northern Star - Quarterly Costs & Average Realized Gold Price (Company Filings, Author's Chart)

{kind=link}

Meanwhile, from a financial standpoint, Northern Star will benefit from a higher gold price sequentially in fiscal Q2 (calendar year Q4 2022) and an even higher gold price in fiscal Q3 (CY-Q123). In addition, it should benefit from the pullback we've seen in diesel prices, lower diesel usage (5% reduction in diesel with new fleet), and higher productivity (improved speed). In fact, material movements have been quite impressive, annualizing out to ~95 million tonnes in September 2022.

This combination of increased production from fiscal Q1 to fiscal Q2, a higher gold price, and lower-strip and higher-grade ounces from Golden Pike should contribute to higher margins for this asset. On a consolidated basis across the portfolio, I would also expect margin improvement due to the higher gold price.

{kind=link}

Looking at the gold price above, we can see that assuming limited deliveries into hedges, Northern Star's average realized gold price should come in above A$2,570/oz in fiscal Q2 2023, a 4% improvement sequentially vs. its most recent quarter (A$2,494/oz). Meanwhile, looking ahead to the current quarter in fiscal Q3 2023, I would expect a minimum average realized gold price of A$2,650/oz, a further 3% improvement on a sequential basis. To summarize, investors can look forward to margin expansion as the year progresses, assuming the gold price doesn't collapse from here, with a favorable mix of a tailwind in the gold price and steadily declining costs as production ramps up.

Recent Developments

Moving over to more recent developments, Northern Star continued to execute its relatively aggressive share repurchase program last quarter, repurchasing stock on several different days and continuing with its share repurchases into the new year. In total, the buyback will represent over 3% of the company's outstanding shares, one of the larger buyback programs sector-wide, and an intelligent use of capital while the stock was undervalued below US$7.00. especially given Northern Star's strong balance sheet. Importantly for investors focused on yield as well, the buyback program will not interfere with its dividend policy. To date, over 15 million shares have been repurchased, translating to 1.3% of the outstanding share count.

