NG:CC - NovaGold: Don't Chase The Stock Here

Summary

- NovaGold was one of the better-performing gold developers in 2022, down just 12% for the year vs. several 40-50% declines among other gold developers.

- This outperformance is likely related to the fact that it massively underperformed its benchmark in the prior year with a 30% decline vs. the 11% decline in the GDX.

- While NovaGold continues to be a favorite optionality play, I see it close to fully valued at $6.20, trading above 1.0x estimated attributable NPV (5%) when adjusting for inflationary pressures.

- So, while the stock could continue too rally with the benefit of a rising gold price, I don't see any way to justify chasing the stock above US$6.25 here.

2022 was a rollercoaster ride of a year for the Gold Miners Index ( GDX ), swinging from a 30% gain to a 31% loss before finishing the year down 10.0%, a decent performance given the sharp losses in the S&P-500 ( SPY ) and Nasdaq Composite. I was fortunate to put together a positive gain for the year by taking advantage of some of the swings, but I did miss on a few trades and entries, including a poorly-timed bullish call on Wallbridge ( OTCQX:WLBMF ), where I had to cut my losses, and being brutally early on Agnico Eagle ( AEM ) at $50.00 per share. I believe strongly in staying disciplined once a thesis is built and a buy target is established for a stock, but sometimes that rigidness can result in missing an entry, as it did with NovaGold ( NG ). My buy target was US$3.90, but the stock bottomed 4% above this level in September, so I missed establishing a position. It's soared over 50% since.

{kind=link}

This significant outperformance for NovaGold vs. all other developers has surprised me, given that, unlike NovaGold, many developers are well advanced, can fund their projects independently, and could be in production as early as H2-2025. One example is Osisko Mining ( OTCPK:OBNNF ) which just released a Feasibility Study for its Windfall Project in James Bay, Quebec, and hopes to start production by Q4 2025 if it can get permits before year-end and put together a financing package. However, in NovaGold's case, it continues to look like the company will be lucky to pour its first gold before the end of the decade, with the Donlin Partnership working on trade-off studies and toward making a Feasibility Study decision.

