NESRF - Northern Star Resources: Tracking Well Against FY2023 Guidance

Summary

- Northern Star Resources has been one of the best-performing gold miners year-to-date after significant underperformance following its acquisition of Saracen.

- I attribute this recent outperformance to the stock hitting its most oversold levels in years at its September lows and trading at arguably its most attractive valuation since 2018.

- However, with the stock up 90% off its lows, I don't see any way to justify paying up for the stock here even if it is a solid growth story.

The Calendar Year Q4 Earnings Season for the Gold Miners Index ( GDX ) has finally begun, and one of the first companies to report its results is Northern Star Resources ( OTCPK:NESRF ) on the Australian Market. The company released its fiscal Q2 2023 (CY-Q4) results last month, reporting gold sales of ~404,300 ounces and production of ~397,800 ounces. This has placed year-to-date gold sales at ~773,000 ounces, with the company in a position to deliver on its FY2023 guidance of ~1.62 million ounces of gold sales given that H2 will be much stronger than H1. Let's take a look below:

{kind=link}

Unless otherwise noted, all figures are in Australian Dollars (), and all exchange rates are based on $0.70 AUD/USD . Northern Star trades significant volume daily on the Australian Stock Exchange (NST.ASX) but trades very limited volume on the OTC Market. Therefore, the best way to trade the stock is on the Australian Stock Exchange. There is a significant risk to buying on the OTC due to wide bid/ask spreads, low liquidity, and no guarantee of future liquidity.

