NVSEF - Novartis: Q2 Beats Expectations But Still Pricey

2023-07-19 12:58:12 ET

Summary

- Swiss pharmaceutical group Novartis raised its full-year earnings forecast due to strong first half performance and plans a share buyback of up to $15 billion by 2025.

- The company also announced the separation of its generic drugs unit, Sandoz, through a 100% spin-off set for Q4 this year.

- Including patent expiration, we forecast $11.8 billion lower top-line sales by 2028.

- We positively view the share buyback, which adds 7% to our EPS estimate. Despite that, Novartis' valuation looks full, so we confirm our equal weight valuation on a twelve-month estimate.

Since our last update called " We are still neutral ," Novartis' stock price has been flat ( NVS , NVSEF ). The company's Q2 beats expectations with higher revenue by 9% to $13.6 billion and core operating profit, which reached $4.6 billion. Cross-checking analyst expectations, Refinitiv Eikon data showed consensus sales at $13.2 billion and EBIT at $4.3 billion. With these positive results, the pharmaceutical giant confirmed its buyback of $15 billion, which will be completed by 2025 end. Management is also optimistic about Sandonz's spin-off (the group's generic medicines division). Thanks to a better outlook, Wall Street positively reacted, and Novartis shares are up by more than 4% to CHF 88.12 (close to our 12-month target price set at CHF 90 per share ).

{kind=link}

Q2 results

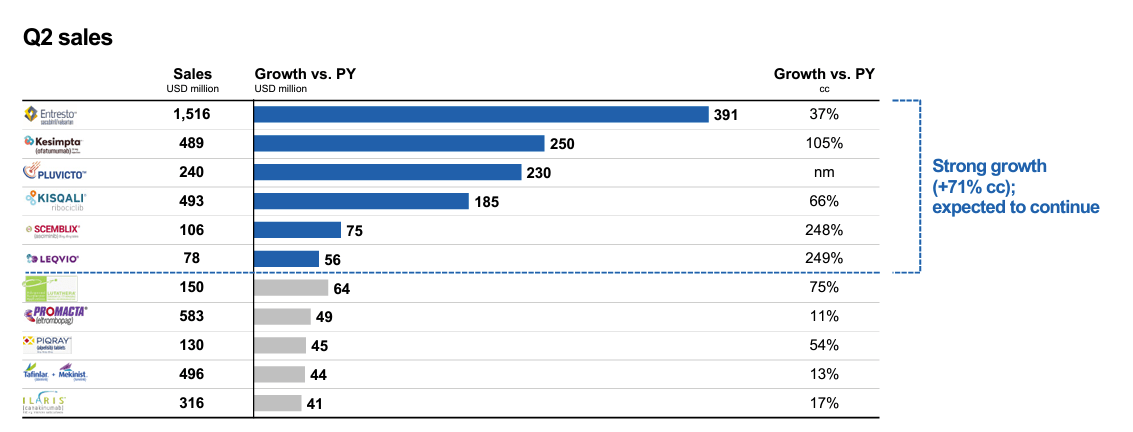

During the second quarter, Novartis delivered a 9% increase in top-line sales. Key revenue drivers were Entresto products (used for chronic heart failure), Kesimpta (used for multiple sclerosis), Pluvictio (radiotherapy used for prostate cancer treatment), and Kisqali (used for breast cancer treatment) - fig 1. The operating margin grew by 31% thanks to higher sales and lower restructuring costs, with the company's net profit increasing by 37%. In absolute value, the company's Q2 net profit rose to $2.32 billion from $1.70 billion achieved in the previous year. Regarding the second quarter results, Novartis CEO Vas Narasimhan explained that the company " delivered another quarter of strong sales growth and robust margin expansion that supported an increase in guidance. " On the company's operations, we should emphasize how Novartis's good performance was a broad-based beat in all the core therapeutic areas and in all geographies areas in which the company operates. Related to Entresto, the drug was up by 37% on a yearly basis, with revenue at $1.52 billion. As a reminder, the company is in litigation with generic players to launch cheaper alternatives ahead of Entresto's patent protection which expires in 2025. Pluvictio sales were up by $240 million on a quarterly basis thanks to an industrial upgrade in New Jersey facility that helped to overcome production shortages. Kesimpta also surpassed consensus expectations, with top-line sales doubling to $489 million sequentially. We recently participated in the ASCO investor meeting and are not surprised to see Kisqali's sales performance evolution. Looking at the drug Q2 outcome, we confirmed a $5.5 billion sales peak representing 6.5% of the company's future net present value.

To sum up our calculation, considering patent expiration, we anticipate $11.8 billion lower revenue until 2028, including $4.7 billion in oncology and $3.8 billion from Entresto turnover. Related to Entresto EU, the company got a patent extension protection to November 2026 (Fig 2).

{kind=link}

Fig 1

{kind=link}

Fig 2

What we liked was the restructuring process which started to be evident in the second quarter and reflected the company's margin improvements. In addition, the company has a few assets in approval processes with non-competitive profiles from generics.

