NVSEF - Novartis: Limited Upside Despite Strong First Quarter Results Improved Guidance

2023-04-25 08:40:12 ET

Summary

- Novartis reported strong Q1 2023 results, beating the analyst EPS and revenue consensus.

- Both innovative products and the Sandoz business unit performed well.

- Novartis increased the full-year revenue and earnings guidance after the strong performance in the first quarter.

- The existing innovative product portfolio and pipeline are likely sufficient to fill the patent cliff gap in the following years. Still, the company must do more deals to deliver higher growth.

- Novartis stock looks fairly valued at current levels with modest upside potential in the near/medium term.

Novartis Q1 Results

Novartis ( NVS ) had a strong start to the year and it handily beat first-quarter revenue and EPS estimates. The company also raised the full-year revenue and earnings guidance due to the strong performance in the first quarter and it now expects total revenues to grow in the mid-single digits, up from low to mid-single digits, and core operating earnings to grow in the high-single digits, up from the mid-single digits.

The generic and biosimilar business unit Sandoz also performed well in the first quarter with total revenues growing 8% over the same quarter of last year. Novartis said that the planned spin-off of Sandoz is on track to complete in the second half of 2022. This would make Novartis a pure-play innovative biopharma company with a more attractive and sustainable business model and higher margins.

The innovative products performed well.

Entresto grew 32% Y/Y to $1.4 billion and growth was coming from both U.S. and ex-U.S. markets with the company noting strong momentum in Japan and especially in China after the recent reimbursement win as a first-line treatment option for hypertension.

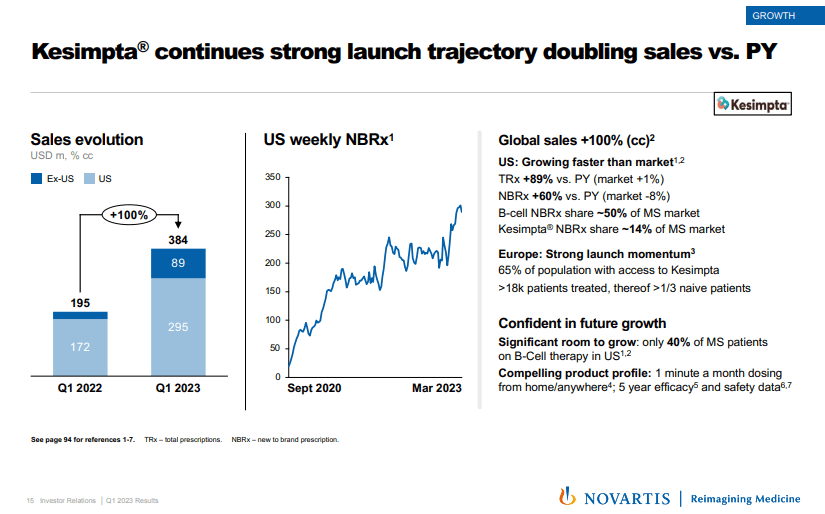

Kesimpta's net sales more than doubled to $384 million, but its momentum has slowed as sales were $369 million in the fourth quarter. This was by far the lowest sequential percentage increase in net sales since launch. However, looking at the new-to-brand prescriptions, there should be no reason for concern. There was a period of flat new-to-brand prescriptions which are a leading indicator of future growth, but growth has picked up considerably toward the end of the first quarter, and new-to-brand market share has reached 50% of the B-cell therapy market and 14% of the overall multiple sclerosis market.

