TPC - Northwest Pipe Company: An Interesting Business With Some Issues

Summary

- Northwest Pipe Company has a history of attractive sales growth, but bottom line results have been volatile from year to year.

- 2022 proved to be a solid year for the business, with sales, profits, and cash flows rising nicely.

- Shares look cheap, but the robust cash flows it's experiencing are likely to be temporary.

One of the most vital and, because of climate change, scarce, resources on the planet today is water. Although water scarcity can and does have significant negative consequences, it can also create opportunities for the companies that can work with it in ways that are valuable for society. One company that's dedicated to this space to a degree that few others are is Northwest Pipe Company ( NWPX ), an enterprise that produces water-related infrastructure products. Over the past several years, management has done a good job growing the company's top line. The bottom line, however, has not always been all that great. Most recently, the company has demonstrated strength in this area. And, as a result, shares of the business look cheap. Unfortunately, this does come with some strings attached. The most notable issue that investors should be aware of is that bottom line volatility does create some uncertainty moving forward. For those who can't handle extreme fluctuations in profits or cash flows, this is definitely not the kind of prospect to consider buying. But for value-oriented investors who don't mind yearly gyrations on this front, it could offer some nice upside in the long run.

A water-centric play

As I mentioned already, Northwest Pipe Company operates as a producer and seller of water-related infrastructure products. According to management, the company is actually the largest producer of engineered steel water pipeline systems in North America. But to truly understand the company, we should dig into each of the two segments that it runs. The first of these is the Engineered Steel Pressure Pipe segment. Through this, the business produces large-diameter, high-pressure steel pipeline systems that are used in water infrastructure applications. These specific applications are largely centered around drinking water systems. However, they can also be used in hydroelectric power systems, wastewater systems, and more. Other products produced under this segment include industrial plant piping systems and other related offerings. Using data from the company's 2021 fiscal year, this particular segment accounted for 78% of the firm's revenue and for 70.7% of its gross profits.

The other segment that the company has is called Precast Infrastructure and Engineered Systems. This unit is responsible for the production of precast concrete products that are manufactured using either a dry-cast or wet-cast concrete mix. Specific products here include manholes, box culverts, vaults, catch basins, oil water separators, pump lift stations, biofiltration of products, and more. This is the smaller of the two segments, accounting for 22% of revenue and for 29.3% of gross profits.

