NG - NovaGold: Relative Valuation Remains Unattractive

2023-05-28 06:16:13 ET

Summary

- NovaGold is one of the worst-performing precious metals stocks this year, down 13% year-to-date vs. a 5% gain for the Gold Miners Index.

- I attribute this poor performance to the stock heading into the year being fully valued, plus weaker economics than pre-COVID-19 levels because of sticky inflationary pressures.

- And while the hope was that Donlin might get pushed forward quicker in a $2,000/oz gold price environment, I believe there are more attractive returns for Barrick elsewhere.

- So, while NG may be sharply off its highs, I continue to see it as an inferior way to play the sector, with Barrick and smaller cash-flow generating producers trading at more attractive valuations with simpler investment theses.

Just over four months ago, I wrote on NovaGold (NG), noting that there was zero justification for chasing the stock at US$6.30. This is because not only was the stock trading at a meaningful premium to estimated net asset value vs. other gold developers that had a clearer path to first production, but it also had an unfavorable reward/risk setup from a technical standpoint. Since then, NovaGold has underperformed the Gold Miners Index ( GDX ) by over 1500 basis points, contrary to comments from some that a higher gold price would propel NG higher and that it was a must-own name in January. Obviously, this hasn't come to fruition, and the stock has been a massive drag on portfolio returns for those unwilling to take profits in the stock.

This severe underperformance and drawdown in the stock highlights why it's important not to let emotions cloud investment decisions when an individual miner becomes fully valued. It also highlights why there's tremendous value from a return standpoint to owning the most undervalued names and being willing to step outside of the precious metals sector occasionally to generate new ideas such as CrowdStrike ( CRWD ) purchased at $95.10 in January vs. some approaches that advocate having 90% plus exposure to precious metals stocks at all times. In fact, and by default, the latter approach (90% exposure to precious metals at all times) means that one will have several lower-quality names in a portfolio to maintain this target exposure, or will be too heavily concentrated across just a few miners, with neither being ideal.

Portfolio Returns - August 5th 2020 to May 26th 2023 (Personal Portfolio Returns)

{kind=link}

As shown in the above chart, I have been able to outperform the Gold Miners Index by over 130% since the August 5th 2020 peak (100% return vs. a 33% decline for the GDX vs. its peak at $45.00) by not getting married to any individual miners and being extremely rigid regarding when I'm willing to be more aggressive. Plus, these excess returns have been achieved with much shallower drawdowns, meaning fewer grey hairs. And peace of mind is arguably more important than returns, since no return is worth sleepless nights and frustration. In this update, we'll dig into recent developments for NovaGold and while despite strong exploration results, it still does not meet my rigid investment criteria.

I have purposely highlighted returns vs. the worst possible comparison date, the peak over the past decade for the Gold Miners Index (August 5th, 2020) vs. only showing favorable periods such as multi-year lows for the GDX when it's much easier to generate positive returns.

Q1 Results & Recent Developments

NovaGold released its Q1 results in April, ending the quarter with $116 million in cash and $25 million set to be received early in its fiscal Q3 2023 period (July 2023) as part of deferred consideration for its Galore Creek sale in 2018. This has allowed NovaGold to maintain one of the stronger balance sheets within its peer group of developers, and this is certainly a unique attribute when financing terms from an equity standpoint are becoming less favorable and interest has dried up almost completely for some, plus cost of capital has rarely ever been higher for the sector. Meanwhile, and as I've highlighted extensively in past updates, the company has a 50% ownership in arguably one of the best undeveloped projects globally. However, these two attributes are not enough to justify an investment, even with some world-class drill results released in during Q1 sprinkled on top.

As discussed by the company in its Q1 results, Donlin Gold (50% Barrick ( GOLD ) /50% NovaGold) is working toward an updated Feasibility Study for the mammoth-sized Alaskan Project after the most aggressive drill program in 15 years. This includes trade-off studies which would help to improve project economics and work is also ongoing to advance the Alaska Dam Safety certifications for water diversion/water retention structures, with the major item being the proposed TSF, expected to be constructed in the Anaconda Creek Valley (3.5 kilometers south of the open pit). In addition, NovaGold has applied for a new air quality permit from the Alaska Department of Environmental Conservation [ADEC].

