NWPX - Northwest Pipe: Robust Project Demand And Backlog Growth

2023-09-27 14:29:20 ET

Summary

- Northwest Pipe Company reports strong long-term demand for water infrastructure projects and short-term demand for engineered steel pressure pipe projects.

- Internationalization efforts in Canada, Latin America, or Asia could bring substantial net sales growth.

- Management reported a significant amount of backlog for SPP water infrastructure steel pipe products. The company usually receives payments within 30 days of invoicing.

Northwest Pipe Company ( NWPX ) recently reported strong long-term demand for water infrastructure projects, and short-term demand for engineered steel pressure pipe projects. Given the balance sheet and previous experience in the M&A markets, I think that inorganic growth could enhance future FCF growth. There are obvious risks from delays in public projects and environmental regulations, however I think that future FCFs would justify richer stock price valuations.

Business Model

Northwest Pipe Company is a manufacturer of water-related infrastructure products in North America. Its wide range of products includes engineered steel pipe systems, stormwater and wastewater technology, high-quality precast products, pump lift stations, steel casing pipe, and bar-wrapped concrete cylindrical pipe.

Source: Presentation To Investors

Additionally, the company offers an extensive variety of gaskets, accessories, and specialized components for piping systems. Strategically located to serve growing water infrastructure needs, Northwest Pipe Company is distinguished by its commitment to quality, innovation, and strong values ??of responsibility, commitment, and teamwork.

First FCF Catalyst: Internationalization Could Bring Significant Net Sales Growth

Northwest Pipe’s primary customers are installation contractors who incorporate its products into bids for government agencies, private water companies, and specific project developers. Its commercial success is linked to spending on urban growth and new water infrastructure, with a growing trend towards investment in replacement, repair, and improvement of existing infrastructure. It offers a wide range of products, from steel pipe for larger diameter and pressure applications to precast concrete products for sanitary sewer and stormwater systems. Considering the type of clients that demand the products offered by Northwest Pipe, I think that further internationalization efforts in Canada, Latin America, or Asia could bring substantial net sales growth. With know-how developed in North America, I do not see why the products would not be successful overseas.

Source: 10-k

Backlog Of Close To $292 Million

In the last quarterly report, management reported a significant amount of backlog for SPP water infrastructure steel pipe products. The company usually receives payments within 30 days of invoicing. With this in mind, even if the backlog does not increase in the coming years, I believe that Northwest Pipe Company will most likely receive payments. In terms of visibility of future FCFs, Northwest Pipe will most likely be appreciated by investors out there.

"Payment terms of amounts billed vary based on the customer, but are typically due within 30 days of invoicing." Source: 10-Q

"Backlog represents the balance of remaining performance obligations under signed contracts for SPP water infrastructure steel pipe products for which revenue is recognized over time. As of June 30, 2023, backlog was $292 million. The Company expects to recognize approximately 46% of the remaining performance obligations in 2023, 46% in 2024, and the balance thereafter. " Source: 10-Q

There Is Strong Demand For Water Infrastructure Projects In The United States

Northwest Pipe Company will most likely benefit from expected demand for water infrastructure projects as well as recent short-term demand for engineered steel pressure pipe. Management discussed some of these recent trends in the last quarterly report.

"Long-term demand for water infrastructure projects in the United States appears strong and we have experienced an improvement in recent short-term demand for our engineered steel pressure pipe ." Source: 10-Q

Besides, I believe that the Bipartisan Infrastructure Deal and Inflation Reduction Act would most likely continue to accelerate the increase in backlog growth. Management also mentioned some of these revenue drivers in previous communications .

The Company Targets A Large Market Opportunity

With net sales of less than $0.7 billion, Northwest Pipe Company is targeting two markets that could sum up to $5.6 billion. The Steel Pressure Pipe market is valued at $450-$600 million, and the Concrete Pipe and Precast stand market is valued at $2-$5 billion. In my view, if the company continues to offer innovative products, and the capex continues, there will most likely exist demand for the products. As a result, we may see net sales growth and FCF growth.

Source: Presentation To Investors

Strategic Acquisitions Could Also Bring FCF Growth

Northwest Pipe Company's business strategy has focused on growth and expansion through strategic acquisitions. The company acquired ParkUSA, a steel and precast concrete company specializing in water and environmental solutions, strengthening its presence in the water infrastructure technology market. Additionally, there is the acquisition of Geneva Pipe and Precast Company, which expanded the company's capabilities in water infrastructure products, including reinforced concrete pipe and a variety of precast concrete products. These acquisitions have strengthened the company’s market position, and allow it to offer a broader range of water infrastructure solutions to its customers. Considering the current state of the balance sheet, I think that we could expect further inorganic growth to enhance FCF generation.

