NWE - NorthWestern: A Little Too Much Premium Too Little Growth

Summary

- I love investing in quality utilities. They bring about great yields, very good returns if there's an undervaluation to be had as well, and their cash flows are conservatively backed.

- NorthWestern Corporation is a multi-utility with a market cap of around $3.5B. That makes the company relatively small, but not uninteresting.

- A quick review shows you an appealing potential investment - a deeper view shows you the valuation for where a good upside could be had if you invest.

- Here I will share with you my initial thesis on NorthWestern Corporation - and why I consider it a "HOLD" here.

Dear readers/followers,

In this article, I'm going to present you with NorthWestern Corporation ( NWE ), and why this multi-utility investment could be interesting to you. The company is a utility servicing state I usually don't cover that often with utilities - specifically South Dakota, Nebraska, and Montana, with headquarters in Sioux Falls, South Dakota.

The company offers employment to over 1,500 people, and focuses on conventional electricity as well as natgas operations, through a revenue mix of regulated distribution of power and natgas, transmission, and energy supplies. The company is also starting to focus on things like generation opportunities and expanding its transmission base.

Let's look at the company and see what it does and what makes this portfolio potentially interesting.

NorthWestern Corporation - The company from A to Z

NWE is a 100% pure electric and natgas utility business that has a 100+ year operating history behind it. The company's rates for Natgas and resi power are below the national average, it has a solid system with good reliability among class-leading stability and resilience indicators, such as lack of leaks and so forth. It also has a leading customer satisfaction score.