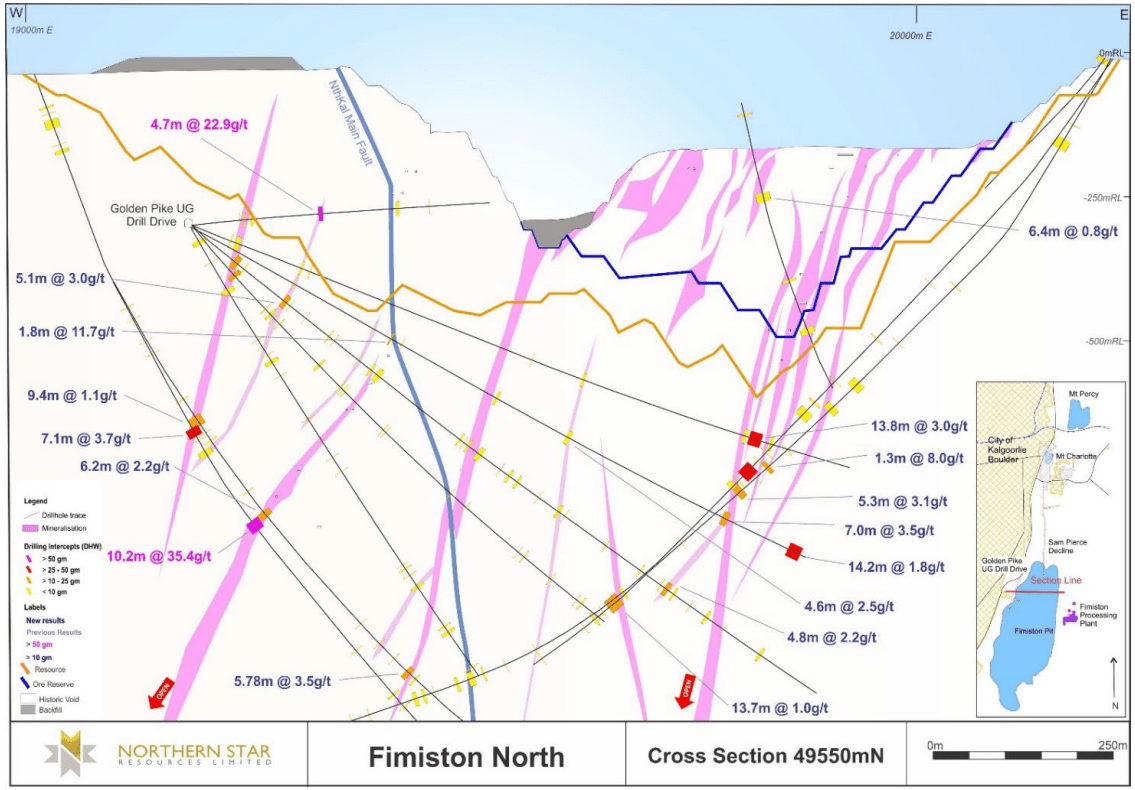

Regarding other developments, Northern Star put out an exploration upside for its portfolio last quarter, and the results were very encouraging. Beginning with its Australian portfolio, the company reported solid drill intercepts from Fimiston North (10.2 meters at 35.4 grams per tonne of gold) and Fimiston South (8.2 meters at 9.6 grams per tonne of gold, 7.8 meters at 9.8 grams per tonne of gold, and 4.5 meters at 23.2 grams per tonne of gold). The drilling at Fimiston North was from the first dedicated underground drill drive, with several hits beneath the resource pit hitting impressive grades. Meanwhile, drilling at Fimiston South is focused on converting inferred ounces and confirming the grade continuing of the inferred resource areas.

{kind=link}

Moving over to the Maritana orebody, which is part of Mt. Charlotte Underground (3 kilometers north of the Fimiston plant), drilling targeting the southern extents of the lower Maritana orebody has identified a new lower zone of gold mineralization north of the Golden Pike Fault. Northern Star noted that the drill results have outlined a new panel of mineralization, and it will be doing additional drilling to see whether there's a down-plunge extent to this new mineralized zone.

Highlight intercepts included an incredible 18.0 meters at 33.8 grams per tonne of gold, 48.0 meters at 3.79 grams per tonne of gold, 38.9 meters at 4.0 grams per tonne of gold, and a very thick intercept of 74.0 meters at 1.9 grams per tonne of gold. This is very encouraging, given that it could add meaningful ounces near existing infrastructure.

