NWPX - Northwest Pipe: 2024 Can Be An Inflection Year (Rating Upgrade)

2023-12-10 22:04:18 ET

Summary

- Northwest Pipe Company faces near-term headwinds from a reduced backlog and order book, but 2024 could be an inflection year.

- The company's revenue growth has turned negative in 2023, but a meaningful improvement in the bidding market is expected in 2024.

- Margins have declined in Q3 2023, but the medium- to long-term outlook is favorable with improvements in the bidding market and cost reduction initiatives.

Investment Thesis

I last covered Northwest Pipe Company ( NWPX ) in September when I preferred remaining on the sidelines due to the challenging bid market and declining backlog. The stock has corrected ~10% since then validating my stance. While Northwest Pipe Company continues to face near-term headwinds from a reduced backlog and order book resulting from a weak bidding market and high interest rates, I see light at the end of the tunnel and believe 2024 can be an inflection year. The company’s backlog and revenues should return to growth as FY24 progresses with a meaningful improvement in the bidding market, which should support the Engineered Steel Pressure Pipe Segment ((SPP)) segment, and a potential reversal in the interest rate cycle, which should support the Precast Infrastructure and Engineered Systems Segment (Precast) segment. Further, the company should benefit from secular demand drivers like aging waste and wastewater infrastructure which should drive the company's revenue growth in the medium to long term. In addition, the revenue growth should also see gains from initiatives under the “product spread strategy” which should help the company to post good organic growth.

In terms of margins, while there are near-term headwinds from a weak bidding market and volume deleverage, the medium to long-term margin outlook is favorable with benefits from improvement in the bidding market, synergies from integration of ParkUSA, and cost reduction and productivity initiatives. Moreover, operating leverage resulting from sales recovery, especially in the second half of FY24 onwards, should also contribute to margin expansion. Further, the company is trading at a discount versus its 5-year historical averages. Considering a good probability of a return to growth in FY24 and a discounted valuation, I am moving to a buy rating on the NWPX stock.