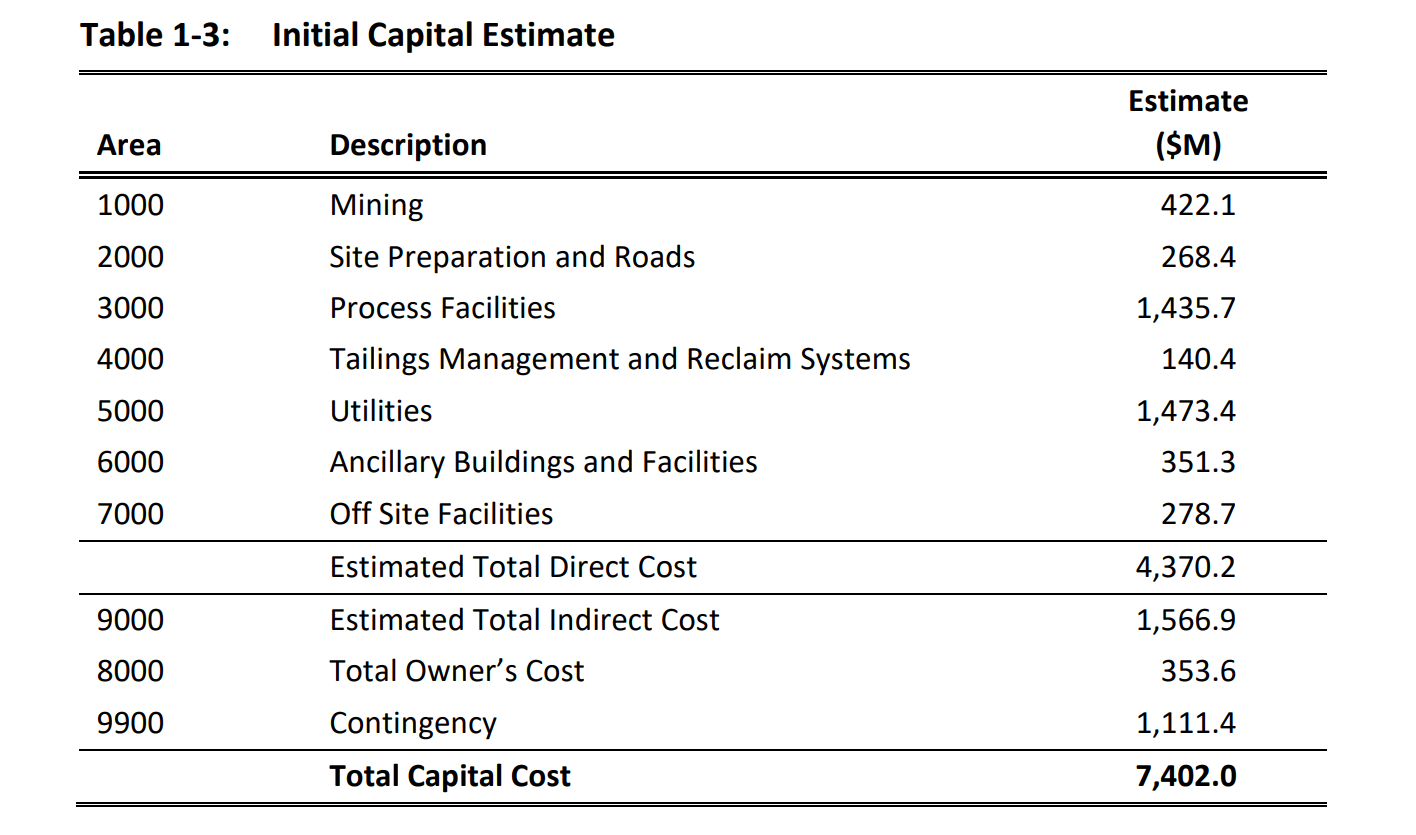

The other issue for NovaGold is that nearly all of the largest and mid-scale miners sector-wide have seen considerable inflation resulting in revised capex estimates on projects that have yet to begin, including those that were well advanced before inflation hit. Some examples include the Tanami Expansion, Magino, Valentine, Cote Lake, Gramalote, Fetekro, Media Luna, and several others. So, while trade-off studies might have some positive impact, I would not be surprised to see a minimum 15% increase in upfront capex for Donlin, which already boasts a projected capex bill of $7.4 billion. Let's take a closer look at recent developments and how the stock looks after its recent rally.

