NWE - NorthWestern Remains An Ideal Income Pick Is Fairly Valued

2023-08-11 14:59:26 ET

Summary

- NorthWestern Corporation is a utility company serving over 700,000 customers in South Dakota, Montana, and Nebraska.

- NWE has experienced a decline in revenues and net income in Q2, but increased free cash flow driven by operational cash flows.

- The company focuses on remaining a pure play utility, expanding into higher margin production methods, and improving earnings and free cash flow.

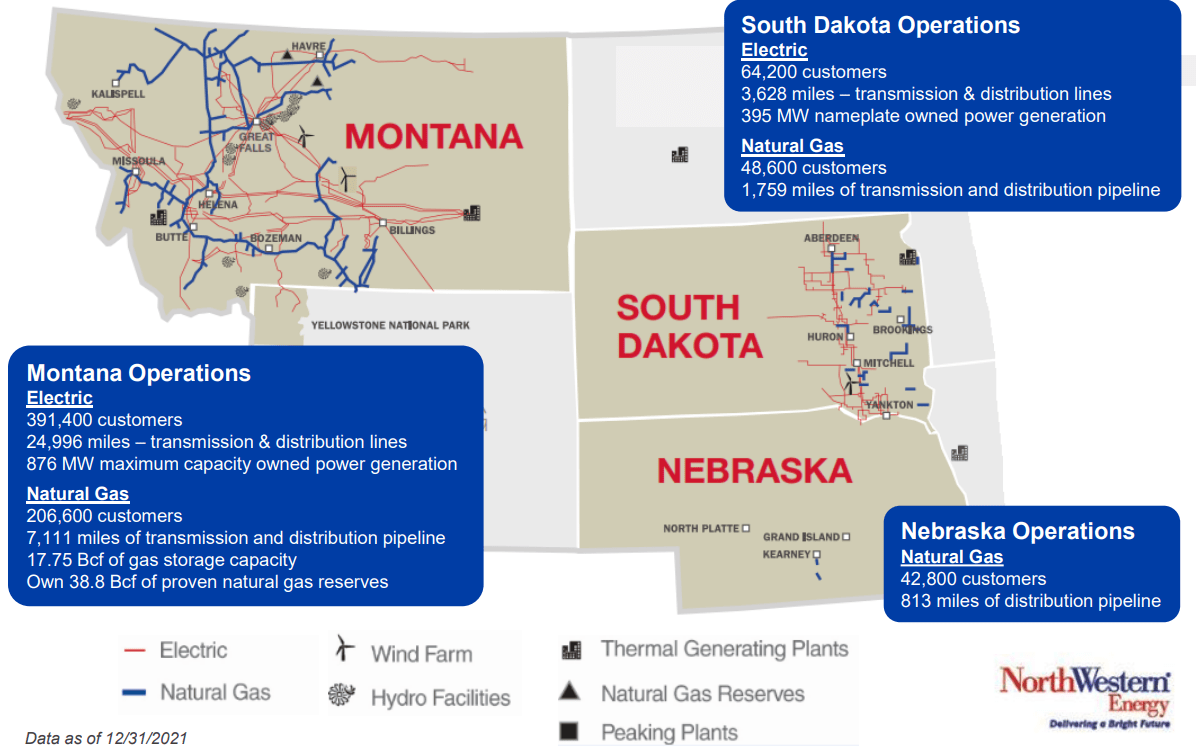

NorthWestern Corporation ( NWE ) is a Sioux Falls, South Dakota-based utility company providing electricity and natural gas services. The firm currently serves ~718,000 customers, with operations primarily across South Dakota, Montana, and Nebraska.

{kind=link}

Through these activities, NWE has achieved Q2 revenues of $290.50mn- a 10.06% YoY decline - alongside a net income of $19.12mn- a 35.80% decline- and a free cash flow of -46.39mn- a 43.22% increase driven by increased operational cash flows.

