NOV - NOV: 2023 Off To A Bad Start

2023-03-27 17:43:30 ET

Summary

- Despite seeing green shoots for a recovery growing larger and stronger during 2022, sadly the fourth quarter saw weaker financial performance for NOV Inc.

- Even more worryingly, the United States oil and gas rig count is now dropping.

- This makes weaker financial performance more likely, especially given the recent banking crisis that could foretell a recession.

- At least NOV Inc. is well-positioned to outlast another downturn given their low leverage and strong liquidity.

- Given this mixture, I believe that maintaining my hold rating on NOV Inc. is appropriate.

Introduction

Despite NOV Inc. ( NOV ) seeing green shoots for a recovery growing larger and stronger during 2022, back in early 2023 I felt it was time to lock in some profits. Their share price was up circa 30% because, as my previous article warned, they were unlikely to see significantly stronger financial performance. As fate would prove, their share price subsequently dropped over 20% and, sadly, it sees 2023 off to a bad start with harder days likely ahead.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

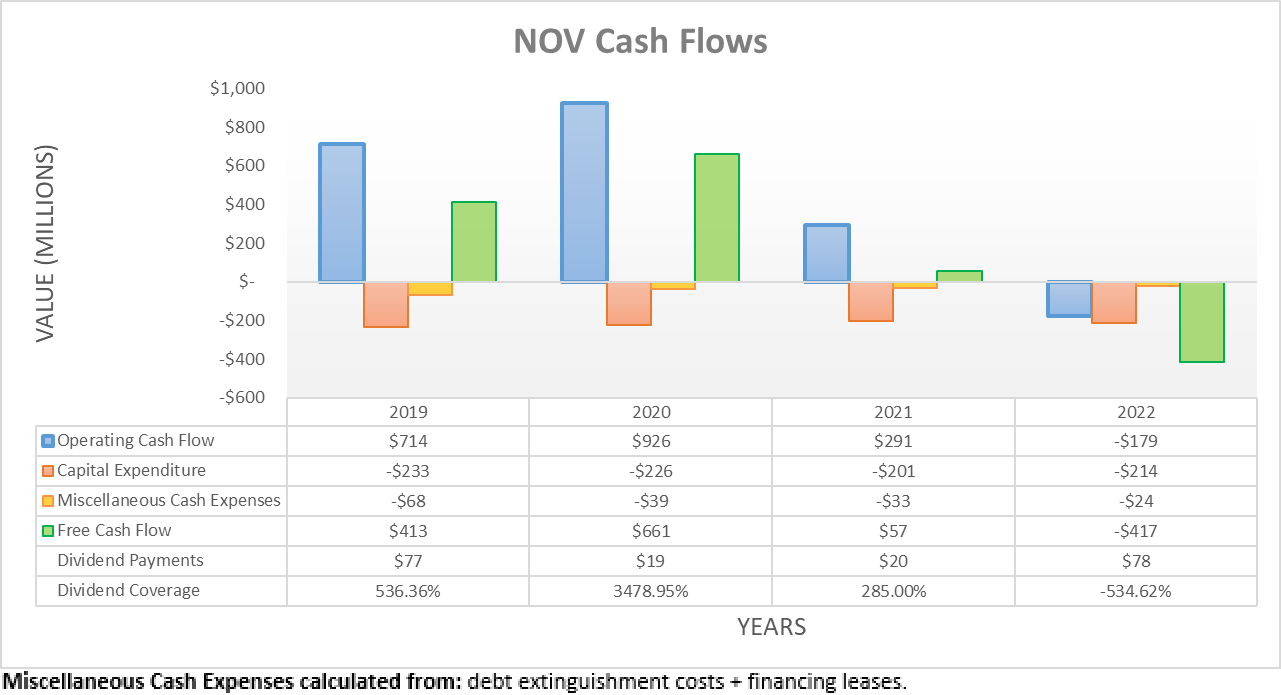

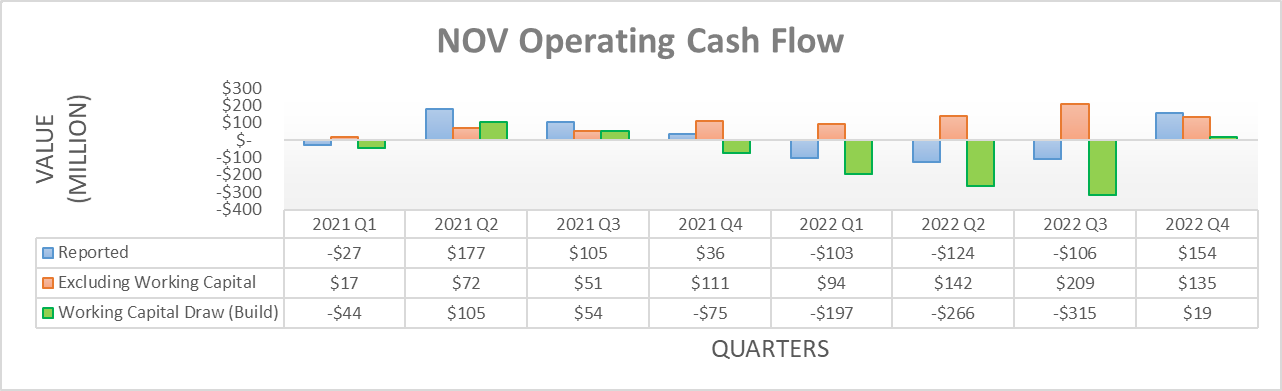

After seeing the NOV Inc. cash flow performance marred by a very large working capital build during the first nine months of 2022, thankfully the fourth quarter finally saw a reprieve. Although, this was still insufficient to reach a positive result with the full-year landing at negative $179m, but at least if nothing else, it nevertheless is better than their previous result of negative $333m during the first nine months.

{kind=link}