{kind=link}

Q3 Results & Recent Developments

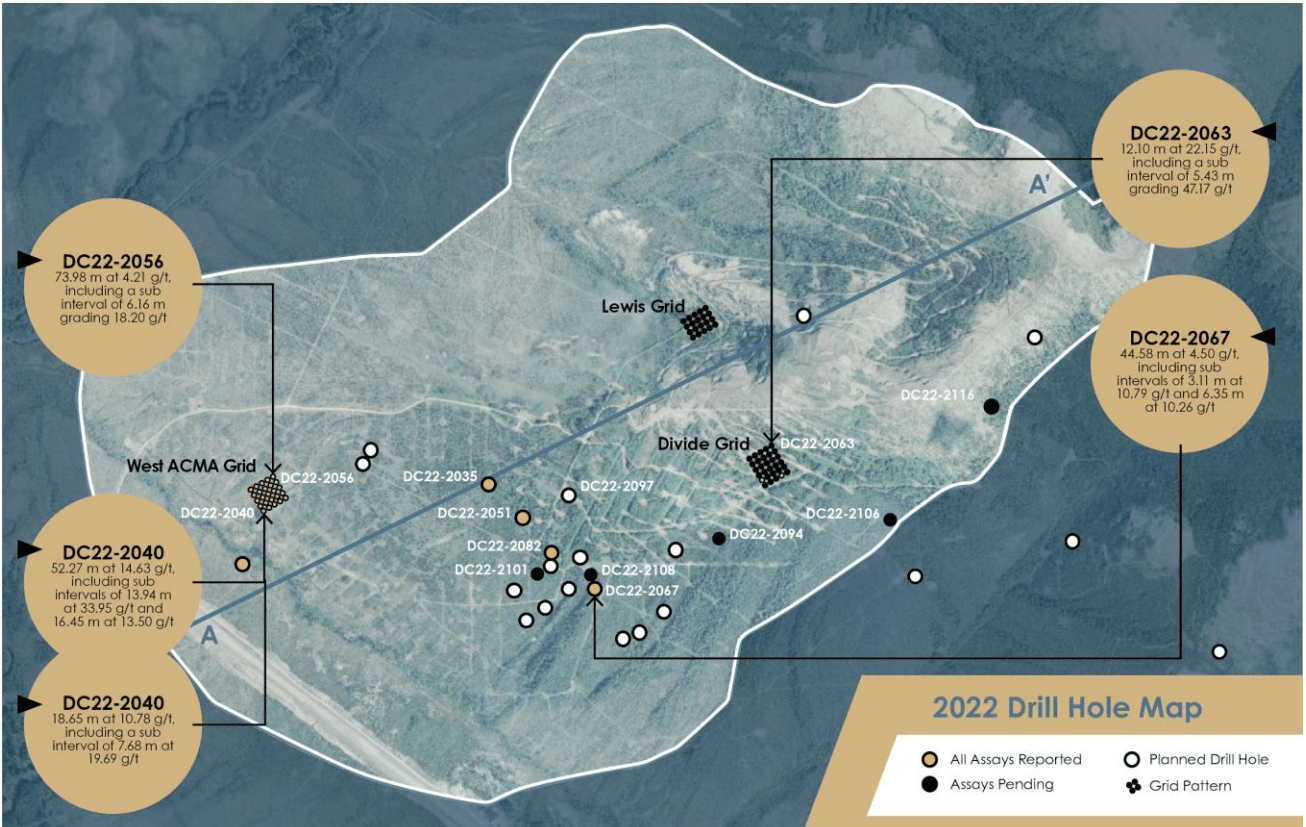

NovaGold released its Q3 results in October and noted that its ~42,000-meter 2022 drill program was wrapping up, and results have exceeded my expectations, with several solid intercepts that confirm the project's industry-leading open-pit grades. The focus of drilling was on tight-spaced drilling and in-pit and ex-pit exploration, and the two highlight holes were 42.28 meters at 30.68 grams per tonne of gold and 52.27 meters of 14.63 grams per tonne of gold, with several other 300+ gram-meter intercepts. These are world-class results, with NovaGold's partner Barrick ( GOLD ) noting that "significant progress was made enhancing the geological and mineral resource models" and that the geological model has been improved, which "confirms the size and continuity of the ore bodies."

{kind=link}

This is certainly exciting news for both companies, but especially NovaGold, given that cash flow from this asset would be a serious needle-mover for a ~$2.2 billion company like NovaGold compared to Barrick, which already has a ~4.5 million-ounce per annum gold production profile. That said, while the continued positive drill results, which confirm Donlin's robust grades, should give Barrick more confidence in continuing to direct dollars toward the Alaskan Project, there's one negative thing working against Donlin's economics. This is the fact that inflation has soared since the partnership released its last Technical Report with Q1 2020 cost inputs, and putting this ~1.3 million-ounce per annum project into production was already expected to cost $7.4 billion.

Initial Capex Estimate Donlin (100% Basis) (Donlin Technical Report)

{kind=link}

Even if we assume just 15% inflation on upfront capex, which I would argue to be conservative, this would place upfront capex at ~$8.5 billion or more than double Barrick's expected capex bill for its Reko Diq Project that it green-lighted in Pakistan (expected production in 2028). This is not a small amount of cash flow to spend by any means, even on an attributable basis ($4.25 billion), representing more than a full year of operating cash flow for Barrick. For NovaGold, this isn't a figure to sneeze at either, and while debt is an option, the company would likely see significant share dilution as well to help fund its portion of the project. In fact, we could see minor share dilution even before Donlin is green-lighted if it takes until 2026, with ~$145 million in cash at year-end for NovaGold and assuming a $45 million burn rate per year.

