SWX - Northwest Natural: Some Strong Fundamentals But Also Facing Headwinds

2023-12-26 10:22:16 ET

Summary

- Northwest Natural Holding Company's stock price has declined 16.24% over the past year, underperforming the broader market and the utility sector.

- The company's customer growth rate has slowed, potentially due to rising interest rates and population decline in certain areas.

- Northwest Natural Holding has stable cash flows and a relatively high dividend yield, but its net debt-to-equity ratio has increased and its valuation is considered expensive compared to peers.

- The company may be adversely if winter forecasts are correct.

- The 4.98% dividend yield is higher than its peers and appears to be sustainable.

Northwest Natural Holding Company (NWN) is a natural gas utility that operates in the Pacific Northwest states of Oregon, Idaho, and Washington. The company also owns a water utility that serves the above states plus Texas and Arizona:

{kind=link}

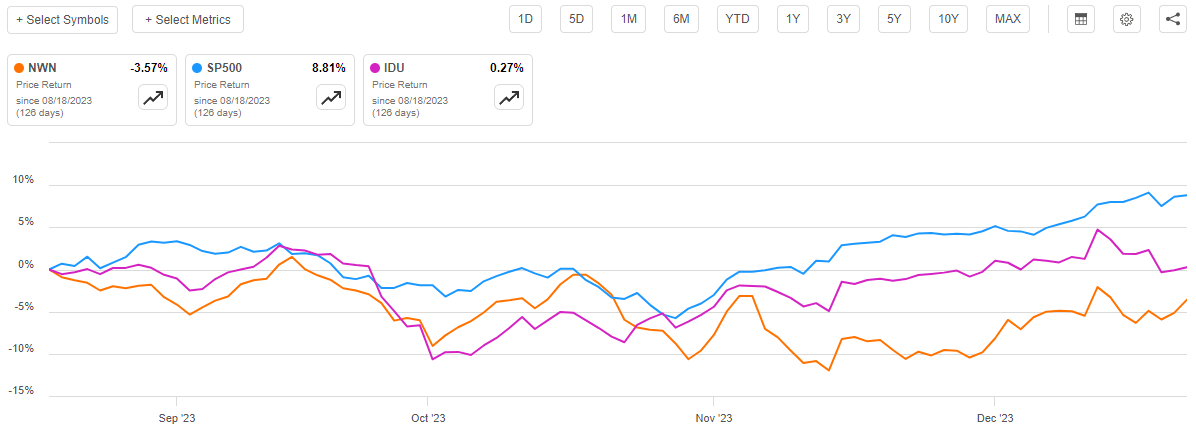

The utility sector in general has long been popular with risk-averse investors such as retirees. This is because of the general stability of the companies in it. Unfortunately, the sector has struggled somewhat in the market over the past few years as rising interest rates have applied downward pressure on their stock prices. As we can see here, Northwest Natural Holding’s stock price is down 16.24% over the past twelve months. This is considerably worse than the broader stock market, as represented by the S&P 500 Index ( SP500 ):

{kind=link}

The stock has also not benefited from the recent market strength to any significant degree. As regular readers may recall, we last discussed Northwest Natural Holding in the middle of August. The stock’s price is down 3.57% since that time, which is substantially worse than the 8.81% gain of the S&P 500 Index. It is also much worse than the U.S. Utilities Sector ( IDU ), which has been roughly flat since that date:

{kind=link}

The company’s poor performance in the market relative to other stocks, including other stocks in its sector, will probably not attract too many investors to Northwest Natural. The fact that the stock still looks a bit expensive relative to its peers will only add to the general attitude of avoiding the stock. However, this does not mean that the company has nothing going for it. Let us have a closer look at Northwest Natural and attempt to determine what action might be most appropriate for us as investors with respect to this company.

About Northwest Natural Holding

As mentioned in the introduction, Northwest Natural Holding is primarily a natural gas utility that operates in the Pacific Northwest states of Oregon, Idaho, and Washington. This is a very large area geographically, but many parts of the Pacific Northwest are not very heavily populated. As such, the company only provides natural gas service to approximately 2.5 million customers. That is still sufficient to make it one of the largest utility companies in the United States in terms of customer count, but it is not an especially large number when we consider the square mileage of the company’s geographic reach. It does differ somewhat from an electric utility though, in that its service area consists of parts of those three states as opposed to the entire state. A natural gas utility does not usually operate in areas that do not have a sufficient population density to justify the cost of running natural gas lines. This is why many people who live in more rural areas have propane or oil heat instead of natural gas.

