NWHUF - NorthWest Healthcare REIT: JVs Debt Reduction And An Upgrade

2023-06-18 01:45:32 ET

Summary

- We had switched from a bearish view after Q3-2022 results.

- The stock has cooperated and dropped 27% since.

- We tell you why we are giving this an upgrade.

NorthWest Healthcare Properties REIT ( NWH.UN:CA ), ( OTC:NWHUF ) has been an instructive case study. The REIT which was once one of our favorites, slowly and steadily eroded our confidence. It was deals after deals and constant issuance of stock below NAV that changed our view point. The impact was clearly there for anyone studying the long term trajectory of adjusted funds from operations (AFFO). Despite all the deal making the AFFO kept going lower. That is what happens when you buy low cap-rate properties with variable interest rates and issue your own stock at below NAV. Basic math meeting blatant empire building. While we had switched off our buy rating a long time back, it was after Q3-2022 that we first threw in an outright "Sell".

So far, NWHUF has pretty much had to pay top dollar for all refinancings that we have seen year to date. Weighted rates are far higher today across the globe and headed higher for at least the next six months. Equally important, a quick rate cutting cycle is not in the cards. We think when all is said and done, interest coverage will deteriorate further and NWHUF will have a hard time holding on to even a 17 or 18 cent quarterly AFFO.

Source: Q3 2022 Shows Trouble Is Brewing

That has worked and NorthWest has lagged the broader market by 35%.

Seeking Alpha

This has happened despite the dividend being maintained, contrary to our expectations. But we are having a slight change of heart for three reasons. We explain below.

Reason One: The Deal Got Done

Market conditions have improved since late October and perhaps that was the extra help that the REIT needed to get some asset sales through. The UK property sale was important to take some pressure off the company's AFFO and reduce leverage levels.

On June 7, 2023, the REIT and an institutional investor (the “Investor”) waived conditions and finalized terms on the previously disclosed UK JV including an investment into the REIT’s existing UK structure which holds a portfolio of 14 UK hospitals. The transaction, which is in line with the REIT’s Q1-2023 IFRS value, includes the assumption of associated debt and other customary adjustments resulting in net consideration of approximately $276 million (£165.8 million). The UK JV will be owned 70% by the Investor and 30% by the REIT and will be externally managed by the REIT for market-based management fees.

Source: NorthWest Healthcare

We will note here that the entire UK portfolio was valued near $620 million in 2020 after the second purchase. So this is not all of it. But the REIT definitely took a hit on this sale. The REIT took a $151 million bath on the value of all of its properties in Q1-2023 and we are certain a good deal of it was related to this sale.

NorthWest Q1-2023 Financials

NorthWest also closed a second sale at a relatively attractive multiple and the best news was at the end.

On May 31, 2023 the REIT closed the sale of Bakersfield Hospital located in California, USA for $76 million (US$56 million) at a 6.5% capitalization rate. Bakersfield hospital is a high-quality property but was considered non-core owing to it being the only acute care hospital in the REIT’s US portfolio. This sale represents the first sale from the REIT’s previously disclosed $340 million non-core asset sale program that is expected to be substantially completed in Q3-2023.

Collectively, the sale of 70% of the REIT’s UK assets and the sale of Bakersfield Hospital will generate net equity for the REIT of approximately $300 million. Proceeds will be used to repay debt with a weighted average interest rate of 8.2% and result in proportionate leverage decreasing from 57.6% to 53.1%.

Source: NorthWest Healthcare (emphasis ours)

Reason 2: AFFO Run-Rate Trending Higher

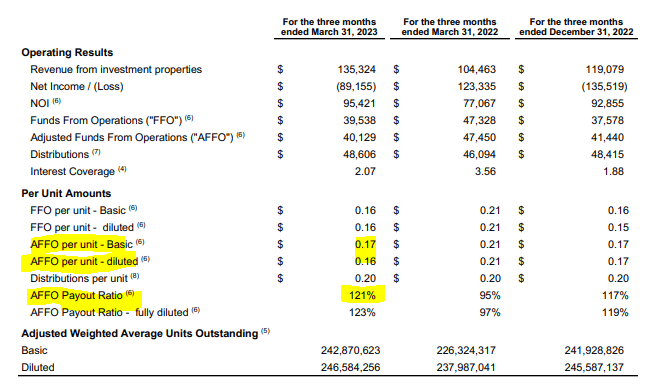

While Q1-2023 results did not have any major surprises, the AFFO was slightly better than what we expected.

{kind=link}

NorthWest Q1-2023 Financials

Yes, granted the payout ratio now over 120% is a very big red flag, but we actually expected worse. The saving grace was that same property Net Operating Income (NOI) was strong and helped the final numbers.

Reason 3: Valuation Is Better

It is one thing to have a sell call when consensus is bullish and the stock is trading at 16X our AFFO estimates. It is another to press that call when the stock has dropped 27% and the AFFO has actually come in better. We are now looking for 72 cents in AFFO after the interest rate hedging and new management fees for the JV. So our Sell call came in at 16X and we are at close to 10.5X today.

Verdict

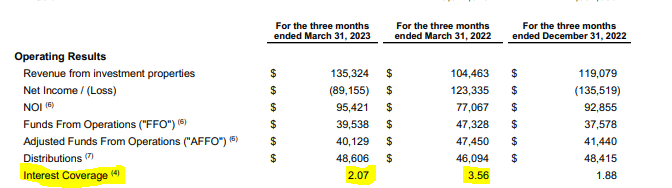

At 10.5X AFFO we don't think a case can be maintained for a Sell rating. Sure it can go down further. The dividend is still not covered and the company's interest rate coverage is near 2.0X. That coverage was over 3.5X in 2022.

{kind=link}

NorthWest Q1-2023 Financials

The company still has a massive US side portfolio that it planned to sell, but cannot find buyers for.

NorthWest Healthcare Properties REIT has made its debut in the U.S. market with a $765-million portfolio acquisition, expected to close in Q2 2022.

The portfolio is comprised of 27 health care properties including seven hospitals, five micro-hospitals, and 15 medical office buildings totaling 1.2 million square feet.

The current plan for the REIT is to bring an investment partner into the portfolio by the end of 2022 , although Dalla Lana did not disclose details on this or on the origin of the U.S. portfolio, only that it was an “institutional vendor.”

Thanks to the planned completion of a U.K. joint venture, its planned U.S. portfolio and global health care precinct initiatives, all of which are expected to close later in 2022 , the REIT’s total assets under management plus capital commitments are expected to increase to approximately $20 billion in the near-term.

Source: Renx (emphasis ours)

So there are negatives, but the properties are indeed excellent (we have visited a few) and they are performing quite well. So these offsets along with the valuation compression gets us to a "Hold/Neutral" rating. Investors might be curious as to why we are not focusing on the newly announced buyback. Honestly, management has lost all credibility with us as they have issued stock so many times far below NAV. Even now, their dividend is not covered and in all likelihood won't be covered in 2023. So the idea that one should get excited over a largely symbolic buyback, is not exactly appealing. For those looking for a play, we would suggest the debentures trading on TSX.

{kind=link}

TMX

Those have an 8.71% yield to maturity in 4.2 years. Those look interesting.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

NorthWest Healthcare REIT: JVs, Debt Reduction And An Upgrade