NG - NovaGold Resources Stock: Valuation Starting To Improve

2023-12-20 10:14:25 ET

Summary

- NovaGold Resources Inc. stock has suffered a 40% drawdown in the past six months, underperforming its peers and the gold price.

- The company finished the quarter with ~$130 million in cash after receipt of a deferred payment, with continued progress permitting/optimizing the Donlin project.

- Unfortunately, high upfront costs pose challenges for green-lighting the project, and even current gold prices leave the IRR on an inflation-adjusted basis for costs below Barrick's hurdle rate.

- In this update, we'll look at recent developments, the stock's updated valuation, and how it looks from a relative value standpoint following its decline to US$3.60.

Just over six months ago, I wrote on NovaGold Resources Inc. (NG), noting that the stock's relative valuation remained unattractive with it trading at a premium to developers (and even some producers) that controlled their own destiny, were takeover targets, and many that were already in construction/production. Since then, NovaGold has suffered a nearly 40% drawdown, massively underperforming its peer group and the gold price which has hit new all-time highs in the same period. In this update we'll look at recent developments, the stock's updated valuation, and how it looks from a relative value standpoint following its decline to US$3.60.

{kind=link}

Q3 Results

NovaGold released its Q3 results in October, reporting a net loss of $11.1 million on the back of $5.2 million in G&A spend and field expenses at Donlin and higher interest expense on its promissory note, offset by increased interest income in the period. The lower net loss was year-over-year (Q3 2022: $16.1 million) was related to lower expenditures at Donlin after a busy 2022 drill season to confirm the size and continuity of the pits (ACMA and Lewis), and increase overall confidence. These results exceeded my expectations, with highlight intercepts of 42.2 meters at 30.7 grams per tonne of gold, 49 meters of 20.6 grams per tonne of gold, and an even thicker intercept at Divide of 61 meters at 12.4 grams per tonne of gold.

NovaGold - Quarterly Net Losses - Company Filings, Author's Chart

{kind=link}

Meanwhile, the company has been working on finalizing resource models and geotechnical drilling to complete Alaska Dam Safety certification applications, as well as hydrogeologic drilling and pump tests for mine planning and design. Donlin also noted that work on metallurgy could improve recoveries "a couple of percent," and even a 170 basis point improvement in overall recoveries would be quite significant and translate to an extra ~22,000 ounces per annum assuming a ~53,500 tonne per day processing rate at ~2.1 grams per tonne of gold.

The other positive news was NovaGold sharing that all appeals against the project have been unsuccessful to date, and it continues to make solid progress from a permitting standpoint with the State Air Quality permit re-issued, the Alaska Pollutant Discharge Elimination System permit extended and expected to be re-issued in 2024, and several other major permits in place.

"Despite multiple challenges, all appeals against Donlin Gold permits have been unsuccessful to date, underscoring our ongoing confidence in the process. We recognize the importance of preparedness and organization in these matters. With the unwavering support of Donlin Gold and its Owners, we will continue to back the agencies in defending their thorough and diligent permitting process."

- NovaGold, Q3 2023 Results .

{kind=link}

Finally, despite ~$20 million in cash burn to date, the company's cash position has increased with the final deferred payment related to Galore Creek of $25 million. This has left Donlin with just over $130 million in cash and cash equivalents, which should allow it to continue progressing Donlin with its partner Barrick Gold Corporation (GOLD) with no required equity raises until 2027, assuming a $35 million annual burn rate. The fact that NovaGold has advanced the project without share dilution is certainly a differentiator and very fortunate given the horrid share price performance of developers sector-wide, with this leading to significant share dilution with equity raises at multi-year lows by many companies.