Ultimately, the key will be whether the project meets Barrick's rigid criteria, but Barrick tends to use very conservative gold/copper prices when modeling new and prospective projects, and even at a $1,500/oz gold price (above Barrick's conservative assumptions), Donlin had a 9.2% IRR and this was before inflation. So, even if we see positive impacts from trade-off studies, I would expect some offset from inflationary pressures and difficulty getting this above a 10.0% IRR at a $1,500/oz gold price. Obviously, if this were another operator willing to use more aggressive prices, this might be a different story. However, I can't see Barrick making a production decision on Donlin utilizing a gold price above $1,550/oz, and that's what matters to NovaGold with them being partners.

To summarize, while the drill results are phenomenal, the project has considerable exploration upside, and the fact that Barrick still continues to discuss this as a core project is positive. Still, one can't only list the positives without pointing out the negatives, which are:

- Potentially higher-cost debt for NovaGold due to higher interest rates

- Potentially a much higher capex bill for its share

- Potentially weaker project economics due to inflation which could impact mining and processing costs, upfront capex, and sustaining capital

How Donlin Stacks Up Vs. Other Projects

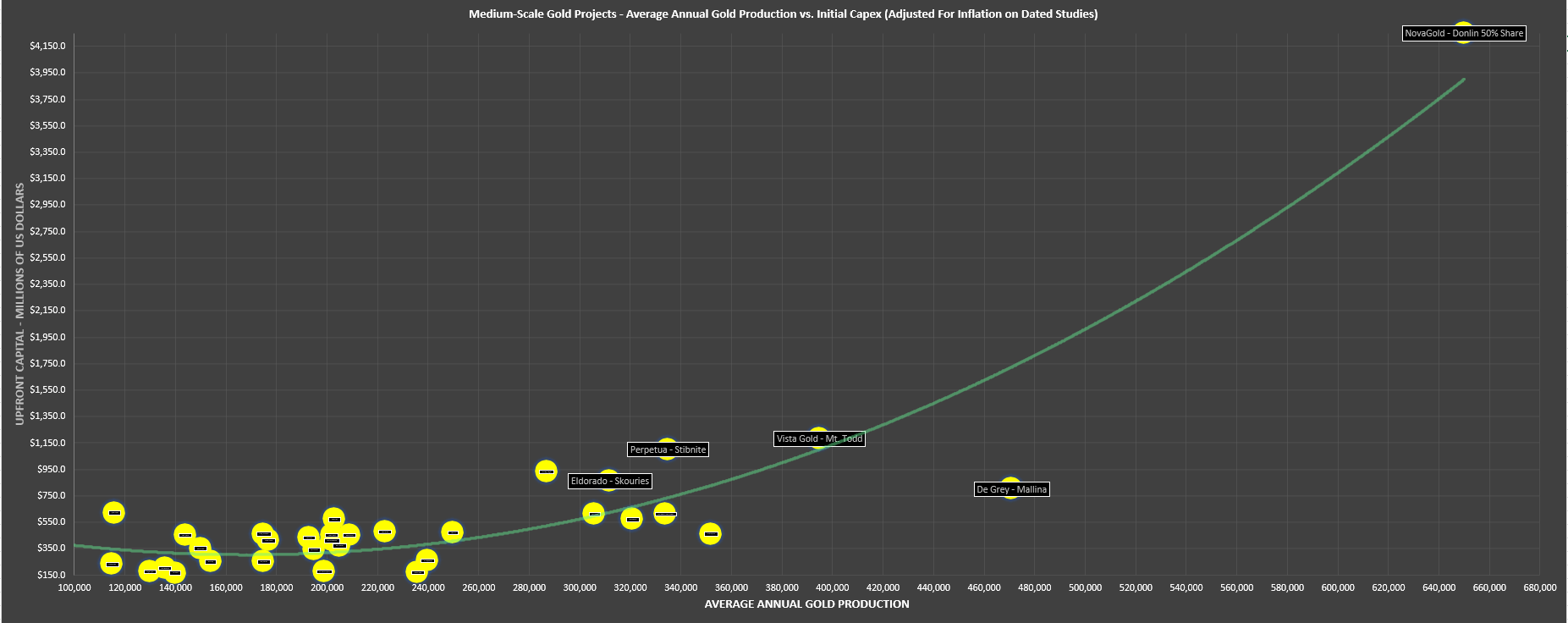

For those unfamiliar with Donlin, this is truly an incredible project. This is why NovaGold commands such a high market cap despite being a company still years away from generating positive cash flow. Looking at the numbers, the mine would produce ~1.5 million ounces of gold (100% basis) in its first five years of production and would enjoy 55%+ cash operating margins even if we factor in some cost creep due to inflationary pressures. As it stands, it's expected that a future mine would operate at a 53,500 tonne per day rate and process 2.0+ gram per tonne material over a 27-year mine life with 355 operating days per year due to weather conditions.

Undeveloped Gold Projects vs. NovaGold 50% Donlin Share (Company Filings, Author's Chart & Estimates)