Introduction

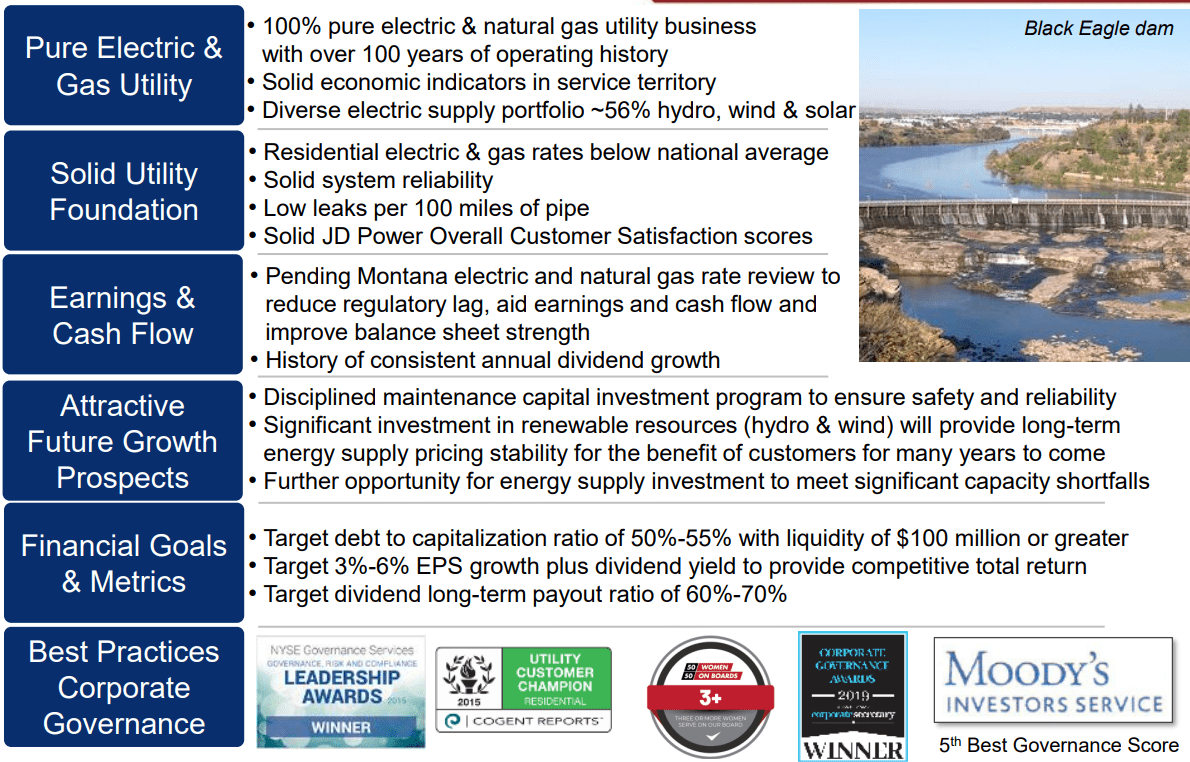

At the core of NWE's operational capabilities remains a fivefold focus on remaining an electric and gas utility pure play, retaining its customer base through reliability and affordability, ensuring that NWE persists as a leader in corporate governance - thereby supporting talent retention and remaining ESG inclusionary, expanding gradually into higher margin production methods and acquiring wallet share, all culminating in improved earnings and free cash flow through the said methods and rate increases.

{kind=link}

On a more granular level, NWE seeks to preserve its superior utility stability across the grid and on its pipelines, raise rates pending review, still at a rate priced for the benefit of consumers, ultimately supporting the firm's financial goals of a debt/equity of 50-55% alongside 3-6% EPS growth and a dividend payout ratio between 60-70%.

{kind=link}

The combined effects of NWE's diversified revenue base, prudent capital deployment strategy, and dividend support the firm's long-run stability and growth. However, the firm does trade at or slightly above fair value, leading me to rate the company a 'hold', largely driven by its high-income potential.