Inflation & Scarcity

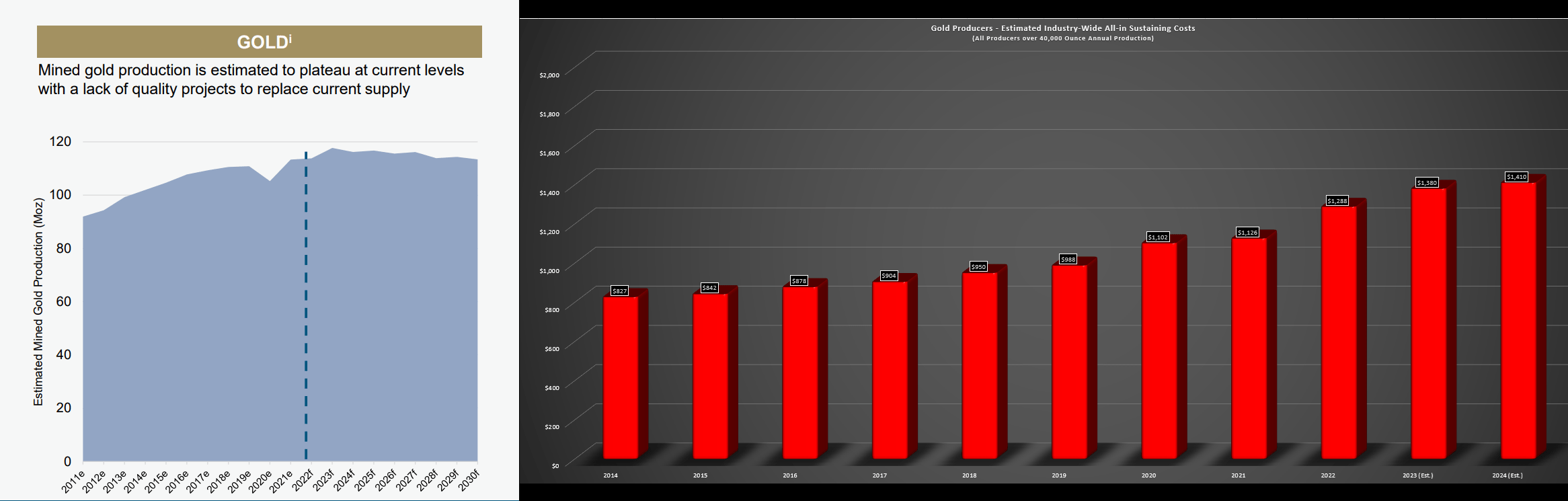

Unfortunately, while NovaGold remains cashed up and progress on site has been positive, inflation has not let up, remaining above historical levels and on track for another year of inflation after near unprecedented inflation in 2021 and 2022 sector-wide. In fact, many gold producers have seen even higher operating costs this year due to labor/consumables inflation, and this is despite the pullback in energy prices which has been a minor tailwind in the period. As I've noted in past updates, this significant inflation is not positive news for the Donlin Project owned by NovaGold (50%), as the project already had a ~$7.4 billion upfront capex bill based on Q1 2020 pricing which was calculated before we saw runaway inflation.

"The capital cost estimate is based on updated, first quarter 2020 pricing applied to the engineering designs and material take-offs from the 2011 feasibility study. The level of accuracy for the estimate is ±25% of estimated final costs, per Association for the Advancement of Cost Engineering [AACE] Class 3 definition. Except the following two design changes, no changes to engineering or material take offs (MTOs) were made. The 2020 sustaining capital estimate was updated for 2020 pricing. No changes to the mine plan or Project engineering were made.

- Donlin Gold 2021 TR (emphasis added).