{kind=link}

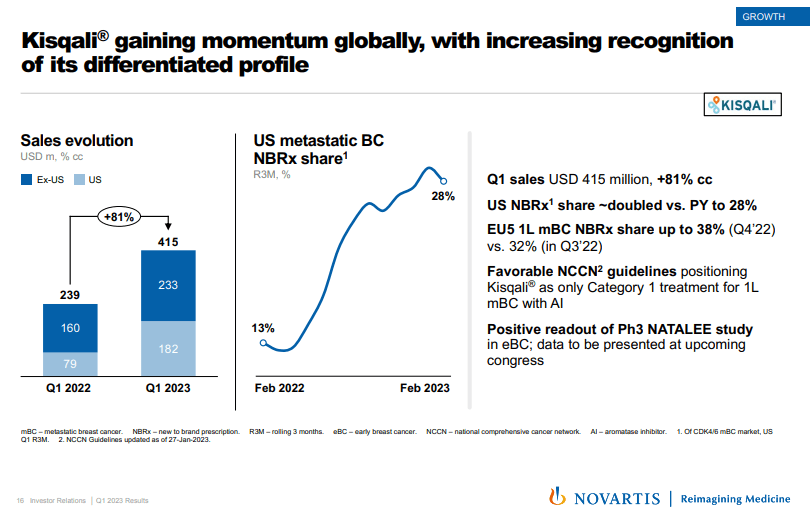

Kisqali was another strong performer with net sales growing 81% Y/Y to $415 million. The product's new-to-brand market share in the metastatic breast cancer market has more than doubled, from 13% in Q1 2022 to 28% in Q1 2023. The future is also very bright for Kisqali after the recent clinical trial win - it was successful in the NATALEE phase 3 trial in early breast cancer. The data will be presented at an upcoming medical congress but the success should considerably expand the addressable market for Kisqali and add several billion to its peak sales potential.

{kind=link}

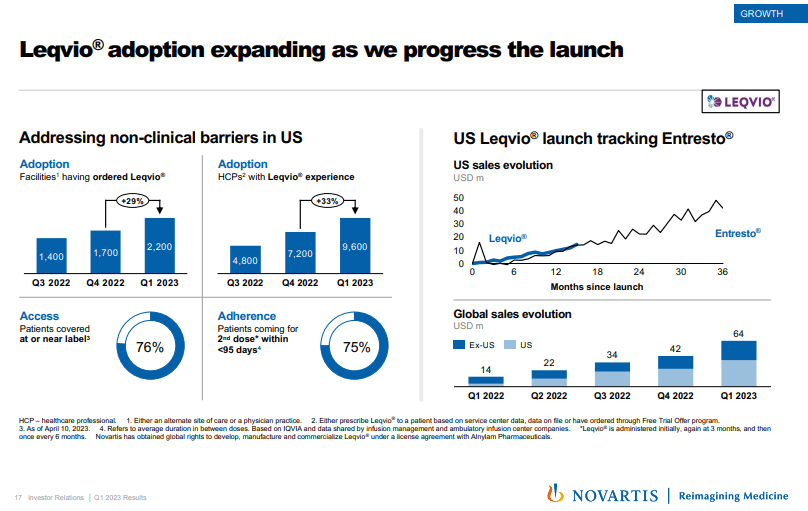

After a very slow start, the adoption of the cholesterol-lowering drug Leqvio is increasing. Net sales grew more than 50% sequentially to $64 million and the company notes that the sales evolution in the United States is very similar to that of Entresto which is on track to deliver more than $6 billion in global net sales this year. Access has improved considerably and 75% of patients are coming for the second dose within 95 days (the second dose is given three months after the first, after which Leqvio is administered once every six months).

{kind=link}

Pluvicto is off to a strong start. Net sales in the last four quarters were $10 million, $80 million, $179 million, and $211 million, respectively. However, the company says Q2 net sales will be at roughly similar levels to Q1 levels due to manufacturing constraints, but Novartis is working hard to expand the manufacturing capacity and with new lines coming online, Pluvicto should continue to grow in the second half of the year and continue its path to becoming a $2 billion+ a year product.

And last but not least of the innovative products, Scemblix continues its decent growth trajectory after the late 2021 launch. Global sales grew nearly 50% sequentially to $76 million. This is another product with peak annual sales potential in excess of $2 billion.