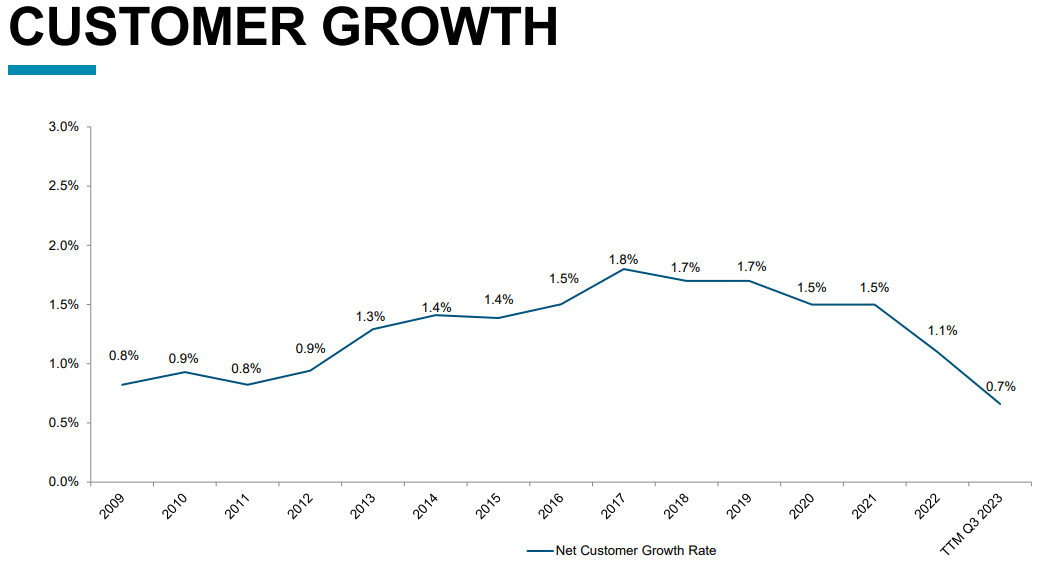

In previous articles on Northwest Natural Holdings, we discussed how the company has been actively growing its customer count. As there are still a number of people in the company’s geographic area who do not have natural gas services, this is not that difficult to accomplish. As we can see here, the company’s customer count increased by 0.7% in the trailing twelve-month period:

{kind=link}

As I pointed out in my last article on Northwest Natural Holding:

This is something that is very nice to see. After all, adding customers is one of the few ways that a company like this can grow. As utilities tend to be geographically confined to a single area by regulations, it is also largely out of the company’s control. After all, a company cannot force people to move into its service territory, nor have I ever seen a utility company attempt to convince people to move.

We do notice though that the company’s customer growth rate has been slowing in recent months. The company’s customer growth count was at 1% during the first quarter of this year, so if it is now at 0.7% then it clearly slowed down during the second and third quarters. This may not be surprising when considering where interest rates have been over the period. I have seen mixed reports about the impact that today’s high mortgage rates relative to most of the past decade have had on home sales. The general consensus though tends to be that people have been less willing to move or construct new real estate in certain areas than they were back in 2021 or earlier. That could be partly responsible for the slowdown in customer growth that Northwest Natural Holding has been experiencing. With that said, the current trend that we see here is still much better than some other utilities that have been seeing their customer base decrease in size.