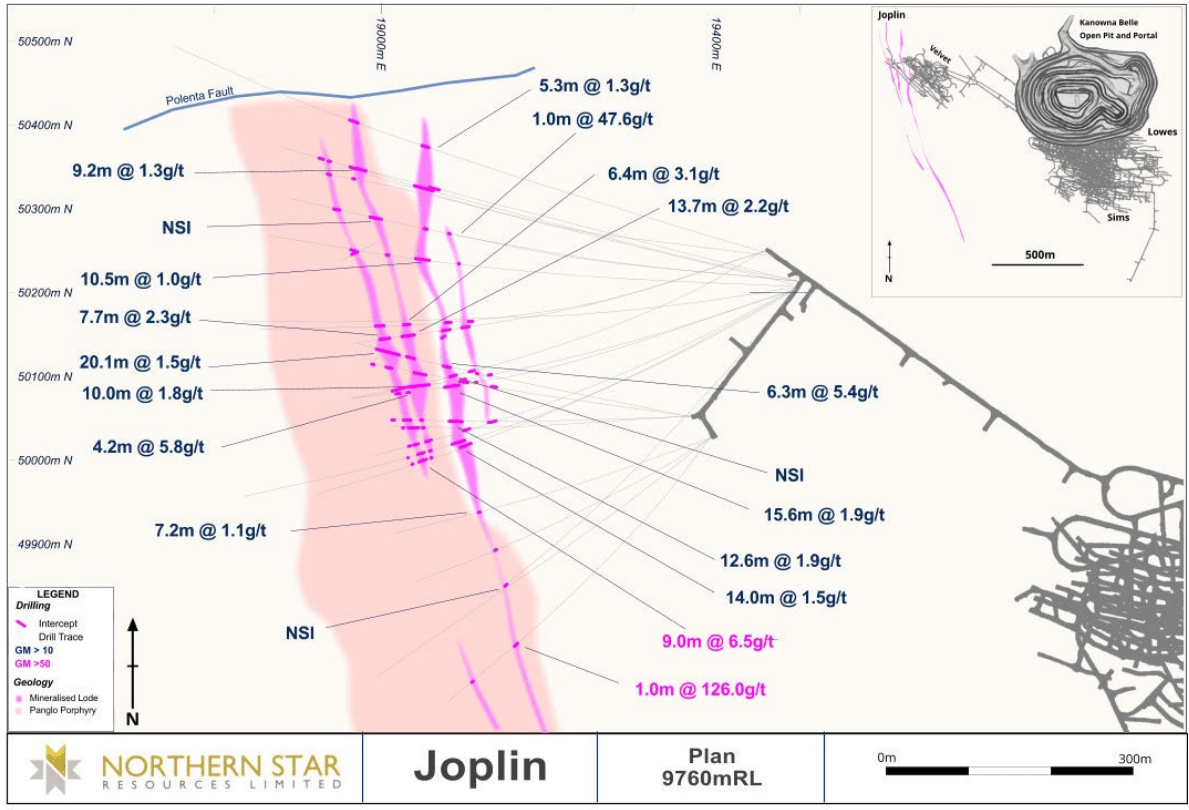

At the company's Kalgoorlie Operations, Northern Star noted that it made a new discovery, the Joplin deposit, which is located within 1 kilometer of Kanowna Belle and less than 300 meters from Velvet mining development. This was a blind discovery 500 meters below the surface, and recent underground and surface drilling has defined mineralization over a 1.4-kilometer strike to a vertical depth of 1,000 meters. Highlight intercepts included 7.2 meters at 3.2 grams per tonne of gold, 8.96 meters at 6.52 grams per tonne of gold, 4.24 meters at 5.78 grams per tonne of gold, and 6.3 meters at 5.4 grams per tonne of gold. This new discovery could boost resources near existing infrastructure and add new mining areas for this operation.

Joplin Discovery & Velvet Mine Development (Company Website)

{kind=link}

Moving to the east, Northern Star has seen very impressive results from the Red Hill deposit, which sits just 3 kilometers east of the Kanowna Belle plant and 22 kilometers from the Fimiston plant at KCGM. Red Hill was a historical open-pit operation from 2001-2007, and intercepts beneath the pit have outlined broad zones of mineralization within the host porphyry intrusion. Highlight intercepts include 239 meters at 1.2 grams per tonne of gold, 161 meters at 2.8 grams per tonne of gold, and 195 meters at 2.7 grams per tonne of gold, with several other high-grade hits over smaller intercepts. The company noted that an updated resource incorporating these results will be released later this year, providing the company with a better idea of the size of the opportunity here.

{kind=link}

Finally, at the company's Pogo Mine in Alaska, Northern Star has released solid results from near-mine drilling, suggesting the potential to expand resources near existing workings. The highlight hit at the North Zone was 5.9 meters at 56.6 grams per tonne of gold, and Northern Star hit several solid intercepts, including 2.0 meters at 44.1 grams per tonne of gold and 3.9 meters at 26.7 grams per tonne of gold at South Pogo.