Whilst positive on the surface to see a cash inflow for the first time in a year, beneath the surface the fourth quarter of 2022 was actually disappointing. Once excluding their working capital movements that marred their reported results throughout the year, their underlying result was only $135m and thus disappointingly, it is a weaker result versus their previous equivalent result of $209m during the third quarter. Sadly, this appears to have trimmed the green shoots of a recovery that my previous analysis highlighted and thus does not create strong momentum for 2023, especially given the accompanying situation within the oil and gas rig count in the United States.

Y-Charts

When conducting the previous analysis, the United States oil and gas rig count had stagnated after only increasing marginally higher to 772. Well, fast forward a few months to the present day and disappointingly, this stagnation ultimately gave way, alongside oil and gas prices. As a result, the oil and gas rig count is now only 758 and whilst yes, this is only a small decrease, it nevertheless is not a positive sign for their upcoming financial performance. Furthermore, there is a lag before the recent turmoil from the banking crisis flows through to oil and gas drilling and thus if anything, the rig count is likely to drop lower in the coming weeks and months.

If the Western world slides into a recession as feared later in 2023, this will prove toxic for oil and gas drilling in the United States, especially as oil and gas companies have remained cautious about expanding production even during 2022 when oil prices surged to triple-digit levels. Whilst making a perfect prediction is not possible given the inherent volatility of their industry, this sees 2023 off to a bad start with harder days likely ahead.

