NWHUF - NorthWest Healthcare REIT: Debenture Yields Reach 14%

2023-11-29 14:10:20 ET

Summary

- In our last coverage, we upgraded NorthWest Healthcare Properties Real Estate Investment Trust to a "Hold" from a "Sell" due to reduced downside risks.

- The stock crashed through our suggested bottom levels near $4.50/.

- We analyze the Q3-2023 results and refinancing risks and tell you why the debentures look like your best bet here.

Note: All amounts discussed are in Canadian dollars. All quotes and prices refer to the TSX.

On our last coverage of NorthWest Healthcare Properties Real Estate Investment Trust ( NWH.UN:CA ) ( OTC:NWHUF ) we upgraded the beleaguered REIT from a "Sell", while noting that the upgrade only meant that the downside risks had reduced, not gone away.

Those asset sales need to come in fast and furious as based on their AFFO metrics, interest coverage likely declines below 1.5X in 2024. That is dangerous territory and where things can break and covenants can be tripped. At present with a price of $5.37, we are upgrading this to a "Hold" and removing our Sell rating. This reflects a more appropriate price for the risks, though we think we are likely to visit $4.50 before a bottom.

Source: Buy High-Sell Low, Why The Remaining Distribution Could Go

The $4.50 number was another nod to the perennially optimistic bent that we have. The stock went as low as $3.89 before rebounding to $4.53.

As part of our update, we look at the Q3-2023 results, the refinancing risks and the debenture redemption extension.

Q3-2023

NorthWest delivered an inline quarter for Q3-2023 with funds from operations coming in at 14 cents per unit. Adjusted FFO (AFFO) was at 13 cents and both were significant decreases over the prior year.

{kind=link}

NorthWest Q3-2023 Financials

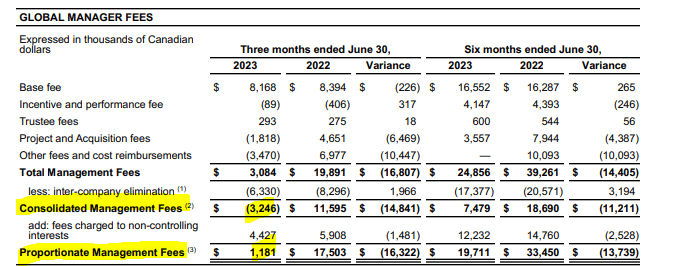

The key thing to keep your eye on is the interest coverage ratio, which came in at 1.82X. This was actually an improvement over the last quarter, despite a rising interest expense level. One driver here was the increase in management fees.

{kind=link}

NorthWest Q3-2023 Financials

We show the Q2-2023 numbers below as a comparative.

{kind=link}

NorthWest Q2-2023 Financials

Other factors that helped maintain this level of interest coverage came from the strong increases in net operating income (NOI) from inflation adjustments. This created a 3.7% increase in same property NOI despite a 100 basis point drop in occupancy levels.

The REIT which has seen some turbulence in its top management made more changes in this area. Craig Mitchell was appointed the REIT’s permanent CEO, and Karen Martin has been appointed interim CFO, replacing Shailen Chande. This is hopefully a good new direction as the previous management's empire building strategy is why we are where we are today.

Outlook

You are likely to get the mandatory "their properties are so great" comment at some point. So let us acknowledge that. Their properties are great, but won't play a role in whether NorthWest makes a great investment. You heard that right. As we have been saying for well over a year, the REIT is leveraged to the maximum as they have combined toxic levels of debt with good properties. This mixture has been made far worse by two other factors.

1) They are using a valuation on their own asset management business in their debt to gross asset value calculation. That is not a hard asset by any stretch of the imagination. If you take that out of the equation, their leverage goes from bad to awful.

2) They went all-in into floating rates and are paying a heavy price.

So it is now a liquidity battle and whether they make it or not, will depend on the largesse of the credit markets. On that front, just observe some of the interest rates these guys are now paying.

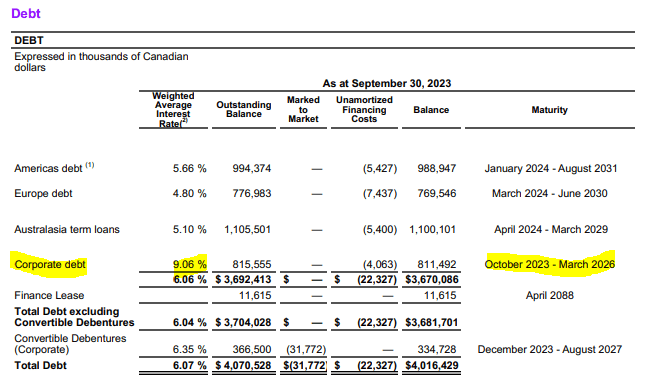

On August 2, 2023, the REIT executed an interim non-revolving tranche under its revolving credit facility to increase availability by $50.0 million. The tranche matured in October 2023. The facility is secured by certain assets in the REIT's Americas portfolio and it bears interest ranging from 10.6% to 13.8%. In September, the REIT further amended its credit facility by extending the maturity date of its non-revolving credit facility tranche with an outstanding balance of $173.2 million by one year to January 2025, The facility bears interest ranging from 10.37% to 10.55% (previously 9.97% to 10.37%).