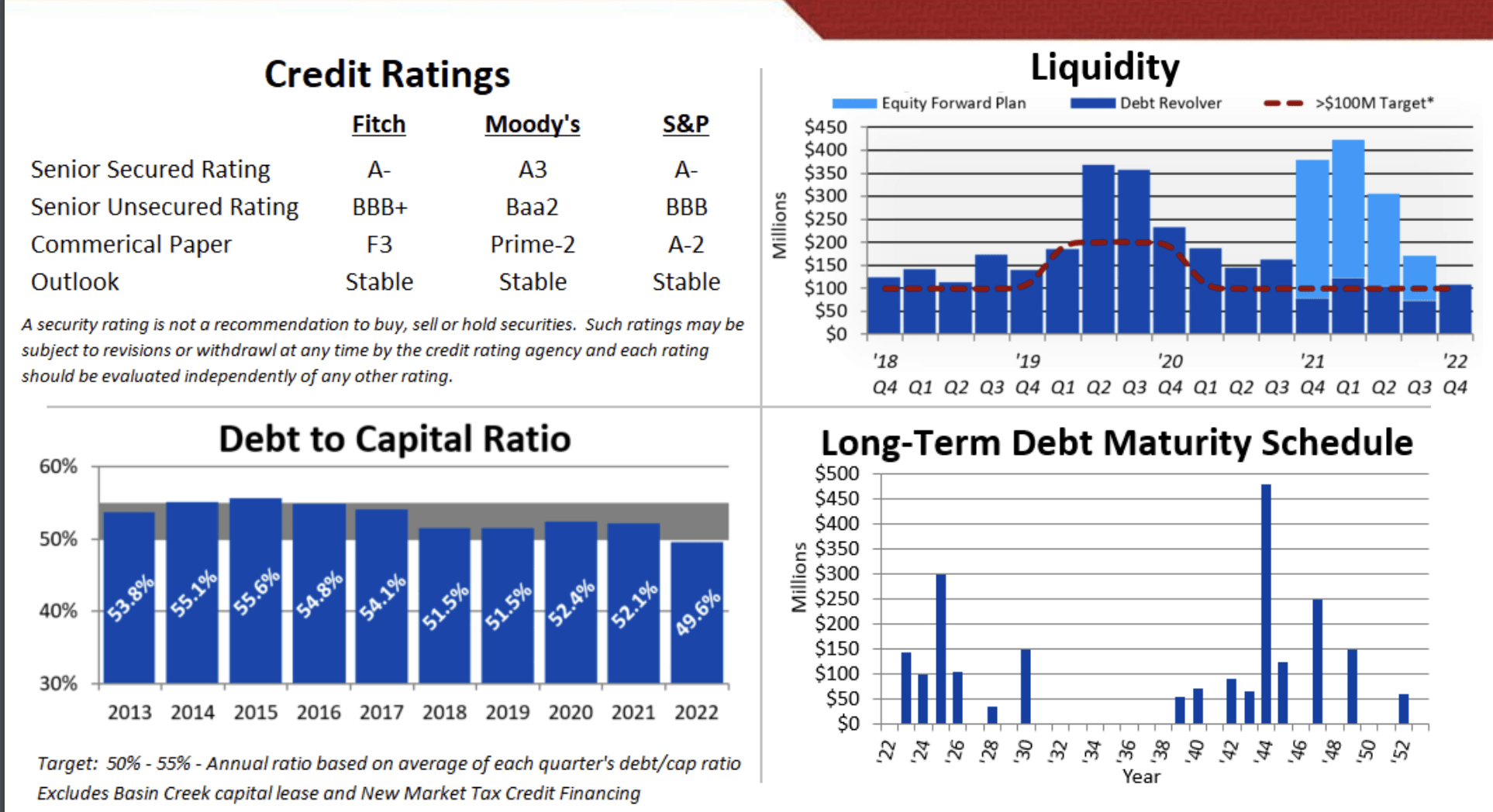

This low pricing/rates indicates a certain regulatory lag in terms of bumping rates, and there is a pending review to address these concerns, but the company nonetheless has solid cash flows and a good balance sheet. It's investment-grade rated at BBB and has a history of providing consistent and annual, increasing dividend growth.

The company targets a debt/cap of around 50%, with liquidity of no lower than $100M to provide cushioning, while also working for a 3-6% EPS growth, coupled with a competitive yield to provide market-outperforming and competitive returns over the long term. The company's long-term dividend payout ratio is around 60-70%.

