NVS - Novartis: Underlying Performance Is Compelling

Summary

- Novartis reported Q4 results that missed the consensus revenue estimate.

- The underlying performance was good, however, as currency-neutral revenue and profit grew.

- The outlook for 2023 is positive, and the company offers nice shareholder returns.

Article Thesis

Novartis (NVS) reported its fourth-quarter earnings results on Wednesday morning. The company's underlying performance was healthy, even though Novartis reported a small revenue decline versus the previous year's quarter. A dividend increase and ongoing buybacks are nice as well, although Novartis has become more expensive in recent months.

What Happened?

These are the headline numbers for the quarter:

Seeking Alpha

Starting with the top line, Novartis missed estimates by around 4% and reported a mid-single digits revenue decline. That's not great, but investors should consider a couple of items that we'll get into. Novartis beat profit estimates easily, however, with earnings per share hitting a run rate of well above $6. That was possible thanks to strong underlying profitability growth, showcased by the 15% increase in Novartis' core operating income.

Novartis Is Executing Well

How do declining revenues and earnings beats go hand in hand? One of the biggest factors is the US dollar. Over the last year, the dollar has strengthened considerably vs. most currencies, including the Yen, Euro, and so on, as the US is seen as less impacted by the global energy crisis. A strengthening US dollar means that revenues that are generated outside of the US are worth less once denominated in USD. A strengthening US dollar is thus a major headwind for a company like Novartis that generates a vast portion of its revenue in non-US markets. The good thing is that some of Novartis' costs are impacted by these currency rate movements as well - costs that are paid in Euros, for example, also are lower once denominated in USD, all else equal. Currency rate movements had a big impact on Novartis' revenue, which explains the reported top-line decline, but the hit to NVS' profits wasn't as hard as one might assume, as some costs declined as well in reported terms.

Looking at currency-neutral results, Novartis would have delivered a revenue increase of 3% year over year:

{kind=link}

Sales growth in the 3% range is not outstanding in absolute terms, but it's solid for a big and diversified pharma company such as Novartis. If a sales growth rate of 3% could be maintained forever, while the company also buys back some shares and pays out a nice dividend, that could make for very solid long-term returns.

Delving into Novartis' product portfolio, we see that the major growth drivers were in Novartis' innovative medicines portfolio, whereas Sandoz, which will be spun off in H2 according to management, has not generated meaningful growth. That's not too surprising, as the generics market isn't experiencing strong market growth, and since the company can't boost sales via the introduction of new and high-performing drugs in this segment. In its IM segment, however, Novartis benefits from relatively new introductions such as Kesimpta, which grew by more than 150% at constant currency rates. Kesimpta (ofatumumab) is used as a treatment for relapsing multiple sclerosis. There are unmet patient needs in this area, and there's also a major market opportunity for companies such as Novartis, as the MS market opportunity is close to $30 billion in 2023, and since this market continues to expand. Novartis has a lot of competitors in this space, of course, but even a 10% market share would be enough to generate $3 billion in revenue eventually.

Pluvicto has been another strong performer in Novartis' portfolio. The drug, which is used for the treatment of prostate cancers, has been launched very recently but has already generated $180 million in revenue during the fourth quarter. It's very likely that the run rate will be north of $1 billion soon, as the $180 million in revenue in Q4 were achieved with just 160 active centers, and Novartis will be adding significantly to that number in the coming quarters and years. On top of that, Pluvicto also will benefit from a recent phase III study (PSMAfore) result that was reported in Q4 that indicates the drug performs well in the treatment of metastatic castration-resistant prostate cancer, which has led to approval in the EU. Pluvicto is currently being evaluated in two more phase III studies, both for different niches in the prostate cancer indication. When results are positive, the drug's market opportunity will grow further - together with an ongoing ramp-up in the indication the drug already is approved for, this could allow for significant revenue growth in the coming years.

Outlook For 2023

We don't know yet when exactly Sandoz will be spun off, but management states they see this happening during the second half of the current year. Guidance is including Sandoz, however. Per management's guidance, Novartis will grow its revenue at a low to mid-single-digit rate this year. That suggests growth in the 2%-5% range, I assume, which would be very solid, although not spectacular. Importantly, management believes that profit growth will be somewhat stronger, as operating income is forecasted to grow at a mid-single-digit rate - I assume that's around 4%-6%.

The introduction of new drugs in Novartis' portfolio that have higher average margins, a sales shift towards the more profitable IM drugs relative to Sandoz's products, as well as cost reduction efforts across its operations, will allow Novartis to grow its underlying profits at a faster pace relative to its sales, which is great for investors.

Since the US dollar has strengthened considerably in 2022, but since no further gains in the USD vs. the Euro, Yen, etc., have been seen in 2023 so far, I believe that currency rates will be less of a headwind this year. Investors can thus expect that reported results and underlying results will be more in line with each other unless currency markets experience unforeseen turbulence (which can't be ruled out, of course).