Valuation & Financials

General Overview

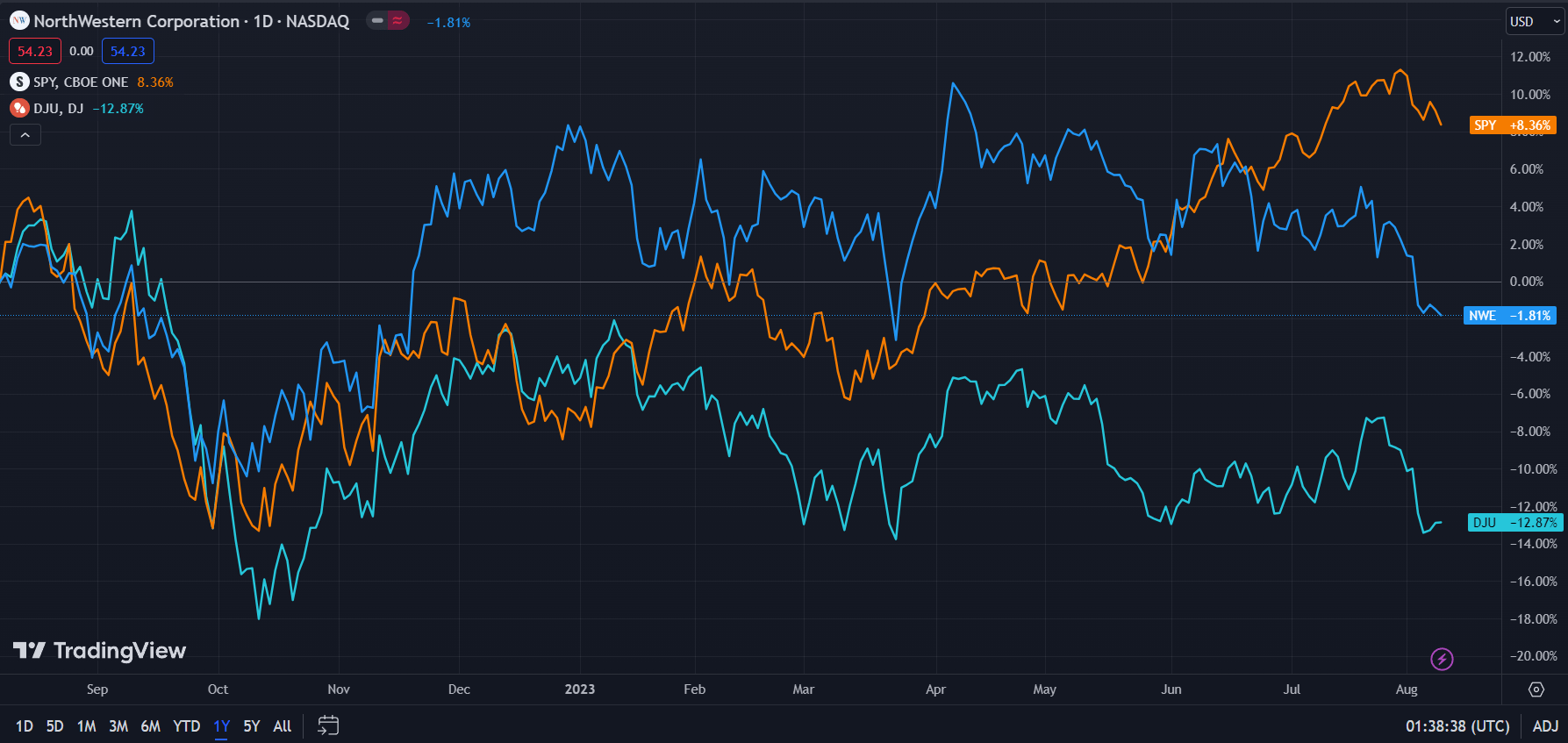

In the TTM period, NWE's stock - down 1.81% - has experienced middling price action, between both the Dow Jones Utilities Index ( DJU ) - down 12.87% - and the broader market, as represented by the S&P 500 ( SPY ) - up 8.36%.

