NVSEF - Novartis: Valuation Seems Fair

2023-04-26 13:09:44 ET

Summary

- Novartis delivered very strong Q1 results.

- Sandoz spin-off is advancing, but there were no major details.

- The company raised its FY outlook. Despite that EPS growth is likely limited and Novartis valuations look full.

Novartis ( NVS , OTCPK:NVSEF ) just released a solid set of numbers with a beat both at top-line sales as well as at the core operating profit by 3% and 9% respectively. This outperformance was driven by Sandoz and its Innovative Medicine division. In detail, the Pharma margin results were particularly remarkable, with IM core operating margin at 38.7% compared to average consensus estimates set at 36.8%. As we were expecting, the Novartis pipeline was focused on the recent Kisqali NATALEE adjuvant study success and the recent new Pluvicto manufacturing facilities approval thanks to the Food and Drug Administration's latest decision. Both Pluvicto and Kisqali were the positive drivers of Novartis' Q1 performance and here at the Lab, we believe these are the reason behind the company's better 2023 outlook.

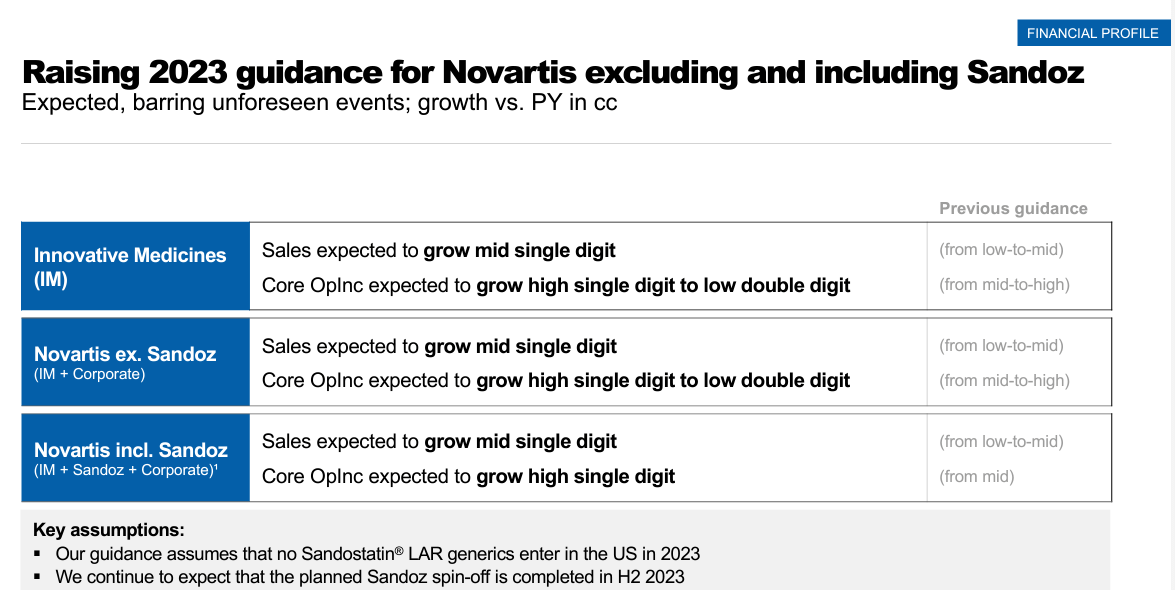

Indeed, the company raised its 2023 estimates. In detail, the Swiss pharmaceutical giant increased expectations for both pharma sales and its operating profit. The company's management now targets mid-single-digit top-line sales growth from low-to-mid-digit and high-single-digit operating profit growth from mid-single-digit. And again, related to Sandoz, the company upgraded its estimates. For the above reasons, we were not surprised to see a +4% increase at the stock price level after earnings.

{kind=link}

Q1 products outperformance & weakness

As already mentioned, the sales growth driver was Kisqali which beat Wall Street estimates by more than 20%. In the Q1 presentation, we understand that the drug outpaced the competition and increased its market penetration. With the positive Kisqali NATALEE adjuvant new data, here at the Lab, we are confident that Novartis will continue to gain traction in the ER+ metastatic breast cancer markets. Pluvicto also was a success with a beat of 11%. Drug demand is known to be solid but top-line sales were better than expected thanks to supply constraints. In our assumption, this positive performance should ease in the second half of the year given the recent approval of Milburn US and the new manufacturing facilities in Zaragoza. Thanks to US prescriptions, Entresto continues to be a success story with solid sales momentum, beating consensus by 5%. Here at the Lab, we believe that this strong underlying growth will be recorded ex-US and a positive trend is expected in the whole of 2023. Piqray also surprised analyst estimates being 22% ahead of consensus.