{kind=link}

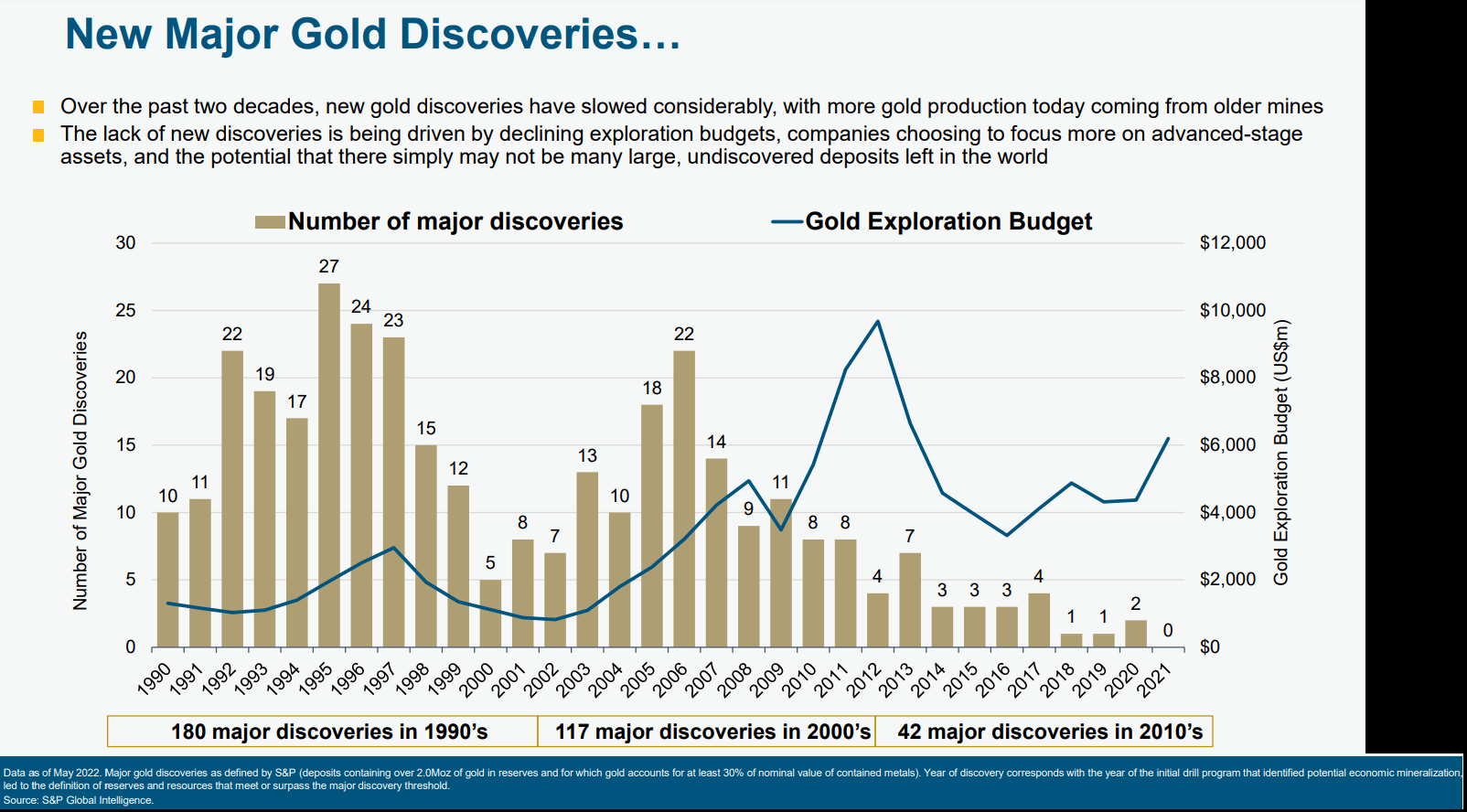

On a positive note, it isn't getting any easier to make discoveries, and even having one of the best assets is not enough if you're First Quantum ( FQVLF ) in Panama, which has been ordered to halt production at the massive 100 million tonne per annum copper mine (Cobre Panama). In addition, operating costs sector-wide continue to increase with inflationary pressures and declining reserve grades, making a ~40 million ounce resource at double the average open-pit a very attractive asset, especially given that it sits in one of the better jurisdictions sector-wide, Alaska.

To summarize, an asset like Donlin has never been more attractive, with its grade and scale allowing for above-average margins, its jurisdiction being lower risk, and its size being nearly unrivaled in a sector where we've seen a dearth of major new gold discoveries over the past few years relative to the previous few decades.

Gold Production Plateau, Estimated Industry-Wide AISC - Barrick Presentation, Company Filings, Author's Chart New Major Gold Discoveries - Barrick Gold, S&P Global Intelligence

{kind=link}

{kind=link}

Recent Developments

Barrick Gold had favorable comments related to Donlin in the company's Q3 2023 Conference Call, noting that "a 32 to 36 million ounce resource" is important in its portfolio when asked if it would consider selling the asset. The company also reaffirmed what NovaGold shared, which was that it's looking at a:

" detailed first principles update of capital and operating costs, along with an ongoing review of power generation and alternative fuel source options, transmission, and logistics strategies,"

which might help to pull down the massive $7.4 billion upfront capex bill. And

"The next one is, one of the big things that have changed, in the last, a few years is the cost profile and the capital cost, particularly, so we need to refresh all the capital estimates for that design. So once we get a real handle on that and when it is not far away, we will be able to do that. And then the important other aspect is because power cost, power generation, power strategy has all changed. Then you start getting to the stage where you can actually understand at what gold price this project will be viable, as an investment. And for us, we are a very focused, gold mining company that has an obsession about sustainability. And a big 32 million to 36 million ounce resource is important in our portfolio."

- Barrick Gold CEO, Mark Bristow, Q3 2023 Conference Call .

Donlin Gold is shown below on a 100% basis, with well above-average open-pit grades, and a massive resource base of 600+ million tonnes.

High-Grade Gold Assets Owned by Barrick & Others (Grade/Tonnes) - Company Filings, Barrick Presentation, Author's Edits

{kind=link}

So, why has Barrick not rushed to build an asset of this caliber and scale with the gold price hovering above $2,000/oz?

While Donlin is an incredible asset, it's quite costly to build, and even keeping upfront costs under $9.0 billion would be an impressive feat given the 50% plus inflation for most greenfields project since 2020, and that Donlin's upfront capital was estimated at ~$7.4 billion based on 2020 pricing. In addition, we have seen significant labor/consumables inflation that has contributed to higher mining/milling costs and sustaining capital estimates, suggesting that total capex for Donlin Gold could come closer to ~$11 billion vs. ~$9.0 billion previously even with trade-off studies. And even if we assume a 100 basis point improvement in LOM recoveries, a $2,000/oz gold price offset by factoring in more conservative operating/upfront cost estimates, Donlin's NPV (6%) comes in closer to ~$4.3 billion or a ~12% internal rate of return [IRR].

