VICI - November's 5 Dividend Growth Stocks With 5.57%+ Yields

2023-11-19 10:14:12 ET

Summary

- Dividend growth stocks often provide reliable cash flows and long-term wealth for income investors.

- Screening dividend stocks based on safety, growth, and consistency can be beneficial to find new opportunities important for investors.

- In this month's article, we highlight these five dividend stocks: Medifast, Realty Income, ONEOK, VICI Properties, and Cogent Communications Holdings.

Written by Nick Ackerman.

For some background on this monthly publication, here is my view on dividend growth stocks :

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines, and they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all returned back into your pocket from that point forward.

All of this being said, it is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 397 stocks at this time from the 535 listed last month. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

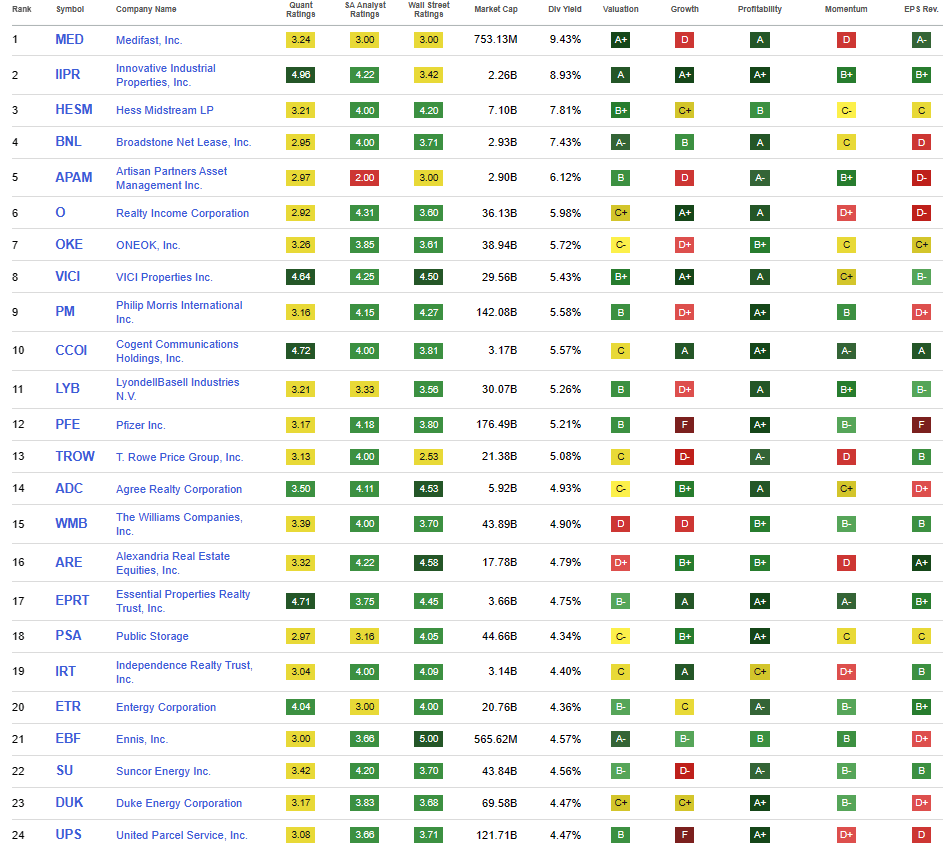

I will share the top 24 that showed up as of 11/05/2023.

Top 24 Screening (Seeking Alpha)

{kind=link}

We recently covered Innovative Industrial Properties ( IIPR ), Hess Midstream ( HESM ), Broadstone Net Lease ( BNL ) and Philip Morris International ( PM ), so we'll be skipping those today.

Artisan Partners Asset Management ( APAM ) we will skip because they pay a variable dividend, though it could be worth a look in a different article.

The five we will be touching on are Medifast ( MED ), Realty Income ( O ), ONEOK ( OKE ), VICI Properties ( VICI ) and Cogent Communication Holdings ( CCOI ).

Medifast 9.43% Yield

MED is an interesting name that continues to have to grapple with its post-pandemic slump. This Covid darling was taken to the woodshed after the whole health trend kind of fell off - as these sorts of fads tend to do.