On October 25, 2023, the REIT executed a term loan for total proceeds of $140.0 million, bearing initial variable interest of 11.6%, maturing on April 26, 2025. The loan is secured by certain Brazil properties. The proceeds were used to repay the $50.0 million revolving credit facility maturing on October 31, 2023 bearing interest at 12.31%. The remaining proceeds were used to repay additional variable rate debt. On November 1, 2023, term debt of $783.0 million pertaining to the REIT's Australasian JV, which is equity accounted in the REIT's financial statements, has been refinanced, extending the weighted average term to maturity by 1.3 years, reducing interest expense by 0.12% and increasing total availability by $13.1 million (A$15.0 million).

Source: NorthWest Q3-2023 Financials

Some might consider these one-off examples, but the entire corporate debt structure is now at over 9%.

{kind=link}

NorthWest Q3-2023 Financials

The REIT also went out of its way to extend the maturity of its maturing debentures and successfully got it done using 10% interest rates and a 2% incentive payment.

Northwest Healthcare Properties Real Estate Investment Trust (the ‘ REIT ‘ or ‘ Northwest ‘) is pleased to announce that holders of its ‘Series G’ Convertible Unsecured Subordinated Debentures due December 31, 2023 (TSX: (NWH.DB.G:CA) passed an extraordinary resolution approving certain amendments to the Debentures previously announced (the ‘ Amendments ‘) at a meeting of Debenture holders held today (the ‘ Meeting ‘).

The adoption of the Amendments was overwhelmingly supported by the Debenture holders who voted by proxy or in person at the Meeting, with the adoption being approved by approximately 89.24% of the principal amount of the Debentures voted (either in person at the Meeting or by proxy).

Craig Mitchell, Northwest’s CEO, commented, ‘Management continues to take steps to renegotiate and extend its near-term debt maturities. In addition to several previously announced credit facility and term loan extensions that we have successfully completed in the past few weeks, Debenture holders today voted to extend the maturity of the Series G debentures from December 2023 to March 2025.’

‘Northwest has eliminated all 2023 debt maturities, and over 60% of its 2024 debt maturities, giving the REIT added financial flexibility. We would like to thank our Debenture holders for their support, as we continue to work to take steps to strengthen our capital structure and set up the REIT for future growth.’

Source: NorthWest Healthcare Website

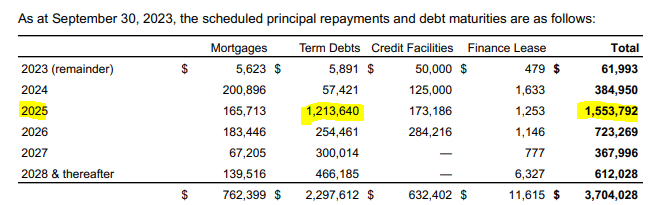

While that sounds great, just have a look at what is left to refinance. Almost $400 million in 2024 and $1.55 billion in 2025.

{kind=link}

NorthWest Q3-2023 Financials

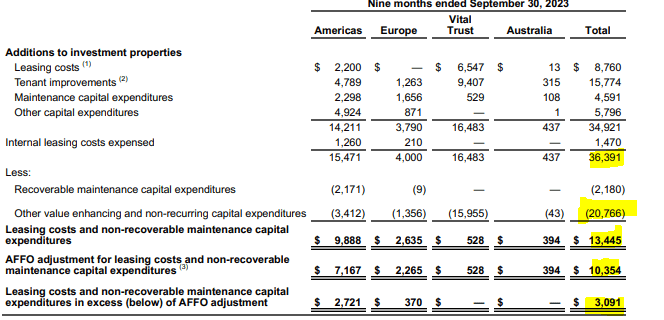

The REIT also has almost no organic cash flow after distributions to help with this. This is even after the large reduction to the distribution. This large property base requires a lot of capex and some of this does not show up in the AFFO numbers. For the nine months ended September 30, 2023, the REIT spent $36.4 million in leasing and capex costs but $20.77 million was considered to be "value enhancing".

{kind=link}

NorthWest Q3-2023 Financials

We are not debating whether or not these might be value enhancing or not. Our point is that an asset base of this size requires a lot of capex and it will drain badly needed liquidity from the REIT. In other words, the AFFO numbers overstate the cash flow capacity of the firm.

