NVSEF - Novartis: Post Investor Day Higher Guidance Priced In

2023-12-05 04:57:41 ET

Summary

- Novartis has upgraded mid-term sales guidance to 5% CAGR until 2027.

- The core operating margin target is at 40%, and this implies a 6.5% upgrade in our EPS estimates.

- We are still concerned about sales post-2027 due to patent expirations. Therefore, we maintain our neutral rating while increasing our target price.

Following our deep-dive analysis called Novartis: Better Margin Visibility Ex-Sandoz (NVS) (NVSEF), last week, the company upgraded its mid-term sales guidance. Here at the Lab, we attended Novartis R&D Day, where the company outlined product mix and pipeline drivers. Today, we presented our forward-thinking outlook and summarised our key takeaways below. As a reminder, in a stand-alone model post-Sandoz spin-off, we forecasted a top-line sales CAGR growth of 3% until 2027. Looking at the company's press release, Novartis now aims to increase:

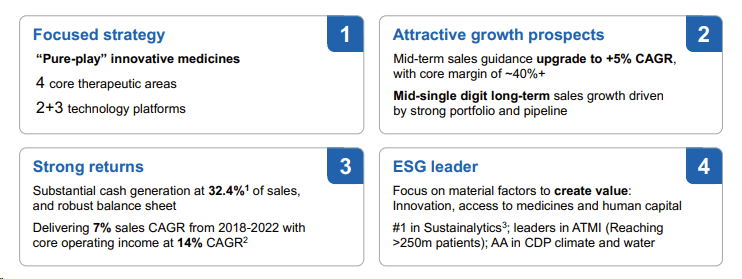

Mid-term sales guidance upgrade to 5% CAGR (2022-27), with core operating income margin of ~40%+ by 2027, driven by a continued strong momentum of crucial growth drivers thanks to a focus on four therapeutic areas and five technology platforms, which offer potential for consistent growth.

{kind=link}

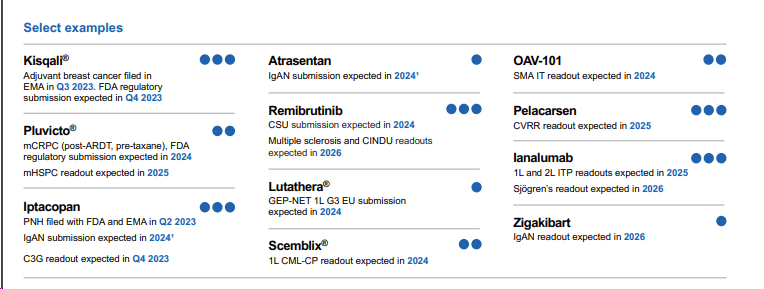

Before commenting on the numbers, these are our main drug updates:

- Pluvicto. The PSMAfore OS output release is on track to achieve 75% of data information in 2024. However, this signed a delay in readouts, which is now expected in 2025. These data are required to be filed by the FDA. Novartis has currently completed PSMAfore OS at a 45% data information level. As a reminder, this drug served for the hormone prostate cancer cure;

- Remibrutinib. The latest data show no liver toxicity signals. Remibrutinib was tested in Phase III with a 25mg dose. Novartis is now moving on with Phase III REMODEL trials in multiple sclerosis with a potential readout in 2026;

- Kisgali. The OS analysis data are sufficient to confirm no detriment. This should be sufficient for filing in the US for the above reason. Therefore, the company is on track to launch the drug in mid-2024;

- Novartis left its estimates on CV Outcomes data unchanged for Legvio and Pelacarsen for 2026 and 2025, respectively. The company also confirmed Phase III for JD0443 in the upcoming months and the Scemblix 1L ASC4First trial for H1 2024;

- Iptacopan FDA rule-out is expected in December 2023. The FDA decision in PNH and the Phase III C3G are both on track.

Changes in Estimates

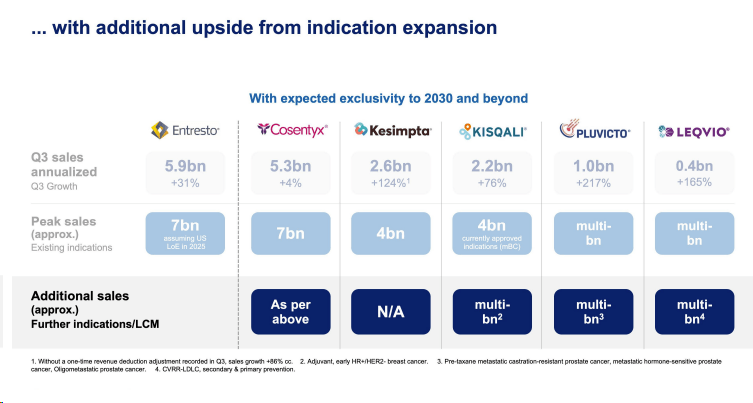

Here at the Lab, we are guiding sales growth by 5% until 2027 and a core operating margin of 40%. This implied a 6.5% upgrade to our previous internal EPS estimates. Novartis forecasted sales indicated Entresto US generic launch in mid-2025. Plugging in sales growth and a Core EBIT margin of 40%, we arrived at an uplift in EPS numbers of 6.5%. Cross-checking the Investor Day pipeline details, we noticed no significant updates in the management presentation post-2027, and the negative outlier was the Pluvicto competition trial shifted from 2024 to 2025. Our internal team has concerns about Novartis's medium-long revenue growth trajectory, and we believe the company is still a show-me story . Indeed, here at the lab, we see a challenging outlook with a series of harmful patent expirations. This includes Cosentyx, with an expiry by 2029 (Fig 3); Kisqali, with an expiry by 2030-2031 (Fig 4); and Kesimpta, with an expiry by 2030-2031 (Fig 5). For this reason, the company is running to standstill after 2027, with sales declining in the medium-term horizon (2027-2032). Therefore, Novartis' top management forecasts revenue growth on the current drug portfolio, and we believe that the company's stock price will be volatile on pipeline assets development. Wall Street is likely to assess Novartis's pipeline under significant scrutiny.

{kind=link}

Fig 1

{kind=link}

Fig 2

{kind=link}

Fig 3

{kind=link}

Fig 4

{kind=link}

Fig 5

In our forward-thinking estimates, we project a sales pipeline at a peak of $3 billion. Our inflection point is Iptacopan, with pivotal data in Q4 2023, remibrutinib (2026) , pelacarsen (2025), and lanalumab (2025). Following Novartis' higher guidance on the current portfolio, we increased peak sales of Kisgali and Kesimpta by $4 billion each, respectively. We also increased Entresto sales to $7 billion, and Cosentyx guidance was re-iterated at $7 billion. In 2024, we now project sales of $47 billion with a core operating profit of $17.7 and a margin of 37.7%.

Conclusion and Valuation

Although we had a favorable view of the recent company's progress ex-Sandoz, we are cautious about the post-2027 estimates. For the above reason, we retain our preference for Grifols and Roche . Post R&D day results, we raised our EPS forecast to CHF 7, and valuing the company with an unsighted P/E of 14.5x (in line with our EU pharma peers), we arrived at a valuation of CHF 101.5 per share ( from CHF 90 ). Therefore, we continue to remain equal weight on Novartis' equity value.

For further details see:

Novartis: Post Investor Day, Higher Guidance Priced In