NWBI - Northwest Bancshares: Great Dividend Not So Great Price Though

2023-07-29 08:18:19 ET

Summary

- Northwest Bancshares Inc's share price dropped almost 40% after news of liquidity issues at First Republic Bank.

- Despite a dividend yield of over 6%, the current price is not a good enough deal for investors.

- The company's fundamentals are solid, with steady growth in gross loans and net income, but the recent report highlighted the impact of shifting company strategies.

Introduction

As we have been observing in the regional bank industry, many of the companies in its share prices have been plummeting after there was news released of First Republic Bank (FRCB) having liquidity issues and ultimately conceding. This sent shockwaves through the markets and for the case of Northwest Bancshares Inc (NWBI), the share price went down almost 40% from top to bottom. The company is quite small and only has a market cap of $1.55 billion. This left a larger impact on the share price it seems.

However, the valuation doesn't scream a buy right now, despite where the price is now compared to back in February. The most appealing part of the company right now for an investor, I think is the dividend yield of over 6%. The dividend has been consistently increasing for the last 12 years which means that investors do have something to gain from a position here. I just don't think the price is a good enough deal right now. It could have been the case if the Q2 report showed a stronger net income result, rather than a YoY decline. For the moment, I feel NWBI is a hold for investors.

Company Structure

Northwest has been in the financial sector for a very long time, ever since 1896, and has grown its valuation to $1.55 billion. Gross loans for the business have been growing steadily over the last 10 years at a CAGR of 6.84% and this has resulted in NWBI having a ROE of 9.19%.

As for what, NWBI focuses on right now and works with can be described as a state-charted savings bank that offers customers and clients personal and business banking solutions. The company has broadened its offerings and it now includes loan products for one-to-four family residential real estate loans.

Besides the mentioned services, NWBI also offers investment management and trust services title insurance services. This broad set of services and offerings within the company seems to have been very beneficial to them. The most recent earnings report from NWBI showed the loans receivable growing over 30% YoY reaching $132 million in Q2 FY2023.

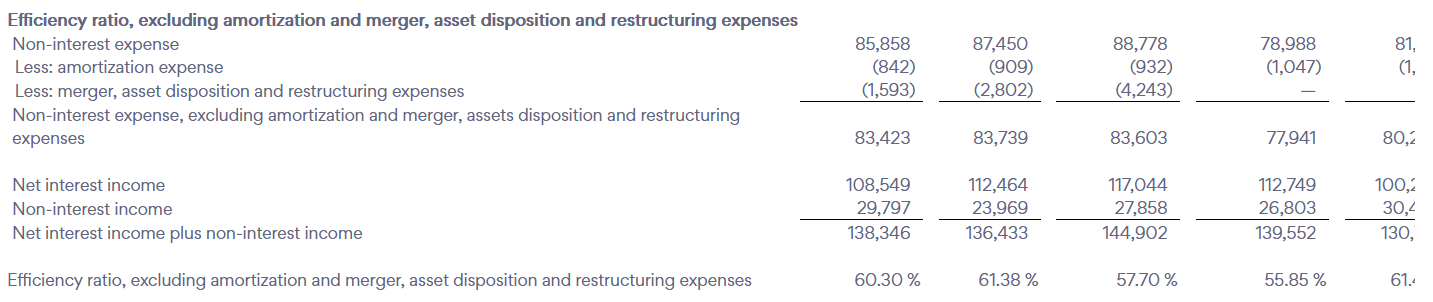

Loan Portfolio (Earnings Report)

Looking at the loan portfolio of the company, we can see that it is very well diversified at the moment. The most prominent positions or loan areas are in 5 or more unit dwellings and nursing homes. These aren't necessarily risky areas to be lending money to I think but they are unlikely to help carry NWBI to a much more profitable stage. The company noted in the last report that the inversion of the yield curve and the change in customer deposit mixes had an impact on the bottom line. The increase in the overall cost of funds grew and outpaced the yield curve. This seems to be persistent throughout 2023 and awaiting any significantly higher EPS report seems unlikely in the short-term.

Fundamentals

The fundamentals of the business seem very solid. The gross loans have been growing steadily over the last 10 years. One factor when assessing banks is that even how much you try and dig up about them regarding risk you never quite get the full picture and often the same goes for the management of the business. Banks are very broad and operate differently compared to regular businesses. So to find the best option and most reliable one in the industry, I often go with historical metrics and performances. Here NWBI shines.

Growth Rates (Seeking Alpha)

The net income has been growing at a strong rate over the last few years. The EPS has achieved a 5.03% CAGR over 10 years and this has helped drive the dividend upwards too it seems. The dividend has been increasing for 12 years consequentially and sits at a payout ratio of 70%. This seems to be a roof for the company I think and a higher payout ratio would most likely lead to a deteriorating business structure. Too much capital distributed harms potential expansions.

Recent Report

The last earnings report didn't come out that long ago and the management had some comments that I think are worthy to highlight. The comments are from the CEO Louis J. Torchio.

-

" Specifically, as a result of the new commercial lending verticals we have recently implemented, commercial loans have grown $416.9 million, or 42.2%, over the past year. As part of this balance sheet shift towards commercial banking, we sold the mortgage servicing rights on approximately $1.3 billion of one- to four-family mortgage loans for an $8.3 million gain, which enabled us to sell approximately $110.0 million of investment securities for an equivalent loss, resulting in no impact to tangible capital ".

This comment highlights very well the impact that shifting company strategies have had on the results of the business. The shifted priority to more commercial banking seems to be a decent path forward as the reliability of the end market seems better than what they've had before.

Risk Associated

In the current economic landscape, numerous banks find themselves facing similar challenges, if not more severe ones. The persistently high-interest rates have put considerable strain on the financial markets, and it is only when these rates begin to come down that we can anticipate some relief in the market risk.

The prolonged period of elevated interest rates has implications across various sectors. For banks, it impacts their lending and borrowing operations, making it more expensive to raise capital and potentially reducing consumer demand for loans due to higher borrowing costs. As a result, banks may experience reduced profitability and face difficulties in generating new sources of income.

{kind=link}

Moreover, the uncertain economic environment stemming from the pandemic and other global events has added to the complexities faced by banks. Heightened market volatility, fluctuating investor sentiment, and changing consumer behavior have created a challenging landscape for financial institutions.

Investor Takeaway

For investors that seek a dividend opportunity at a great price, I, unfortunately, don't think NWBI is there right now. A dividend of over 6% makes sense to take part for investors already in the company. But with the share price trading at a P/E of 12, or 23% higher than the sector. That is a premium rarely worth paying I think. NWBI has historically traded at a quite high premium, averaging over 14 in the last 5 years. But that isn't to say now makes it worth buying into. There is still some downside risk for buying right now and I think investors are better off holding shares right now instead.

For further details see:

Northwest Bancshares: Great Dividend, Not So Great Price Though