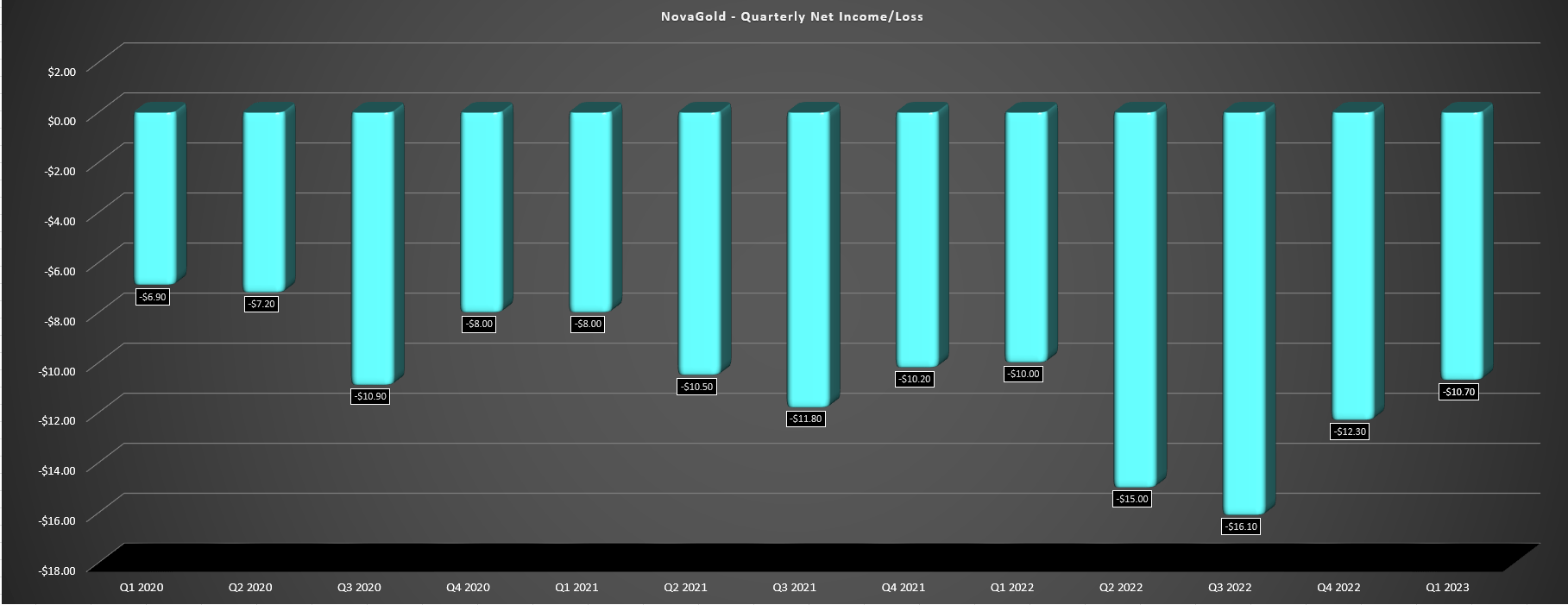

While the recent drill results shown above are certainly positive and the much-awaited updated Feasibility Study should help investors to discern whether this is a project that is likely to be green-lighted this decade, there are some negatives worth pointing out. For starters, NovaGold has been able to fund its share of expenditures at Donlin with limited growth in its share count over the past few years, helped by the sale of its stake in Galore Creek. However, its cash balance is likely to be sub $120 million heading into 2024, meaning that some share dilution or debt looks inevitable post-2025. Looking at the Q1 results, NovaGold reported a net loss of $10.7 million which isn't surprising given that it's not generating any revenue, with increased G&A expenses of $5.6 million (Q1 2022: $5.2 million) and increased permitting costs.