{kind=link}

I believe the relative underperformance of the utility industry and NWE to the broader market is a result of the increased attractiveness of higher-interest bonds on a risk-adjusted basis.

However, NWE's superior price action to DJU is indicative of the company's operational strength and regional positioning, which sees lower risk exposure.

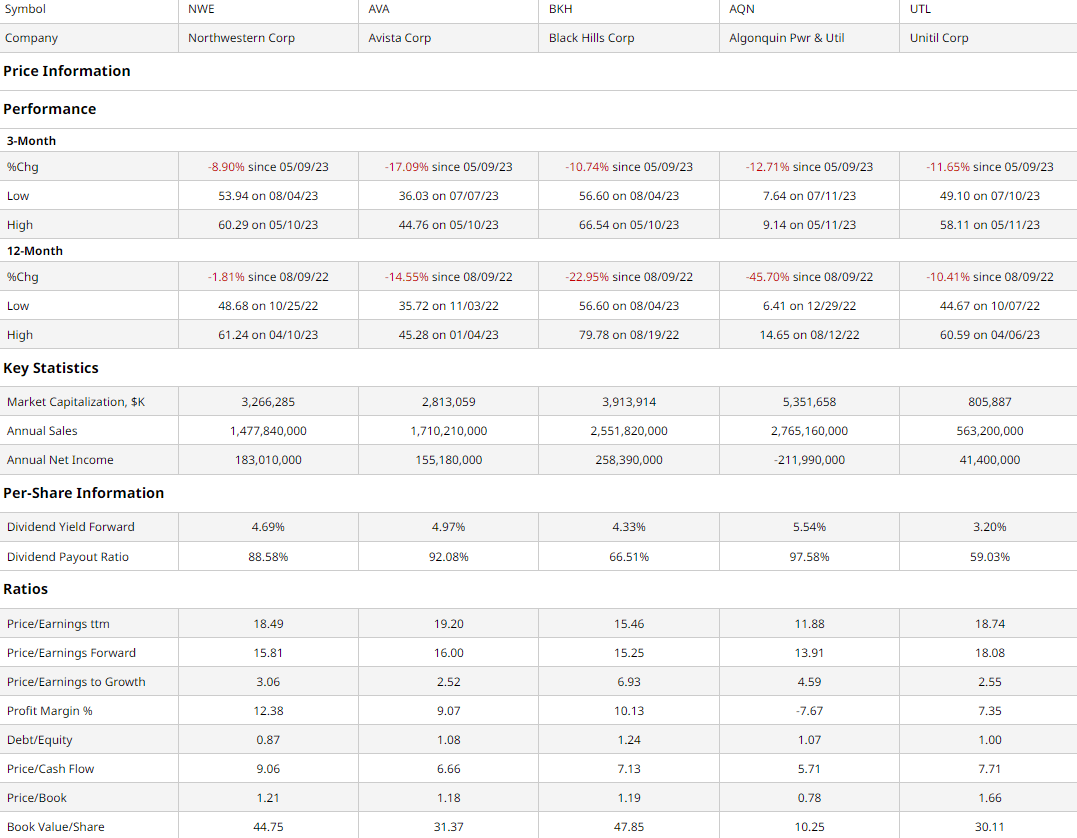

Comparable Companies

Utilities inherently remain natural monopolies, constricted by geographic and operational realities. As such, although utilities are consolidated on a regional level, nationally they are still fragmented. As such, I seek to compare NWE with similarly sized multi-utilities across the US. This group includes Spokane, Washington-based electricity and gas distributor, Avista ( AVA ), Rapid City, South Dakota-based utility Black Hills Corporation ( BKH ), Canadian renewables and utility conglomerate, Algonquin Power & Utilities ( AQN ), and Hampton, New Hampshire-based New England-servicer, Unitil ( UTL )

{kind=link}

As demonstrated above, NWE has experienced both the best YoY price action in addition to the best quarterly price action. This dynamic can largely be attributed to the firm's superior operational capabilities and the firm's dominating presence in less penetrated markets, with lower tax rates and competitive intensity abound.