Shareholder Returns, Valuation, And Outlook

Novartis is an established pharma major that invests in its pipeline, but that generates significant surplus cash flow on top of that, like most of its major peers. That allows Novartis to return large sums of money to its owners over time.

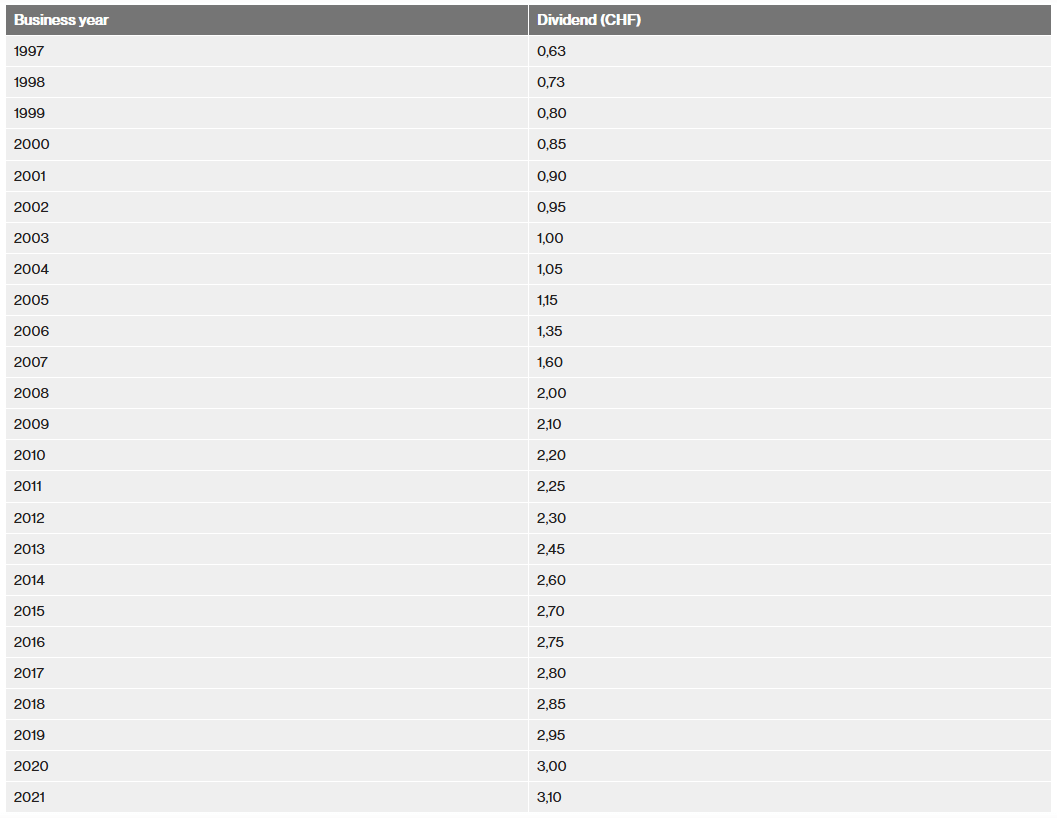

The company has been increasing its dividend for decades in its local currency, the Swiss Franc:

{kind=link}

Between 1997 and 2021, Novartis grew its dividend by 7% per year on average. That's a compelling result, especially considering that the dividend has been raised every year, no matter what the economic picture or the macro environment looked like. Even during the Great Recession and amidst the COVID pandemic, Novartis continued to increase its dividend.

For 2022, Novartis has announced another dividend increase: The company plans to pay out CHF 3.20 early this year, which represents a ~3% increase versus the dividend payment for 2021 that was made in early 2022. Like many other European companies, Novartis makes just one dividend payment per year. A 3% growth rate is less than what Novartis has delivered over the last two decades, but that was to be expected, as Novartis' dividend growth had slowed down to a low-single-digits rate in recent years.

Novartis also offers some buybacks under its current $15 billion program, which covers around 8% of the company's market capitalization. Around $5 billion of that is still available before additional approvals will be made, which is enough to reduce the share count by around 3%. History suggests that Novartis will not spend all of that in 2023, however, as Novartis has bought back 1%-2% of its shares per year over the last decade. Still, over time, the buybacks add meaningfully to NVS' earnings per share growth.

If Novartis managed to grow its sales by 3% per year going forward while growing its profit at a slightly higher pace of 4% per year thanks to margin expansion initiatives, a 1% buyback pace could allow for 5% annual earnings per share growth. Add the dividend yield of 3.8% (using the CHF 3.20 dividend at current exchange rates), and Novartis could deliver annual returns in the 9% range at constant valuations.

Novartis currently trades at 14x forward earnings (using the analyst consensus estimate), which is far from expensive in absolute terms. It's not the absolute bargain it was a couple of months ago, however, when NVS traded in the mid-$70s for a while. From a timing perspective, waiting for a better entry point could pay off, as Novartis currently trades close to its 52-week high. But even from here, returns should be very solid in the long run, thanks to some expected growth and NVS' attractive dividend.

For further details see:

Novartis: Underlying Performance Is Compelling