NovaGold - Quarterly Net Income/Loss (Company Filings, Author's Chart)

{kind=link}

Second, and more importantly, inflationary pressures have remained stickier than many expected and some producers are expecting mid single-digit inflation this year even after two years of material inflation, which could have a severe impact on Donlin Project economics unless trade-off studies can reveal significant improvements. For those unfamiliar, the Donlin Project was expected to cost over $7.4 billion to build on a 100% basis, placing its upfront capex at nearly 8x that of De Grey's Mallina Gold Project, which even under more conservative assumptions is likely to cost ~$1.0 billion. However, Mallina is expected to have a very attractive production profile with ~540,000 ounces in the first ten years at sub $925/oz AISC, roughly ~40% of the production profile but at a fraction of the upfront cost. So, while Donlin is bigger, Mallina wins by a mile from an After-Tax NPV (5%) to Initial Capex standpoint.

Let's take a look at Donlin's previous project assumptions below:

The Impact Of Inflationary Pressures

As discussed in past updates, we saw a double-digit increase in upfront capital expenditures for Donlin in its 2021 update, which was below my estimates and certainly well below the inflationary pressures experienced by other developers and producers on greenfields growth projects from pre-2018 to 2021. However, on close inspection, these cost estimates were based on Q1 2020 pricing, as highlighted below and in my previous article in more depth . And given that this did not capture the near unprecedented inflation experienced in 2021 through 2022, I would argue that these estimates are extremely stale. In fact, even if we use a 25% increase in costs which would appear to be below the average increase on upfront capex for greenfield projects (Q1 2020 to Q1 2023), upfront capex at Donlin would increase from $7.4 billion ~$9.2 billion, and that still doesn't capture the impact on operating costs and sustaining capital over the mine life.

{kind=link}

"The capital cost estimate is based on updated, first quarter 2020 pricing applied to the engineering designs and material take-offs from the 2011 feasibility study. The level of accuracy for the estimate is ±25% of estimated final costs, per Association for the Advancement of Cost Engineering [AACE] Class 3 definition. Except the following two design changes, no changes to engineering or material take offs (MTOs) were made:

• The operations WTP was changed from a High Density Sludge plant to a Reverse Osmosis ((RO)) plant.

• The natural gas pipeline was updated for an increase in pipe diameter from 12? to 14? (305 to 356 mm) and for modifications made to the route (i.e., the North Route Alignment) between mile post 85 and 112."

- NovaGold Technical Report on Donlin Gold Project

So, why is this an issue?

Aside from the fact that NovaGold will need to raise more than double its market cap ($4.0+ billion) to fund project construction if it wants to maintain its 50% ownership and if the scope of the project isn't changed , the average investor that is bullish on Donlin and NovaGold may not be factoring in how these costs could impact project economics. Some points worth thinking about include the potential level of share dilution needed to build this project even with a large debt component, and whether this project even meets Barrick's criteria if trade-off studies/optimization work can't push the after-tax IRR north of 15%. And, while some investors might believe NovaGold is undervalued on a per ounce basis, its valuation leaves a lot to be desired despite its recent correction on a P/NAV basis, with deterioration in the After-Tax NPV (5%) figure being highly likely after incorporating these expected inflationary pressures. Let's take a closer look below:

Valuation

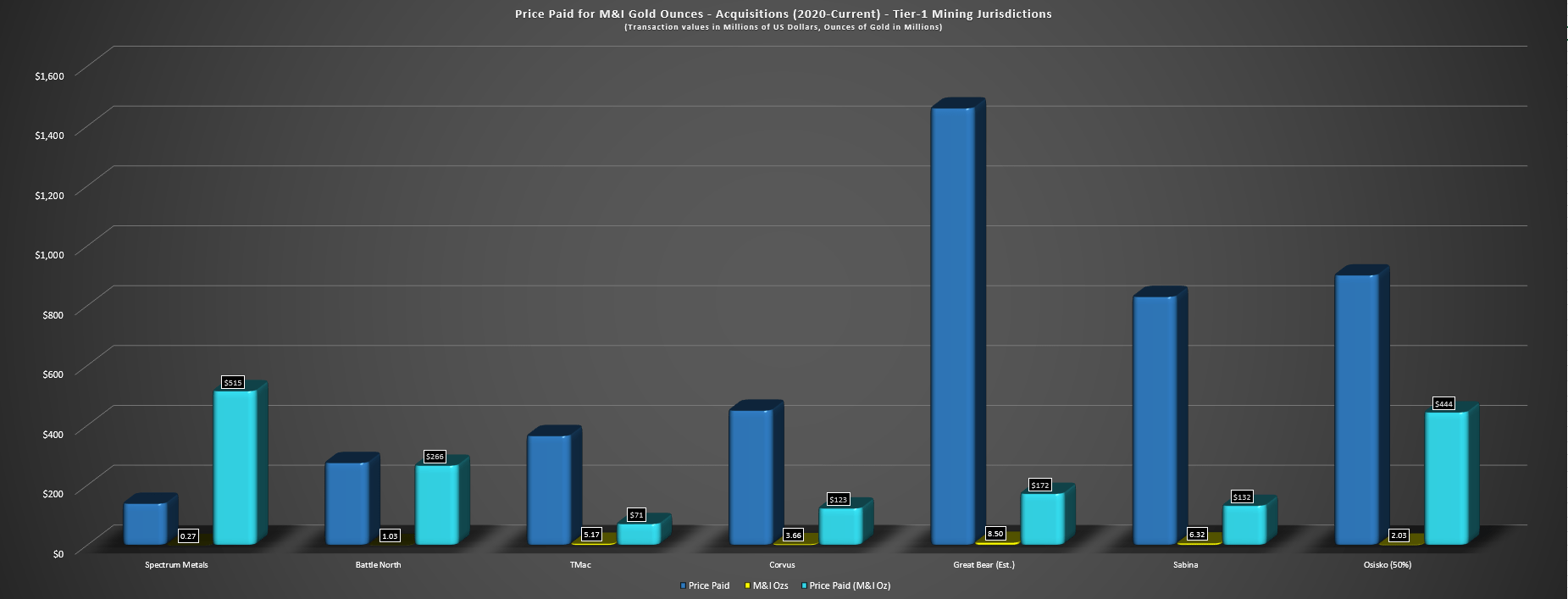

Based on ~346 million fully diluted shares and a share price of US$5.25, NovaGold trades at a market cap of ~$1.82 billion. At first glance, one might conclude that this is a dirt-cheap valuation for a stock that has an attributable reserve base of ~16.9 million ounces of gold at industry-leading open-pit grades, with NovaGold valued at just ~$108/oz on reserves or ~$93/oz on M&I resources. And if we look at what suitors have paid for other projects in Tier-1 jurisdictions (Canada, United States, Australia) over the past three years, this value per M&I ounce pales in comparison, despite Donlin dwarfing these companies in resource scale, and also boasting some of the most impressive open-pit grades of any large-scale undeveloped project in Tier-1 jurisdictions, even beating out De Grey's Mallina Project (1.80 grams per tonne of gold in first ten years).

Price Paid For M&I Gold Ounces - Acquisitions 2020 to Current in Tier-1 Mining Jurisdictions (Company Filings, Author's Chart & Estimates)

{kind=link}

That said, bigger is not always better, and there comes a point where size can be an impediment to putting it into production, especially in an inflationary environment. Unfortunately, for a project of this size in a remote area of Alaska with refractory ore, the capex bill will be massive, even when shared with the second-largest gold producer. And while the 2021 update gave some more realistic estimates regarding upfront construction costs ($7.4 billion vs. $6.7 billion), we've seen runaway inflation and many projects have seen 25% plus misses on costs even using mid-2021 cost estimates, let alone Q1 2020. Hence, with the combined impact of higher labor costs, higher fuel costs (TR assumed $0.69/liter diesel prices), higher consumables costs, and the impact of higher sustaining capital, it's likely we'll see significant cost creep in the updated study across upfront capex, sustaining capex, and operating costs.