{kind=link}

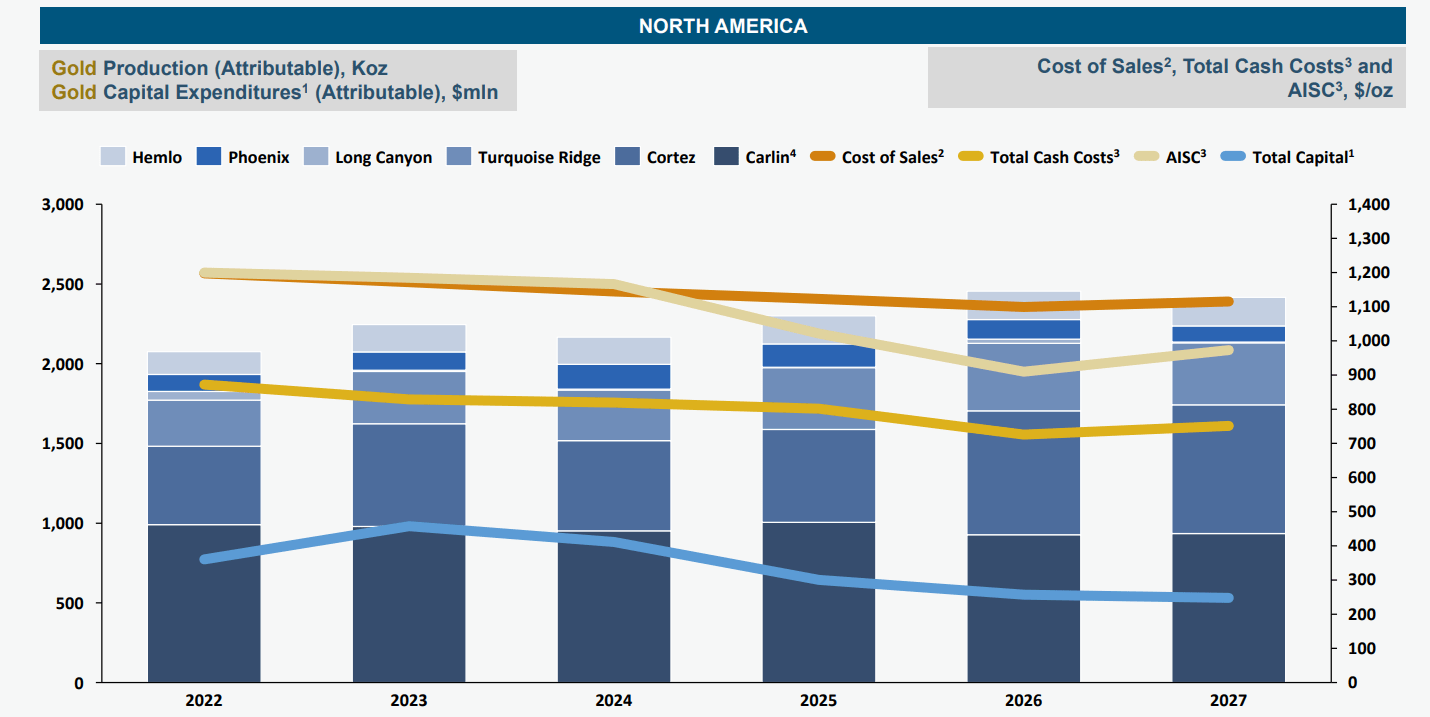

To put this in perspective, NovaGold's 50% share of this mine over its first five years would be larger than Osisko's Windfall, and Skeena's ( SKE ) Eskay Creek combined, and it would generate over $13.0 billion in after-tax cash flow over its mine life based on the 2021 Technical Report. However, as I've tried to make clear above, the one negative about this project is that it is not cheap to build, and while NovaGold needs Donlin to graduate to producer status, Barrick does not need Donlin, at least not this decade. In fact, the company's portfolio is looking the best it has in years, including its Nevada portfolio after the creation of NGM and three years with its new CEO Mark Bristow at the helm.

Hence, NovaGold is in the unfortunate position of not being able to advance this without a partner, and its partner isn't desperate to add a new major mine.

Barrick Gold - Nevada Production/Cost Profile (Barrick Investor Day)

{kind=link}

Meanwhile, several other developers may not have ~650,000-ounce per annum projects, but they do have very robust projects, and they're in a position where they can fund these projects with a mix of debt and equity or mostly debt in the case of 40% plus IRR projects. I would argue that a developer with a great project and a clearer timeline to move it into production with limited dilution is in a better position than an even better project but without any real clarity on when it might reach production.