{kind=link}

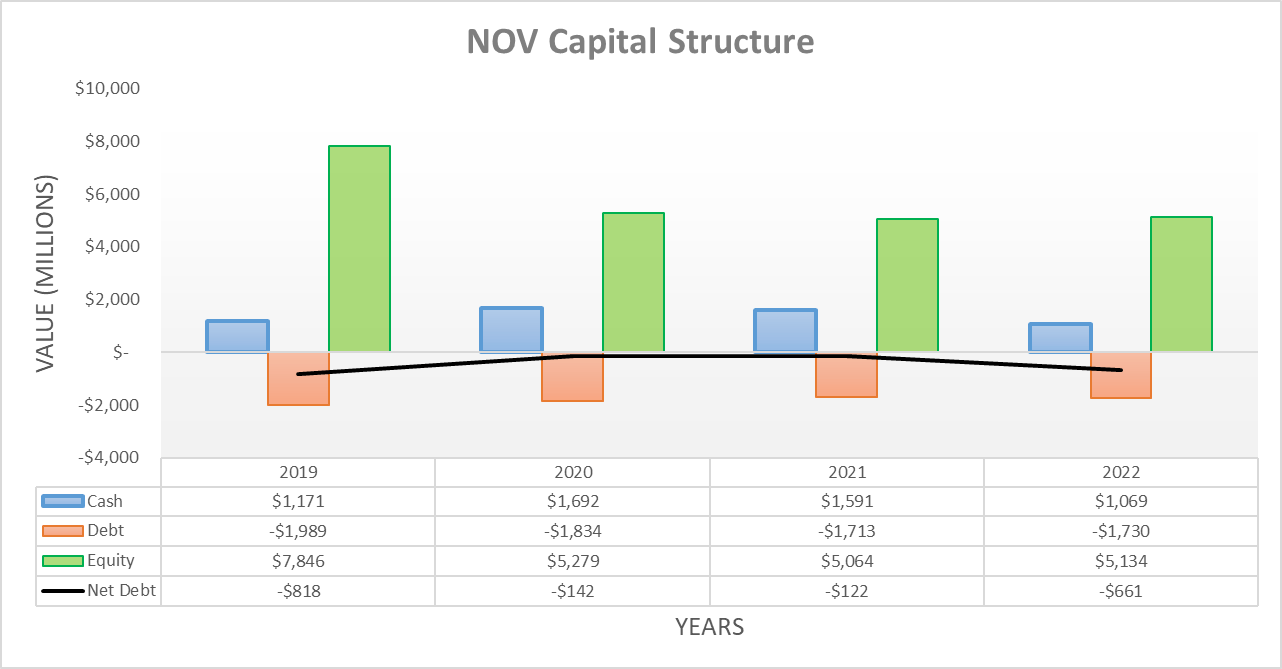

Even though their underlying cash flow performance was weaker during the fourth quarter of 2022, it was able to see their net debt drop lower thanks to their aforementioned working capital builds ending. As a result, their net debt dropped to $661m and thus is down modestly versus its previous level of $732m following the third quarter. Despite their financial performance being anything but desirable lately, at least this capital structure does not retain significant net debt, hence this relatively noticeable change following only one weak quarter. This provides resilience heading into uncertain times, especially as the volatility of their operating cash flow makes it impossible to accurately predict the direction of their net debt going forwards into 2023.