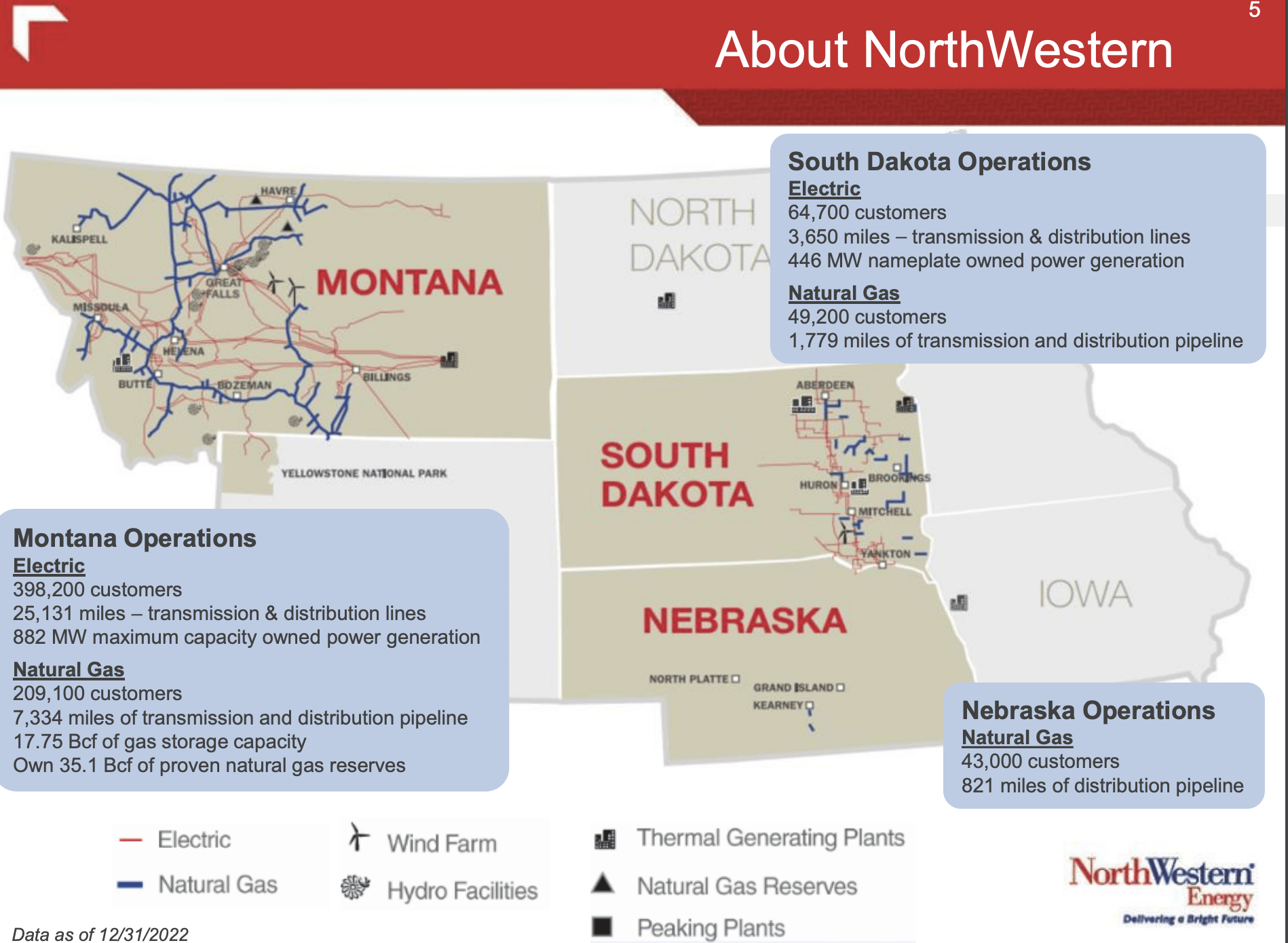

Here are the company's operations.

{kind=link}

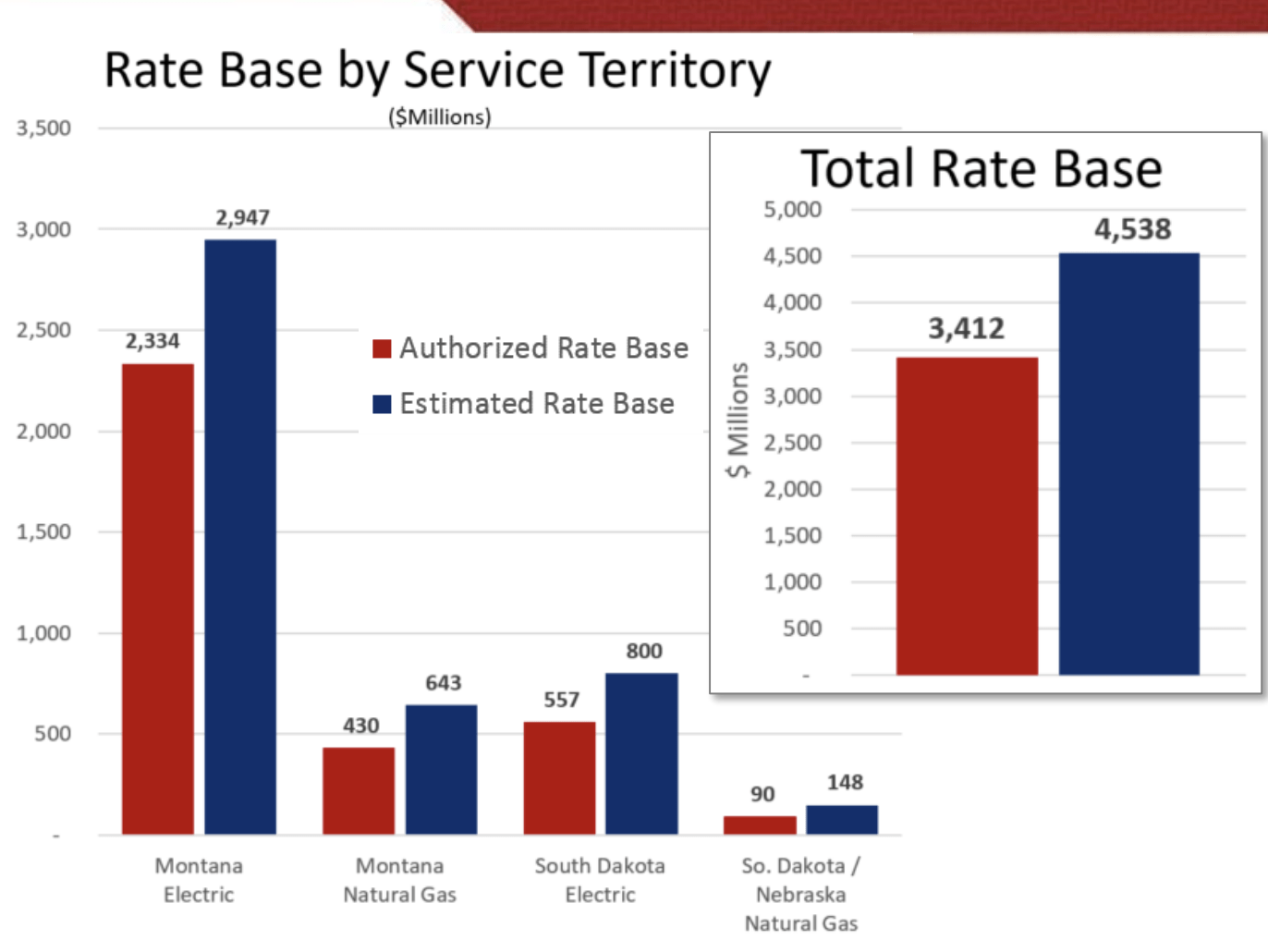

The company has a utility margin that's around 79% electric and 21% gas, and geographically is 85% Montana, 14% South Dakota and around 1% Nebraska. This gives you some idea of how the split goes in terms of income. Here is the company's current rate base.