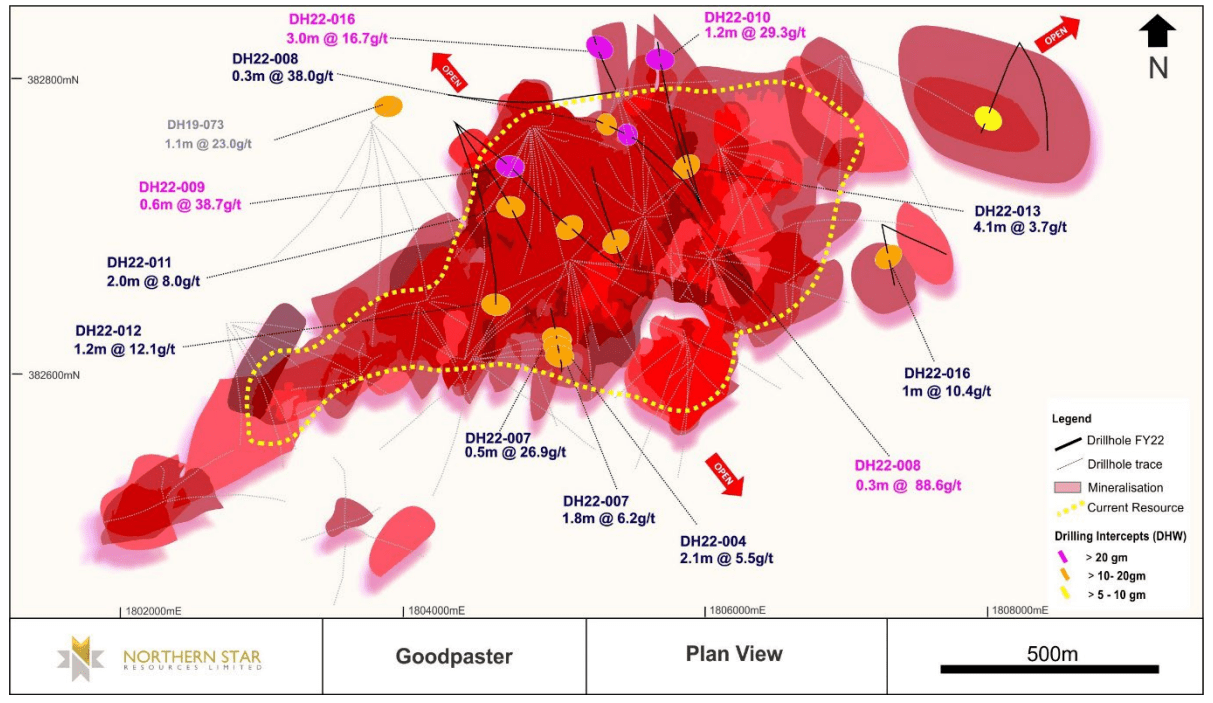

South Pogo represents the up-dip continuation of the Liese vein system. Meanwhile, at Goodpaster, which is a regional discovery 2 kilometers west of Pogo on the other side of the Goodpaster River, results continue to be impressive with multiple 15.0+ grams per tonne intercepts that are expanding an already large resource base (3.2 million tonnes at 10.3 grams per tonne of gold).

Overall, I see these exploration results from its three mining centers as very positive, and they certainly justify the company's plans and already completed throughput expansions. In fact, and although not discussed here, the potential resource growth at the Yandal Mining Center is just as encouraging, with the Wonder North Project continuing to grow and a new discovery made more than 1.0 kilometers to the east.

Notably, this is just 25 kilometers from the larger Thunderbox Plant (3.0 million ---> 6 million tonnes per annum), potentially setting up a future spoke. To summarize, while the company is doing an exceptional job from an operations standpoint, it's seeing great results from an exploration standpoint, which will allow Northern Star to sustain these production levels past 2035, a positive development.

Valuation & Technical Picture

Based on 1155 million fully-diluted shares and a share price of US$8.25, Northern Star trades at an enterprise value of ~US$9.4 billion. This is no longer a significant discount to its peer group, with similar-sized or larger producers like Endeavour Mining ( EDVMF ) trading at a valuation of ~$5.8 billion and Kinross ( KGC ) at a valuation of ~$7.7 billion. Obviously, Northern Star deserves a premium valuation due to its purely Tier-1 jurisdiction profile and long reserve life at KCGM (top-10 reserve base globally just behind Detour Lake, Cadia, and Lihir). Still, with the stock now trading at ~1.3x P/NAV vs. an estimated net asset value of ~$7.3 billion, I see the stock as getting closer to being fully valued short term.