It's important to note that this does not mean that this isn't an incredible project once in production, with cash costs likely to come in below $750/oz even when adjusting for inflationary pressures. Still, with an upfront capex bill that's likely north of $9.2 billion using constant assumptions to the previous Technical Report, putting a significant dent in the After-Tax NPV (5%), with a more conservative estimate using a $1,900/oz gold price being sub $4.8 billion vs. the ~$6.45 billion estimate using Q1 2020 pricing. If we divide by two to account for NovaGold's 50% attributable interest, this places a fair value on NovaGold's share of ~$2.2 billion, leaving NovaGold trading at 0.83x P/NAV. This multiple is steeper than some gold producers in the market today, and nearly double that of the average gold developer.

Plus, this doesn't even address the discount rate issue, with 5% being far too low in today's environment, and 8% being more appropriate for developers.

Even if one sticks with a 5% discount rate, which is the industry standard, and one uses a premium multiple of 0.90x P/NAV for NovaGold vs. the developer average at sub 0.50x using a $1,900/oz gold price assumption, this would place NovaGold's fair value at $1.98 billion or US$5.70 per share. And while this more conservative estimate of fair value points some upside from current levels, I am looking for a minimum 40% discount to fair value to justify buying small-cap names in the gold sector, and or gold developers. After we apply this required margin of safety to NovaGold, the stock would need to drop below US$3.50 to become attractive from a valuation standpoint. So, while some gold producers that control their own destiny offering much larger margins of safety, I don't see any way to justify owning NG here from an absolute or relative value standpoint.

Production Timeline & Project Approval

While some investors might argue that the fair value here is significantly higher than I've assumed after adjusting for the impact of inflationary pressures, the bigger question which is key to the NovaGold investment thesis and cash flow actually being realized is whether this project gets developed at all this decade. As I've argued in past updates, Barrick is looking for a 15% after-tax IRR to green-light projects at conservative gold price assumptions ($1,500/oz or lower), and I think the Donlin Project will struggle to maintain a 10% IRR at $1,900/oz gold when incorporating inflationary pressures. Hence, unless we see a dramatic improvement in project economics from trade-off studies, I don't have high confidence in Barrick green-lighting the project before 2028, which is required to push it forward.

