NWN - Northwest Natural: Can Slow And Steady Win The Race?

2023-03-31 07:42:43 ET

Summary

- In October 2022, Northwest Natural Holding Company closed its largest water and wastewater acquisition to date, Foothills.

- This acquisition increased NW Natural Water's number of connections by 70% and serves approximately 25,000 connections in Yuma, Arizona's Foothills area.

- NW Natural has been slow to grow its EPS. Since 1995 earnings per share have only increased by around 50% in aggregate.

- Likely a big part of the reason why NWN's EPS growth has been so much slower than its peers is due to its reluctance to grow its debt load at the same rate as its peers have.

Introduction

Hello everyone, today I'd like to highlight one small but interesting Utility company by the name of Northwest Natural ( NWN ), a gas and water utility provider primarily serving, you guessed it, the northwestern portion of the USA.

As investors batter down the hatches, and brace for a potential recession, many turn to utility stocks, famous for their consistency and reliability as investments. Their regulated cash flows often serve as an inflation and uncertain hedge, albeit with arguably less upside.

And well if you're looking for reliability, Northwest Natural just might have it for you.

Take a look at that chart, if you invested your money in NWN in the early 70s you could have grown your investment by 2.6K%!

...If only I was alive back then to do such a thing.

Not to mention that dividend which has grown, year over year, for 66 years straight (even YCharts can't look that far back)! This makes NW Natural one of the rare few dividend kings.

But the company is still kicking, reliably generating income and capital appreciation for its investors, and with a sub-$2B market cap, this company may have a long runway to go yet.

Overview

Northwest Natural is a long-established energy company with over 160 years of experience serving the Pacific Northwest, talk about history!

The company owns and operates NW Natural Gas Company, which provides natural gas service to approximately 2.5 million people in more than 140 communities in Oregon and Southwest Washington. NW Natural also owns NW Natural Renewables Holdings and NW Natural Water Company, which provides water distribution and wastewater services to communities throughout the Pacific Northwest, Texas, and Arizona.

And while gas has historically been its bread and butter, the company is keen to talk more and more about its activities within the water utility sub-sector.