Fiscal Q2 Production & Sales

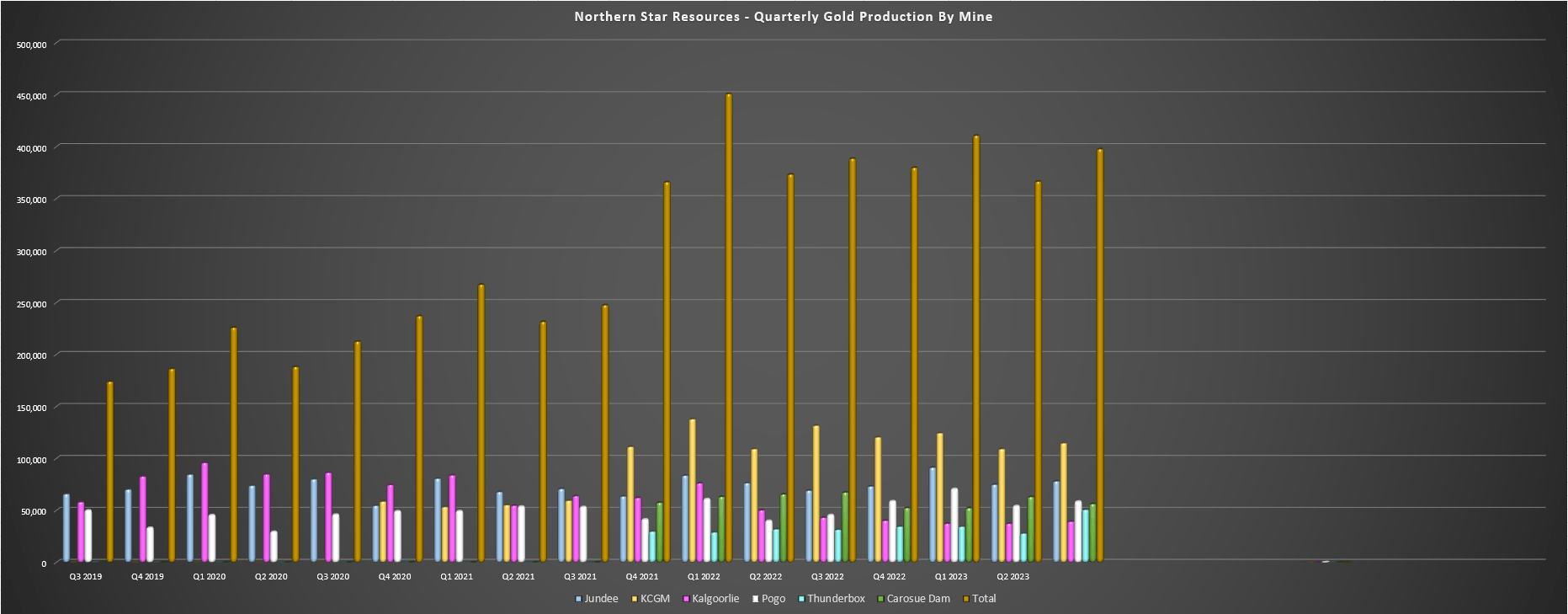

Northern Star Resources ("Northern Star") released its fiscal Q2 2023 results last month and reported quarterly gold production of ~397,800 ounces, a nearly 3% increase from the year-ago period. The company achieved this solid performance despite a softer quarter from its largest operation, KCGM, a weaker quarter from its #3 operation (Carosue Dam) and relatively low grades at its Pogo Mine in Alaska where grades came in roughly 20% below reserve grades. This is because its Thunderbox Operation is benefiting from higher throughput following the mill expansion to 6.0 million tonnes per annum, with Bronzewing and Thunderbox feed helping to push quarterly production to ~50,700 ounces in fiscal Q2, a 47% increase year-over-year.

Northern Star - Quarterly Gold Production by Mine (Company Filings, Author's Chart)