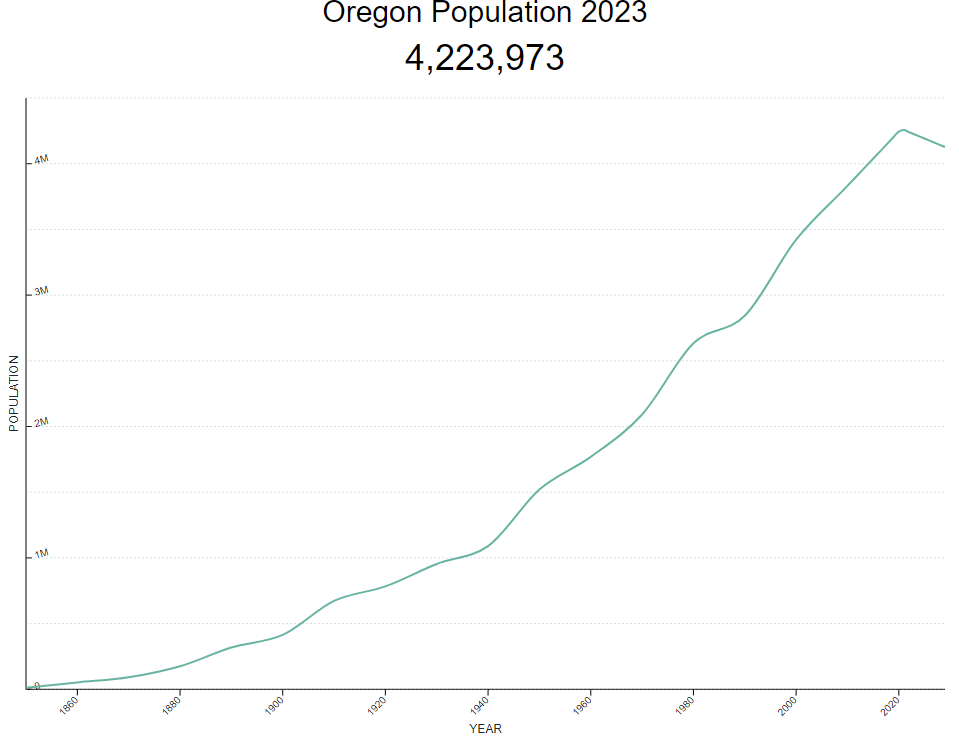

There may be some customer growth headwinds for Northwest Natural Holding going forward. In particular, the state of Oregon is expected to experience a population decline over the remainder of this decade:

{kind=link}

The U.S. Census Bureau projects that the state’s population will be 4.1 million by 2029, down from today’s figure. This could have negative effects on Northwest Natural’s ability to increase its customer count in that state, depending on the areas that experience the population shrinkage.

Fortunately, both Washington and Idaho are expected to see the exact opposite effect over the period. Idaho, in particular, is the second fastest-growing state in the country right now as people leave the coastal areas and move inland. In its third-quarter conference call , Northwest Natural Holding provided no real additional information about the demographics in its service area in the Pacific Northwest. It did state that it expects that it will continue to see customer growth, but it did not specifically state which of the three states in that region it expects growth in. The population trends of the three states may not even be as relevant for Northwest Natural Holding as they would be for an electric utility. As already mentioned, not everybody has any sort of utility-supplied heat source for their homes. The company might be able to generate growth by convincing people to switch from oil, propane, or some similar heat source to natural gas as it expands its distribution network. In fact, it has been suggested that it is doing exactly that in previous investor conferences and press releases. Thus, it may be able to grow its customer count even if a given state that it serves actually experiences a population decline.

Northwest Natural Holding did mention that its water utility operation in Texas is experiencing significant customer growth in its third-quarter conference call:

The county where we operate in Texas experienced a 4.3% population growth in the latest census data. Coeur d’Alene, Idaho posted nearly 2% growth. These factors translated into good customer growth. Collectively, our gas and water utility customer base grew by 4% or approximately 33,000 meters over the last 12 months ending September 2023. That included more than 5,200 gas customers and 28,000 customers, mainly driven by six water acquisitions that we closed during the year.

Overall, this suggests that the company’s customer count continues to grow, which explains why the company’s guidance suggests that it will continue to grow its gas utility’s customer base at an average 1.1% rate over the next five years. The water utility might be able to grow more rapidly, as it did over the past year. However, the water utility business is a much smaller portion of the company’s overall total operation.