The other benefit to owning 100% of a project with strong economics but very modest capex is that this developer could see an accelerated re-rating if a major decides to launch a takeover offer. Some examples include Liberty Gold ( OTCQX:LGDTF ), Osisko Mining, Skeena Resources, and Sabina Gold & Silver ( OTCQX:SGSVF ), which are moderately advanced to well advanced with world-class projects in Tier-1 jurisdictions, but with ~$600 million or less capex bills. So, while I think Donlin is truly a unique project which we may not see a repeat of as major discoveries have become so rare, the better way to get exposure to this asset looks to be through Barrick, which should benefit from it but will pay attractive capital returns in the meantime to shareholders.

Meanwhile, I continue to see other names as superior to NovaGold for the above reasons when it comes to getting exposure to the gold price in the developer space.

Valuation & Technical Picture

Based on ~345 million fully-diluted shares and a share price of US$6.20, NovaGold trades at a market cap of $2.14 billion or an enterprise value of ~$1.98 billion. This compares unfavorably to an estimated After-Tax NPV (5%) of ~$3.8 billion at $1,700/oz gold after adjusting for increased upfront costs and higher operating costs due to inflationary pressures seen in the sector since the 2021 Technical Report that relied on Q1 2020 pricing. On a 50% basis, this places NovaGold's fair value for Donlin at ~$1.9 billion and leaves NG trading at 1.13x P/NAV. I would argue that this leaves NovaGold fully valued, given that a 1.1x P/NAV multiple is generous for a developer that does not control their own destiny (a shared project with an inability to fund it alone).