{kind=link}

The company's mix is already fairly well-diversified in terms of ESG. The electricity generation is 55% Carbon-free and includes a fair bit of Hydro, some solar, and a good deal of wind - both contracted and owned generation, For the most part when it comes to renewables, the company's current capacity is owned.

However, the company also has a headwind in the form of its Coal production. 28% of production is coal, and the company owns that generation. The company is still better than the national average here in terms of its mix, but this is something that needs to be addressed going forward.

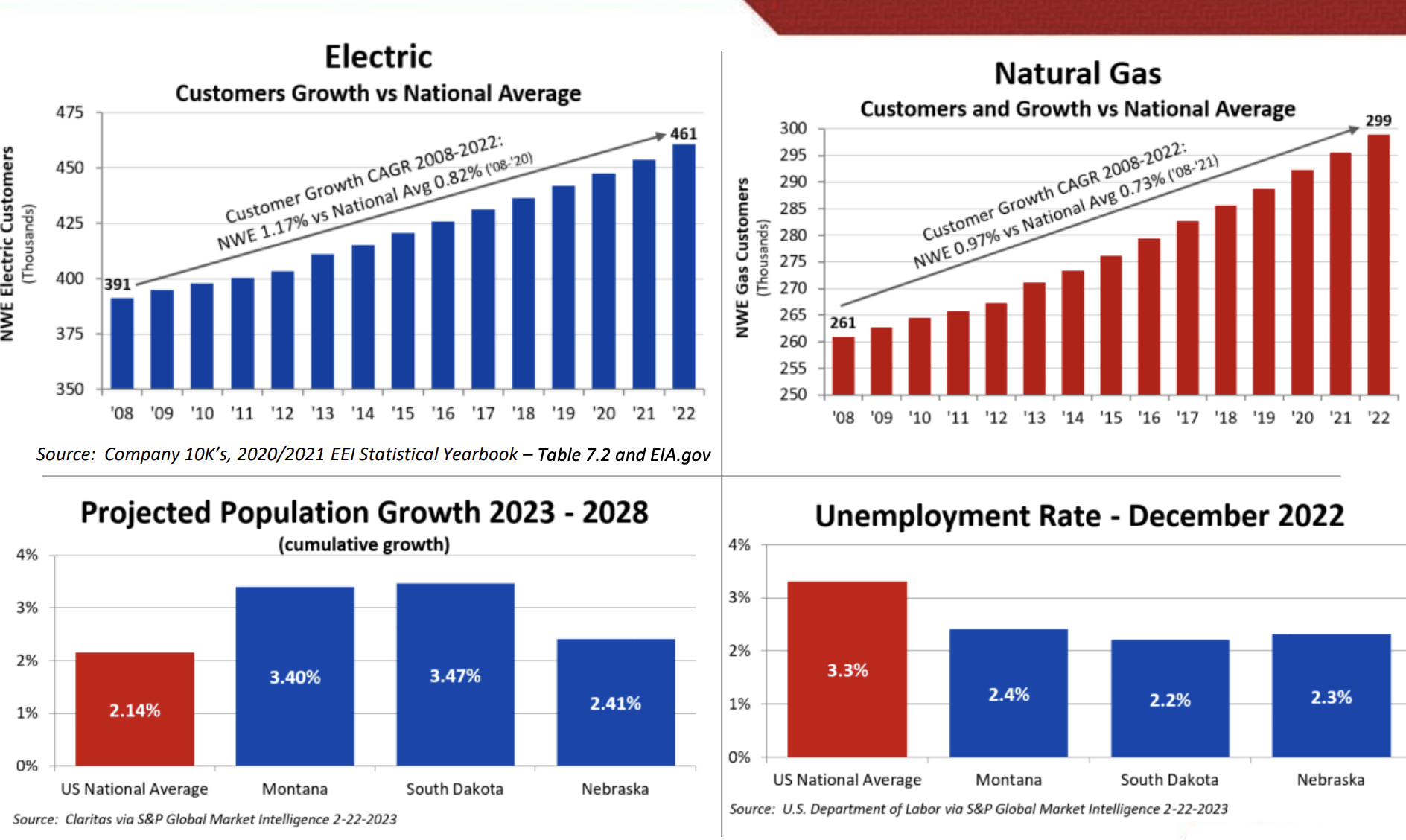

The foundational economic indicators for the company's operating geographies are extremely solid. This is what provides the implications for how the company's rate base, the company's EPS and the company's sales may be growing going forward.