{kind=link}

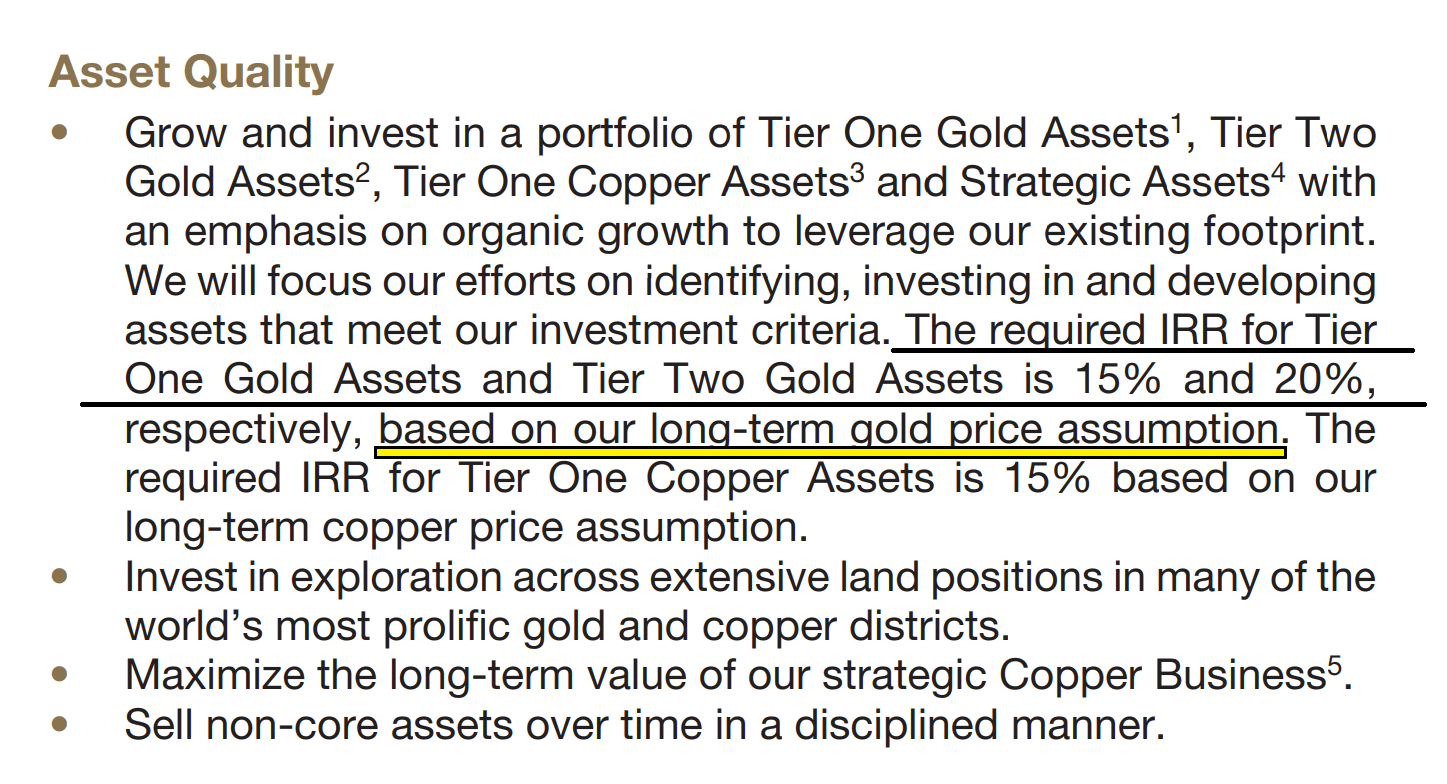

Some investors might argue that this is a reasonable return, and for an asset that could transform the operator's production profile and significantly increase its weighted average mine life while increasing Tier-1 jurisdiction gold exposure, it's not a poor investment choice by any means if one has a bullish long-term outlook on the gold price and assumes that $1,900/oz gold is the new floor. However, Barrick has stated the following in its 2022 Annual Report, with the major take-away being that it is looking for a minimum 15% IRR on Tier-1 scale gold projects. And while Donlin is just below this level, it's important to note that must be available using pricing in line with Barrick's long-term gold price assumption .

Currently, Barrick is calculating mineral reserves at $1,300/oz and its long-term gold price assumption is closer to $1,550/oz, if we use assume Barrick moves to $1,750/oz on its long-term gold price assumption by 2027, Donlin's IRR when factoring in more conservative cost assumptions slides below 9%, over 600 basis points below the minimum IRR requirement, and using prices above Barrick's current long-term gold price assumption ($1,550/oz). And while it might be possible to keep upfront capex under $9.0 billion with the benefit of trade-off studies using 2024 pricing, I have already used this assumption in calculating a more current NPV (6%) estimate and it still doesn't meet the required hurdle rate at a $2,000/oz gold price (~12% vs. 15%).