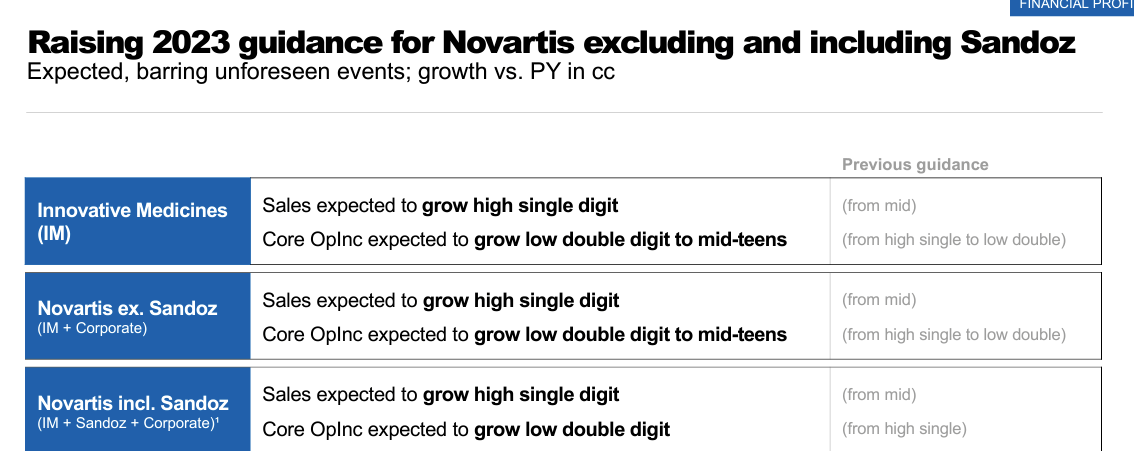

The company has also increased its 2023 guidance with the group's sales increase from 5-6% (in the mid-single digit estimate) to 8-9% (or high single digit). While operating profit moved from 8-9% to an increase in the 11-12% range. Supported by these positive performances, as already anticipated, Novartis announced a new $15 billion stock buyback plan ending in late 2025. This approval alleviates worries about a relevant acquisition; however, Novartis still has a solid balance sheet. In detail, the company has a capital structure, despite repurchasing 61.3 million shares in H1. This was equal to a cash outflow of $5.8 billion. In June, also considering the buyback, Novartis' net debt increased moved from $7.2 billion to $15.4 billion versus December. This was driven by the dividend payment for a total consideration of $7.3 billion, partially offset by the free cash flow generation of $6.0 billion.

{kind=link}

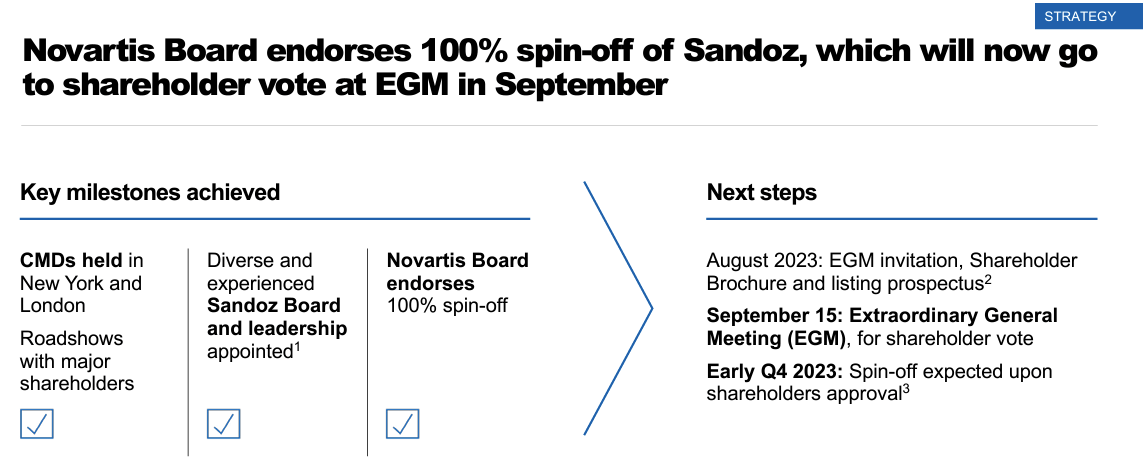

On the Sandoz spin-off, we understood that the Novartis board has unanimously supported the plan to separate the company and create an independent generic player. The next step is a shareholders' vote which will take place thanks to an extraordinary meeting scheduled for 15 September. According to Novartis, the Sandoz sale is expected in the first days of Q4 with a plan to IPO the group in the Swiss exchange Six in combination with an American depositary receipt (ADR), i.e., a structure that allows American investors to buy shares in dollars easily. In our estimates, Sandoz accounts for 10% of Novartis sales.

{kind=link}

Conclusion and valuation

With the current spin-off, the company will move on with its transforming strategic plan to become a pure Innovative Medicines player. Novartis will focus on five core therapeutic divisions (hematology, immunology, cardiovascular, tumors, and neuroscience), with significant market share penetration and a rich pipeline in each segment. This will address Wall Street's negative comment on turnover growth estimates. In addition, the company is now prioritizing investment in emerging platforms such as xRNA and cell therapy, with investment into manufacturing scale and new R&D capabilities. Novartis's priorities are 1) growth acceleration, 2) higher returns with a friendly shareholder remuneration policy, and 3) scaling technology and data to build better drugs for society.

In our estimates, we were already ahead of Wall Street numbers. Here at the Lab, considering patent expiration and Sandoz spin-off, we forecast a 2.5% CAGR pharmaceutical revenue growth combined with a 3.7% EBIT growth until 2028. Once again, we positively view Novartis' buyback, which should drive the company earnings per share growth by approximately 7%. Despite that, looking at the company's peers at a price/earnings level, Novartis' valuation looks full. Last time, we raised top-line sales and earnings per share estimates, and so today, we confirmed our CHF 90 target price valuing Novartis with a 2024 P/E of 14.5x, including a 6% historical discount vs EU peers. We prefer Roche and Griflos (recent rating upgrade) within our EU coverage.

For further details see:

Novartis: Q2 Beats Expectations, But Still Pricey