{kind=link}

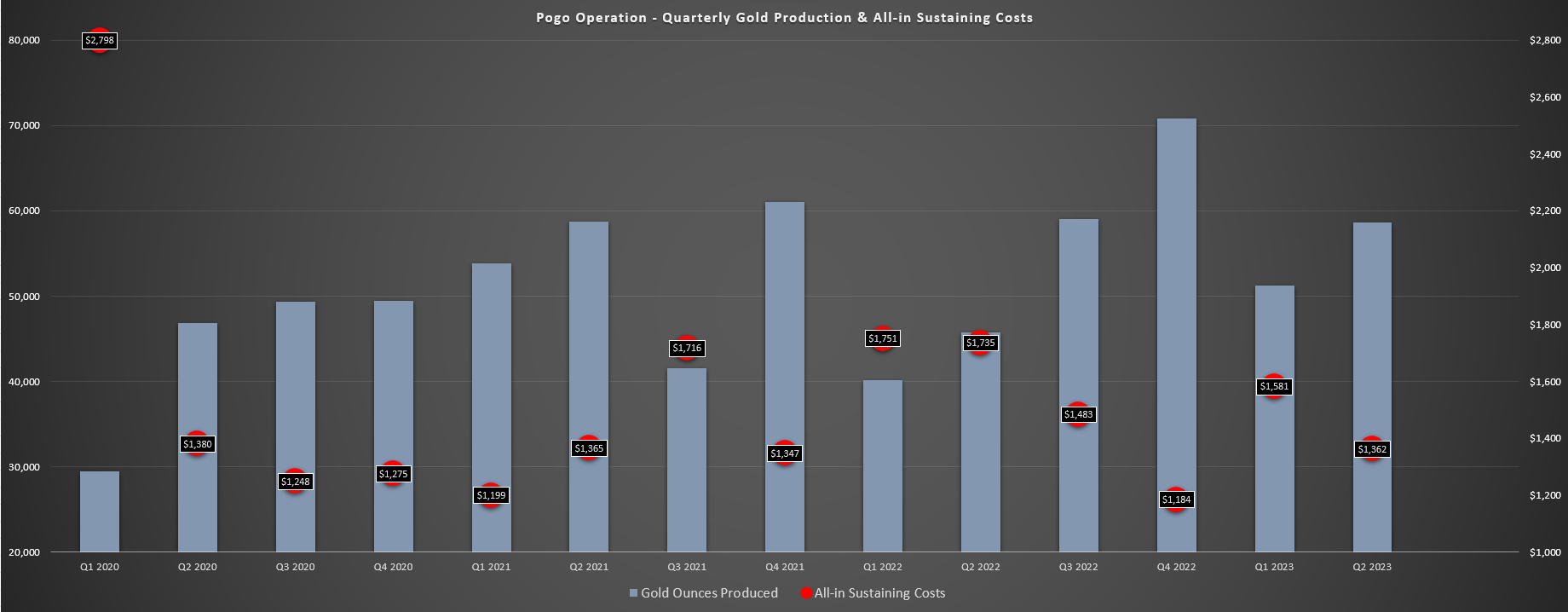

Meanwhile, heading north at its Yandal Operations to Jundee, the mine had another solid quarter, with ~740,000 tonnes processed at 3.6 grams per tonne of gold, up from ~709,000 tonnes at 3.4 grams per tonne of gold in fiscal Q2 2022. The result was a ~13% increase in production year-over-year to ~78,100 ounces, with AISC coming in at a very respectable figure of A$1,387/oz [US$971/oz]. Finally, although grades were low at Pogo, the increased throughput easily made up for the grades, with the Alaskan operation producing ~58,600 ounces (fiscal Q2 2022: ~45,700 ounces), with throughput increasing from ~255,000 tonnes to ~317,000 ounces at similar grades and stope ore representing 72% of the ore blend in the quarter.

Given the solid performance at these four mines (Bronzewing, Thunderbox, Jundee, Pogo), Northern Star enjoyed its 2nd best quarter in the past 18 months regardless of the lower contribution from its largest mining center: Kalgoorlie. This has placed year-to-date gold sales at ~773,200 ounces, tracking at ~48% of its guidance mid-point. As the company noted in its prepared remarks, H2 2023 will be stronger with ~8.0 gram per tonne grades at Pogo and a throughput rate closer to ~1.5 million tonnes per quarter at Thunderbox (fiscal Q2 2023: ~1.21 million tonnes processed).

Pogo - Quarterly Production & Costs (Company Filings, Author's Chart)

{kind=link}

So, why did the Kalgoorlie mining center underperform in the period?

Beginning with its Kalgoorlie South operations, the company noted when it headed into the year that the focus was on margins, not absolute ounces, and that it would place its Jubilee Mill (~1.0 million tonnes per annum) in care and maintenance, representing a ~30,000-ounce annual headwind from a comparison standpoint as part of a change in milling strategy. Meanwhile, Carosue Dam saw lower underground grades in the period and lower tonnes processed, with the latter impacted by planned maintenance shuts.