Despite this, I believe NWE remains fairly valued, trading above market value when assessing multiples, but retaining a sure footing in regard to its balance sheet and shareholder return capacities.

For instance, NWE maintains >15 trailing and forward P/E, alongside the highest P/CF ratio and second-highest P/B. Although temporary headwinds compressing profitability and cash flows may be skewing these ratios, it does not justify relative overvaluation.

However, when incorporating NWE's high but fiscally prudent dividend, the firm's larger margins, and the best debt/equity and joint-best book value per share, NWE looks to be fairly valued.

Valuation

According to my discounted cash flow valuation, at its base case, the net present value of NWE is $50.61, meaning, at its current price of $53.82, the stock is overvalued by 6%.

My model, calculated over 5 years without built-in perpetual growth, estimates a discount rate of 8%, reflecting the firm's low leverage and lower equity risk premium. To remain conservative, I additionally projected an average forward revenue growth rate of 2%, lower than the trailing 5Y average of 2.86%, but incorporating the effects of rising interest rates and increased regulatory rate pressure.

{kind=link}

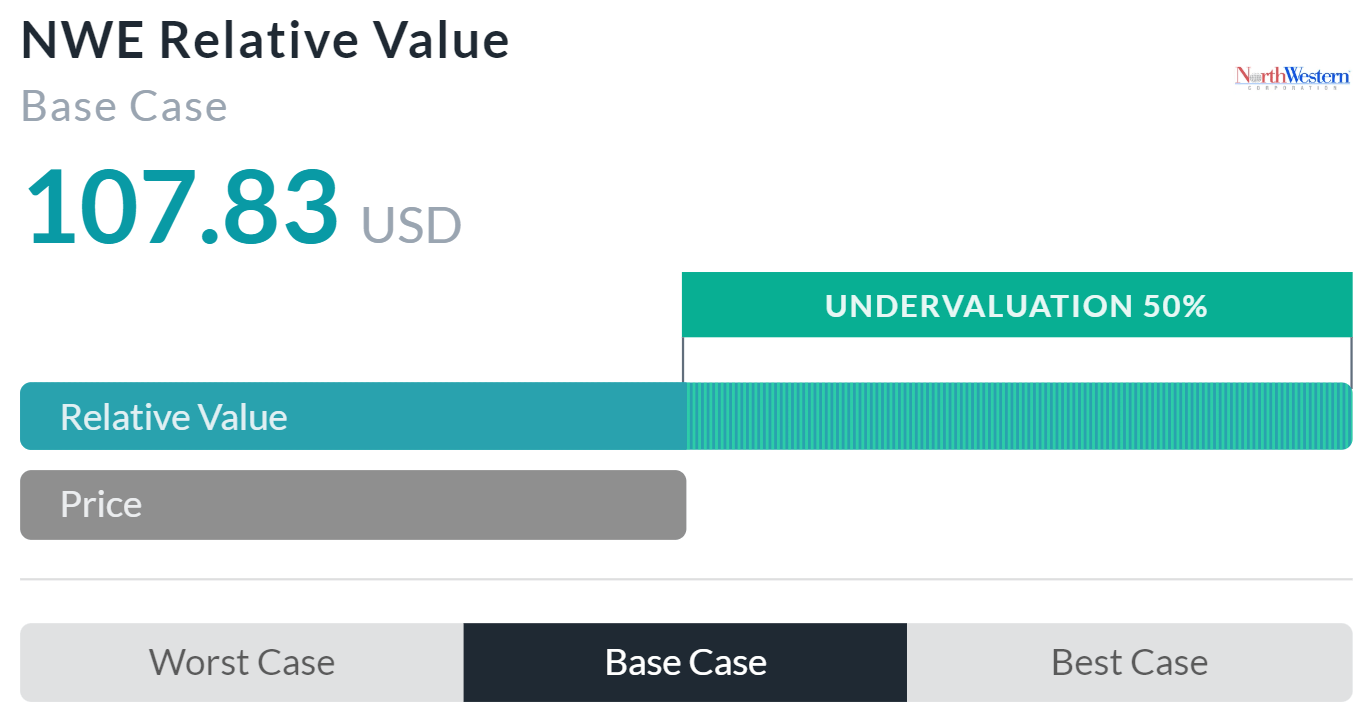

On the other hand, Alpha Spread's multiples-centric relative valuation model estimates that NWE is undervalued by 50%, with a fair value of $107.83.

Regardless, I believe Alpha Spread's model artificially inflates the stock's value, unable to adequately discount for dividends, incorporate forward risk, and with multiples skewed by outliers and macro uncertainties alike.

As such, although Alpha Spread's model is informative as to how other utilities are reacting to general forward uncertainty and is a testament to NWE's resilience, I believe my NPV accurately represents the value of the company.