Ycharts

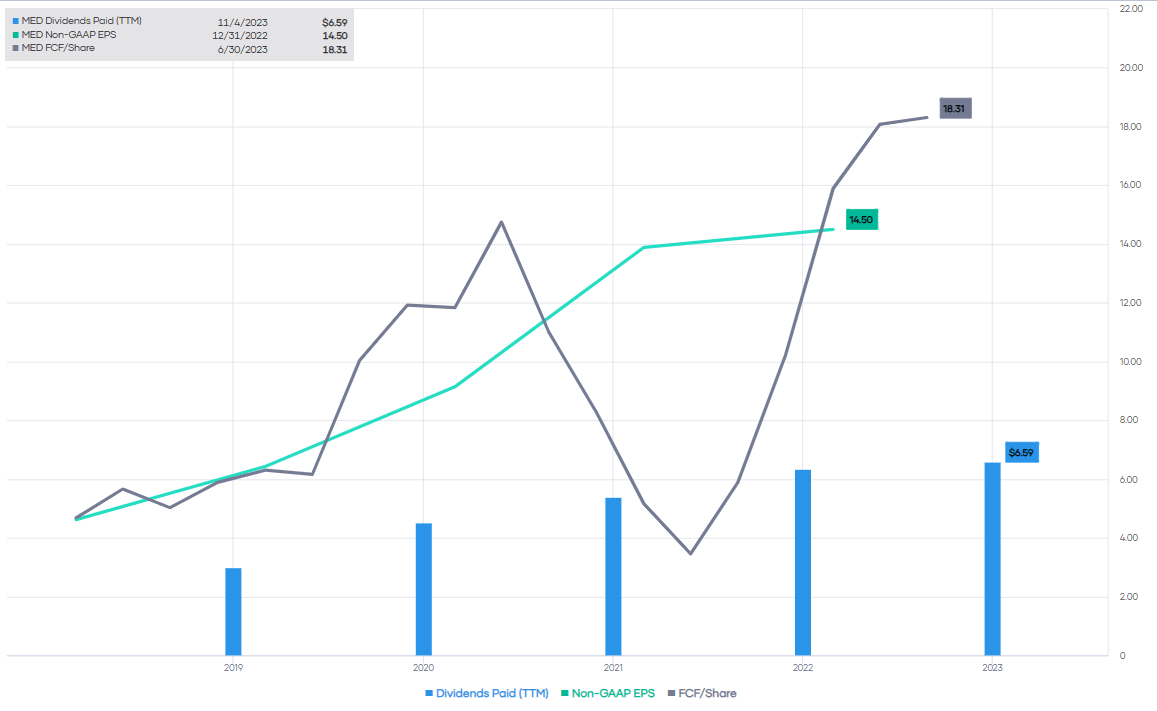

That said, it has pushed the stock to trade at an abnormally large dividend yield in this slump. That said, the FCF/share of this company still leaves it with tons of room as sales soften.

MED Earnings and FCF vs. Dividends Paid (Portfolio Insight)

{kind=link}

Analysts expect EPS in 2023 to slide down to $8.53 and then in 2024 once again go lower to $8.13. Still, that would indicate that the current $6.6 annualized dividend is more than covered. A dividend that has been growing for the last seven years. They even raised the token $0.01 when the last raised for 2023 to keep that streak alive, so they clearly find that it is important.

That being said, the company itself doesn't have as rosy of an outlook. In their last earnings, they noted that they expect Q3 results to come in at $0.71 to $1.32 - after they had posted $2.77 for earnings in Q2. However, things didn't seem to be as ugly as they thought, as EPS came in at $2.12 .

Interestingly, though, the company seems to have a problem with forecasting. They had an outlook when they announced their Q1 results that Q2 would see EPS come in at $1.32 to $1.44 while it blew those away by about double.

Full-year 2023, they anticipate EPS to be between $8.65 and $9.55. Given that they have already baked in $8.56 for the year, that means they are once again forecasting for a dire next quarter.

So it appears the management team is horrible at forecasting, and/or their operations aren't declining as much as they believe they are. While the goal is to under-promise and then over-deliver, there is a point where it is too much. At this point, it would at least seem they have no clue what their business will do, so throw out the kitchen sink every quarter and hope it isn't as bad.

I'd view this as only a more speculative bet and wouldn't be going in with the expectation that the dividend necessarily holds as they themselves project a shortfall.

Realty Income 5.81% Yield

O is new to the top five names that we'll be touching on, but of course, it needs little introduction. It's a consistent monthly payer and is top quality overall. They boasted with their latest dividend announcement the 640th consecutive monthly dividend . They're a dividend aristocrat member with 25 years of consecutive annual dividend growth under their belt.

O Dividend History (Seeking Alpha)

{kind=link}

However, when announcing the acquisition of Spirit Realty ( SRC ) in an all-stock deal, the stock initially dropped significantly . That being said, it did rebound nearly just as significantly. They anticipate that the merger will be accretive to earnings, and they have a history of making successful acquisitions. There is no reason to doubt that they aren't making a smart move at this time that they feel will move the needle. To move the needle on this behemoth, they need these sorts of large acquisitions anyway. With the acquisition, the coverage of the dividend only improves due to being an accretive deal.