And for these areas, things are looking good, because every single relevant economic indicator is excellent there.

{kind=link}

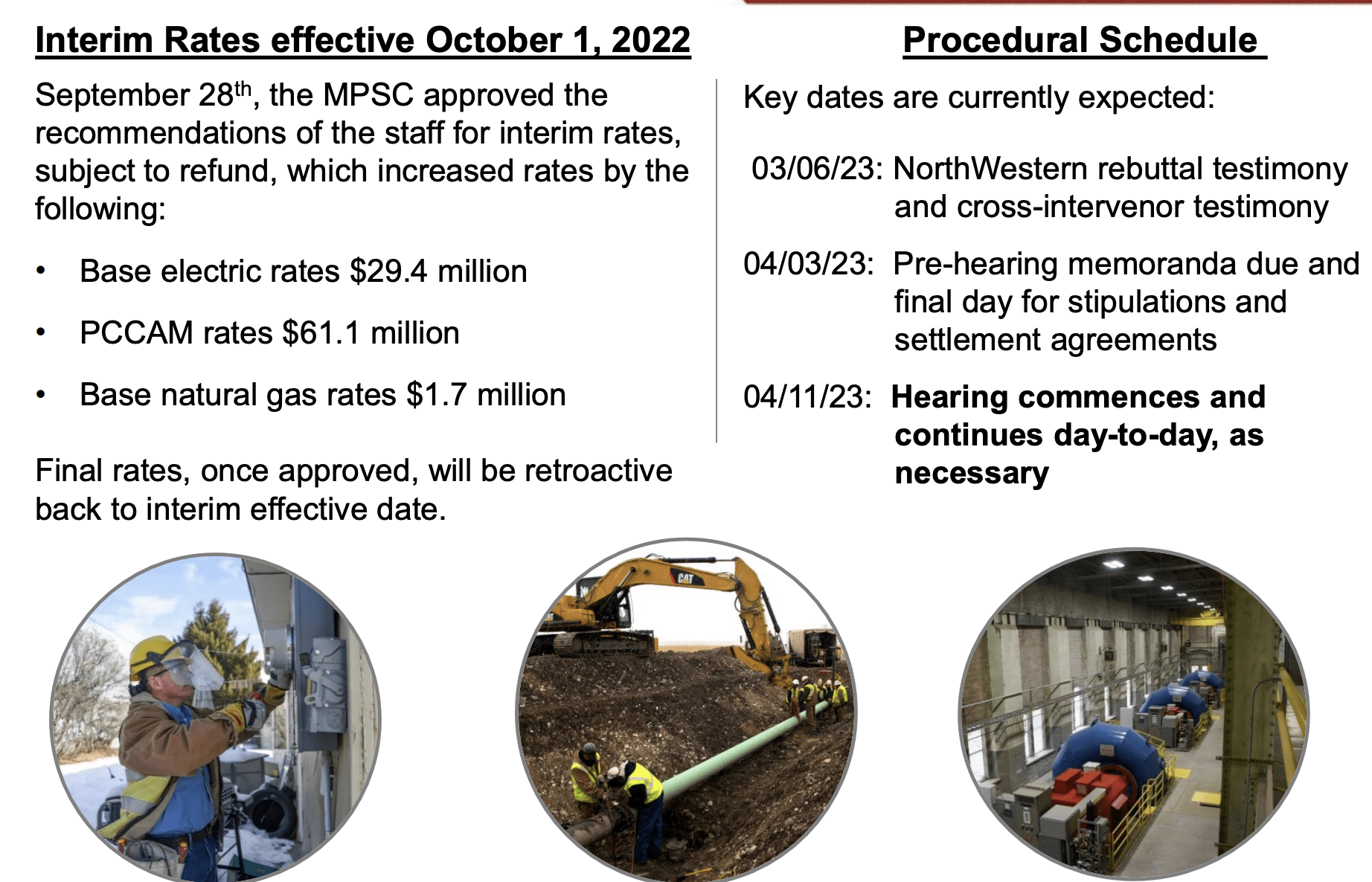

What about regulation and the rate base? The company has requested a base rate increase to support significant infrastructure investments in Montana, though the operating costs will remain below its peers. About 42% of the recently requested revenue increase is flow-through costs which the company has no control over. As of this request, the company customer bill level is in line with overall national inflation. NWE has proposed a 48.02% equity ratio, with an RoE of 10.6%. Forecasting how this rate case is going to go is still somewhat difficult, but the Montana one is the "big one" given that most of the company's revenue comes from this part of the business.