On a negative note, three top-twenty products missed expectations. 1) Cosentyx was a negative outlier with a 4% miss. This was due to weakness in US reimbursement and lower Chinese price. Despite that, in the Q1 analyst call, Novartis remains convinced that label expansion will increase sales growth from the second 2023 half. As a reminder, the company took a provision in Q4. 2) Zolgensma was the other drug that missed expectations by 8%. We noted margin mix pressure. And finally, 3) Gilenya generic erosion was particularly strong and came 17% below consensus. However, we see limited mid-term consequences as this was well expected by the market. Indeed, in Q4, there was a negative decision concerning 405 patent validity and US prescription data was already reporting that branded volumes were down by more than 60%.

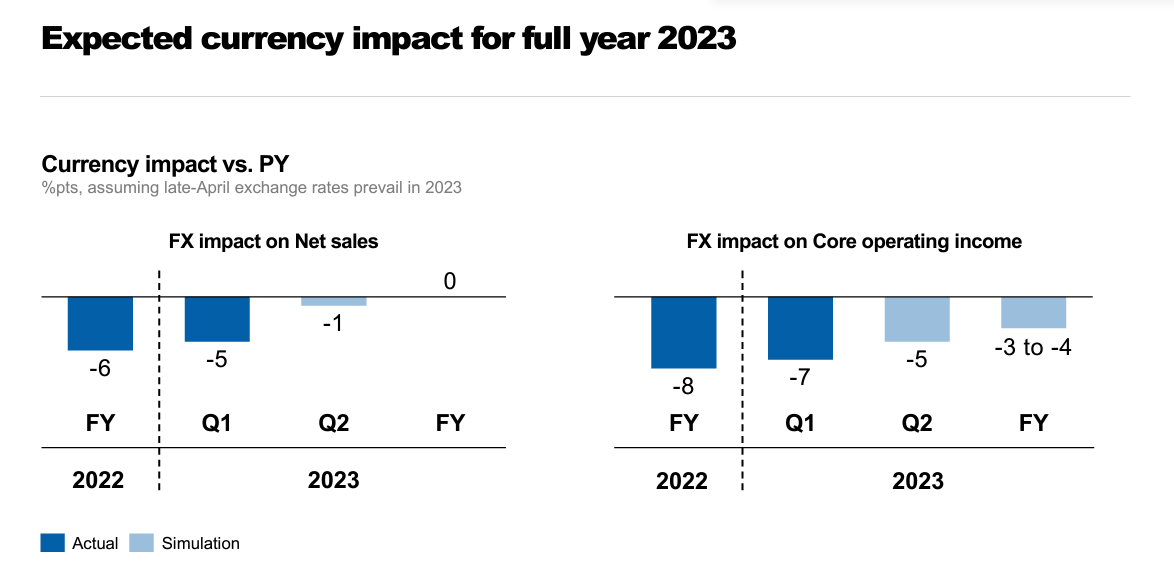

In mid-March 2023, the company published its expected FOREX impact on Q1 as well as on the Fiscal Year 2023 results. Cross-checking the Novartis release, the company is in line with the initial estimates. Here at the Lab, for 2023, we are forecasting a minus 1% impact on top-line sales and a minus 3.5% on core operating profit.

{kind=link}

Conclusion and valuation

As Novartis prepares for the Sandoz spin-off expected in 2H23, here at the Lab, we are forecasting stand-alone investment in infrastructure. We are still waiting for an update on the carve-out financials as well as on the ongoing biosimilar approval pipeline.

Even if the company now targets a mid-single-digit earning per share growth in the next years, Novartis is trading at 15x 2023 EPS. In our last analysis, we valued Novartis with a target price of CHF 80 based on 13x P/E 2023 with a 13% discount compared to its closest Pharma peers. The company's limited growth potential confirms our previous valuation and we believe that this valuation is fair. Therefore, our neutral rating is reiterated .

For further details see:

Novartis: Valuation Seems Fair