{kind=link}

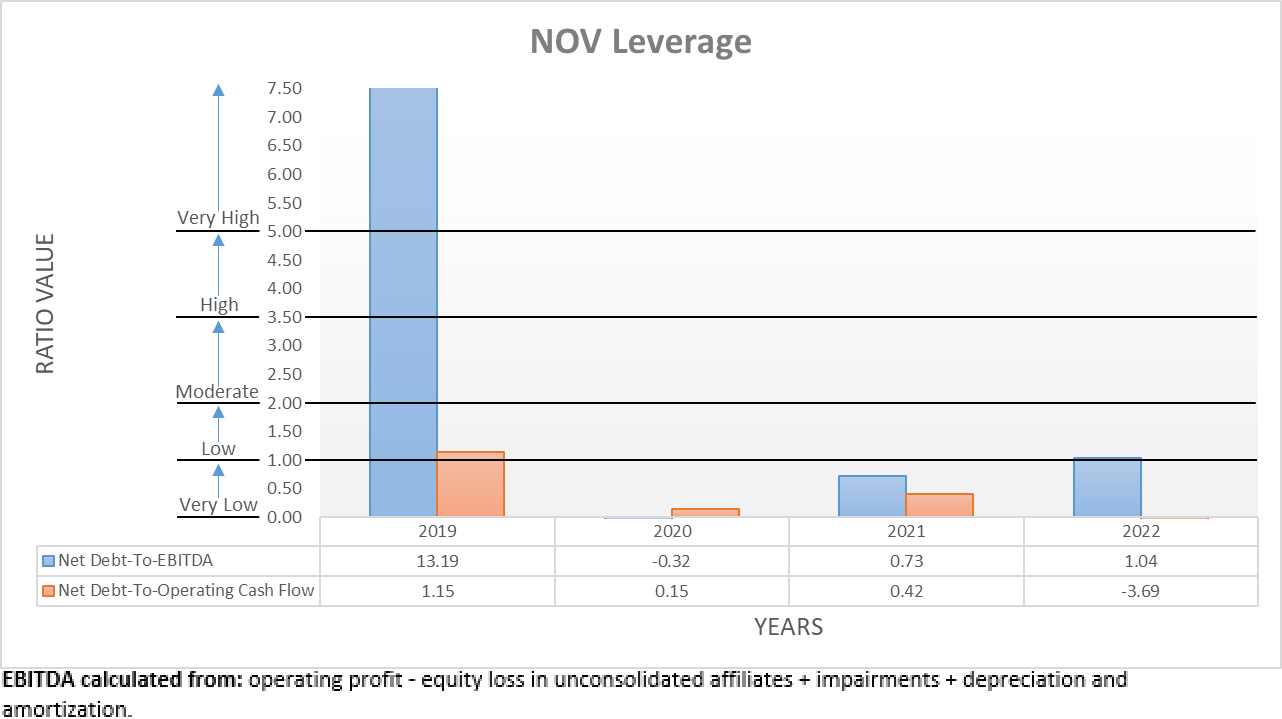

Since 2022 still saw a very large working capital build overall despite the small relief during the fourth quarter, the resulting negative operating cash flow renders their net debt-to-operating cash flow useless with logically invalid negative results. At least their accompanying net debt-to-EBITDA only sees a result of 1.04, which thanks in part to their net debt dropping is modestly lower versus their previous result of 1.53 following the third quarter. Even though the outlook for 2023 is anything but ideal right now, at least this nevertheless places their leverage right at the bottom of the low territory of between 1.01 and 2.00, which further supports their resilience heading into uncertain times.