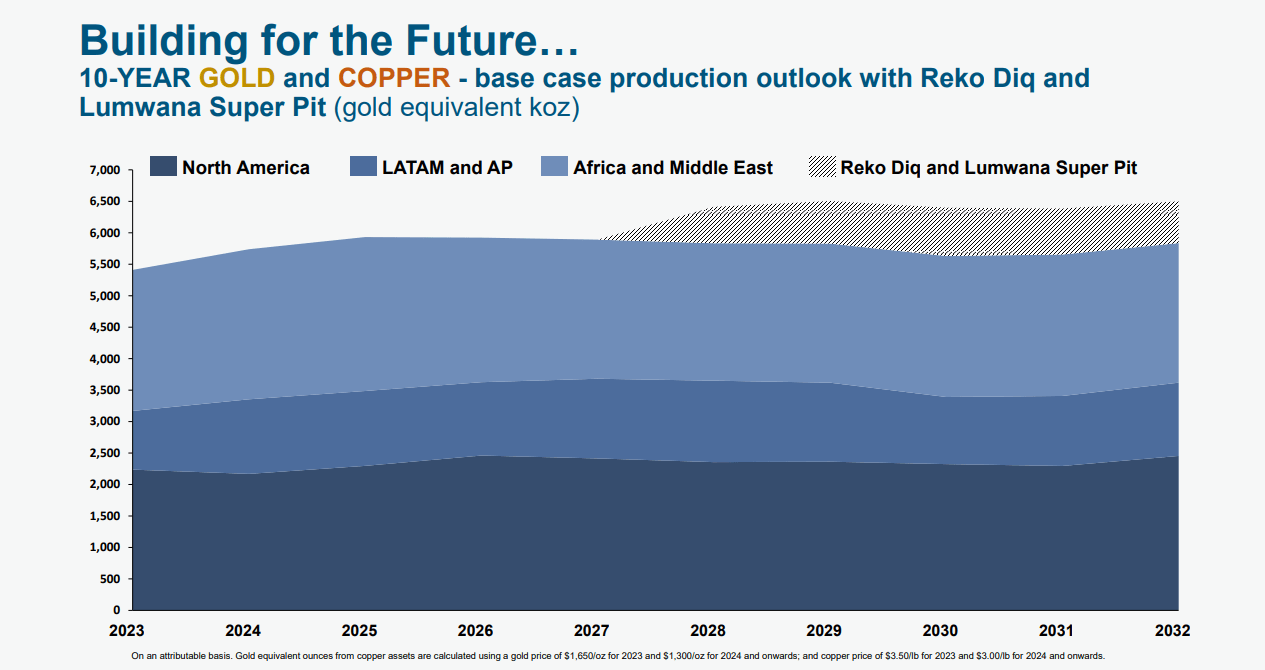

Barrick Gold - 10-Year Gold & Copper Production Outlook With Higher Priority Growth Projects (Barrick Gold Presentation)

{kind=link}

Second, Barrick appears quite intent on building Reko Diq, a massive copper-gold project in Balochistan, with a capex bill that's likely to come in near $4.5 billion (100% basis for Phase 1), and second in priority for mega projects appears to be the Lumwana Super Pit which will extend the mine life at the Zambian copper asset. And with what looks like it will be a lower return and $4.5+ billion capex bill for Barrick at Donlin (attributable basis), I can't see the company taking on three major projects at once, especially when it could supplement this growth with lower-capex and higher-return projects like Fourmile and Robertson vs. taking on a third major project simultaneously and increasing execution risk. So, with NovaGold remaining a longer-dated option behind two other mega projects with what's likely to be an inferior return, I would be amazed to see NovaGold generating any meaningful free cash flow before 2031, with a nearly decade wait ahead of them.

To put this in perspective, multiple developers have made meaningful progress over the past year through early works, construction, financing, and joint-ventures, meaning they are closer to generating free cash flow, are fully-financed or close to fully-financed, and investors have visibility into first gold pour in 2025/2026. One example is Marathon Gold ( MGDPF ), which trades at a 30%+ FY2026 free cash flow yield and less than 0.70x P/NAV even using an 8% discount rate vs. the 5% discount rate I've used to assume NovaGold's fair value in order to be generous. So, with this being just one example among many of more de-risked developers trading at more attractive relative valuations, NG remains unattractive from an investment standpoint, and especially on a relative basis as other developers inch closer to the finish line (first gold pour).

Summary

The NovaGold investment thesis is arguably intoxicating given that investors have the opportunity to get exposure to half of one of the world's best undeveloped gold assets in a safe jurisdiction. However, investors can get this same exposure by owning a company like Barrick that is already generating free cash flow from a diversified portfolio, regularly returning capital to shareholders through opportunistic buybacks, and paying an attractive dividend yield today. Plus, after its recent sell-off, Barrick trades at a similar P/NAV multiple to NovaGold (~0.85x vs. ~0.80x) with little value assigned to Donlin, suggesting investors are getting a producer today with exposure to Donlin for free, while being paid to wait.

To summarize, I continue to see NovaGold as an inferior way to get exposure to Donlin at best, and a gamble at worst with no clear margin of safety. Hence, it continues to be a pass at current levels, with far more attractive ways to put capital to work elsewhere in the sector.

For further details see:

NovaGold: Relative Valuation Remains Unattractive