NWE Operationally Builds Off of Macro Tailwinds, Strong Foundation

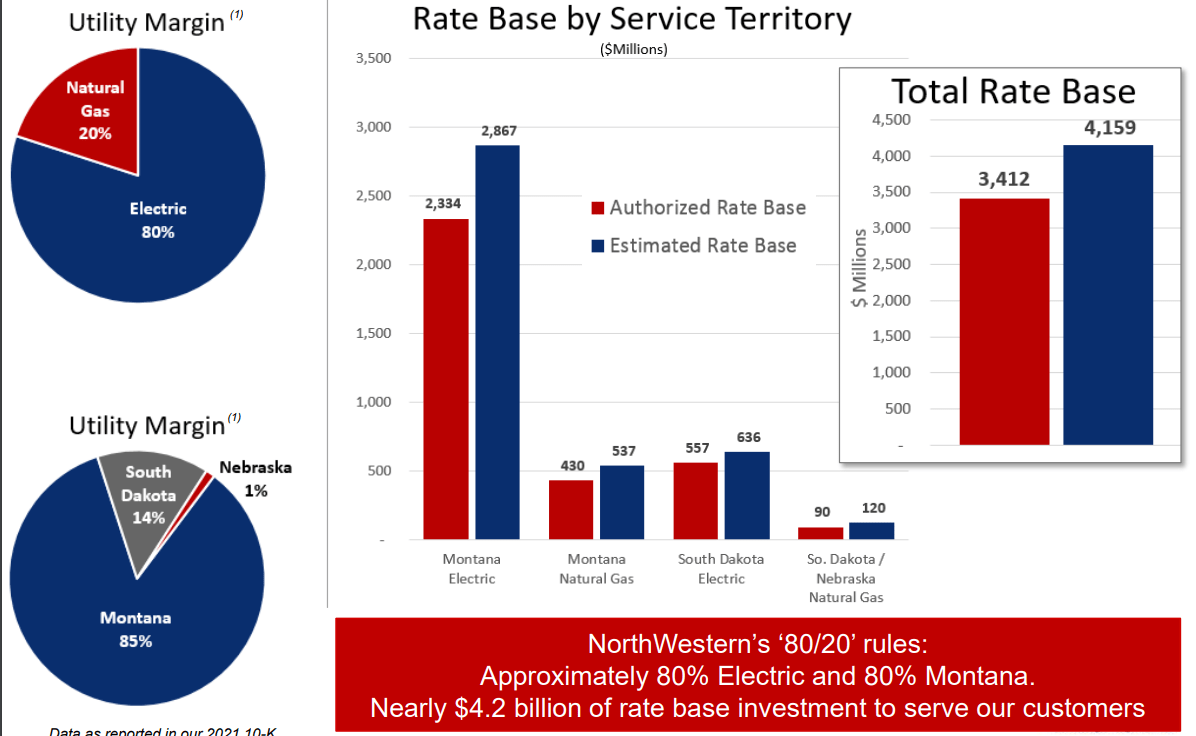

The underlying value proposition for NWE remains its well-diversified and secure rate base. The firm maintains stable cash flows across three states, through electric and natural gas products, with a growing rate base across all geographies and verticals. Alongside its commitment to ESG inclusionary investments and slow rate increases below peer increase velocities, NWE sustains a customer base that is both loyal, can see increase unit revenue extraction, and sees gradual margin increases.