{kind=link}

Author - SEC EDGAR Data

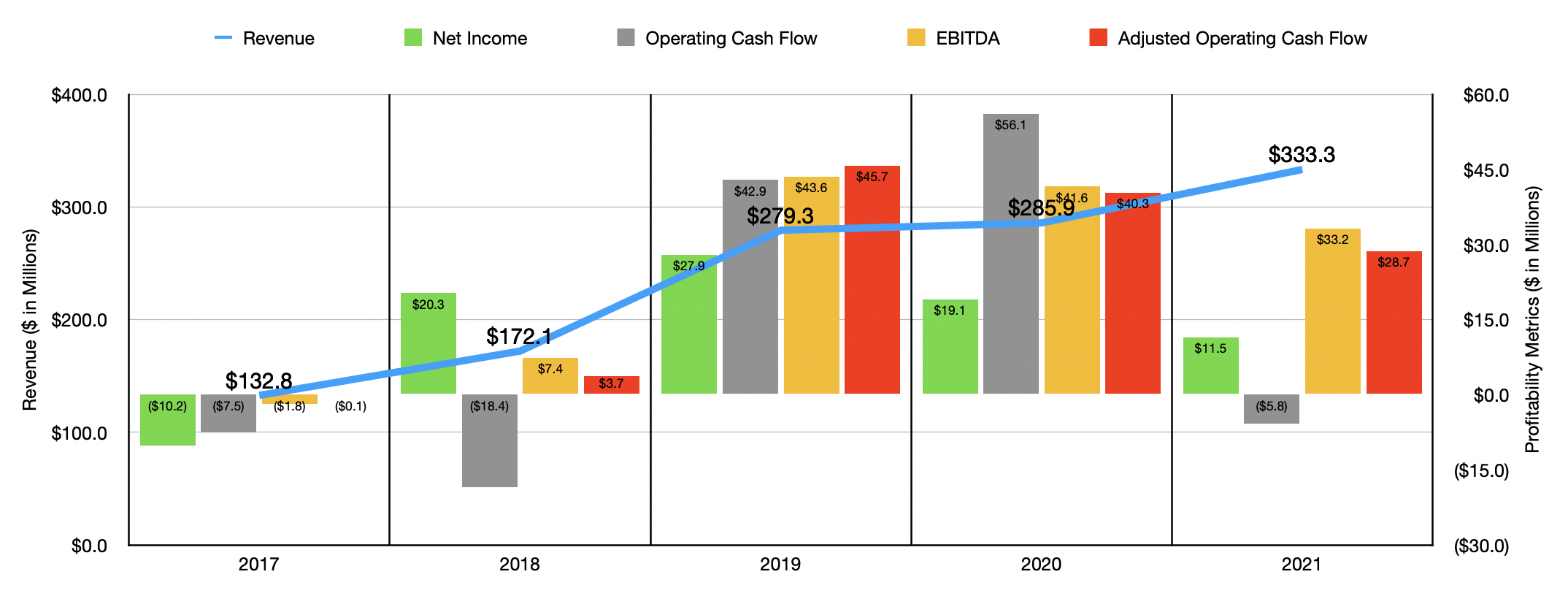

Over the past five years, management has done a solid job growing the company's top line. Revenue went from $132.8 million in 2017 to $285.9 million in 2020. Then, in 2021, revenue popped up 16.6% to $333.3 million. It's worth noting that the greatest increase the company experienced during this time was in its Precast Infrastructure and Engineered Systems segment. Revenue here spiked from $44.2 million in 2020 to $73.5 million in 2021. This 66.2% rise was driven mostly by its acquisition of ParkUSA in October of 2021, as well as 26% increase in sales from its Geneva operations that were acquired in early 2020.

If only the bottom line of the company had been as impressive as its top line, I would be very enthusiastic. But, unfortunately, that is not the case. Over the five-year window covered, the firm experienced a great deal of volatility on this front. It did see an improvement from a net loss of $10.2 million in 2017 to a net profit of $27.9 million in 2019. In 2020, profits then shrank to $19.1 million before dropping to $11.5 million in 2021. Other profitability metrics have followed a similar path. Operating cash flow over the past five years has ranged from a negative $18.4 million to a positive $56.1 million. In 2021, it came in negative to the tune of $5.8 million. If we adjust for changes in working capital, the picture looks a bit better, with the metric climbing from negative $0.1 million in 2017 to $45.7 million in 2019. But over the following two years, the metric fell, dropping to $28.7 million in 2021. That same kind of trend can be seen when looking at EBITDA as well, with the metric peaking at $43.6 million in 2019, only to fall to $33.2 million in 2021.

