SWX - Northwest Natural: Worth Accumulating For Safety And A 4.8% Yield

2023-08-18 06:13:00 ET

Summary

- Northwest Natural Holding Company is a natural gas utility serving the Pacific Northwest with stable cash flows and a high dividend yield of 4.80%.

- The company has been steadily growing its customer base and reported a 22.0% increase in total revenue in the second quarter of 2023.

- Northwest Natural Holding plans to invest in infrastructure to expand its rate base and achieve a 4% to 6% growth rate in earnings per share through 2027.

- The company boasts a 4.80% dividend yield at the current price, and it appears to be sustainable.

- The company is trading at a much more attractive valuation right now than it has in a while, so it might be worth slowly accumulating for a safe dividend.

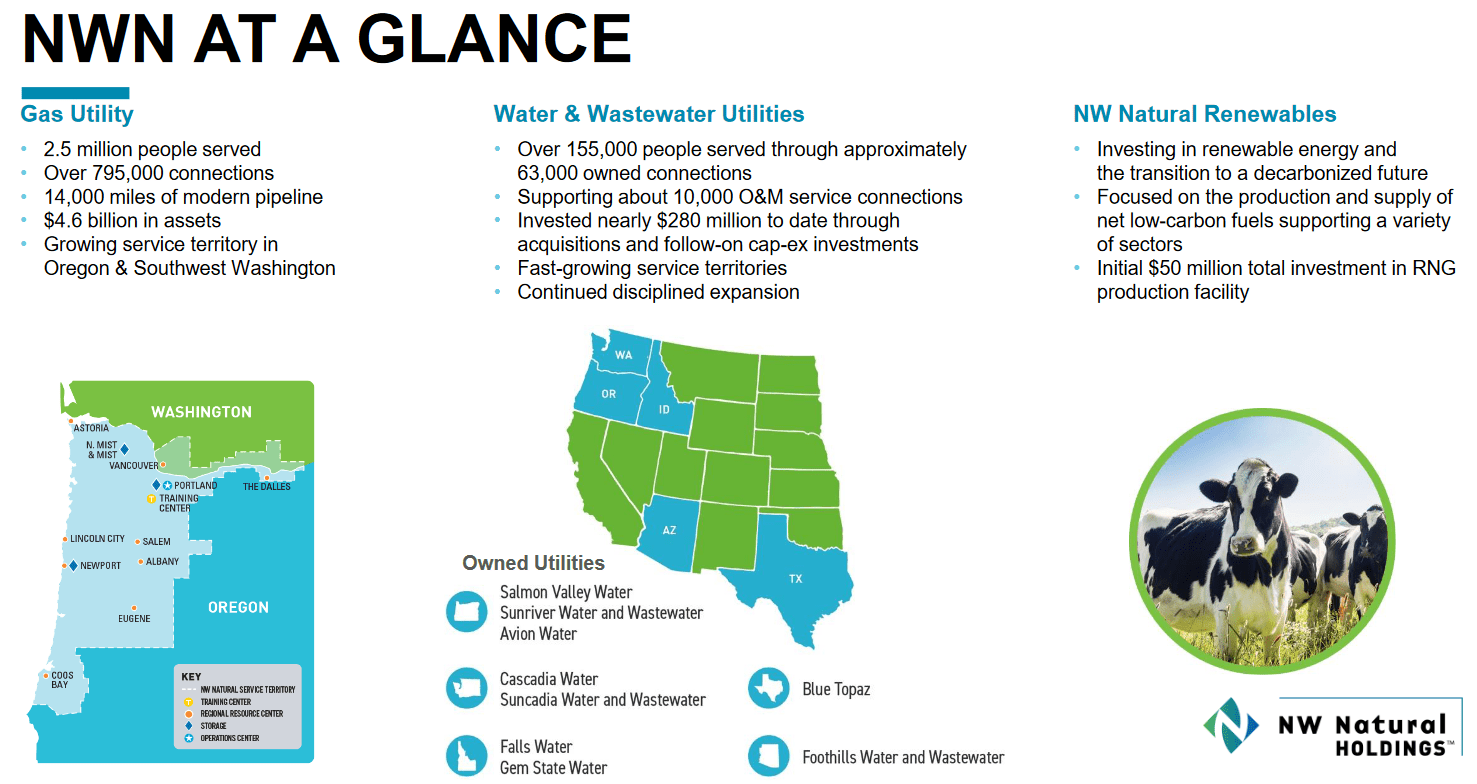

Northwest Natural Holding Company (NWN) is a natural gas utility that primarily serves the Pacific Northwest states of Washington, Oregon, and Idaho, although it also has operations in a few other areas throughout the United States:

{kind=link}

The utility sector in general has long been a favorite of conservative investors, such as many retirees. This is largely due to its stable cash flows and relatively high dividend yields. Northwest Natural Holding is certainly no exception to this as the stock yields an impressive 4.80% as of the time of writing. When we combine this with the company's very reasonable growth prospects, it could make a good investment in today's environment of general uncertainty. Unfortunately, the market has not been particularly interested in natural gas utilities recently, as the promotion of electrification by politicians, activists, and media personalities has caused many people to believe that natural gas utilities may be rendered obsolete in the very near future. However, nothing is further from the truth as we have discussed in past articles, such as this one . This general market aversion has resulted in natural gas utilities generally trading with fairly attractive valuations, particularly when compared to their electric utility cousins. While Northwest Natural Holding does look much more attractively valued than the last time that we discussed this company, it does still look rather expensive for a natural gas utility. However, it might still be worth buying given its general stability and very high yield.

About Northwest Natural Holding Company

As stated in the introduction, Northwest Natural Holding Company is primarily a natural gas utility that serves the Pacific Northwest states of Washington, Oregon, and Idaho. While parts of this territory, especially Idaho, are relatively rural, the company still serves 2.5 million people and boasts approximately 795,000 customers. That represents an increase of 6,400 customers year-over-year, or 0.8%. That is a respectable growth rate for a utility, and it is nice to see it because growing its customer base is one of the only ways that a utility can actually grow its business. We will discuss the company's growth potential in more detail later.

As mentioned in the introduction, one of the defining characteristics of utilities is that they have remarkably stable cash flow over time. Northwest Natural Holding is no exception to this. In the second quarter of 2023, the company reported total revenue of $237.9 million, which represents a 22.0% increase over the $195.0 million that the company had in the equivalent quarter of last year. The company's operating cash flow also exhibits a great deal of stability over time. This chart shows its operating cash flow during each of the past twelve-month periods:

{kind=link}

This was a period of time that included a number of different economic events. For example, the COVID-19 lockdowns of 2020 would be included in some of the earlier periods, which resulted in numerous people becoming temporarily unemployed and falling behind on their utility bills. We also see the inflation of 2021 and 2022 reflected above. Another notable event was the outbreak of the war in Ukraine, which caused natural gas prices to temporarily spike. These prices crashed earlier this year, which is also included in the period of time covered by the chart above. However, none of these events appears to have had an effect on the company's operating cash flow, which remained quite stable over the entire period.

The reason for this inherent stability is that Northwest Natural Holding supplies a product that most people consider to be a necessity for modern life. After all, anyone with a natural gas furnace for heat is going to need that natural gas to heat their home during the cold winter months in the Pacific Northwest. The government even supports this status as a necessity as it offers aid to people that cannot afford to pay for heating. As such, people will typically prioritize paying their natural gas utility bill before making discretionary expenses during times in which money gets tight. There are certainly some signs that money is getting tight for many people, as indicated by the desperate measures that a growing number of Americans are engaging in around the nation. We are also seeing companies like Apple (AAPL) experience quarterly revenue declines, which could be a sign that people are cutting back on luxuries in order to direct their money toward necessities. As such, a company like Northwest Natural Holding could prove quite appealing as its cash flows should hold up just fine regardless of the conditions in the broader economy.