The recovery was also helped significantly with the risk-free Treasury Rates dropping fairly dramatically after the Fed's latest meeting. Which coincidentally also meant that O would be picking up SRC for quite an attractive offer. Since it is an all-stock offer, it is a bit of a moving needle on what the final price would be, as SRC shareholders would receive 0.762 shares of O.

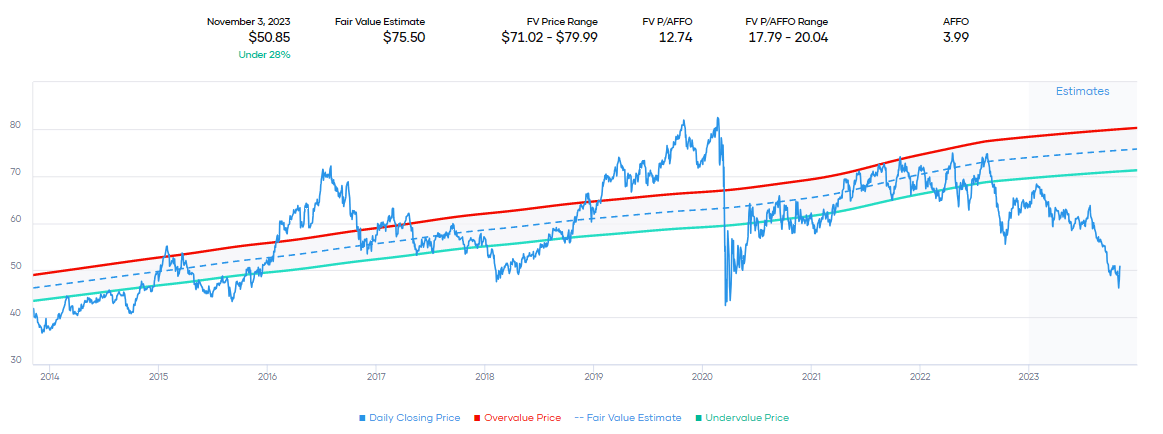

Given the higher interest rate environment, O trades at a much lower P/AFFO than it once did. However, at this point, the downside is quite absurd, in my opinion. Though I'm probably biased with a significant position in O already, and when the SRC was announced, I sold more puts to potentially make my position even larger. That said, at just 12.75x P/AFFO, we are trading at an attractive level for one to consider initiating a position at these prices.

O Fair Value Estimate (Portfolio Insight)

{kind=link}

ONEOK 5.72% Yield

OKE is a regular on this list, and the last time we touched on this name was back in May of this year . It was right around that time that OKE announced that they were looking to acquire Magellan Midstream ( MMP ). It seemed there was some pushback to the deal due to tax considerations for MMP, but it gained approval from investors anyway.

In September, that acquisition was completed , and it made OKE a more sizeable midstream player with a diversified portfolio. The breakdown below is the company representing earnings by each segment of the combed business.

OKE Business Segments (ONEOK)

OKE has been delivering a growing dividend for the last 25 years, experiencing no cuts during this time. While it has held steady for the last few years, they are once again in growth mode and raised the dividend starting this year.

{kind=link}

They are looking to give more clarity on dividend growth in 2024 when they were asked about that in their latest earnings call . They also noted that debt was coming down quicker than they had expected, "giving us significantly greater flexibility as we move forward to think about capital allocation." Whether that means more capital for shareholders through a higher dividend or buybacks, or if that capital is going to growth projects, either way, it should benefit current shareholders.