{kind=link}

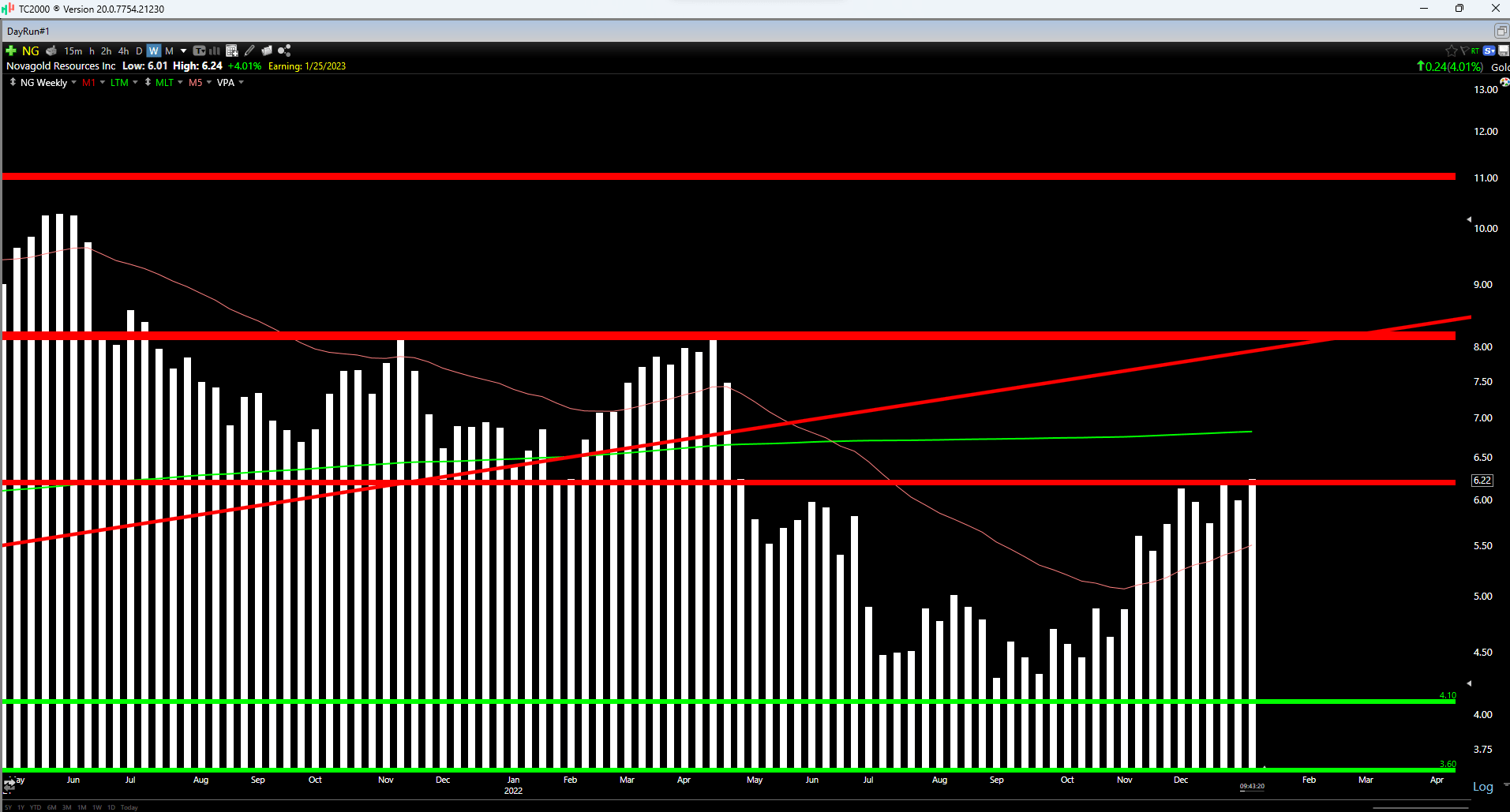

NG 18-Month Chart (TC2000.com)

Looking at NG from a technical standpoint, we can see that it's rallied sharply off its lows and is now butting its head against a short-term resistance level at $6.30, with no strong support until $4.10 per share. This doesn't mean that the stock can't head higher, but I typically prefer a 6 to 1 reward/risk ratio to justify buying gold developers, and with NovaGold trading right up against resistance, it trades at a worse than 0.10 to 1.0 reward/risk ratio. Hence, I do not see this as a low-risk buying opportunity, and I would view any rallies above US$6.60 (5% above resistance) before March as an opportunity to book some profits.

