NG:CC - NovaGold: An Inferior Way To Play The Gold Price

2023-09-21 12:29:10 ET

Summary

- NovaGold's Donlin Gold Project is one of the largest undeveloped gold assets globally, but its high upfront capex and remote location make it a tough one to approve.

- And while it may seem cheap on a per-ounce basis, valuation per resource is high relative to optionality projects while P/NAV is high relative to advanced developers.

- NovaGold's stock is still not cheap, trading at a premium to its peers, and its future development and production timeline is uncertain, making it an unattractive investment.

Just over nine months ago, I wrote on NovaGold ( NG ), noting that there was no way to justify chasing the stock above US$6.25. This is because it was trading at a premium valuation reserved for multi-asset producers despite being a development-stage company that was likely at least eight years away from reaching commercial production. Since then, NovaGold has slid 30% vs. a 7% decline in the Gold Miners Index ( GDX ). Unfortunately, the stock still isn't offering any margin of safety; it remains expensive relative to its peers, and we're no closer to a construction decision on Donlin, and are actually arguably further away with Barrick (GOLD) reaffirming that its best growth opportunities that look to be the highest priority are in copper (Reko Diq 50%, Lumwana Super Pit). In this update, we'll dig into what makes Donlin special, why it hasn't been green-lighted, and look at its valuation vs. peers.