Verdict

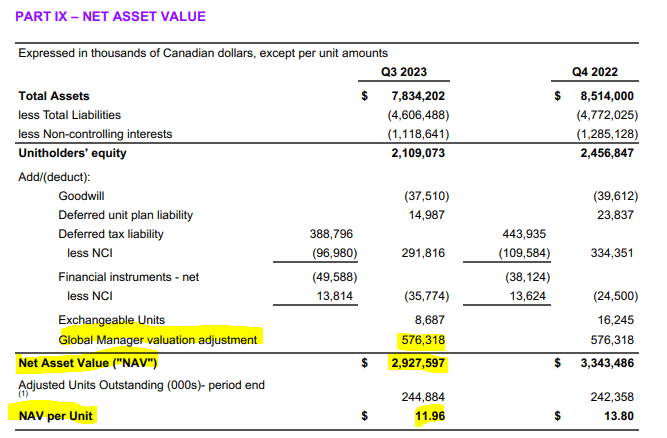

The REIT assesses its NAV at $11.96. That is derived by valuing the management business at close to $575 million.

{kind=link}

NorthWest Q3-2023 Financials

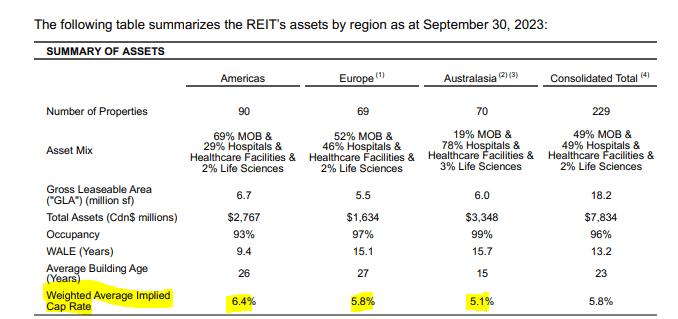

The cap rates for the properties also look slightly optimistic, especially in Australasia.

{kind=link}

NorthWest Q3-2023 Financials

If the REIT believes in these numbers, then we should be seeing at least a few more asset sales instead of signing up for more loans at double digit rates. Perhaps we will see some more asset sales in Q1-2024. Financial conditions have eased remarkably since the end of Q3-2023. A more negative number below means easier conditions.

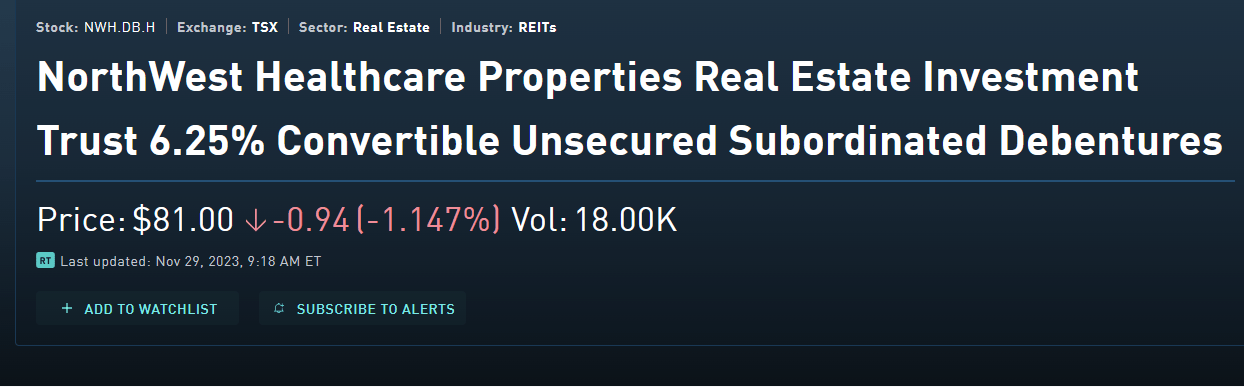

So in the face of that and a wide discount to NAV, it would be imprudent to get extremely bearish on the stock. But the valuation is hardly appealing on other metrics. The REIT is trading at close to 11X AFFO. There are far too many alternative REITs offering better risk-reward. Even for NorthWest Healthcare, the three debentures outstanding offer 12.5% to 14% yields to maturity. Below we show the H debentures maturing in August 2027 (NWH.DB.H:CA) which offer a 13.42% yield to maturity.

{kind=link}

TMX

So chasing the common stock requires a very high degree of optimism, which we lack at present. We rate this a hold and suggest bulls look to the NWH.DB.G under $92.00 (currently at $95.30) as the best setup for a trade.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

NorthWest Healthcare REIT: Debenture Yields Reach 14%