Here are some of the relevant dates.

{kind=link}

Some might say that power costs have gone up too much, but the fact is that the company's pricing and percentage increases over the past 10 years are significantly below every single household and consumer good you can compare it to. NWE is 5% below the national electricity average increase, and compare it to butter which is up 53.2% in 10 years, NWE electric and natgas bill are up significantly less.

The company has provided a financial outlook for the 2023 period - but I would be careful trying to forecast anything with the company at this time, due to the deciding nature of the rate case outcome in Montana, which is pending for this year. This includes over half a billion dollars in Investments in 2023 alone, with $80M in Yellowstone County. The company still targets its long-term expectations of 3-6% EPS and a 4-5% rate base. The annual dividend is expected to be somewhat above the higher range of its target for payout ratio, and the company has accepted this.

In terms of leverage, NWE intends to remain a conservative coverage with an FFO/debt of above 14% - and the company is currently forecasted to deliver this for the next fiscal. The company is very conservatively rated, with stable ratings across the board, and a lowering debt for the last 10 years. The company also has an extremely staggered maturity for its debts and no issues with liquidity.

{kind=link}

The company isn't scandal-free. There was an explosion in Bozeman back in -09 which destroyed several businesses and resulted in both casualties and lawsuits. The company has also been accused of inflating its stock price artificially and illegally, and this was settled with $41M, though this was over 20 years ago.

Today, the risks for NWE can be concluded as follows - valuation. We have analysts covering the company on SA, but the past two articles have resulted in growth, despite a negative outlook from the coverage, though these have mainly looked at technical indicators as opposed to fundamental ones. That's where I differ.

I fail to see any material long-term risks to the company's growth prospects. The company is a solid utility in an underappreciated part of the USA. I personally find that Montana has one of the most beautiful areas in all of the United States, while obviously not being the most densely populated, developed, or industrialized part of the nation. I believe we'll see a move to states like Montana, and the current demographic trends seem to agree with this.

Based on attractive fundamentals, the variable that remains for me, to look at, is the valuation of the company and where I would believe it to be a good "BUY" for you.

Because, let's be clear - I'm in agreement with previous analysts, that this one is a "HOLD".

But not for the same reasons.

NWE - It's a "HOLD", but for these reasons

NorthWestern had a fairly good run from mid-October or thereabouts, with NWE stock advancing almost 20% since that time. That also means that it significantly beat the market at the same time. The mistake some people make is being negative on a utility because it trades at a premium. For many utilities, I do allow a premium - and NWE is one of them.

Even now, the company trades at a yield of 4.5%, which means that it has the capacity of averaging a close to 5% yield at what I would consider undervaluation.

So what is undervaluation for this company?