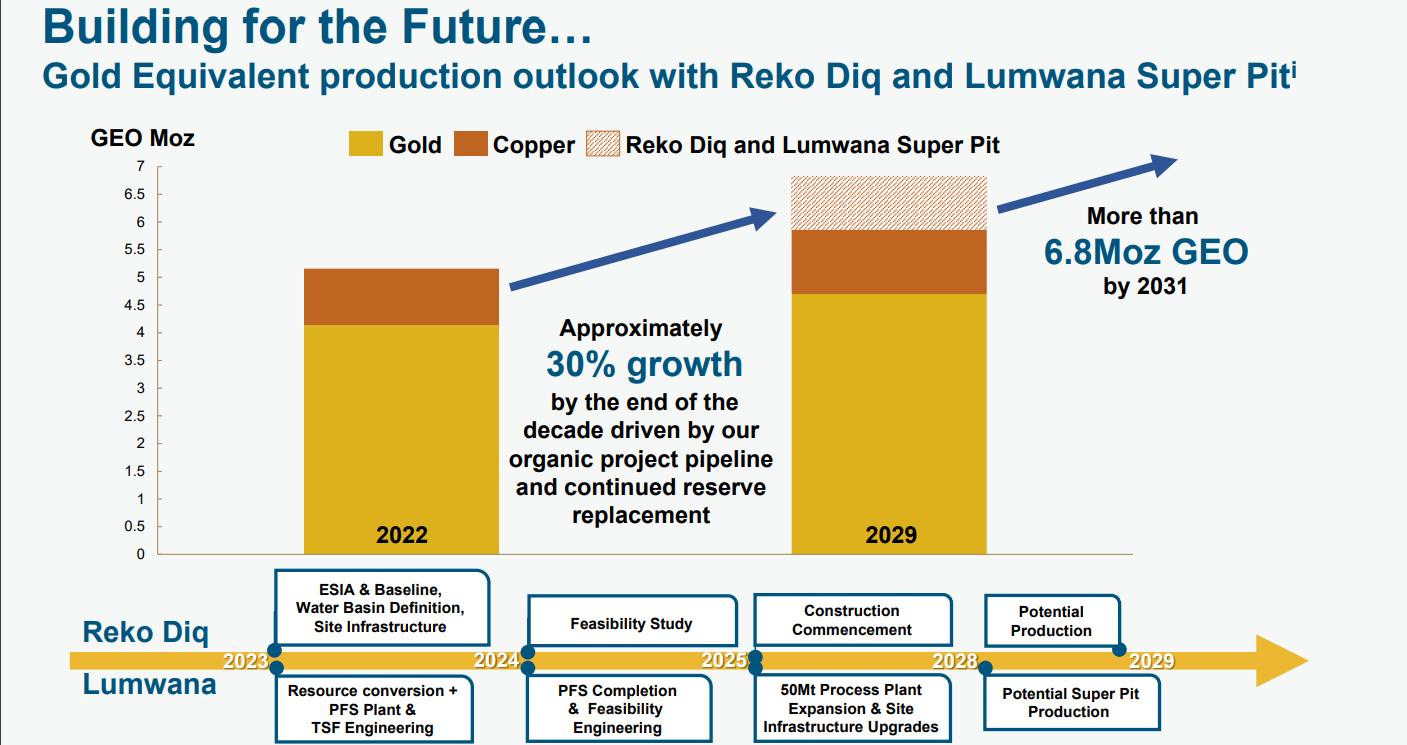

The last point worth noting is that Barrick already has two massive and higher return projects in the wings (Lumwana Super Pit & Reko Diq), and it has been clear that it's interested in growing its copper segment. So, with two high capex projects already in the planning phase (2024 Feasibility Studies, with $6.0+ billion in combined capex), it would surprise me to see Barrick try to tackle another monster asset before 2029 (on top of Lumwana Super Pit and Reko Diq). This is especially true when the company has another very high-margin gold opportunity in Nevada (300,000+ ounces at sub $800/oz AISC from Fourmile with ~$1.0 billion in construction capital) that it could slot in here if it wanted to grow incremental gold production, and/or the Conceptual Porgera PEA which could increase gold production (100% basis) to 750,000 ounces at the high end for less than $1.0 billion.

{kind=link}

Hence, while the lack of new discoveries and declining grades combined with higher jurisdictional risk outside of Tier-1 ranked jurisdictions certainly points to this asset getting built, I would be very surprised to see Donlin construction start before 2029, suggesting that NovaGold investors will wait nearly a decade to see any cash flow while other producers are returning significant capital to shareholders through dividends and buybacks. And in a less positive case scenario where gold prices remain in the $1,800/oz to $2,100/oz range and the project cannot meet the required hurdle rate, the project may not be pursued this decade at all.