{kind=link}

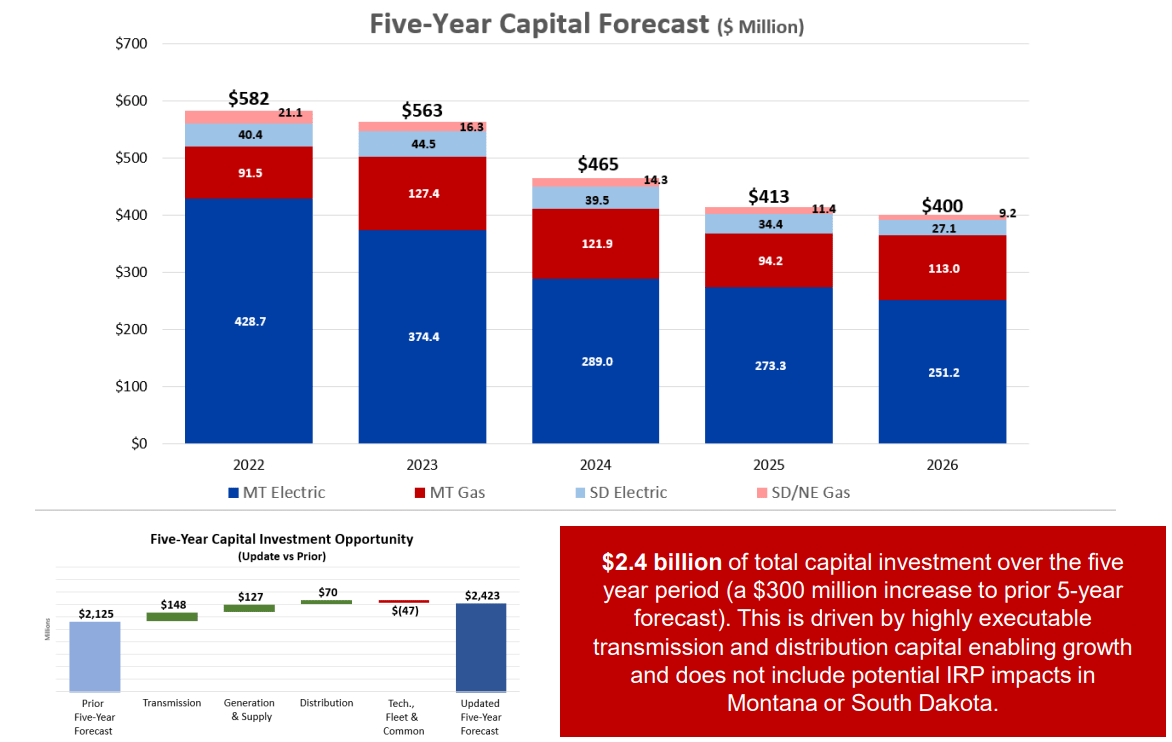

NWE's fundamental strengths are enhanced by its medium-term capital strategy, which emphasizes a versatile capital expenditure arrangement of $2.4bn from the FY22 to FY23 period. To position itself and leverage public investment from the Inflation Reduction Act and the Infrastructure Investment & Jobs Act, NWE's forward capital investment strategy focuses on transmission, generation, and distribution investments above others, securing rate base cash flows and tax advantages.