Source: Presentation To Investors

Balance Sheet, And Analysis Of The Debt

As of June 30, 2023, Northwest Pipe Company reported cash of about $4 million, with trade and other receivables worth $63 million, inventories close to $84 million, and total current assets of about $279 million. The ratio of current assets/current liabilities stands at more than 1x, so I do not see liquidity issues here.

Property and equipment is equal to $137 million, with goodwill of $55 million and total assets of $602 million. The ratio of assets/liabilities is larger than 2x, so solvency does not seem an issue either.

Source: 10-Q

With regards to the list of liabilities, Northwest Pipe reported current debt of about $10 million, with accounts payable of about $26 million, accrued liabilities close to $25 million, and total current liabilities of $95 million. I really do not see that investors would be afraid of the total amount of debt or borrowings. In my view, if Northwest Pipe decides to acquire new companies using new debt, bankers would most likely offer financing. With borrowings of $70 million and operating lease liabilities of $87 million, total liabilities were $274 million, which do not seem significant.

Source: 10-Q

I studied the contractual obligations to see whether we should be worried about any of the obligations. Through August 2022, the company established an Interim Financing Agreement for a total amount of up to $13.5 million for the acquisition of equipment for a new reinforced concrete pipe factory. The IFA accumulates interest at the Guaranteed Overnight Finance Rate plus 1.75%.

I also studied a bit of the credit agreements signed by Northwest Pipe. I really do not think that the interest rate being paid by the company is substantial. In this regard, I believe that investors may do good by looking at the following lines.

"Swingline loans under the Amended Credit Agreement bear interest at the Base Rate plus the Applicable Margin. As of December 31, 2022 and 2021, the weighted-average interest rate for outstanding borrowings was 6.07% and 1.85%, respectively. The Amended Credit Agreement requires the payment of a commitment fee of between 0.30% and 0.40%, based on the amount by which the Revolver Commitment exceeds the average daily balance of outstanding borrowings. Such fee is payable monthly in arrears." Source: 10-k

Valuation

Under my assumptions, I included net sales growth in both business segments. In total, I assumed that we may see double digit sales growth from 2023 to 2028 with net income/sales of approximately 6%-9%. I believe that my assumptions are in line with previous results reported from 2017 to 2022.

I also believe that we may see an increase in the profit margin coming from the recent growth of the Precast Infrastructure business segment. Note that the company reported record backlog in 2022. I do not see why the backlog would not continue to grow north.

Source: My Expectations Source: Presentation To Investors

{kind=link}

Note that I assumed significant net sales growth in the Precast Infrastructure business segment. However, from 2027, net sales growth of both business segments will most likely be similar.