{kind=link}

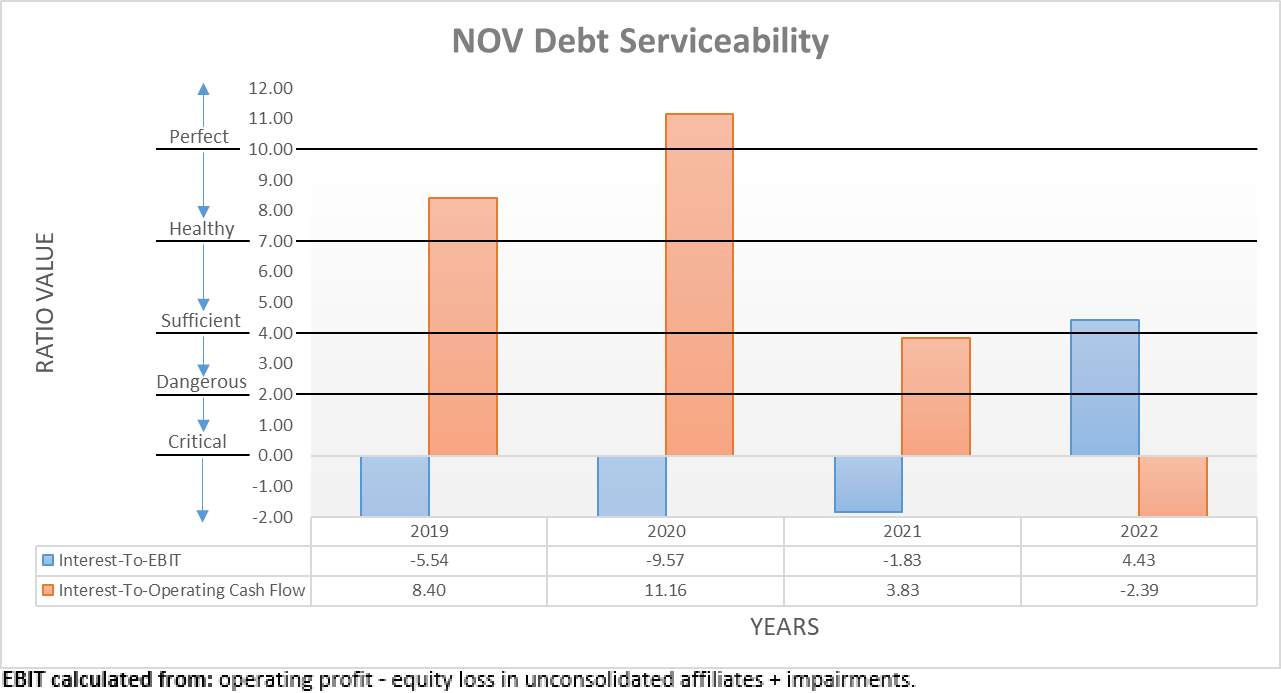

Once again, their negative operating cash flow renders any comparison against their interest expense useless. Regardless, at least the accompanying comparison against their EBIT sees interest coverage of 4.43 that is within the range I consider as healthy, albeit narrowly. Similar to their leverage, this further supports their resilience heading into uncertain times given the margin of safety it affords before dropping to dangerous levels, although it is not actually the most important consideration.

{kind=link}

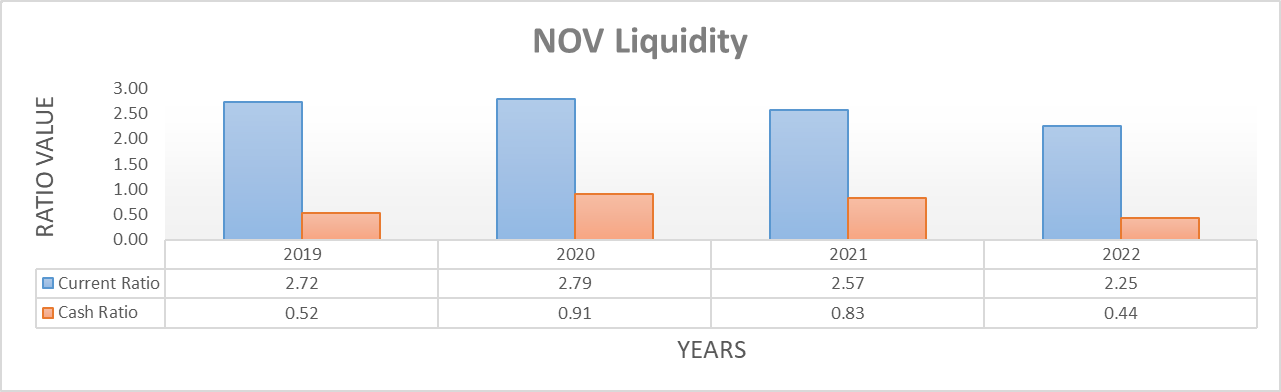

When facing the prospects of a downturn, especially one driven by banks collapsing, their liquidity is actually the most important consideration, at least in my opinion. Thankfully, it remains strong following the fourth quarter of 2022 with their current and cash ratios seeing respective results of 2.25 and 0.44, which are almost identical to their previous respective results of 2.30 and 0.44 following the third quarter.

Thanks to their large cash balance of $1.069b following the fourth quarter of 2022, it provides resilience heading into uncertain times by removing their reliance upon capital markets to bridge any potential gaps within their cash inflows and accompanying outflows. Since they are not a large company, it is equally as important that most of their debt does not mature until December 2042 with the remainder not coming due until December 2029, as per their 2022 10-K . When combined, this effectively isolates the company from the banking crisis as much as possible, although they still have no option other than enduring the likely impact to their financial performance via lower oil and gas drilling.

Conclusion

Even before considering the banking crisis, the United States oil and gas rig count dropping lower sees 2023 off to a bad start, especially after NOV Inc. saw weaker financial performance during the fourth quarter of 2022 that did not create strong momentum when the calendar flicked over. Whilst it remains to be seen whether the banking crisis continues amplifying, thus far into the year everything seems to be dashing hopes for a continued recovery, which is particularly disappointing given that NOV Inc. shareholders barely had a chance to enjoy any recovery from the severe downturn of 2020. Thankfully, the low NOV Inc. leverage and strong liquidity see them well-positioned to outlast another downturn and thus, despite this lackluster outlook, I believe that maintaining my hold rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from NOV’s SEC Filings , all calculated figures were performed by the author.

For further details see:

NOV: 2023 Off To A Bad Start