Donlin Gold Drilling - Company Website

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Donlin Gold Project

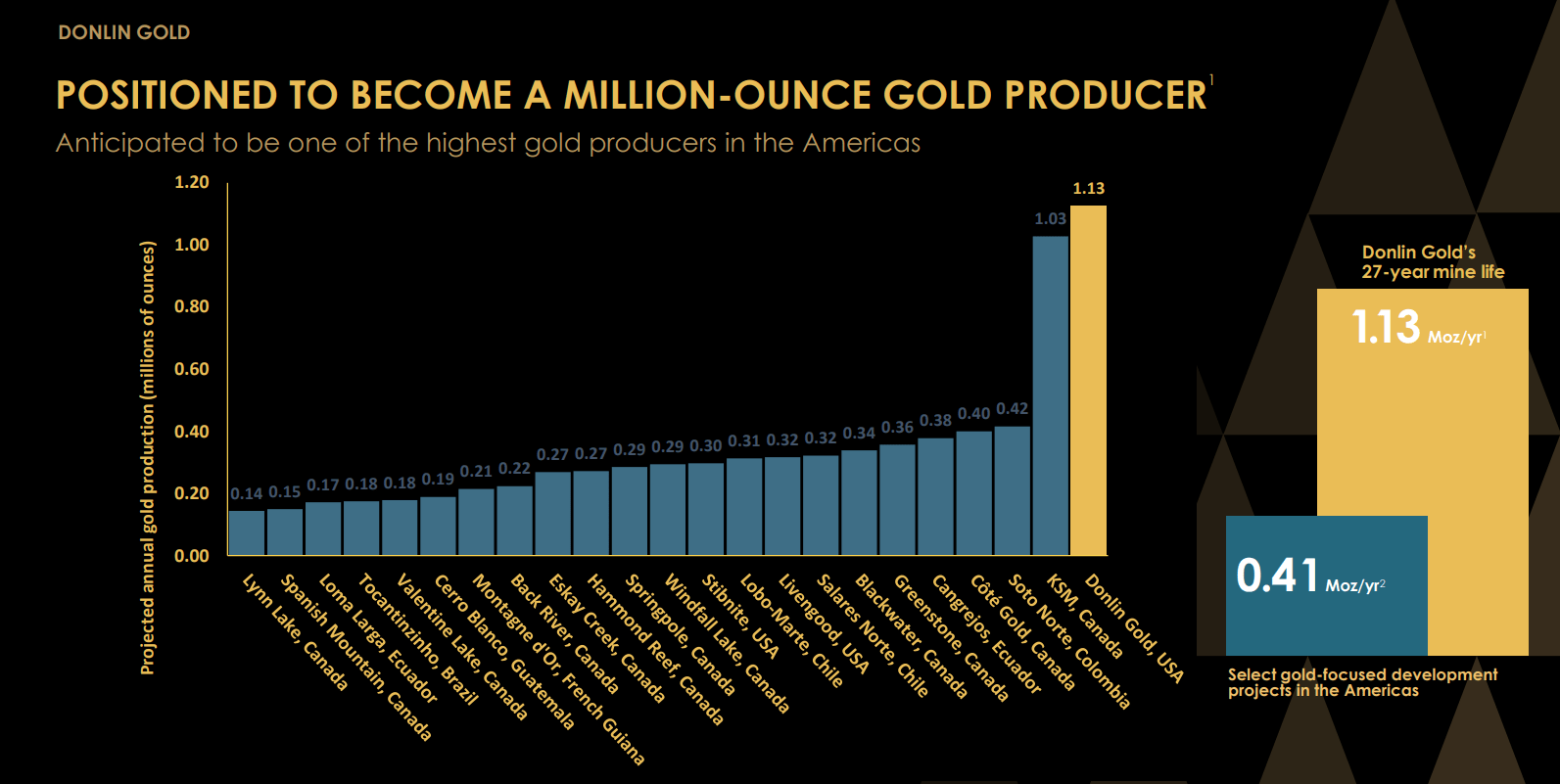

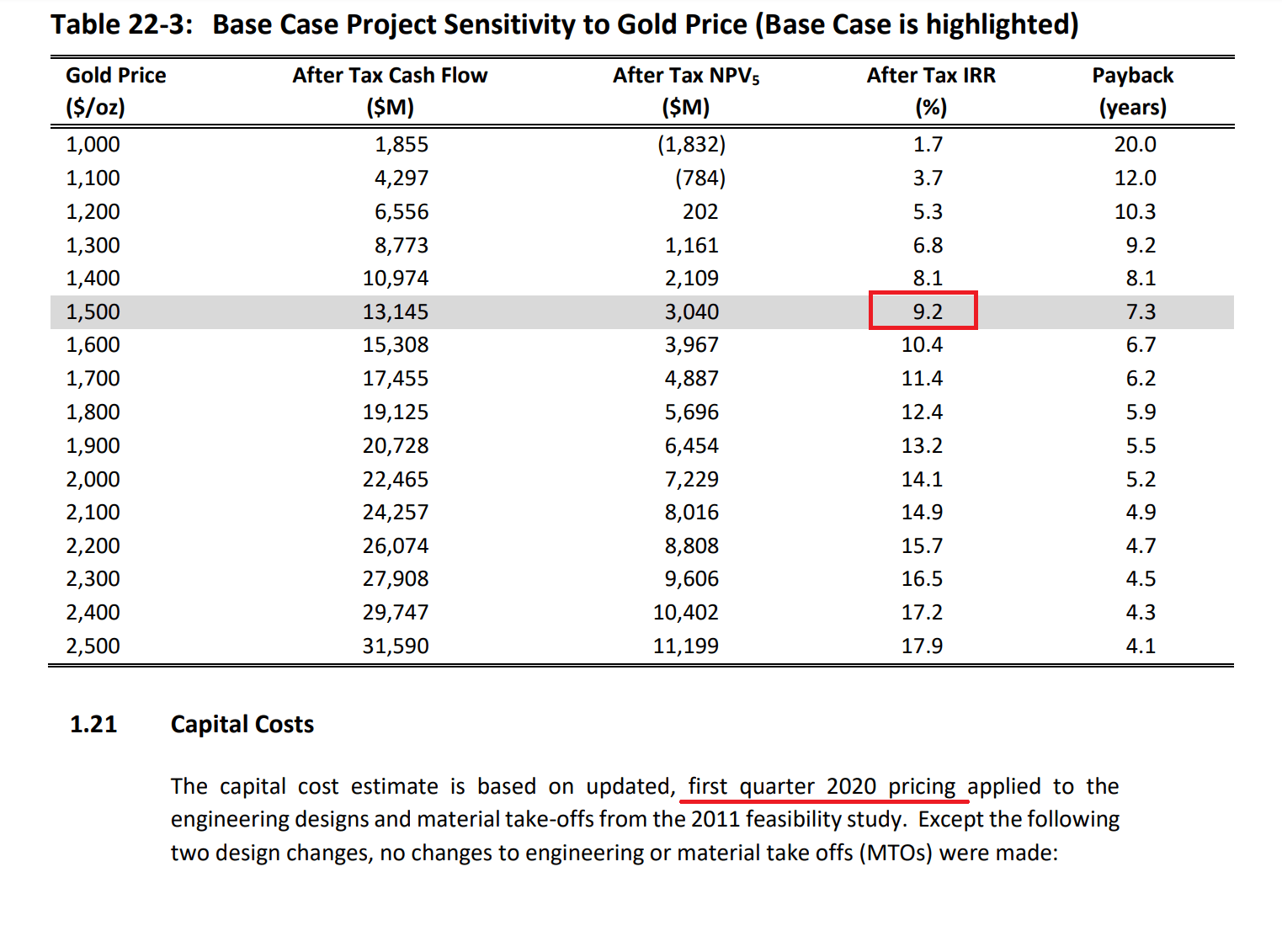

The Donlin Gold Project is one of the largest undeveloped gold assets globally, with an expected 27-year mine life and average annual production of ~1.1 million ounces based on a mineral inventory of over 30 million ounces of gold. This translates to ~16.9 million ounces for NovaGold's 50% ownership, and as the chart below highlights, the asset sits head and shoulders above its peers from an annual production standpoint in the Americas. The closest comparable is Seabridge's ( SA ) KSM deposit in Canada, and globally, Sukhoi Log in Siberia could produce ~2.3 million ounces per annum if developed (~40 million ounces of gold reserves) with it being a massive high-grade open-pit (~33 million tonnes per annum), with cash costs expected to come in below $400/oz. And unlike Donlin, initial capex is expected at less than $4.5 billion even when accounting for inflationary pressures, barely half of Donlin's expected upfront capex of ~$9.6 billion when factoring in 30% inflation vs. its Q1 2020 pricing estimates.

"The capital cost estimate is based on updated, first quarter 2020 pricing applied to the engineering designs and material take-offs from the 2011 feasibility study. The level of accuracy for the estimate is ±25% of estimated final costs, per Association for the Advancement of Cost Engineering [AACE] Class 3 definition.

- 2021 Donlin TR

Projected LOM Annual Production Profile Projects in Americas - Company Presentation