One thing that eagle-eyed readers might note from the graphic provided in the introduction is that Northwest Natural Holding is not exclusively a natural gas utility. The company also operates water utilities and sewage companies in Arizona and Texas (as well as in the Pacific Northwest). However, these are a very small proportion of its operations. In 2022, 92% of the company's net income came from the natural gas utility:

Northwest Natural Holding

As such, we can basically consider this to be a natural gas utility, although the water utilities are located in some of the more rapidly growing regions of the United States so it is possible that they will account for a larger percentage of the company's net income at some point in the future. We can see that possibility in a quote from the company's second-quarter earnings conference call :

On a consolidated basis, our water and wastewater utilities grew 3.1% on an organic basis over the last twelve months. That excludes approximately 30,000 meters we added through acquisitions. Collectively, our gas and water utility customer base grew by 4.4% over the last 12 months.

As already mentioned, the company stated in its earnings press release that the natural gas utility alone increased its customer base by 0.8% during the twelve-month period that ended on June 30, 2023. Thus, the water utility is growing at a much more rapid pace than the natural gas utility. As such, we can assume that the water utility will probably account for a larger proportion of the company's business at some point in the future relative to today. However, that is still a way off and for now, this company can still be thought of as a natural gas utility.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we like to see a company in which we are invested grow and prosper with the passage of time. Fortunately, Northwest Natural Holding is well-positioned to accomplish this. It has two methods through which it is pursuing this goal.