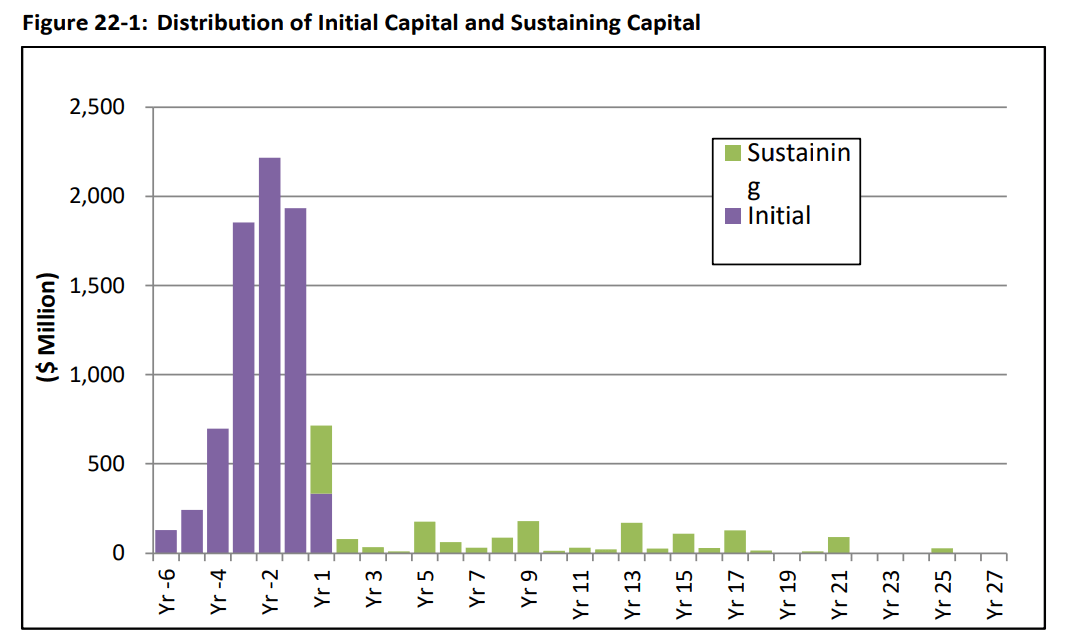

Donlin Project - Initial & Sustaining Capex (Q1 2020 Pricing) - 2021 TR

{kind=link}

Obviously, I could be wrong and the tradeoff studies may cut down capex more than I've assumed, but a double-refractory ore body (autoclave processing) in a remote location in a country with high labor rates with a ~54,000 tonne per day throughput rate is about as expensive as it gets, making it hard to be optimistic about initial capex coming in below $9.0 billion when factoring in near unprecedented inflation rates. Let's look at the valuation to see whether NovaGold has a margin of safety to account for the negative impact of inflation and whether there look to be better bets elsewhere in the sector from a relative value standpoint.