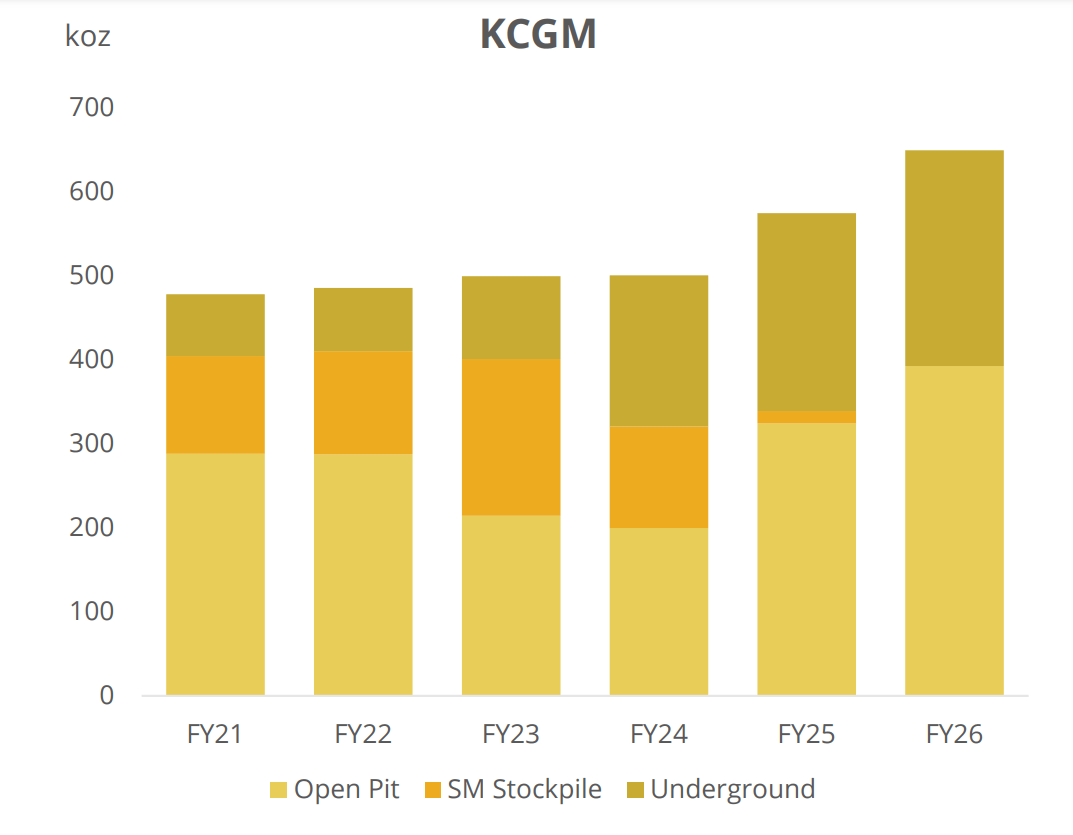

Finally, KCGM actually had a very solid quarter with record open-pit material movements from the new mining fleet, a significant increase in underground tonnes mined from Mt. Charlotte stoping areas (underground tonnes increased to ~470,100 vs. ~365,400 in fiscal Q2 2022). Meanwhile, East Wall remediation is underway and expected to be completed in FY2024, with this wall failure being one reason that Barrick ( GOLD ) and Newmont ( NEM ) placed KCGM in the hands of Saracen and Northern Star, choosing to walk away and divest the asset in 2019. Once completed, this will allow for access to low-cost ounces from Golden Pike North. Ultimately, the goal for this asset is 650,000+ ounces per annum in FY2026, a 30% plus increase from current levels.

However, while work is progressing towards a more significant operation at KCGM and the new 793F mining fleet is delivering productivity gains (14 km/hour vs. 11.8 km/hour) and cost improvements (5% fuel efficiency), the headline production numbers fell short with just ~114,800 ounces in the period, down from ~131,700 ounces in fiscal Q2 2022. The dip year-over-year resulted from lower open-pit grades and fewer tonnes milled, with ~3.34 million tonnes processed vs. ~3.57 million tonnes in the year-ago period. That said, cost performance was still solid despite lower gold volumes and inflationary pressures, with AISC of A$1,538/oz [US$1,077/oz], a figure that sits 16% below the estimated industry average ($1,280/oz).

{kind=link}

Overall and considering the continued labor tightness and skill shortages in prolific regions like Nevada, Western Australia, and Canada/Quebec, I see Northern Star's performance as satisfactory, and the company should have no issue meeting its production guidance. Let's dig into costs and margins below to see how they are trending, especially with the recent improvement in the gold price:

Costs & Margins

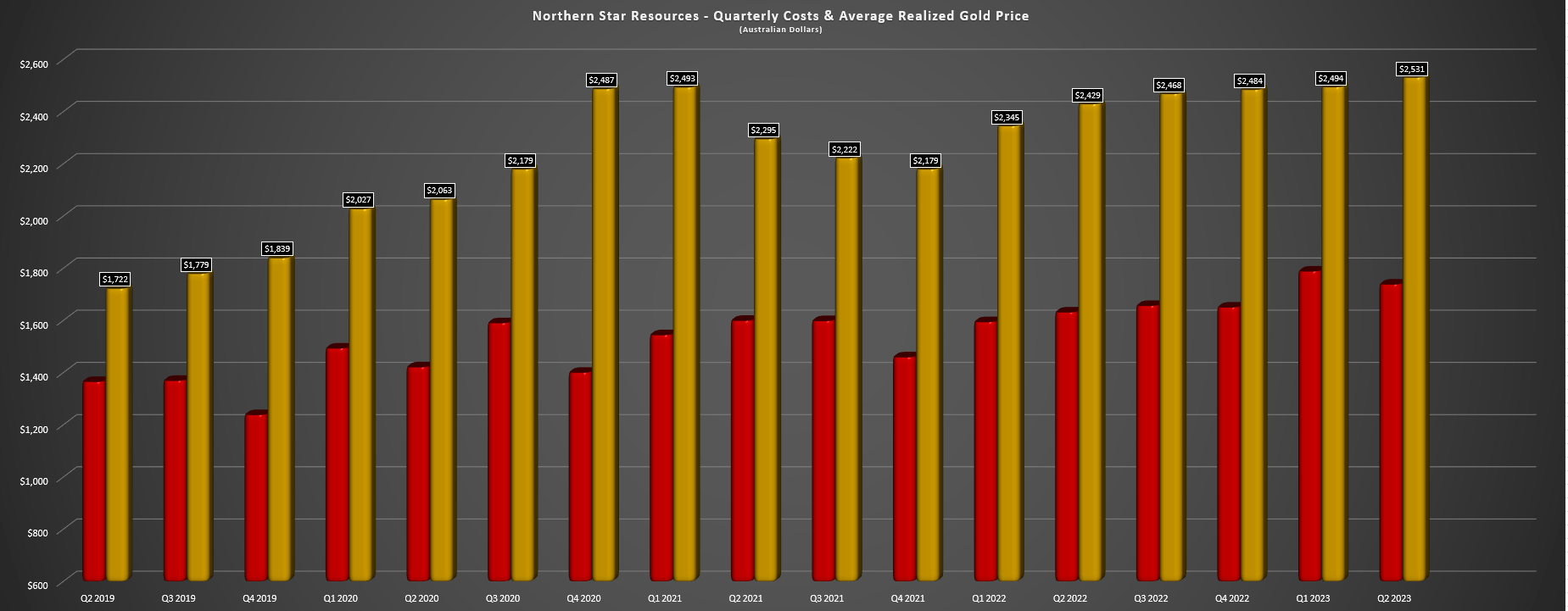

Digging into costs and margins, Northern Star reported all-in-sustaining costs of A$1,746/oz [US$1,222/oz] in fiscal Q2 2023, a 7% increase from the year-ago period. This was affected by inflationary pressures which are not company-specific, with most gold producers reporting higher fuel, cyanide, labor, steel, and reagents costs, with costs further exacerbated by supply chain headwinds. Fortunately, Northern Star benefited from a higher average realized gold price of A$2,531/oz despite delivering into ~174,000 worth of hedges, with its AISC margin declining only marginally from A$798/oz to A$785/oz.

Northern Star - Quarterly AISC & Average Realized Gold Price (Company Filings, Author's Chart)