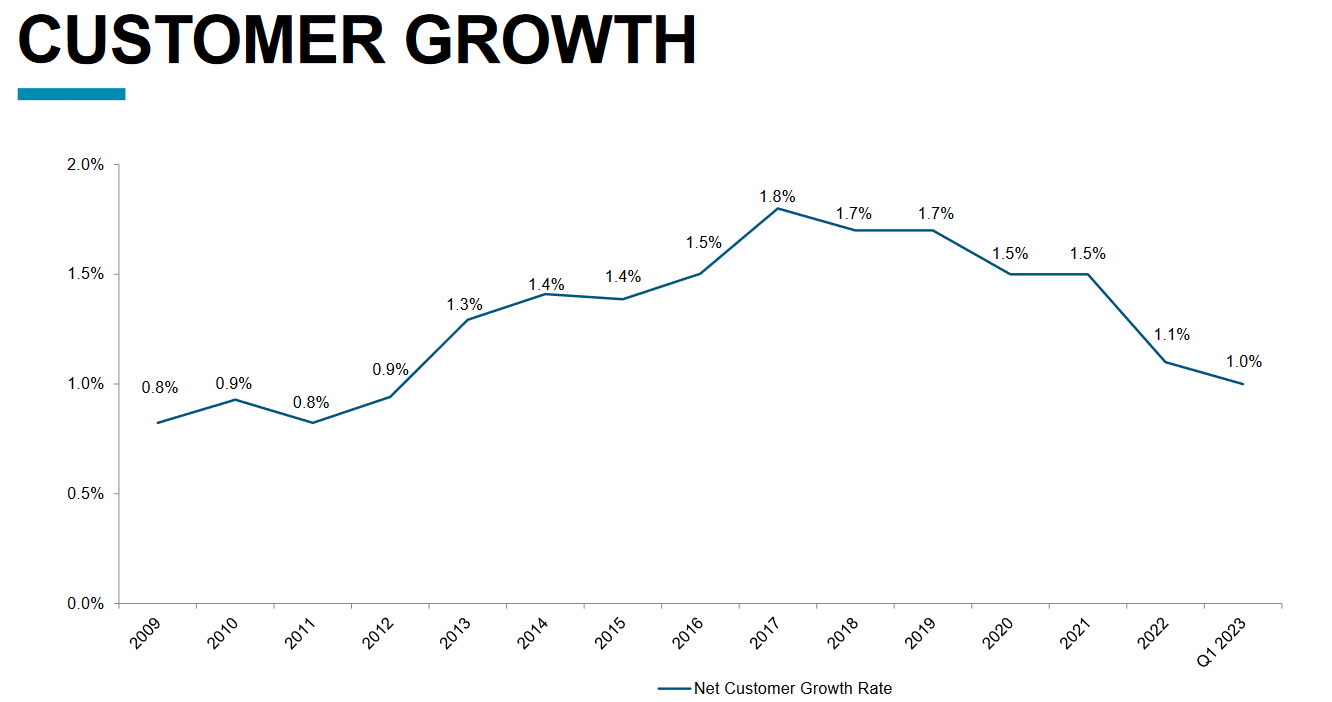

First, Northwest Natural Holding is growing its customer base. This was noted earlier in this article, as the company's natural gas utility served 0.8% more customers at the end of the second quarter of 2023 than it did at the same time during the prior-year quarter. This is the continuation of a long trend of customer growth, however. As we can see here, Northwest Natural Holding has consistently increased its customer count during every single twelve-month period stretching back to 2009:

{kind=link}

This is something that is very nice to see. After all, adding customers is one of the few ways that a company like this can actually grow. As utilities tend to be geographically confined to a single area by regulations, it is also largely out of the company's control. After all, a company cannot force people to move into its service territory, nor have I ever seen a utility attempt to convince people to move. An increase in the company's customer count has a very positive impact on growth, however. After all, more customers means that it has more people paying their monthly utility bills. All else being equal, this results in more revenue for the company and thus more money available to cover its fixed costs. That results in more money being able to move its way down to the bottom-line profits and cash flow.

It seems unlikely that anyone will be satisfied with the slow growth rate that results from simply increasing its customer count, however. As already mentioned, in the most recent quarter the natural gas utility's customer count was only up by 0.8% year-over-year. That is nowhere close to enough to satisfy investors that can achieve much more rapid growth rates in just about any other industry. Fortunately, Northwest Natural Holding has a way to accomplish that. This is by growing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to earn that specified rate of return. The usual way for a company to expand its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure. Northwest Natural Holding is planning to do exactly that as the company currently plans to invest $330 million into its infrastructure over the course of 2023 and then $290 million per year thereafter:

{kind=link}

This is expected to grow the company's rate base sufficiently to allow it to grow its earnings per share at a 4% to 6% rate through 2027. Admittedly, that is not as rapid of a growth rate as some of the other utility companies that I have discussed in recent months. However, when we combine this with Northwest Natural Holding's current 4.80% dividend yield, we see that the stock should be able to deliver a 9% to 11% total average annual return over the next five years. That is certainly a very respectable return on an investment in a conservative utility stock.

Financial Considerations

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt since very few companies have sufficient cash to completely pay off their debt as it matures. That process can cause a company's interest expenses to increase following the rollover, depending on market conditions. As of the time of writing, the effective federal funds rate is at the highest level that we have seen since 2007 so it is a fair assumption that any debt rollover today will cause a company's interest expenses to go up. This is not the only risk of debt, however. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. While utilities like Northwest Natural Holding tend to have remarkably stable cash flow over time, there have been bankruptcies in the sector before, so this is a risk that we should not ignore.

One metric that we can use to analyze the financial structure of a company is the net debt-to-equity ratio. This ratio essentially tells us the degree to which a company is financing its operations with equity as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of June 30, 2023, Northwest Natural Holding had a net debt of $1.5182 billion compared to $1.2403 billion in shareholders' equity. This gives the company a net debt-to-equity ratio of 1.22 today. That is a slight improvement over the 1.24 ratio that the company had the last time that we discussed it, which is nice to see. Here is how Northwest Natural Holding compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Northwest Natural Holding |

| 1.22 |

| New Jersey Resources (NJR) |

| 1.59 |

| NiSource, Inc. (NI) |

| 1.65 |

| Atmos Energy (ATO) |

| 0.61 |

| Southwest Gas Holdings (SWX) |

| 1.50 |

With the notable exception of Atmos Energy, Northwest Natural Holding has the lowest ratio here. This is a clear sign that the company is not overly reliant on debt to fund its operations. That is a good sign considering the current rising-rate environment, and it indicates that we should not have to worry too much about the company's debt load.