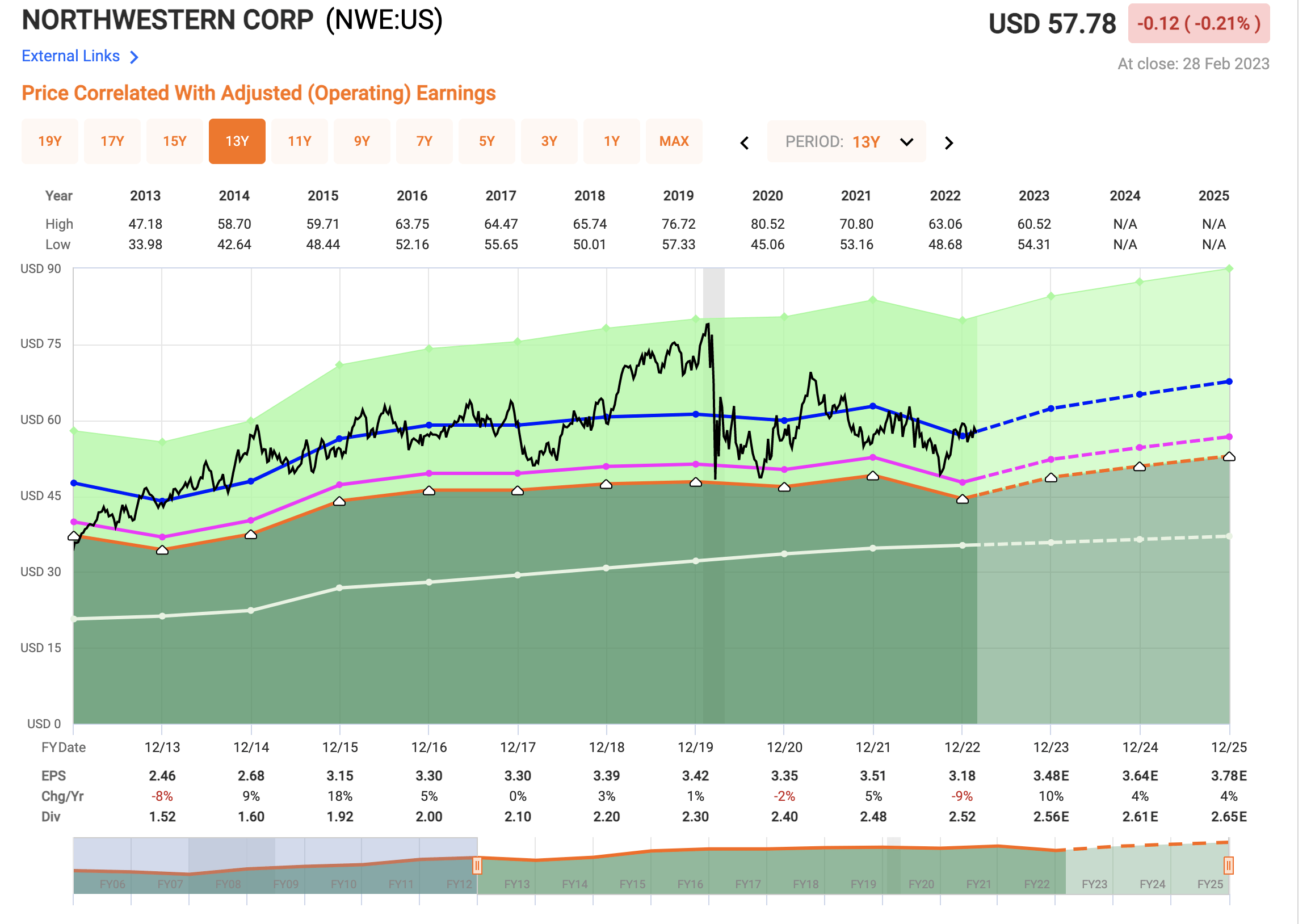

I would say that happens when NWE approaches a 15x P/E.

{kind=link}

As you can see from historical trends, this company goes up and down. The mistake is made when valuing it above 18-19x P/E. The company's limited growth rate, both historical and forward expected, does not justify this sort of premium. But 17.5x, that's something I can agree to for NWE.

Based on that visualization, you should be able to estimate fairly clearly where this 3-5% growing business should be bought. NWE isn't going to be growing fast. 5-6% is the most you can expect here, and that also averages the 2023E-2025E forecast - 5.98%. Even with that expectation, the dividend is only expected to grow a few cents until then.