{kind=link}

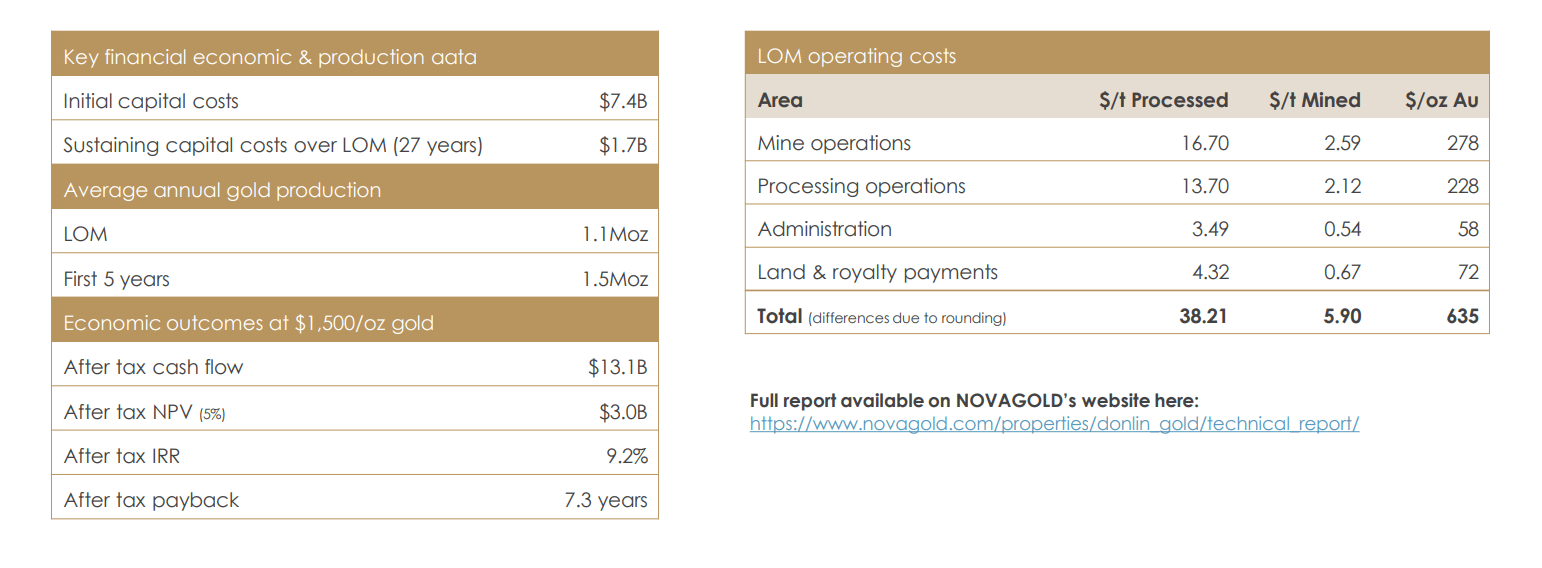

On paper, Donlin looks incredible, with after-tax cash flow generation of ~$13.1 billion even at a conservative $1,500/oz gold price, sub $40.00/tonne unit costs, and first five-year gold production of ~1.5 million ounces per annum, translating to 750,000 ounces attributable to NovaGold. To put this in perspective, this would be the equivalent of NovaGold owning its very own Detour Lake or Canadian Malartic, and if the company owned a producing asset of this scale, its valuation would look very different today. However, as noted, the elephant in the room is upfront capex, and it doesn't help that the most recent capex estimate was based on Q1 2020 pricing ahead of 40%+ inflation on greenfield projects in the period, and in three cases, capex blowouts of 80%+ (Magino, Cote Gold, Rochester POA 11).