Dividend Analysis

One of the biggest reasons why investors purchase shares of utility companies is because they tend to have very high dividend yields. Northwest Natural Holding is certainly not an exception to this, as the company's stock boasts a 4.80% yield at the current price. This is significantly better than the 1.48% current yield of the S&P 500 Index ( SPY ) and it is even quite a bit higher than the 2.67% yield of the U.S. Utilities Index ( IDU ). Northwest Natural does have a long history of raising its dividend on an annual basis, but recent increases have only been a quarter of a cent per share, so they are nothing to write home about:

{kind=link}

The fact that the company steadily increases its dividend annually is something that is very nice to see during inflationary times, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. That can make it feel as though we are getting poorer and poorer with the passage of time, which is a particularly big problem for retirees or anyone else dependent on their portfolios for needed income. The fact that the company increases its dividend annually helps to offset this effect and maintains the purchasing power of the dividend. With that said, Northwest Natural Holding's recent dividend increases have been nowhere close to enough to keep up with inflation, so we still have the problem of our real incomes from this company declining with the passage of time. However, the fact that the company is still raising the dividend means that our purchasing power is not declining as rapidly as it would be with a static dividend.

As is always the case though, it is critical that we ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut because that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company's ability to cover its dividends is by looking at its free cash flow. Free cash flow is the amount of cash that was generated by a company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the amount of money that the company can use for tasks that benefit the shareholders, such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on June 30, 2023, Northwest Natural Holding reported a negative levered free cash flow of $102.3 million. Obviously, this is not enough to pay any dividends, yet the company still paid out $65.8 million to its shareholders during the period. At first glance, this is likely to be concerning as the company does not have sufficient free cash flow to cover its dividend.

However, it is common for utilities to finance their capital expenditures through the issuance of debt and equity. They then pay their dividends out of operating cash flow. This is done because it is incredibly expensive to construct and maintain a utility-grade infrastructure network over a wide geographic area. If the company were to try and pay for all of these expenses out of its free cash flow, it could never provide a return on investment for its shareholders. During the trailing twelve-month period, Northwest Natural Holding reported an operating cash flow of $249.0 million. That was easily enough to cover the $65.8 million that was paid out in dividends and leave the company with a substantial amount of money left over for other purposes. Overall, this dividend appears to be reasonably safe.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Northwest Natural Holding, we can value it by using the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that a stock may be undervalued relative to its earnings per share growth or vice versa. However, very few stocks have such a low ratio in today's richly valued market. This is even more true in the low-growth utility sector. As such, the best way to use this ratio today is to compare Northwest Natural Holding's valuation against its peers in order to determine which stock has the most attractive relative valuation.

According to Zacks Investment Research , Northwest Natural Holding will grow its earnings per share at a 3.70% rate over the next three to five years. This is at the low end of the figure that we used earlier to calculate a projected total return based on the company's rate base growth, but it is in the same ballpark. This earnings growth rate gives Northwest Natural Holding a price-to-earnings growth ratio of 4.05 at the current stock price. Here is how that compares to the company's peer group:

| Company |

| PEG Ratio |

| Northwest Natural Holding |

| 4.05 |

| New Jersey Resources |

| 2.73 |

| NiSource, Inc. |

| 2.36 |

| Atmos Energy |

| 2.55 |

| Southwest Gas Holdings |

| 3.88 |

As we can clearly see, Northwest Natural Holding is significantly more expensive than most of its peers. This could partly be due to the dividend, as utility stocks are sometimes priced in such a way that their dividend yield ends up being at a certain level regardless of the company's earnings growth. Regardless, it might make sense to be cautious and not rush in and buy here, although the stock is down 15.74% year-to-date, so the stock is better priced than it has been in quite a while.

Conclusion

In conclusion, there are some reasons to like Northwest Natural Holding Company today. In particular, the company is one of the few utilities that is delivering reasonably strong customer growth while maintaining very stable finances and an attractive dividend yield. The stock is also trading at a much more attractive valuation than we have seen in quite a while. It might be suffering a little because natural gas is not seen as favorably by some investors as electricity, but its business is certainly not at risk of obsolescence. It might be worth keeping an eye on this company, or even slowly accumulating the stock if you are looking for safety and a respectable yield.

For further details see:

Northwest Natural: Worth Accumulating For Safety And A 4.8% Yield