Source: Presentation To Investors Source: My Expectations

{kind=link}

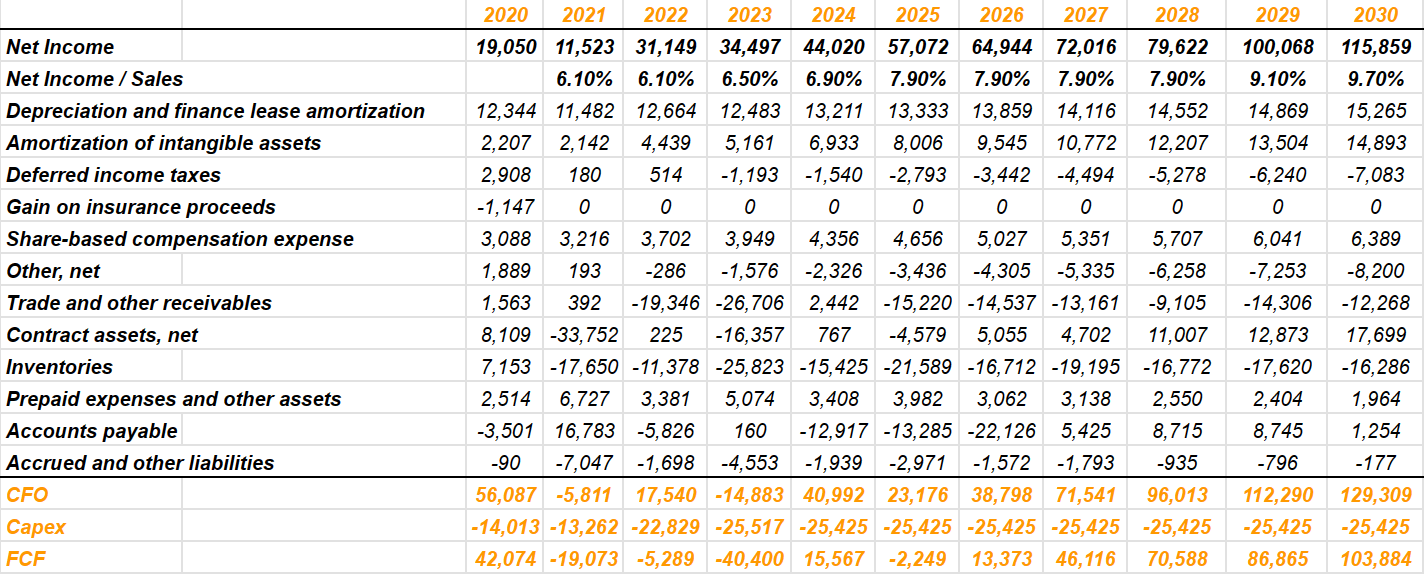

With the net income obtained from both business segments, I believe that we could see 2030 net income close to $115 million, with net income / sales close to 9.7%. I also added depreciation and finance lease amortization of close to $15 million, amortization of intangible assets worth $14 million, and share-based compensation expense of about $6 million. I also assumed changes in accounts payable of about $1 million, and 2030 CFO of about $129 million. Finally, with capital expenditures of -$26 million, 2030 FCF would be about $103 million.

{kind=link}

Readers may want to have a look at previous FCF figures reported since 2014 and the net income/sales ratio. These figures are close to the assumptions I made in my financial model.

Source: YCharts Source: YCharts

With regards to the terminal EV/FCF, I studied previous EV/FCF multiples, which ranged from more than 16x to about 4x. Considering these figures, I think that assuming an exit of 6x FCF appears very conservative.

Source: YCharts

For the calculation of the cost of capital, I took a look at the list of peers used by other investment analysts. Competitors report a median WACC of 6.7%, so I believe that the cost of capital of Northwest Pipe Company may not be far from this figure.

Source: Market Screener

With the previous assumptions, the net present value of the FCFs from 2023 to 2030 stood at close to $182 million. The NPV of the terminal value was close to $371 million, which makes a total enterprise value of $553 million. Adding current debt, borrowings, and equity, the implied price becomes $48 per share. The internal rate of return was somewhere between 8% and 9%.

Source: My DCF Model

The results of my model implied that Northwest Pipe Company is currently undervalued. A close review of the figures reported by SA shows a difference of about -23% and 35% in the EV/Sales, EV/EBIT, and EV/EBITDA ratio.

Source: SA

Risk

Northwest Pipe Company faces several risks in its operation. Unforeseen delays in public water transmission projects can negatively impact the planning and utilization of its facilities, thus affecting the profitability. Additionally, compliance with strict environmental laws and regulations can incur significant costs and penalties for non-compliance. Environmental risks also include potential expenses associated with environmental assessments and remediations. Successful integration of future acquisitions is crucial, as challenges in unifying cultures and systems can impact relationships with customers and suppliers. Strategic alternatives, such as joint ventures or divestitures, should also be carefully evaluated. These factors may have an adverse impact on the company's financial condition and results of operations.

Competitors

In my opinion, Northwest Pipe Company faces intense competition in the market, characterized by competitive bidding and strong price pressure. In addition to price, on-time delivery, custom specifications, and freight costs are critical factors.

The company operates facilities at multiple strategic locations across North America, allowing it to compete effectively throughout the region. Its main competitors in the western US and southwestern Canada are Imperial Pipe and West Coast Pipe, while east of the Rocky Mountains, Thompson Pipe Group, and American SpiralWeld Pipe are its main rivals. The entry of new competitors or expansion of existing facilities represents a potential threat.

My Takeaway

Northwest Pipe Company has a strong position as a water infrastructure manufacturer in North America, supported by a broad range of products. I think that the current backlog, expertise in the M&A markets, potential internationalization in Canada, and current demand could bring future FCF growth. Yes, the company faces competitive challenges and risks, such as delays in public projects and compliance with environmental regulations. With that, I believe that the company remains undervalued at the current stock price.

For further details see:

Northwest Pipe: Robust Project Demand And Backlog Growth