{kind=link}

{kind=link}

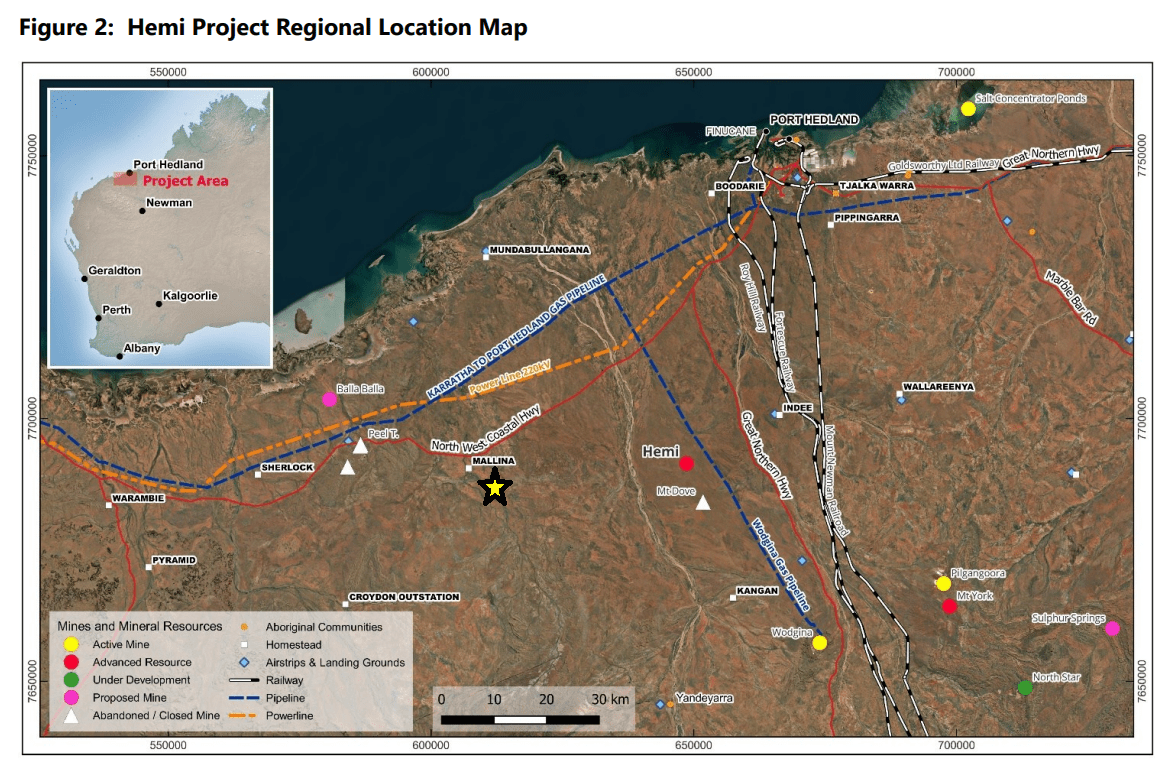

To put Donlin Gold's upfront costs in perspective, the Hemi Gold Project in Australia owned by De Grey Mining (DGMLF) is likely to cost over $1.1 billion to build and does not require a ~45 kilometer access road, and a 14-inch and 500+ kilometer natural gas pipeline (~$2.1 billion cost on inflation-adjusted basis).

Valuation

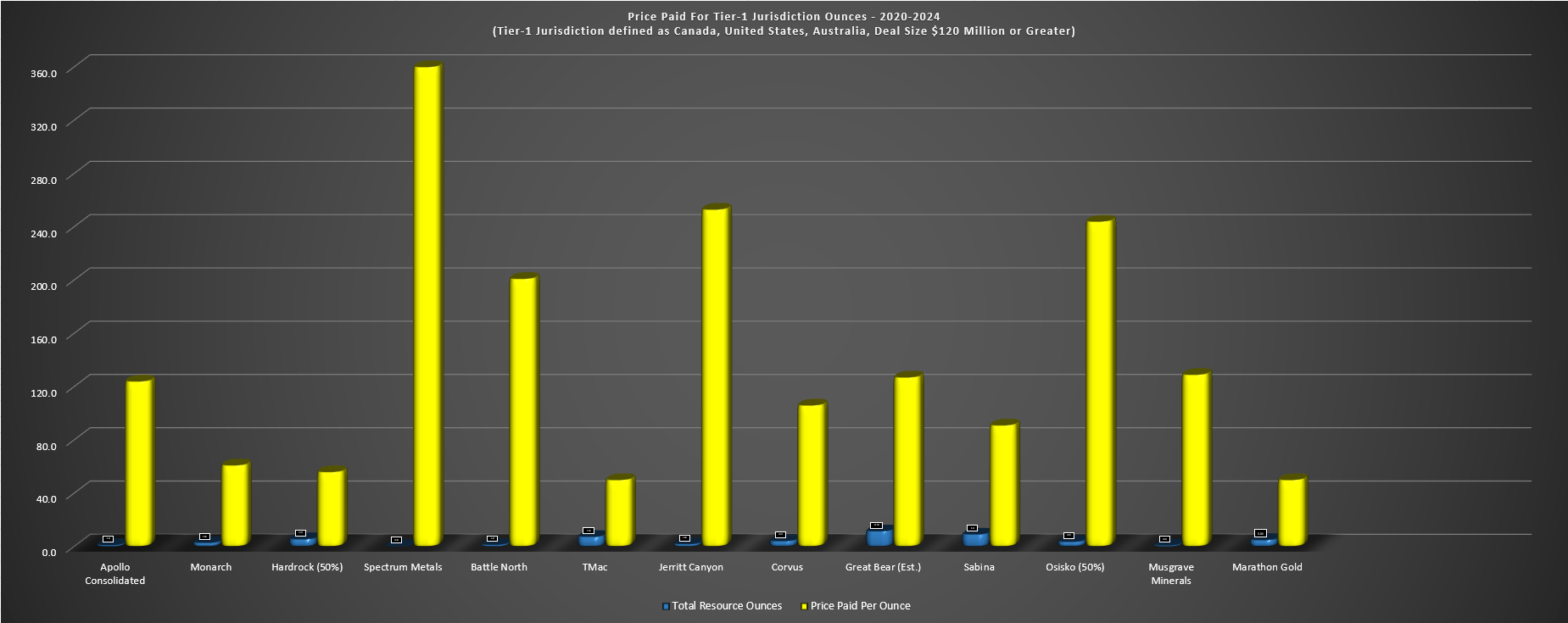

Based on ~336 million shares outstanding and a share price of US$3.65, NovaGold trades at a market cap of ~$1.23 billion. And while this is certainly a very reasonable figure for a developer with an M&I inventory of ~19.5 million attributable gold ounces, leaving it trading at just ~$63/oz. This is well below the median price paid for resource ounces of ~$100/oz for Tier-1 jurisdiction developers from 2020 to 2024. That said, all the developers acquired have had flagship projects that have averaged less than ~$500 million upfront capex and many projects were already in construction at the time of acquisition (Goose, Marathon). In addition, most of these projects will go into production before 2030 (Great Bear, Goose, Marathon, North Bullfrog, Railroad South, Windfall, Cue, Hope Bay), so it's no surprise that the suitors were willing to pay up to and above $200/oz given that cash flow was only a few years away in most cases.