Revenue Analysis and Outlook

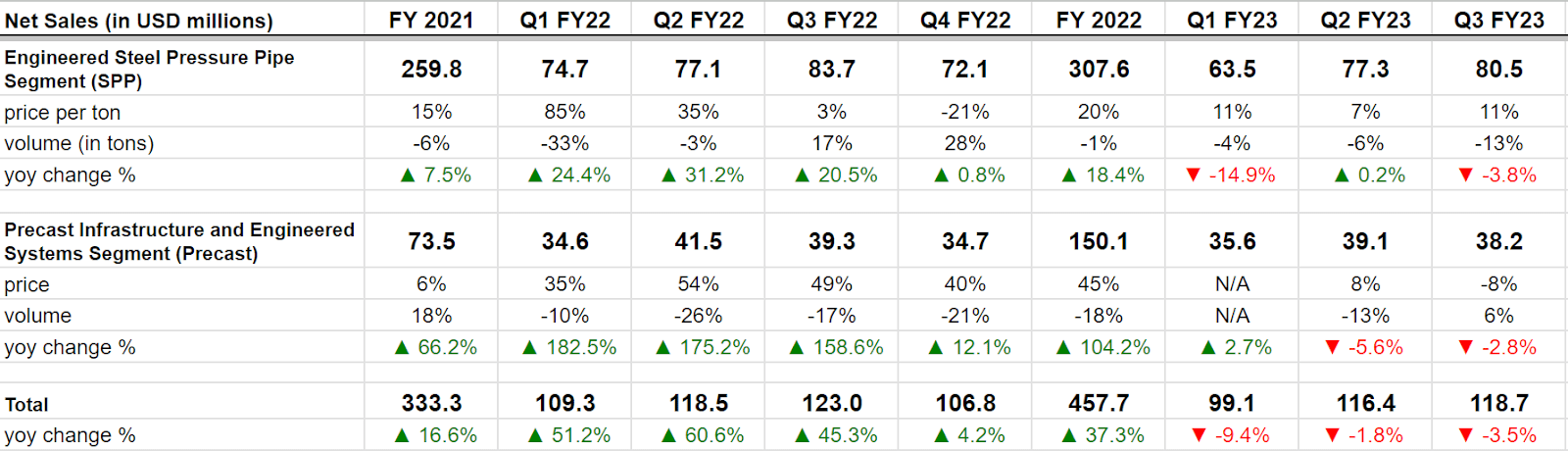

After seeing good growth in FY21 and FY22 driven by healthy end-market demand and acquisitions, the company’s revenue growth turned negative this year. In the third quarter of 2023, the company’s Engineered Steel Pressure Pipe Segment net sales declined 3.8% Y/Y, mainly due to customer-driven contract changes as well as customer-related delays that negatively impacted production timing and resulted in a 13% Y/Y decline in volume (in tons) produced. The Y/Y decrease in SPP's volumes was partially offset by an 11% increase in selling price per ton, driven by a favorable product mix.

The Precast Infrastructure and Engineered Systems Segment (Precast) segment’s net sales declined 2.8% Y/Y due to challenging conditions in the U.S. construction market brought on by higher interest rates. On a consolidated basis, net sales declined 3.5% Y/Y to $118.7 million in the third quarter.

{kind=link}

NWPX’s Historical Revenue Growth (Company Data, GS Analytics Research)

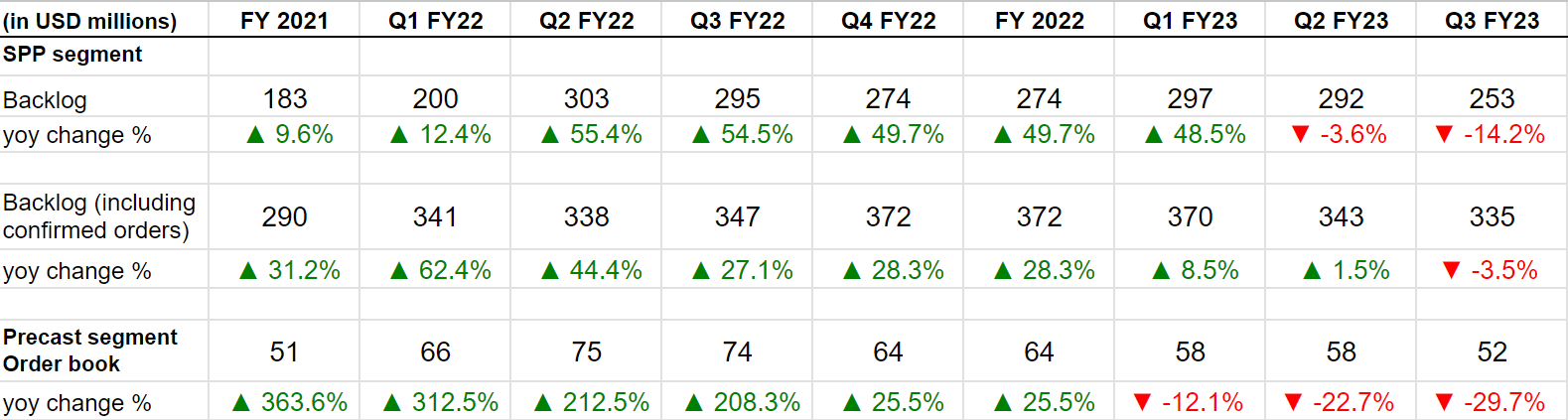

The backlog in both segments continued to decline due to tough market conditions.

{kind=link}

NWPX’s Historical Backlog and Order Bookings (Company data, GS Analytics Research)

Looking forward, while 2023 turned out to be a slow bidding year for the SPP segment and Q4 being a slow quarter is unlikely to change much, the non-recurrence of one-time customer-driven contract changes as well as customer delays which pushed some of the projects from Q3 to coming quarters should help offset the impact of slightly lower backlog (including confirmed orders) in the SPP segment.

I expect a meaningful improvement in the bidding environment in 2024. The Infrastructure Investment and Jobs Act ((IIJA)) has allocated $55 bn in federal funding for water infrastructure through FY26. Some of this funding has started getting deployed for projects and the deployment should accelerate meaningfully in 2024 which should increase the bid activity in the market and help the company’s backlog and revenues. The longer-term outlook for the segment also remains encouraging with secular drivers like aging water and wastewater infrastructure which is driving the need for upgrades, repair, and replacement.