From Gas to Water: Foothills Acquisition

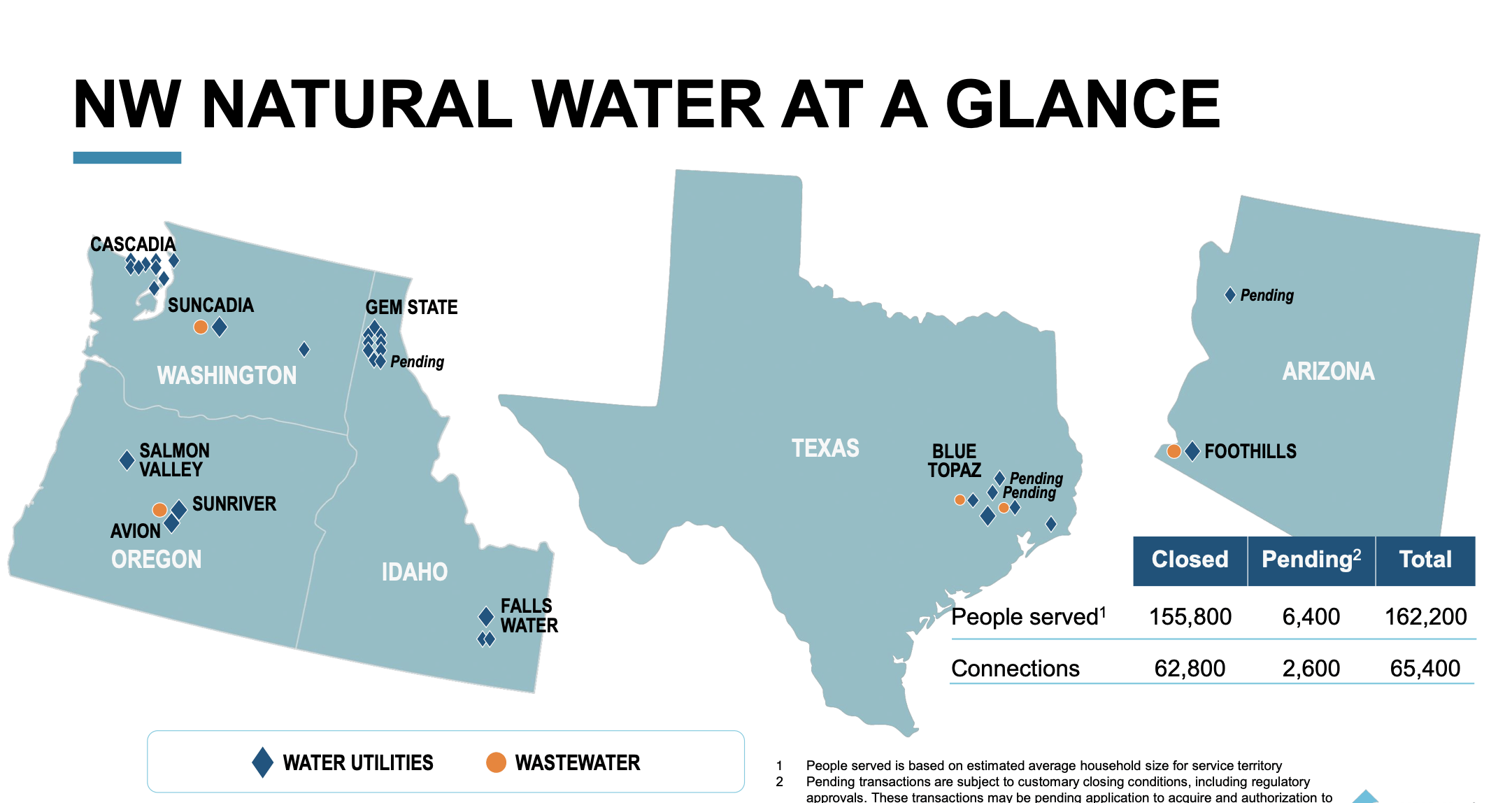

NW Natural Water at a Glance (NW Natural Investor Relations)

{kind=link}

In October 2022, Northwest Natural Holding Company closed its largest water and wastewater acquisition to date, Foothills. This acquisition increased NW Natural Water's number of connections by 70% and serves approximately 25,000 connections in Yuma, Arizona's Foothills area.

The acquisition provided NWN a foothold in Arizona, which management says sets them up with opportunities for additional acquisitions, and positions the company well to serve a growing community with significant development opportunities.

Going forward, NWN plans to continue acquiring water and wastewater infrastructure companies that align with its acquisition strategy. The company is optimistic about the upgrades being driven by federal and state agencies, citing the EPA which estimates that nearly $750 billion will be needed in capital expenditures for water and wastewater infrastructure nationally through 2040.

NWN's investment plan includes approximately $90 million to $110 million in water infrastructure improvement through its five-year 2023-27 capital investment plan which should help them capitalize on that growing need.

Financials

Now that we've gotten the overview out of the way let's get down to the brass tax... what has NW Natural's financial performance looked like over the years, especially in relation to its peers?

Within this article, I'd like to highlight revenue growth, EPS growth, debt load, and returns on invested capital as I believe these are the most relevant metrics for this company.

Revenue

Right off the bat, we can see that NWN has not been the fastest-growing company of all time, nor has it been the fastest among a this peer group of gas-focused utilities. Since 1995 they've roughly tripled their revenue, impressive, but much slower than the growth of Chesapeake ( CPK ) or Spire ( SR ).

Revenues peaked for NWN in the mid-00s after declining significantly post-GFC. They are only now coming close to where they once were. Going forward I am expecting more predictable revenue growth stemming from its water operations which should have even less variable demand than gas.

Normalized Diluted EPS

Even more so than revenue, NWN has been slow to grow its EPS, since around 1995 earnings per share have only increased by ~50%, much less than Sprice, RGC ( RGCO ), and way behind Chesapeake's 642%. This is indeed quite slow, but I am willing to cut them some slack due to their conservative business model which favors stability over growth to help support their dividend king status.

Debt Load

Likely a big part of the reason why NWN's EPS growth has been so much slower than its peers is due its reluctance to grow its debt load at the same rate as its peers have.

For example, yes Chesapeake has grown earnings by over 600% per share, but it has also expanded its debt load by over 2000% in that same time period. NWN's increase of 363% looks much more subdued by comparison.

Return on Invested Capital

Over the past few decades, NWN has generated 3-5% returns on invested capital on average potentially indicating they were/are running out of growth opportunities. Given the increased emphasis on water utility acquisitions perhaps management sees this as vertical to reignite growth through a larger investable universe, perhaps with better returns on capital down the line.

The jury is still out on that one.

Compared to its peers, NWN has performed somewhat below average, its 3.5% ROIC is relatively in line with what Spire has achieved and only a bit below RGC Resources. Chesapeake stands out as the top performer for ROIC among this group.

Valuation

At 17.74x forward earnings, NWN boasts an earnings yield of ~5.6%, which is relatively in line with its historical trading range and a bit below peers like RGC and Chesapeake. Spire has the lowest valuation at 16.7x forward earnings relative to the group.

Conclusion

Ultimately, it's my view, that an investment in Northwest Natural comes down to one sticking point, risk tolerance. Are you the sort of investor looking for growth, maybe you're less concerned about high debt, well in that case, NWN may not be for you. Maybe you already have enough growth in your portfolio, and maybe what you are looking for is a bit more stability to help weather the turbulence in the market, well then NWN could actually be a great fit.

A 5.6% earnings yield that grows 2-5% per year sounds like a much better investment to me than a 30-year treasury which still yields less than 4%.

All in all, I rate Northwest Natural a Hold.

This one is going to come entirely down to your personal risk tolerance level and financial goals.

Thanks for reading!

For further details see:

Northwest Natural: Can Slow And Steady Win The Race?