{kind=link}

Author - SEC EDGAR Data

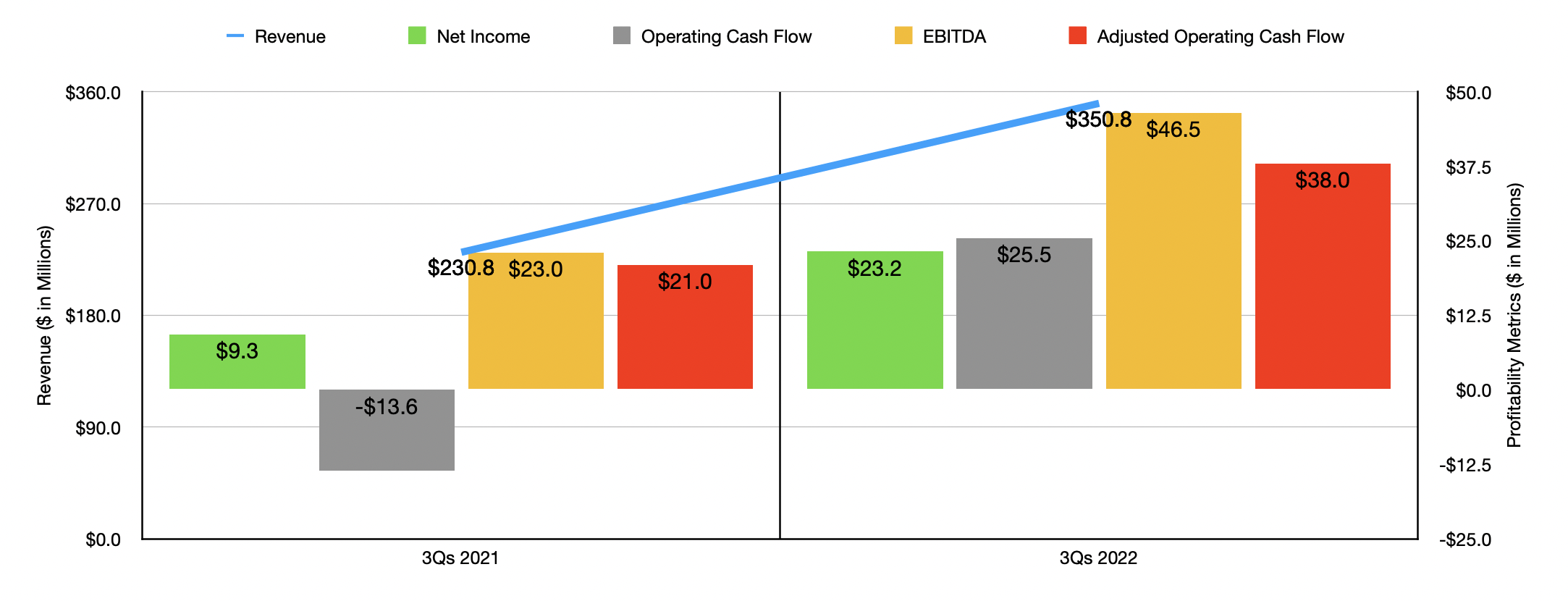

The good news for investors is that the 2022 fiscal year has so far come in strong. Sales spiked in the first nine months of the year to $350.8 million compared to the $230.8 million reported one year earlier. Just as was the case with its 2021 fiscal year, Northwest Pipe Company saw tremendous growth at its Precast Infrastructure and Engineered Systems segment. Revenue here spiked from $42.5 million in the first nine months of 2021 to $115.4 million at the same time of the 2022 fiscal year. This increase, according to management, was largely attributable to the aforementioned ParkUSA operations. However, it also benefited significantly from a 23.9% rise in sales at pre-existing precast operations due to a 49% rise in selling prices. This, management said, was possible only because of high demand for its concrete products and its ability to pass through inflationary pressures to its customers. Unfortunately, this did come at something of a cost. Even though overall revenue rose year over year, total volume shipped during this time dropped by 17%. That suggests that further price increases may not be possible. Meanwhile, the Engineered Steel Pressure Pipe segment reported a 25.1% increase in revenue year over year, with a 37% increase in selling price per ton offset some by a 9% decrease in tons produced. That decrease, management said, was mostly due to changes in project timing.

The rise in revenue during this time brought with it a surge in profits. Net income in the first nine months of 2021 came in at $9.3 million. This shot up to $23.2 million in the first nine months of 2022. Operating cash flow went from negative $13.6 million to $25.5 million. On an adjusted basis, it nearly doubled from $21 million to $38 million. Meanwhile, EBITDA for the company more than doubled, rising from $23 million to $46.5 million.