Summary

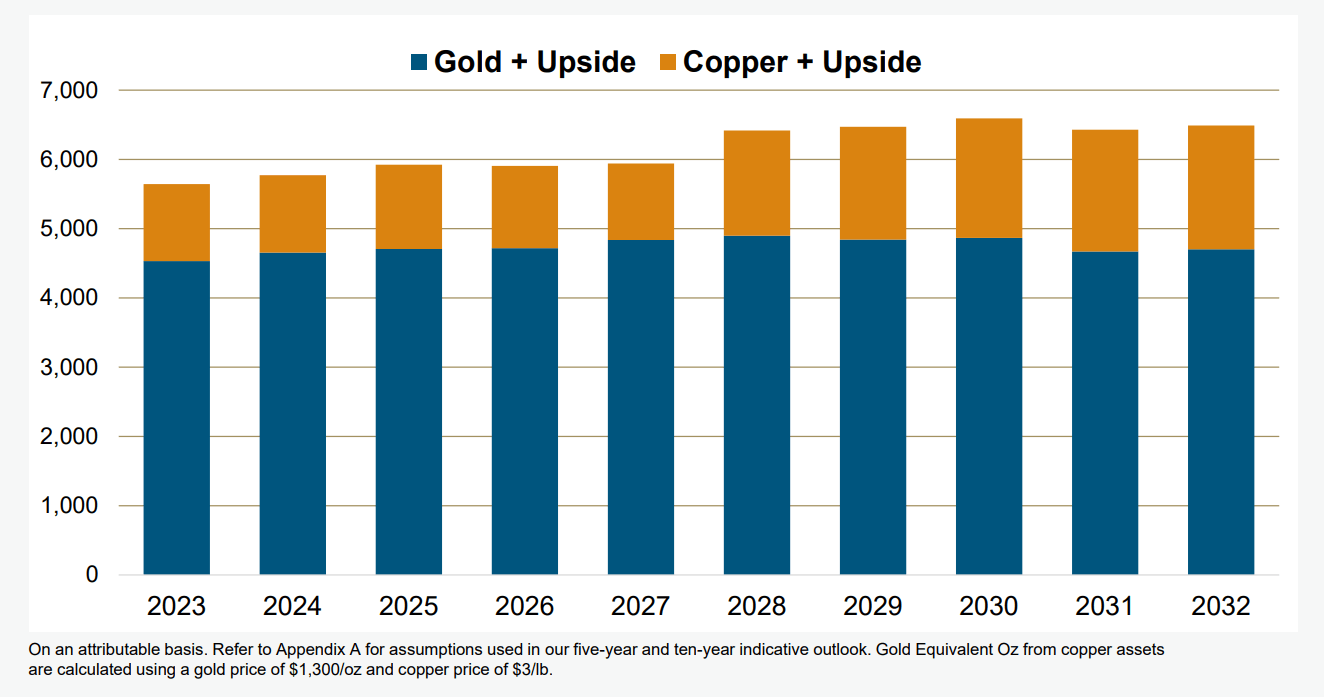

There's no disputing that NovaGold has a phenomenal asset in its portfolio, with a 50% ownership of a mine that would nearly match the total annual output from the Carlin Complex if it were in production today. However, it isn't easy to nail down when the project will be approved. Plus, with Barrick's portfolio looking the best it has in a decade with significant growth (Lumwana Super Pit, Reko Diq, Goldrush, Pueblo Viejo Expansion), one might argue that Barrick doesn't need to rush into anything from a growth standpoint. This means it could be more patient than previously forecasted and do additional optimization work at Donlin before deciding to go ahead with the project.

Barrick Gold - 10-Year Gold & Copper Profile (Company Presentation)

{kind=link}

For Barrick Gold, taking its time to green-light Donlin isn't an issue, given that the company is a cash flow machine at a $1,800/oz gold price, and it can sit on the project for years before making a final decision but still be a very profitable company with growth. However, in NovaGold's case, the company will likely need to raise capital by 2026 to continue funding Donlin, assuming a construction decision isn't made yet. Meanwhile, it will remain a developer until Barrick decides on the project, which could lead to it underperforming those companies like Barrick and Agnico ( AEM ) that are aggressively returning capital to shareholders and growing production.

Given that NovaGold does not control its own destiny like other developers with more modest capex requirements and the fact that there's no guarantee that this project heads into production this decade if metals prices don't improve, I see it as a trickier way to get exposure to the gold price. Instead, I see developers trading at less than 0.50x P/NAV (vs. NG at over 1.0x P/NAV) that can self-fund their operations as more attractive bets or diversified producers with strong growth profiles. To summarize, I remain focused elsewhere, and I would expect any rallies above $6.55 before March to offer an opportunity to book some profits.

For further details see:

NovaGold: Don't Chase The Stock Here