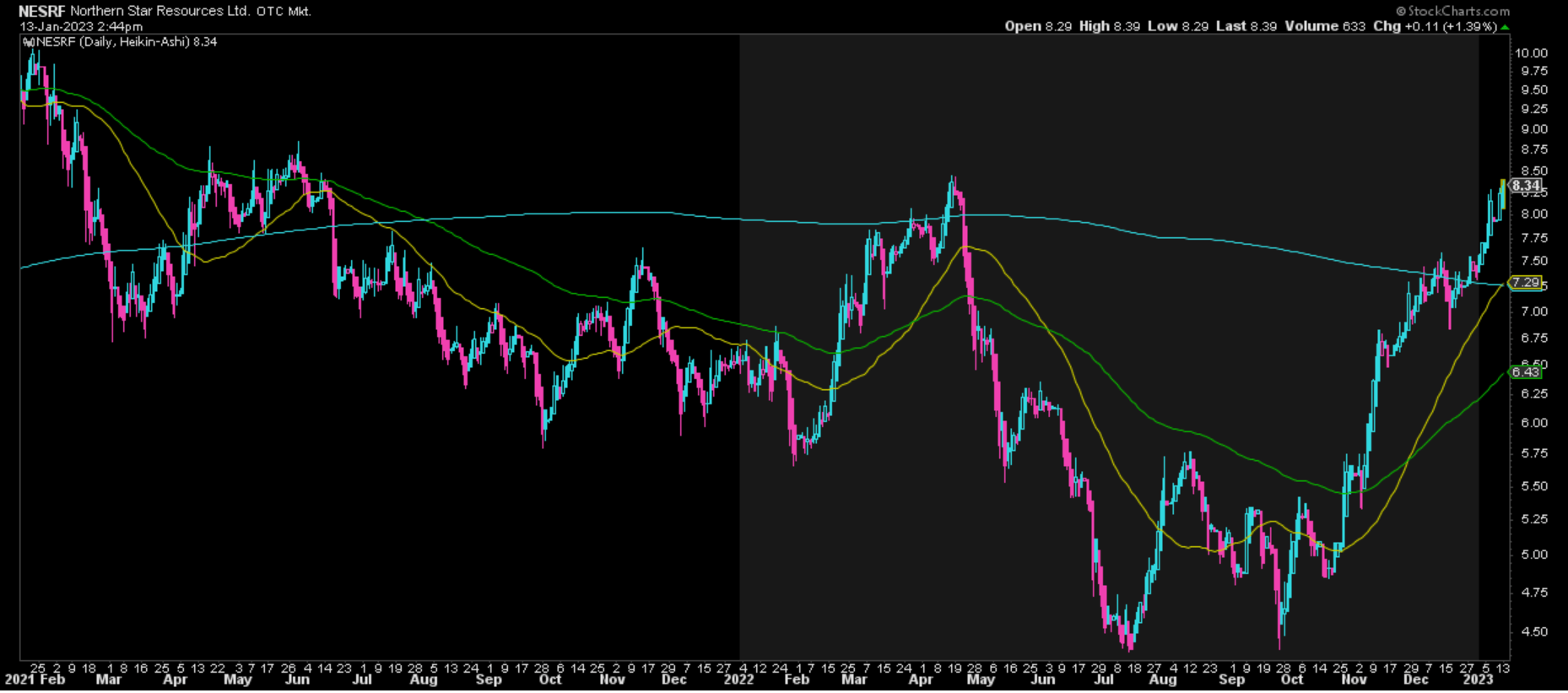

Using a 1.40x P/NAV multiple to reflect the company's unique positioning as one of the only Tier-1 jurisdiction gold producers that will see meaningful production growth looking out to 2026, I see a fair value for the stock of ~$10.3 billion or US$8.90 per share - 8% upside to current levels. Unfortunately, this doesn't point to much upside from current levels, suggesting this is not a low-risk buy point. Meanwhile, the technical picture confirms this, with NESRF's next strong support level coming in at US$5.80 and the stock now within striking distance of resistance at US$8.80. So, with a reward/risk ratio of less than 0.20 to 1.0, I believe there's an elevated risk to chasing the stock at these levels, and I think some profit-taking would be prudent above US$8.20.

{kind=link}

Summary

Northern Star should have a stronger fiscal Q2 report on deck with an improvement in the gold price, and investors can look forward to an even better H2 2023. Meanwhile, the company's multi-year growth plan makes it one of the higher-growth million-ounce producers in the space, and with growth being a rarity among larger producers, there's a lot to like here long-term. That said, the stock is beginning to get a bit extended short term, and I see Northern Star becoming close to fully valued above US$8.30 as we head into its fiscal Q2 report. For this reason, I would be booking some profits above US$8.25, and I certainly don't see any way to justify chasing the stock up here as it approaches its first major resistance level.

For further details see:

Northern Star Resources: Time To Book Some Profits