{kind=link}

Author - SEC EDGAR Data

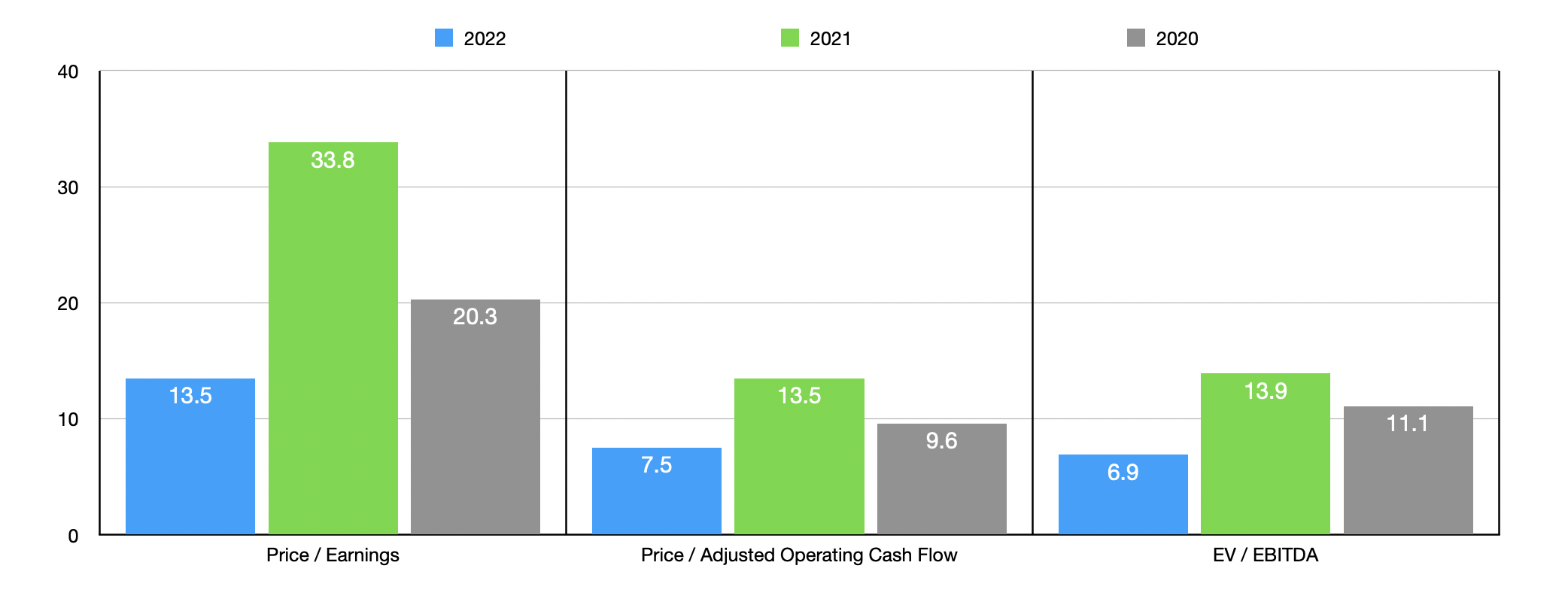

Management has not provided any guidance when it comes to the 2022 fiscal year in its entirety. But if we annualize results seen so far, we would get net income of $28.7 million, adjusted operating cash flow of $51.9 million, and EBITDA of $67.1 million. Based on these figures, the firm is trading at a price-to-earnings multiple of 13.5. The price to adjusted operating cash flow multiple is 7.5, while the EV to EBITDA multiple should be 6.9. On an absolute basis, shares look quite cheap in this case. But we need to keep in mind that such a bullish environment for the company may not stick around forever. In the chart above, you can also see pricing using data from 2020 and 2021. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 8.3 to a high of 97.3. In this case, only one of the five firms was cheaper than Northwest Pipe Company. Using the price to operating cash flow approach, the range was from 1.8 to 36.8. Two of the five firms were cheaper than our target in this case. And finally, using the EV to EBITDA approach, the range would be from 6.9 to 88.3. In this case, our target is the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Northwest Pipe Company |

| 13.5 |

| 7.5 |

| 6.9 |

| Great Lakes Dredge & Dock ( GLDD ) |

| 18.0 |

| 36.8 |

| 88.3 |

| Bowman Consulting Group ( BWMN ) |

| 97.3 |

| 20.2 |

| 26.7 |

| Concrete Pumping Holdings ( BBCP ) |

| 16.2 |

| 4.9 |

| 7.7 |

| Tutor Perini ( TPC ) |

| 8.3 |

| 1.8 |

| 32.4 |

| Emeren Group ( SOL ) |

| 74.7 |

| N/A |

| 66.8 |

Takeaway

It's rare that I come across an investment opportunity that I am on the fence about. In terms of its overall revenue trajectory, its recent fundamental strength on both its top and bottom lines, and the industry in which it operates, I am very much a fan of this business. Shares look cheap on an absolute basis and are tilting toward the cheap end compared to similar firms. On the other hand, I know that current market conditions are not likely to last forever. As a result, shares will get a bit pricier. On top of this, I don't care much for companies that have inconsistent financial metrics. And these are about as volatile on the bottom line as you get. To me, all of these issues, both good and bad, more or less balance out. In the long run, I suspect that Northwest Pipe Company will do just fine given the industry it's in. But for a value investor like me, I think that there are better prospects for investors to consider.

For further details see:

Northwest Pipe Company: An Interesting Business With Some Issues