On the Precast side, there are near-term headwinds from high interest rates which have resulted in a slowdown in residential and commercial construction markets resulting in a ~30% Y/Y decline in precast segment order book at the end of Q3 FY23. However, there is light at the end of the tunnel. With inflation going in the right direction , analysts have started making forecasts for the Federal Reserve rate cut in mid-2024. So, there is a likelihood of improvement in this market in the back half of the next year. The long-term fundamentals of the residential end-markets are also strong as over a decade of underbuilding in this market post the great housing recession of 2008 has made supply-demand dynamics attractive.

In addition to a potential recovery in the end market, the segment should also benefit from the “product spread strategy” under which it is adding the production of ParkUSA products (ParkUSA was acquired in 2021) to legacy Northwest Pipe Plants and vice versa to expand production and maximize overall efficiency. Under this strategy, the company is also increasing capacity utilization at Texas-based ParkUSA plants and bidding projects outside Texas, predominantly in Western and Southeastern regions of the U.S. to increase sales. The company has booked ~$7.1 mn worth of orders outside Texas in the first 9 months for these plants, indicating a good initial success of this strategy.

Further, the company is piloting the production of ParkUSA’s products at its Geneva precast operations facilities and plans to add additional NWPX legacy plants for ParkUSA product production in the coming years increasing the product reach and driving sales.

Overall, while the lower backlog does represent a near-term headwind, the company’s business should see an inflection in 2024 with improvements in the bidding market helping the SPP segment while a reversal in the interest rate cycle helping the precast business’ construction end markets. In addition, the company’s revenues should also benefit from initiatives under the “product spread strategy” which should help drive organic growth. So, I find the company’s medium to long-term prospects attractive.

Margin Analysis and Outlook

In Q3 2023, SPP's gross margin declined by 340 bps Y/Y largely due to customer-driven contract changes and project scope changes, which caused near-term production gaps at some plants, leading to higher levels of under-absorption. Rising interest rates in the residential housing and commercial construction markets caused a decline in the demand for precast products, which led to a reduction in overhead absorption and a shift in the product mix. As a result, the precast segment's gross margin contracted by 590 bps Y/Y. The Y/Y margin contraction in both the SPP and precast segments led to a decline of 410 bps Y/Y in gross margin to 16.3% and 420 bps Y/Y in operating margin to 7.6%.

NWPX’s Segment-Wise gross margin (Company data, GS Analytics Research)

NWPX’s Gross margin and Operating margin (Company data, GS Analytics Research)

Looking forward, the company’s near-term margin outlook is challenging as the weak bidding market has resulted in some pressure on SPP project margins while sales deleverage is expected to result in under-absorption in Precast operations in the near term.

However, the medium to long-term prospects are good, and as the bidding market improves, the pressure on project margins should reverse. Further, as the sales start to recover, especially in the second half of the next year, the company’s margins should benefit from operating leverage. The company’s margins should also benefit from synergies resulting from the integration of ParkUSA, especially the product spread strategy focused on improving efficiency. Management is also focusing on margin over volume, and continued cost reduction and productivity initiatives, which should help the margins in the long run.

Valuation and Conclusion

NWPX is currently trading at 11.90x FY24 consensus EPS estimates and 9.98x FY25 consensus EPS estimates, which is at a discount versus the company’s average forward P/E of 14.03x over the last 5 years.

While the company’s near-term outlook is challenging, I believe the company should be able to return to growth in FY24 with improvements in the bidding market and a potential reversal of the interest rate cycle. Further, product spread strategy, cost reduction, productivity initiatives, and operating leverage from sales recovery should help margins. Moreover, the company is well positioned to benefit from secular trends like aging water and wastewater infrastructure and a decade-plus of under-construction of new homes post the 2008 great housing recession which should support the company sales in the medium to long term. Given the good medium to long-term growth prospects and a lower-than-historical valuation, I am moving to a buy rating on NWPX stock.

For further details see:

Northwest Pipe: 2024 Can Be An Inflection Year (Rating Upgrade)