Donlin Project Economics - Company Presentation

{kind=link}

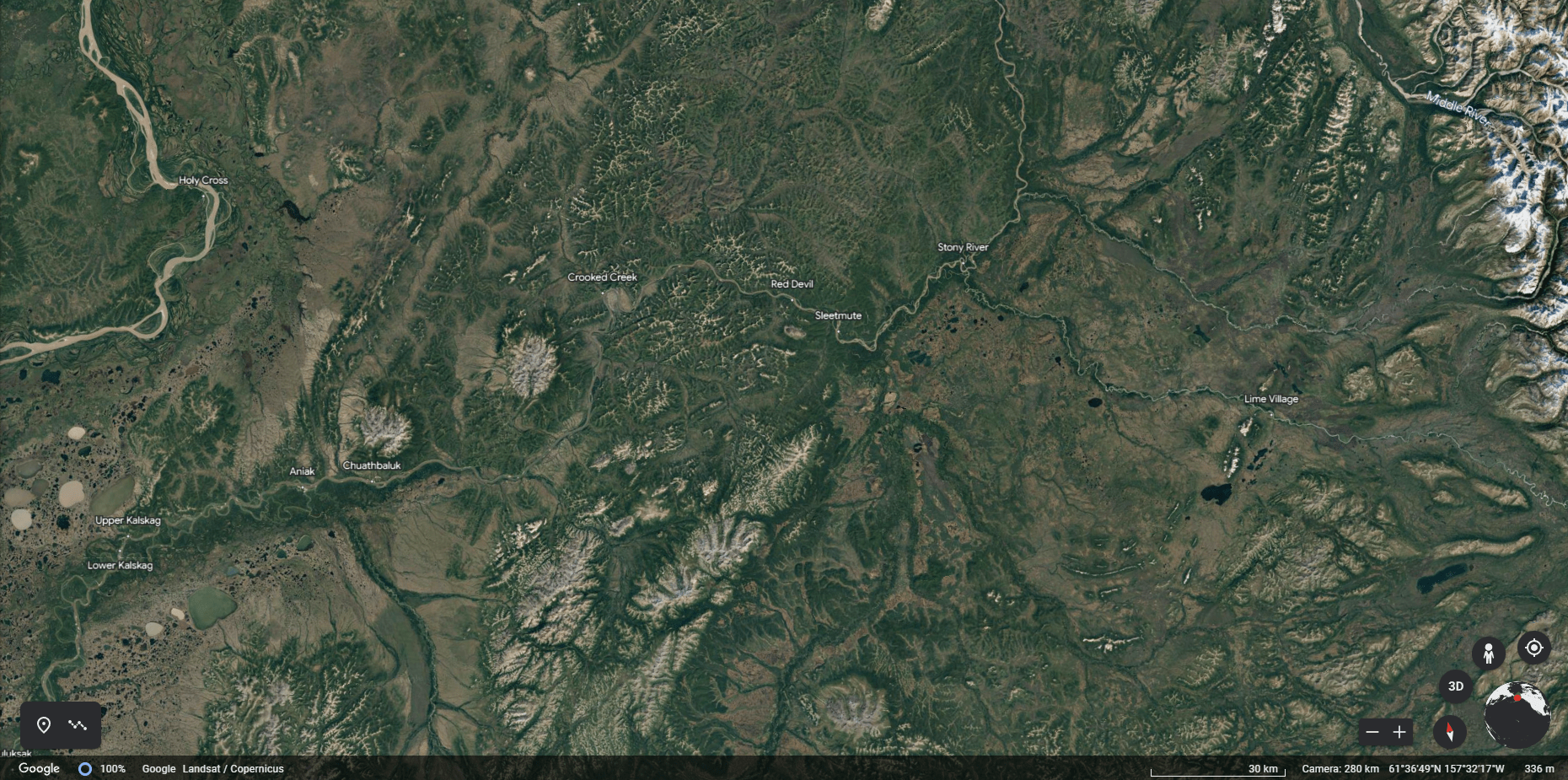

Not only does this increase NovaGold's share of project funding if it were to be green-lighted, it dents the after-tax IRR, and it could make its partner Barrick Gold less enthusiastic about building Donlin near-term given that it's looking for 15% IRRs. Plus, this doesn't even consider the associated impacts on the project's operating costs because of sticky labor/contractor inflation and consumables inflation. Hence, the above numbers (IRR, After-Tax NPV at 5%) are staler than month-old bread, never mind the much higher cost of debt for NovaGold to fund this project vs. Q1 2020 if it were green-lighted today. In summary, while Donlin is near unrivaled on production, the combination of a remote project, the need for an autoclave and the need for a 14 inch natural gas pipeline that spans 500 kilometers make it a very expensive project to build and this certainly affects expected returns for its owners.

Donlin Gold Project Area - Google Earth

{kind=link}

Some investors might note that trade-off studies and optimization work could help to reduce upfront capex and there are opportunities to build a lower-cost project upfront with a better payback. While this is certainly a valid point and something worth considering, I would argue that 30% plus inflation since Q1 2020 will offset much of the benefit of any trade-off studies or optimization work, suggesting that initial capex is still likely to come in well above $6.0 billion. And at these estimates, when combining higher operating costs than envisioned (labor/contractor inflation, consumables inflation) and conservative gold prices, the after-tax IRR is likely to remain below 9%, a full 600 basis points below Barrick's hurdle that it's discussed in the past for approving new projects. So, whether NovaGold wants to build this asset is irrelevant as it needs its partner to green-light it and that doesn't look likely near-term.