As mentioned in the introduction, one of the biggest reasons why utilities such as Northwest Natural Holding are somewhat popular with retirees and other risk-averse investors is that they have remarkably stable cash flows over time. Northwest Natural is not an exception to this rule, although we cannot really tell by looking at the company’s quarterly operating cash flows. Here they are over the past eleven quarters:

{kind=link}

As we can see, the company’s quarterly operating cash flows tend to be all over the place. This is not exactly unusual for a natural gas utility. After all, the primary use of natural gas is as a heating fuel and customers tend to need space heating much more during the winter months than during the summer months. As a customer’s utility bills are dependent on how much natural gas they consume during a given period, we can expect that the company will bring in much more money during the winter than during the summer. We should therefore look at the company’s operating cash flows over a rolling twelve-month period as opposed to quarter-by-quarter. Here are the company’s operating cash flows during each of the past eleven twelve-month periods:

{kind=link}

This certainly shows a great deal of stability over time. As we can see, there are some fluctuations from period to period, but for the most part, the company’s operating cash flows do not vary to nearly the same degree as we might see in companies in other sectors of the economy. I explained the reason for this stability the last time that we discussed this company:

The reason for this inherent stability is that Northwest Natural Holding supplies a product that most people consider to be a necessity for modern life. After all, anyone with a natural gas furnace for heat is going to need the company’s natural gas to heat their homes during the cold winter months in the Pacific Northwest. As such, people will usually prioritize paying their natural gas utility bill before making discretionary expenses during times in which money gets tight.

The biggest risk here is that an unusually warm winter could reduce the need for heating compared to more normal conditions. As Northwest Natural Holding’s cash flows do depend on the amount of natural gas that its customers consume, warm weather that results in lower consumption of natural gas would have an adverse effect. This was the situation that we saw last year as many utilities specifically stated the warm weather as a reason for poor performance.

There are still some areas of the United States that are under the lingering effects of El Nino and have been somewhat warmer than normal so far this winter. The National Oceanic and Atmospheric Administration expects that this winter will be warmer than normal, just like the winter of 2023. As Yahoo! Finance points out :

A warm Pacific Ocean, combined with a lack of snow cover in the northern U.S. and southern Canada, is helping to modify any cold airmass that tries to invade the country.

This could suggest that the Pacific Northwest may be warmer than normal this winter, especially with the warmer-than-normal Pacific Ocean. That naturally could cause Northwest Natural Holding’s financial performance over the twelve months to be adversely impacted by low natural gas demand. This might explain why the stock price has been underperforming the broader U.S. utility sector.

Financial Considerations

As I stated in my previous article on this company:

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt since very few companies have sufficient cash to completely pay off their debt as it matures. That process can cause a company’s interest expense to increase following the rollover, depending on the conditions in the market.

As I have pointed out in a few previous articles, there have been several companies across the utility sector that have been pressured by the fact that interest rates today are substantially higher than they have been in many years. This has certainly been the case for Northwest Natural Holding, as we can see here:

{kind=link}

We can see that the company’s net interest expenses have increased significantly by quite a lot since 2021. During the twelve-month period that ended on March 31, 2021, Northwest Natural paid net interest of $40.7 million, but that figure has since increased to $68.8 million during the most recent twelve-month period. That is a 69.04% increase over the past two years. Naturally, this has an adverse impact on the company’s earnings per share and cash flow growth because the higher expenses offset some of the positive impacts of the company’s growth initiatives that we have discussed in previous articles.

One metric that we can use to evaluate the company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which the company is depending on debt to finance its operations as opposed to its own funds. If this ratio is significantly higher than its peers, then it could be a sign that it is more reliant on debt than may be prudent. That would represent a risk that we should consider before investing in a company.

As of September 30, 2023, Northwest Natural Holding has a net debt of $1.6090 billion compared to $1.2195 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.32 today, which is unfortunately a bit worse than the 1.22 ratio that the company had the last time that we discussed it. This is not a very good sign but let us see how the company compares to its peers. This chart summarizes that comparison:

| Company |

| Net Debt-to-Equity Ratio |

| Northwest Natural Holding |

| 1.32 |

| New Jersey Resources ( NJR ) |

| 1.65 |

| NiSource Inc. ( NI ) |

| 1.70 |

| Atmos Energy ( ATO ) |

| 0.65 |

| Southwest Gas Holdings ( SWX ) |

| 1.55 |

| Spire Inc. ( SR ) |

| 1.62 |

As we can see here, Northwest Natural Holding has seen its leverage increase a bit since we last discussed it following the first quarter of this year. However, it appears that the company is still very conservatively financed relative to many of its peers. The only peer company that has a stronger balance sheet is Atmos Energy. As such, we probably do not need to worry too much about Northwest Natural Holding’s debt load. We naturally do not want its leverage to continue to increase though, so we should watch its numbers going forward.