Price Paid For Tier-1 Jurisdiction Ounces (2020-2024) - Company Filings, Author's Chart

{kind=link}

Given that NovaGold is clearly a large outlier with ~20x the average capex bill of these acquired projects and up to a decade before it heads into production, I think the best way to value the company is on a P/NPV basis. And if we use a long-term gold price assumption of $1,950/oz and an estimated NPV (6%) of ~$3.8 billion and adjust for NovaGold's 50% ownership, NovaGold's attributable NPV (6%) comes in at ~$1.90 billion. This leaves NovaGold trading at ~0.65x P/NPV, which is still above most of its developer peers, and even those peers that are less than two years away from commercial production. Hence, I would argue that NovaGold still doesn't offer a large enough margin of safety, especially given that there's still low visibility into a positive construction decision on the asset (never mind that its partner's own stated requirements can't yet justify green-lighting the asset based on current gold prices).

P/NAV Multiples Americas Developers/Producers - FactSet, Company Filings, G Mining Ventures Presentation

{kind=link}

So, what's a fair value for the stock?

Using what I believe to be a generous multiple of 1.0x P/NPV, an estimated 338 million shares (year-end 2024), and an attributable NPV (6%) of ~$1.9 billion, I see a fair value for NovaGold of US$5.60. However, I am looking for a minimum 50% discount to fair value for developers to ensure an adequate margin of safety, and applying that discount to my updated fair value results in an ideal buy zone for NovaGold of US$2.80 or lower. Hence, although NovaGold massively underperformed the sector and could see a bounce after a waterfall decline, I still don't see any case for an investment at current levels, and especially not from a relative value standpoint when compared to high-margin producers like K92 Mining (KNTNF) trading at lower P/NAV multiples when accounting for their recent resource growth.

In fact, in the period that investors are waiting for Donlin Gold to finally come online, which might be 2031 in a best-case scenario, K92 Mining will generate over ~$2.1 billion in free cash flow from its upcoming Stage 3/Stage 4 Expansions, which is more than double its current enterprise value of ~$1.0 billion, and it assumes no upside in the gold price with an assumed gold-equivalent price of $1,950/oz. Hence, the capital returns coming from K92 Mining should be enormous if it can execute successfully, and there's no risk of capex blowouts (low capex growth), there's no waiting for a partner to green-light the project, and there's no waiting for higher gold prices to justify the upfront investment (K92 Mining's estimated LOM AISC is below $800/oz).

So, what if you absolutely must have exposure to Donlin Gold as you believe it's the best project globally?

Assuming an investor can't part with their thesis on Donlin being the best asset globally (I would disagree when factoring in upfront capex/IRR), the best way to get exposure to this asset is through Barrick Gold, which also owns 50% of the asset, is generating significant free cash flow, and is paying investors to wait for the eventual development of Donlin. Plus, assuming Donlin isn't built in the next decade, investors still have a rock-solid investment thesis in Barrick by owning a top-3 gold producer with growing production, impressive diversification (12+ assets), and multiple Tier-1 scale mines, all in addition to an all-star CEO that has proven he is disciplined with capital allocation, with a side of optionality with 50% exposure to Donlin.

Summary

NovaGold has had a quieter year with the bulk of drilling completed in 2022, but work has continued to look at optimizing the Donlin Project to make it work for its owners. Unfortunately, sector-wide inflation hasn't cooled much, with Gold Fields ( GFI ) guiding for single-digit inflation yet again, and this suggests that even with trade-off studies, Donlin is still likely to be a very expensive asset to build. Meanwhile, even with the recent rise in the gold price, Donlin still doesn't look like it will work under Barrick's framework when adjusting for inflationary pressures, with a ~12% IRR even at a $2,000/oz gold price.

In summary, I continue to see far better bets elsewhere in the sector, and I see NovaGold Resources Inc. as an inferior way to bet on higher gold prices. That said, this doesn't mean that the stock can't put together a sharp rally and it could be a swing-trading candidate. Still, I don't see enough margin of safety for an investment yet, especially relative to cheaper and cash-flowing miners that control their own destiny.

For further details see:

NovaGold Resources Stock: Valuation Starting To Improve