Donlin vs. Other Undeveloped Gold Projects

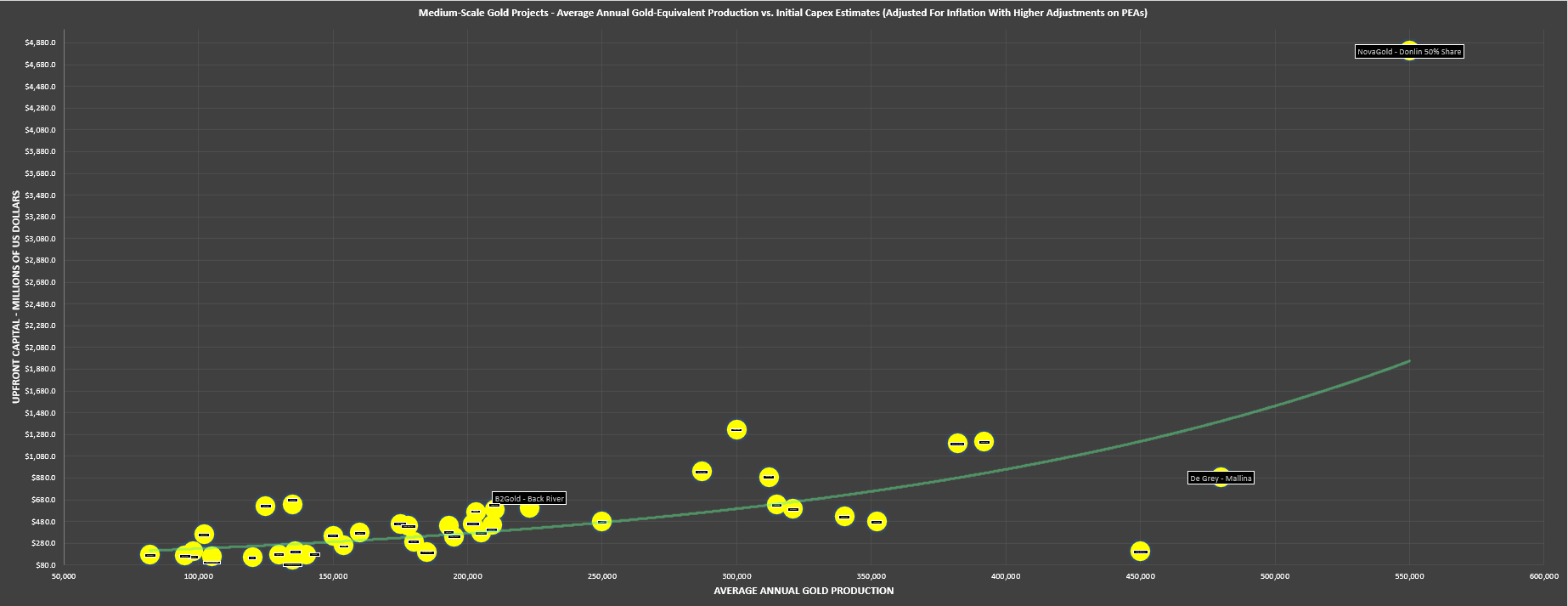

Looking at the Donlin Project vs. other projects, it's clear that it shines from a scale standpoint, dwarfing other undeveloped gold projects with attributable average annual production for NovaGold of ~570,000 ounces. However, as is clear from the chart, other projects have a lot of bang (200,000 to 500,000 ounces) for a lot less buck ($600 million to $1.2 billion) vs. Donlin's estimated capex of ~$4.5+ billion assuming no optimization work and when factoring inflationary pressures into the equation. In fact, this capex estimate might end up proving not conservative enough given that I think a minimum 30% inflation should be applied to Q1 2020 upfront capex estimates for any project.

Undeveloped Gold Projects (Initial Capex & Life of Mine Production) - Company Filings, Author's Chart & Estimates

{kind=link}

And in a sector where bigger is not always better when it also means significant capex as proven by the write-downs of the last cycle, I would argue that sub $700 million capex projects like Windfall, Back River acquired by B2Gold ( BTG ) and Mallina owned by De Grey Mining ( DGMLF ) are far more attractive than trying to build a monster asset in a remote location simply for a little over twice the annual production on average. Instead, two mid-sized 300,000 ounce projects that add up to a similar production profile for a combined capex of ~$1.6 billion would be a more conservative move, or one asset with ~$1.0+ billion in capex that can do ~450,000+ ounces like Mallina. In summary, if I were looking to own developers in a high-interest rate environment when financing is difficult and capex blowouts are still a risk, I would want to own those with modest capex and high margins, making them takeover targets and giving them the ability to go it alone if a suitor doesn't come knocking. NovaGold obviously does not fill this bill, and while it's avoided share dilution to date which is a silver lining, it will eventually have to take on debt or start selling shares post-2025 if G&A remains at similar levels.

Valuation

NovaGold trades at a market cap of ~$1.56 billion based on ~346 million fully diluted shares (year-end estimate) which would appear to be a very reasonable valuation for a company with a reserve base of ~16.9 million ounces of gold in a Tier-1 jurisdiction. However, as pointed out earlier, a stock's valuation per ounce of gold held in resources/reserves often correlates to the likelihood that the project will be developed at all (or developed in a timely manner). And if we compare NovaGold's value of ~$80/oz on M&I resources to some other optionality names with significant capex bills like Vista Gold ( VGZ ), International Tower Hill ( THM ), First Mining Gold ( FFMGF ), and Seabridge Gold, NovaGold is actually quite expensive, with these companies trading below $30/oz on a median and average basis. And while Donlin undoubtedly deserves a premium for exceptional open-pit grades and higher grades overall than these projects, I don't see a high likelihood of this project heading into production before 2032.

First Mining Gold trades at ~$22/oz on M&I resources on solely Springpole ounces, which does not include Duparquet in Quebec (~3.4 million ounces in M&I category).

This is an opportunity cost when several producers are returning capital to shareholders (dividends, buybacks). It's also an opportunity cost when several other advanced-stage developers are likely to pour gold before 2028 and enjoy a re-rating as they go from a depressed P/NAV multiple to a more reasonable P/NAV multiple above 0.80x as they de-risk. Finally, although some believe that a higher gold price will help Donlin to finally get green-lighted, this isn't a project that can be built overnight, and while other producers will increase their dividends (or potentially pay special dividends) and generating enormous amounts of free cash flow immediately if the gold price heads above $2,500/oz at some point, NovaGold will still be stuck waiting for Donlin to move into commercial production even if a construction decision is made. Hence, I don't see the investment thesis here.