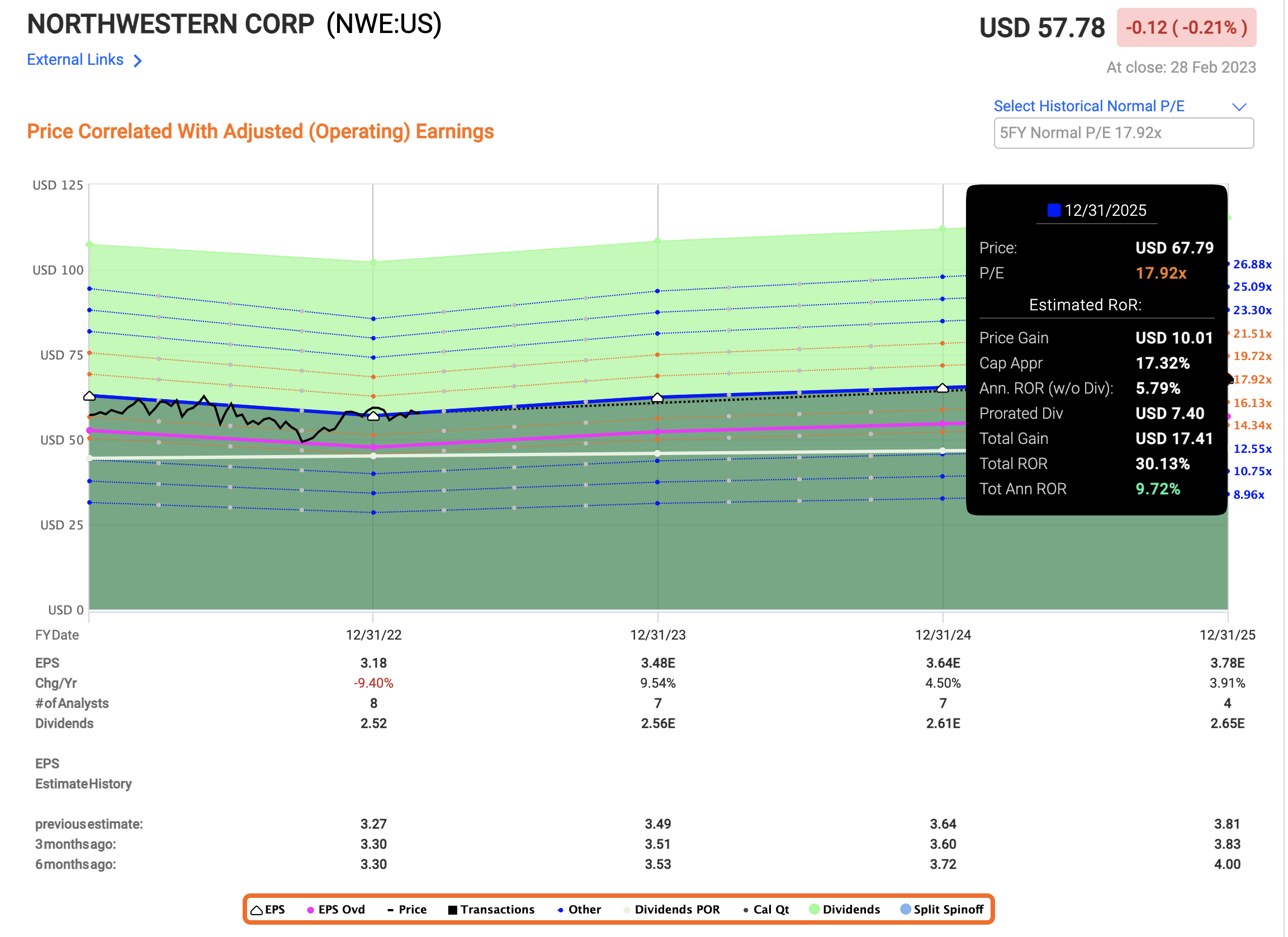

Because the company currently trades at almost 17.9x, you should be able to see what this means for the relative appeal of investment into NWE.

{kind=link}

That's slightly better than the market, but given the company's slight volatility, I believe there is a real potential for 15-16x P/E, which would dial that down below 8% annualized, and therefore below my lowest acceptable level of return on investment.

A reverse to 15x P/E, which is not unlikely based on inflation and the company's ongoing rate case, if it gets decided even slightly against the company, means a 3-4% RoR on an annualized basis, or almost less than double digits in 3 years.

That's the definition of "Not good enough", as I see it. And generally, analysts would agree with my assessment in this case. 8 analysts follow NWE, and out of those 8, only 3 are at a "BUY". This makes sense when we see that the price target range for the company begins at $46 and goes to $68, but the average lies about at $57.5, which is actually below the current price of $57.78, if only by a hair.

I would say the stated price target is the absolute highest we can accept for the company. Anything higher than that cannot, and should not be justified here, and for that reason, this company is a no-go in terms of forecasts and valuations, despite solid fundamentals. Plenty of peers out there to compare it to, and relevant peers are multi-utility companies like Dominion ( D ), CenterPoint ( CNP ), and others.

The company isn't undervalued compared to any one of these - rather, it's overvalued to everything except PEG, which is valued higher at this time.

Because NWE is essentially a play on the outcome of the near-term rate case, it pays in this case, I believe, to wait for the outcome of said rate case before making any final decision - because I believe the chance that the company declines is far higher than it advancing.

This brings me to my current thesis for the company.

Thesis

- NWE is a qualitative multi-utility based in South Dakota, with plenty of appeal in attractive and underappreciated US states. The company has good enough fundamentals where I would say that it can be a no-nonsense "BUY" anytime it goes below a 15x P/E, where the yield would be close to 5%.

- However, at current pricing, it's too close to an 18-19x P/E, which is a premium the growth rate and the risks in terms of rate case outcome, do not justify. Because of that, I would say this company is a most definite "HOLD" here, nothing else.

- I give the company a conservative PT of $51/share, to begin with.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Being neither cheap or having a conservative realistic upside, I say that NWE does not fulfill the demands I have of an investment - 3 out 5 isn't enough for me here, so it's a "HOLD".

For further details see:

NorthWestern: A Little Too Much Premium, Too Little Growth