Pipeline maturation and business development are essential and needed to offset the patent cliff

There is still a long growth runway for products like Leqvio, Kisqali, and Kesimpta, Scemblix, and Pluvicto. However, with an estimated loss of $9 billion in annual net sales in the following years to patent expirations, primarily driven by the expected launch of generic Entresto in 2025, Novartis needs to work hard to make up for these losses and to continue to deliver sales and earnings growth in the following years.

I wrote about iptacopan in late 2022 and believe it is one of the most valuable assets in Novartis' pipeline. As covered, I see iptacopan as a $4 billion+ product at peak for Novartis in late-stage indications such as PNH, C3G, and IgAN, and sales could exceed $10 billion in a blue-sky scenario - if it is successful in two or more higher-value but earlier-stage indications.

The collaboration with BeiGene ( BGNE ) may prove very valuable in the long run but carries higher risk. Novartis is in charge of commercialization in major ex-China markets of BeiGene's tislelizumab, a PD-1 antibody, and the two companies expect to receive the first FDA approval for tislelizumab this quarter, pending an inspection of BeiGene's manufacturing facilities in China. And although BeiGene is doing extremely well in China where tislelizumab is now the market-leading PD-1 product, Novartis will have a hard time competing with established PD-1 drugs like Keytruda and Opdivo and the two companies will have to rely on combination approaches with innovative medicines.

One of those could be BeiGene's ociperlimab, a potent TIGIT inhibitor that is supposed to enhance the efficacy of tislelizumab, although this now seems more of a long shot after a series of disappointments the TIGIT class has delivered over the last few quarters. If ociperlimab in combination with tislelizumab is shown to work well, the two products could add more than a few billion in annual net sales by the end of the decade. However, due to the mentioned uncertainty over ociperlimab's potential, Novartis has not fully bought into ociperlimab and only holds an option it can exercise by the end of 2023. I am not sure how much ociperlimab data we will see this year, but Novartis' decision on the option should show whether the company believes in the project and should offer a strong clue of what the data to date look like.

And while the sales of Cosentyx slightly declined in the first quarter, it could get a new life this year if it receives approval for the treatment of hidradenitis suppurativa. This indication could add $2 billion or more to Cosentyx's annual sales by the end of the decade.

The last pipeline asset I will mention today is pelacarsen, an antisense oligonucleotide designed to reduce the levels of lipoprotein A, or LPa. This is a very promising cardiovascular target with genetic data showing high levels result in increased cardiovascular risk. Pelacarsen was in-licensed from Ionis Pharmaceuticals ( IONS ) and the topline results from the cardiovascular outcomes trial are expected in 2025. This market will take time to build, but if there is a strong treatment effect, I would expect the LPa class to become a $10 billion+ market by the mid-2030s and Novartis will have a significant first-mover advantage.

With all that in mind, the current internal pipeline is probably insufficient for Novartis to deliver topline growth that is better than the low-to-mid single digits and the company will have to put a heavier focus on business development in the following years. The spinoff of Sandoz will help and so will the cash generated in the following quarters and years. The company was focused on smaller, bolt-on deals in the last few years but certainly has the capacity for larger ones - at the end of the first quarter, it had $12 billion in cash and equivalents and net debt of $15 billion.

Conclusion

Novartis delivered strong Q1 2023 results and raised the full-year guidance. I am acknowledging that the stock has had decent momentum in the last few months that can continue another 10-15%, but it is hard to be bullish on the stock with the growth profile the company has at the moment and I remain neutral. Net debt notwithstanding, with an expected mid-single-digit EPS growth rate in the following years, the stock seems adequately valued at 15x this year's EPS.

Lastly, I do see a scenario where gains are more robust in the following years, but the acquisitions the company makes going forward will need to be outstanding, and we would need to see some blue-sky scenarios for some of the pipeline assets I mentioned.

For further details see:

Novartis: Limited Upside Despite Strong First Quarter Results, Improved Guidance