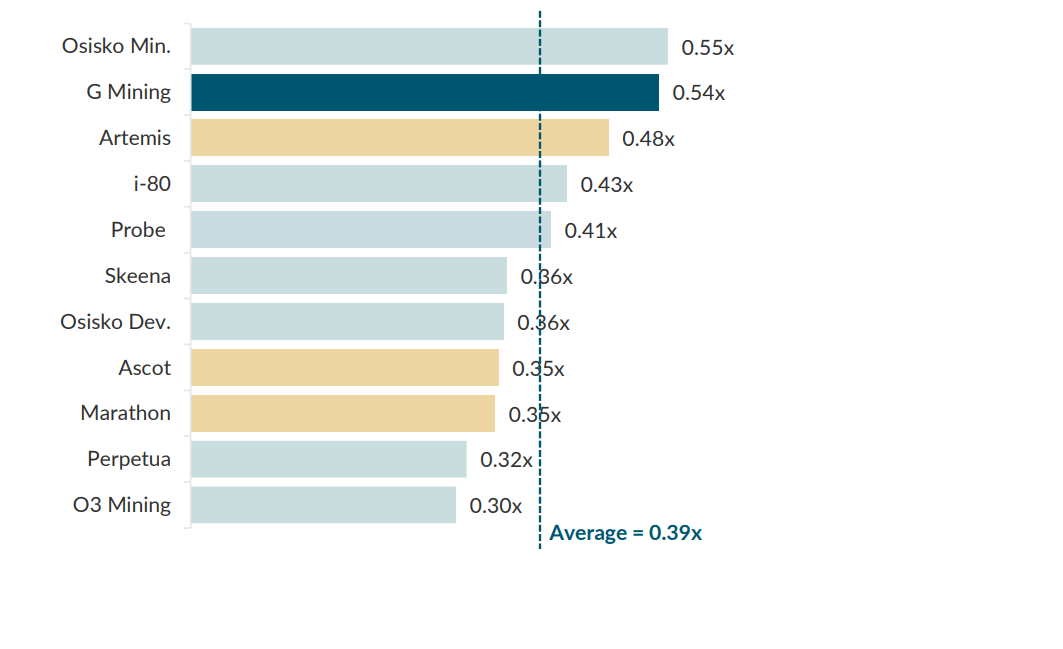

Americas Developers - P/NAV Multiples - FactSet, Company Filings , G Mining Ventures Presentation

{kind=link}

Finally, if we look at Donlin from a P/NAV standpoint, the stock still isn't cheap after its violent correction, trading at ~0.67x P/NAV on 50% of an estimated NPV (5%) of ~$4.6 billion when accounting for inflationary pressures, a large premium to the developer average of ~0.39x as of the end of August. I would argue that NovaGold should trade in the lower end of this developer range (0.30x - 0.55x) given that it's not financed, it doesn't control its own destiny, and it will likely be 2032 at the earliest before commercial production begins, suggesting the stock still isn't cheap enough. And even if we use a generous 0.85x P/NAV multiple at a 5% discount rate to value NovaGold (~$2.3 billion [-] $160 million in corporate G&A = $2.14 billion), I see a fair value for NovaGold of US$5.25 per share, pointing to just a 20% upside from current levels. This might interest some investors, but I want a minimum 50% discount to fair value to justify buying a developer, so I don't see any margin of safety here, and wouldn't become interested in the stock unless it fell below US$2.70 per share.

Some investors will disagree with this view and note that Barrick Gold could buy out NovaGold tomorrow and this would provide shareholders with a large premium takeover. However, there are four reasons this seems unlikely anytime soon.

1. Barrick's CEO Mark Bristow has historically been very disciplined regarding M&A, and I would be shocked to see him offer a large premium for a developer.