{kind=link}

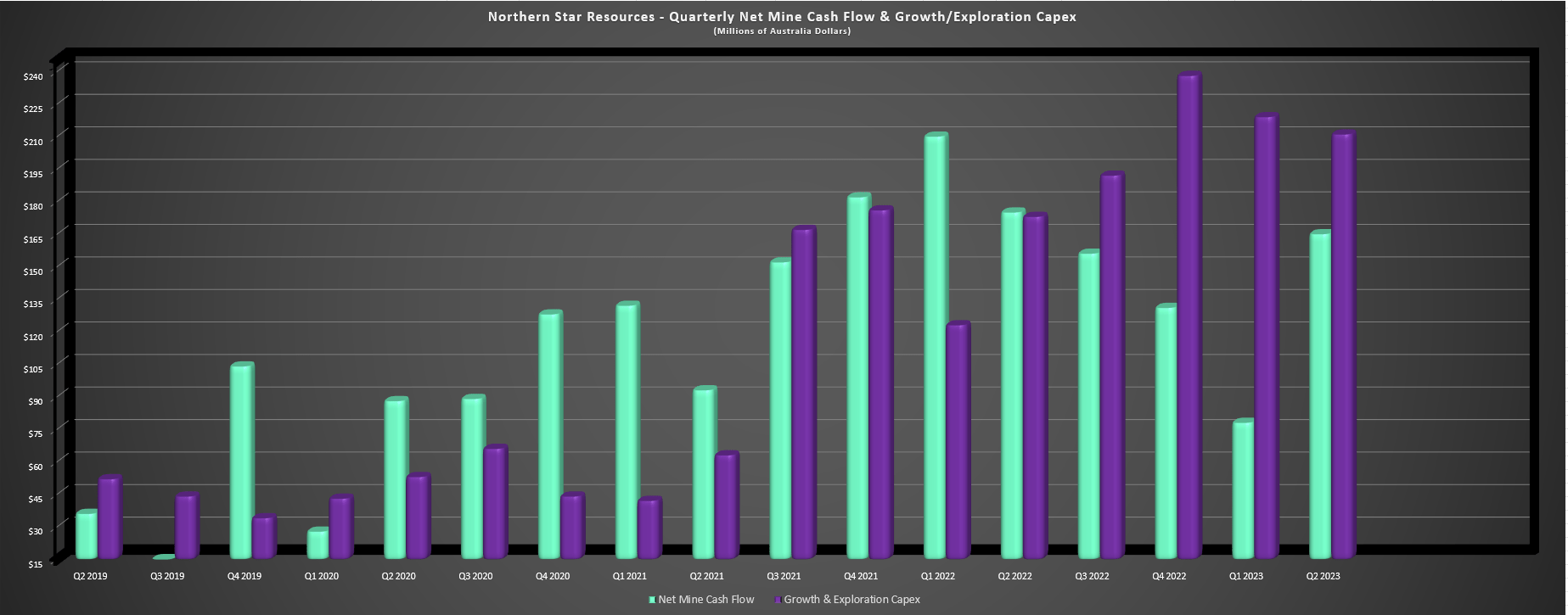

Given the limited margin compression and high sales volumes (~404,000 ounces), Northern Star generated positive free cash flow at all three of its mining centers in the period (Kalgoorlie, Yandal, Pogo), with net mine cash flow of A$165 million despite significant spending on growth capital and exploration (A$211 million). Meanwhile, revenue came in at A$1,023 million and should increase to closer to A$1.1 billion in fiscal Q3 2023 with the benefit of slightly higher sales volumes and a higher average realized gold price (current price: A$2,670/oz). Finally, Northern Star added ~145,000 ounces of hedges at A$2,954/oz, a move that I like a lot, and I wish more producers would employ this strategy for a small portion of total production when things become short-term overheated.

Northern Star - Free Cash Flow & Growth/Exploration Spending (Company Filings, Author's Chart)

{kind=link}

Before moving on, it's worth noting that while Pogo had a sub 60,000-ounce quarter, unit costs at the operation dropped like a stone, sliding from $1,735/oz in fiscal Q2 2022 to $1,362/oz. These are very respectable costs for an asset that has dragged on Northern Star's consolidated margins for a while and it's nice to see this asset hitting its stride. Notably, Northern Star stated it has room for further optimizations at Pogo, so it looks like we could see costs actually drop below the industry average (~$1,300/oz) long term at this asset.