{kind=link}

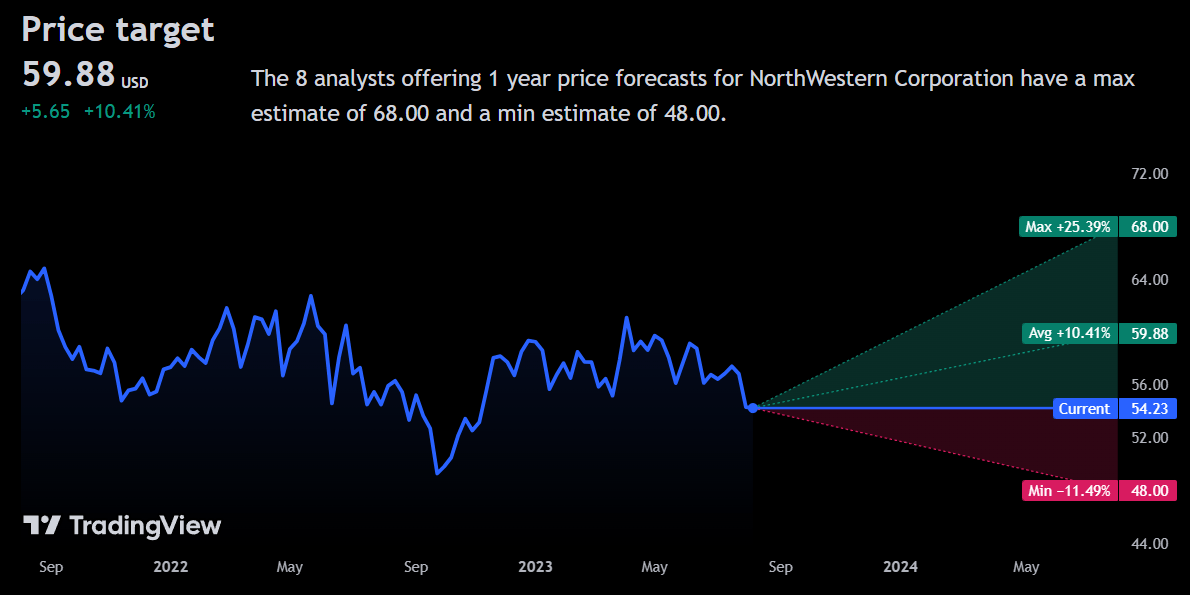

Wall Street Consensus

Analysts largely support a positive view of NWE, projecting an average 1Y price increase of 10.41% to a price of $59.88.

{kind=link}

However, at the minimum predicted price target, analysts foresee an 11.49% decline to a price of $48.00.

I believe these movements are more so a reflection of investor anxieties about interest rates rather than beliefs on the company's operational or financial situation, with higher interest rates supporting negative price movement and vice versa.

Risks & Challenges

Interest Rates Effect Equity Price & Operational Behaviour

Although, as discussed in the 'Comparable Companies' section, NWE maintains a fairly low relative debt/equity ratio, and thus is not as affected by rising interest rates operationally, the firm is privy to the attractiveness of alternative investments with superior risk-adjusted returns. As such, investors may experience poorer price movement, leading to a higher cost of equity and increased leverage, costing more due to the aforementioned interest rates.

High Degree of Regulatory Complexity Inhibit General Capabilities

To its benefit, NWE's positioning in Montana and surrounding states lowers its risk of exposure to climate-related risks and, by extension, regulations. Nonetheless, the company remains sensitive to government and consumer demands for rate hike control. Any extended period of price control may inhibit NWE's long-run profitability, ability to return income to investors, and growth as an organization.

Conclusion

NWE remains a stable income stock, with strong regional positioning and a favourable dividend. However, the firm does trade at or above fair value, and investors may experience limited negative price action.

For further details see:

NorthWestern Remains An Ideal Income Pick, Is Fairly Valued