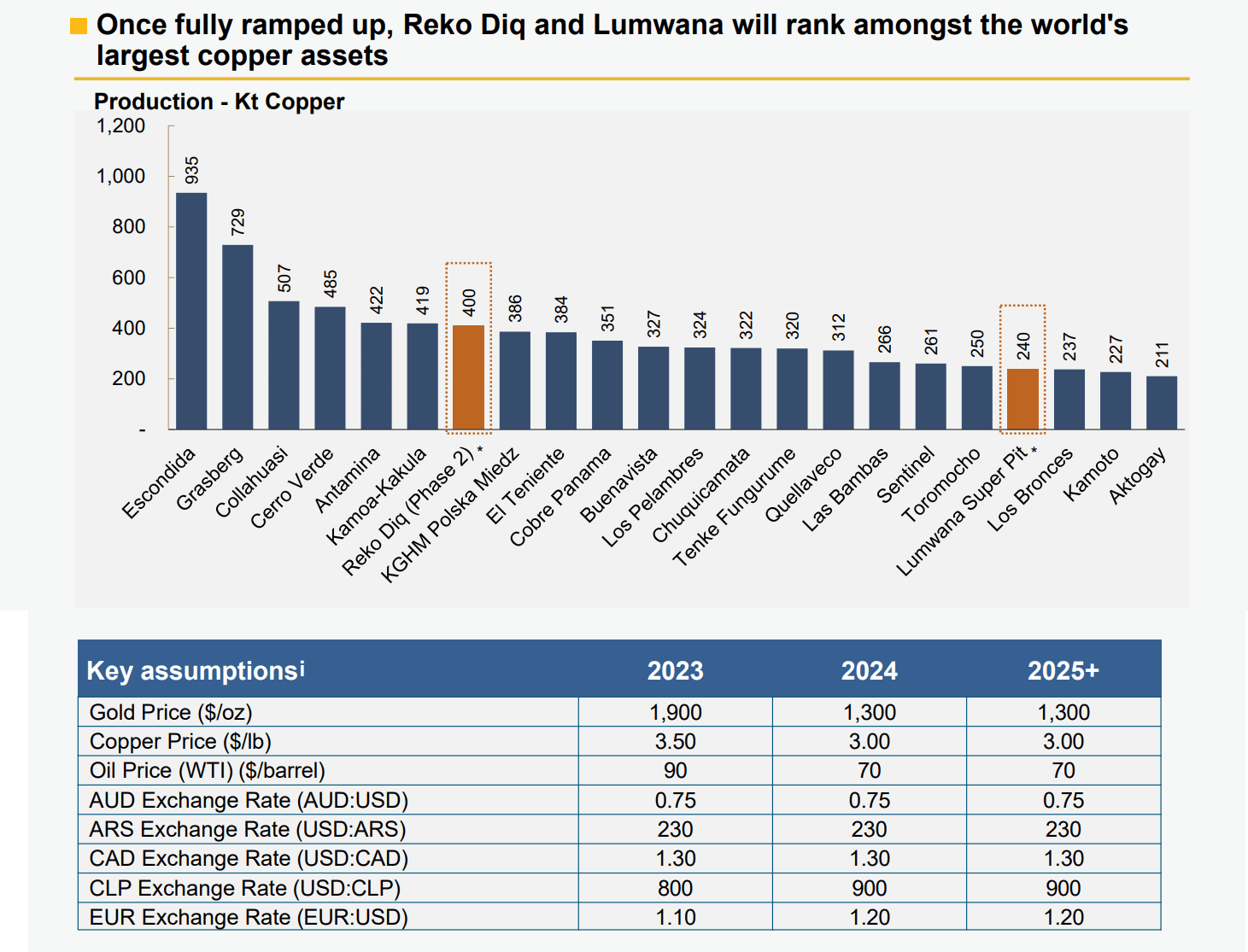

Barrick Gold - Reko Diq & Lumwana Super Pit & Base Case Assumptions - Company Presentation

{kind=link}

2. Barrick has two large capex projects that appear to be higher priority with higher IRRs: Reko Diq and Lumwana Super Pit. With these two major growth projects in the wings, I don't see Barrick approving a third, and certainly not one with a mid-single-digit IRR based on the 2021 TR when factoring in inflationary pressures from Q1 2020 and based on its more conservative metals price assumptions (sub $1,500/oz).

Donlin Gold Internal Rate of Return Before Inflationary Pressures (Q1 2020 Pricing) - Donlin TR

{kind=link}

3 . As noted earlier, there are several less capital-intensive development projects elsewhere in the sector if Barrick were to take a non-organic approach and some smaller producers are also attractively valued, with these arguably being better non-organic opportunities than buying the other half of Donlin today.

4 . Most gold producers do not suddenly adjust their long-term gold price assumptions for calculating reserves and approving projects because gold trades higher, they use long-term averages, evidenced by senior producers miners using $1,250/oz - $1,500/oz (Barrick: $1,300/oz) vs. a three-year average of $1,850/oz. Hence, I don't see Barrick suddenly raising its base case assumptions to $1,800/oz to push Donlin towards a more respectable IRR unless gold spends a couple of years above $2,400/oz.

Summary

NovaGold has underperformed the GDX year-to-date and I don't see any reason for this to change given that the company is expensive relative to other advanced developers and even expensive on a P/NAV basis relative to many producers. In addition, the company does not control its own destiny, and has a partner that's focused on other growth projects. This is not an enviable position to be in, and if one believes we'll see a bull market in gold, the real winners will be those selling the metal, not those stuck in the least favorable portion of the Lassonde Curve (permitting/financing/construction) with a low likelihood of any gold being poured at Donlin before 2031. Hence, I continue to see NG as an inferior way to buy the dip and I would view any rallies above US$4.75 before year-end as an opportunity to book some profits.

For further details see:

NovaGold: An Inferior Way To Play The Gold Price