Finally, in terms of the exhausting battle against inflation that has wreaked havoc on producers' margins, these pressures are stickier than I expected, and Northern Star stated the following:

"So probably the only cost we've seen come off is in fuel, and all the rest are fairly steady, fairly sticky. And it really depends on, I guess, what all the commodities are doing in the same space. So we've seen some relief in staff turnover and stability there post sort of COVID border opening. But we certainly haven't -- every quarter we even ask ourselves if have we peaked, is it coming down. We don't see material signals for it to -- those unit costs to come down. So yes, we've relate it against our strategy, which is growing profitably, the unit cost derived by economies of scale, the larger plants on same fixed cost base. That's really how we're getting our unit cost down. But the inputs we haven't seen lining up with your materials and/or your labor."

- Northern Star, fiscal Q2 Conference Call

Although it's disappointing to hear that costs have barely improved (except for fuel) and there's still a clear shortage of skilled labor sector-wide, the theme appears to be that while costs haven't come down; they aren't really worsening. Plus, unit costs in 2022 were impacted by supply chain headwinds as well and these appear to be subsiding, suggesting that although we may not see the meaningful drop-off I was expecting, we should see a slight improvement in costs for some gold majors in 2023 vs. 2022. That said, Northern Star benefits from a strong balance sheet to invest in optimizing its asset and growing and with increased tonnes processed and its regional milling strategies plus greater economies of scale at Pogo, I expect it to claw back some of its lost margins over the next few years.

Valuation & Technical Picture

Based on ~1155 million fully diluted shares and a share price of US$8.20, Northern Star trades at an enterprise value of ~US$9.55 billion. This is not a cheap valuation, with it now trading at 1.30x P/NAV vs. an estimated net asset value of ~$7.3 billion. Although Northern Star deserves to trade at a premium multiple to peers given its Tier-1 jurisdiction profile (Australia, United States) and diversification, I've never found much value in paying above 1.0x P/NAV for a producer, and certainly not 1.30x P/NAV. So, although the stock could continue to march higher if we see a strong bid under gold prices, I don't see any margin of safety at current levels.

If we use a 1.40x P/NAV multiple which is one of the highest multiples that I would assign to any producer sector-wide and just behind Agnico Eagle ( AEM ), I see a fair value for the stock of ~$10.36 billion or US$8.95 per share. This does point to moderate upside, but I prefer a minimum of a 35% discount to fair value to justify buying mid-cap stocks in cyclical miners, regardless of whether they are sector leaders or have positive attributes. After applying this discount, Northern Star is significantly above its ideal buy zone of US$5.80, suggesting that there's no way to justify paying up for the stock at current levels. In fact, I would take some profits above US$8.30 if I were long from below US$6.00 when the stock headed into a low-risk buy zone .

{kind=link}

Finally, if we look at the technical picture, Northern Star remains overbought short-term, and continues to trade in the upper portion of its support/resistance range. This is based on expected resistance at US$8.80 and no support until US$5.80, translating to a reward/risk ratio of 0.20 to 1.0. I want a minimum of a 6.0 to 1.0 reward/risk ratio to justify entering long positions in gold miners, so I see the current setup as unfavorable with elevated risk of a sharp pullback. Hence, chasing the stock here above US$8.30 could prove to be a bad idea.

Summary

Northern Star Resources put together a solid H1 2023 performance and although sales look to be tracking behind guidance, it's important to note that output is back-end weighted with higher grades at Pogo and increased throughput expected at Thunderbox (~1.5 million tonne per quarter processing rate). Meanwhile, although inflationary pressures have proven sticker than I expected, Northern Star continues to work towards optimizing its operations to drive down unit costs, with room to further improve costs at all its operations. That said, the goal is to buy great businesses when they're out of favor and offering a meaningful margin of safety, and this is no longer the case at US$8.30. So, while I see Northern Star as a top-12 producer sector-wide, I would be taking advantage of this strength to book some profits.

For further details see:

Northern Star Resources: Tracking Well Against FY2023 Guidance