Dividend Analysis

One of the biggest reasons why investors purchase utilities like Northwest Natural Holding is that they tend to have higher dividend yields than stocks in many other sectors. This is due to their relatively low growth rates. The low growth rate has induced the company to pay out a significant portion of its profits to the shareholders in order to provide a return to investors, and the low growth rate has prompted the market to assign lower multiples to the company than we might find in some other sectors. Thus, the dividend is a fairly high percentage of the company’s stock price.

Northwest Natural Holding is no exception to this general rule. As of the time of writing, the company boasts a 4.98% yield, which is higher than that of many of its peers:

| Company |

| Dividend Yield |

| Northwest Natural Holding |

| 4.98% |

| New Jersey Resources |

| 3.73% |

| NiSource Inc. |

| 3.81% |

| Atmos Energy |

| 2.80% |

| Southwest Gas Holdings |

| 3.86% |

| Spire Inc. |

| 4.74% |

This relatively high yield relative to the company’s peers is something that might appeal to some investors. After all, the high inflation that we have seen throughout the economy over the past two or three years has greatly reduced the purchasing power of our incomes. Thus, we all need to earn a higher level of income in order to maintain a desired standard of living.

As is always the case though, it is important that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since that would both reduce our incomes and almost certainly cause the company’s stock price to decline.

The usual way that we judge a company’s ability to afford its dividend is by looking at its free cash flow. During the twelve-month period that ended on September 30, 2023, Northwest Natural Holding reported a negative levered free cash flow of $83.2 million. That is obviously not enough to pay out any dividends, but the company still paid out $66.5 million to its shareholders. At first glance, this is something that might be quite concerning as the company is clearly not generating sufficient amounts of cash in excess of its bills and capital expenditures to pay the dividends that it sends out to its shareholders.

However, as I pointed out in my previous article on this company, it is quite common for a utility to issue debt and equity to cover its capital expenditures. It will then pay its dividends out of operating cash flow. This is due to the incredibly high costs of constructing and maintaining a utility-grade infrastructure network over a wide geographic area.

During the trailing twelve-month period, Northwest Natural Holding reported an operating cash flow of $283.2 million. That was obviously more than enough to cover the $66.5 million that the company paid out in dividends with a substantial amount of money left over for other tasks. As such, it does not appear that the company is having any real trouble affording its dividend right now. It should be able to sustain the current payment going forward.

Valuation

According to Zacks Investment Research , Northwest Natural Holding will grow its earnings per share at a 3.70% rate over the next three to five years. This gives the stock a price-to-earnings growth ratio of 3.93 at the current price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| Northwest Natural Holding |

| 3.93 |

| New Jersey Resources |

| 2.72 |

| NiSource Inc. |

| 2.30 |

| Atmos Energy |

| 2.42 |

| Southwest Gas Holdings |

| 3.79 |

| Spire Inc. |

| 2.61 |

This is quite unfortunate as the above peer comparison suggests that Northwest Natural Holding is rather expensive at today’s price. After all, it is clearly more expensive than many of its peers when the company’s earnings per share growth is taken into account. Investors sometimes value utilities based on their dividends, rather than earnings per share growth, so that might be what we are seeing here. It is still something that we should consider, however.

Conclusion

In conclusion, Northwest Natural Holding is a fairly solid natural gas utility that operates in the Pacific Northwest. The company has been enjoying a reasonable amount of success in growing its customer counts, particularly in states such as Texas and Idaho. However, Northwest Natural Holding Company stock has been underperforming the sector, and if the National Oceanic and Atmospheric Administration is correct about the winter forecast, then an unseasonably warm winter could weigh on the company’s financial performance for the next few quarters. The dividend yield is quite respectable though, so some investors might be willing to just get paid to wait for things to improve for the company.

For further details see:

Northwest Natural: Some Strong Fundamentals, But Also Facing Headwinds