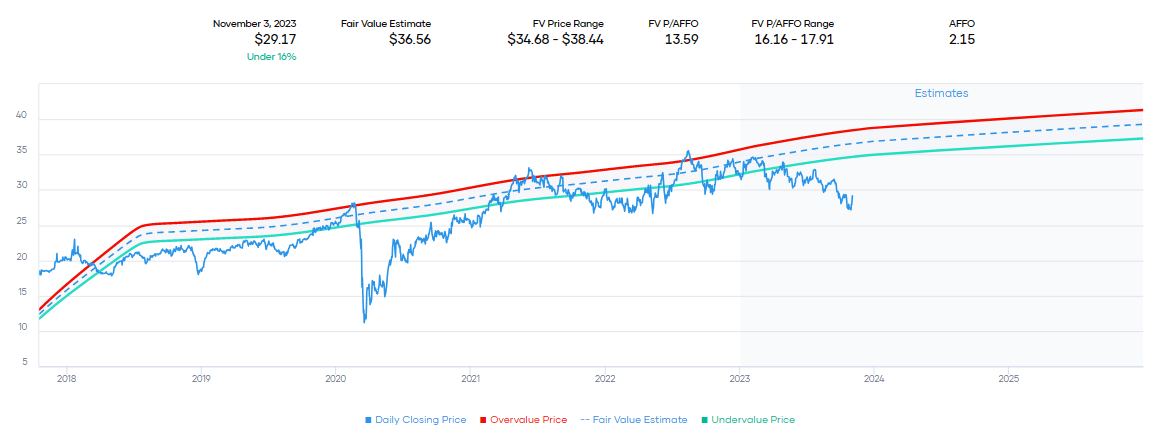

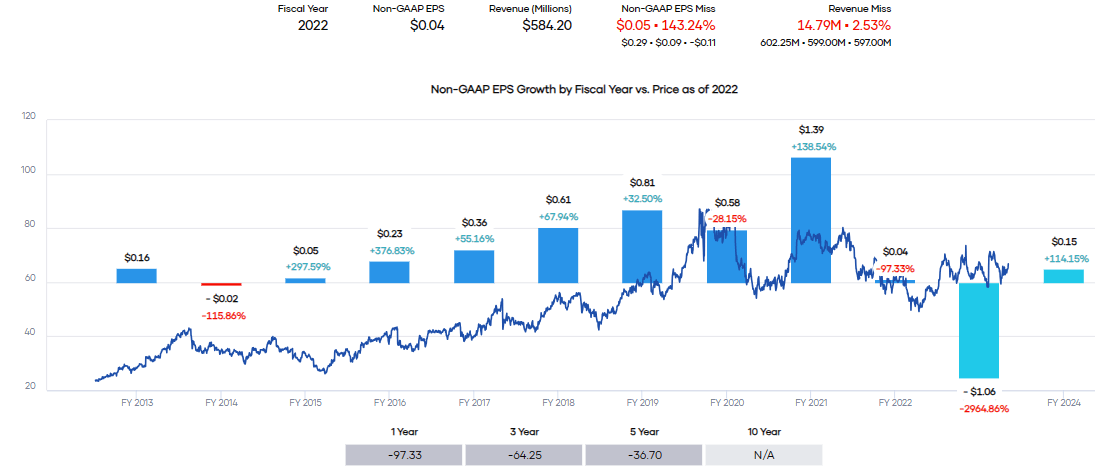

VICI Properties 5.43% Yield

VICI is another name that was hit recently, similar to O, but snapped back with some vengeance as risk-free rates subsided. A recent announcement of acquiring some bowling alleys from Bowlero ( BOWL ) also seemed to cause some anxiety among investors.

However, that anxiety went away with their latest earnings coming in with a beat and boost to guidance for their latest quarter. They posted FFO of $0.54, above the $0.53 projected. They guided for adjusted AFFO for 2023 to come in at $2.14 to $2.15, up a few cents from the $2.11 to $2.14 range. That definitely helped with the snapback of the share price.

Ycharts

This was to my detriment as I was beginning to take a look at making a move on VICI, but my delay made me miss out on the opportunity for now at those lower prices. VICI is always on my watchlist, and it's a name I've held in the past. We've successfully traded it through writing puts and then writing calls.

That being said, VICI, even at these prices, isn't showing any sort of overvaluation, in my opinion. This means there is still some opportunity here, but it's just not as lucrative as when you consider it was at around $27 per share.

VICI Fair Value Estimate (Portfolio Insight)

{kind=link}

If rates stabilize or even continue to head lower, we could definitely see these shares continue to climb.

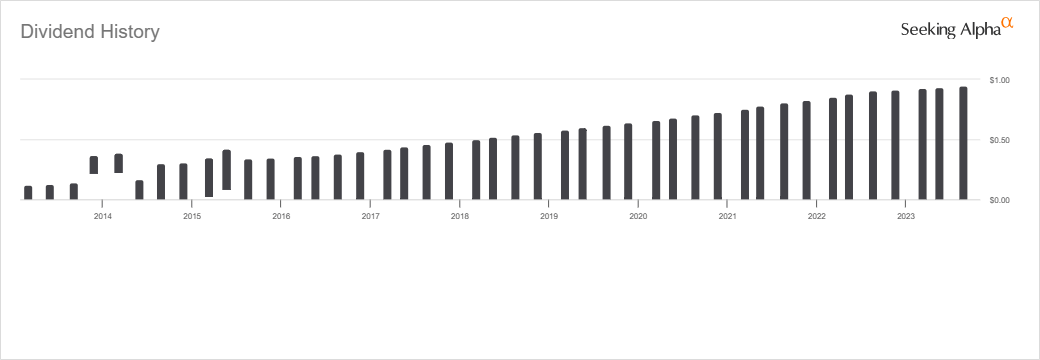

Cogent Communications Holdings 5.57% Yield

CCOI is another one of my watchlist names, but I want a much lower price. This is a company that has been raising its dividend every quarter, though the pace of those raises is starting to slow down.

CCOI Dividend History (Seeking Alpha)

{kind=link}

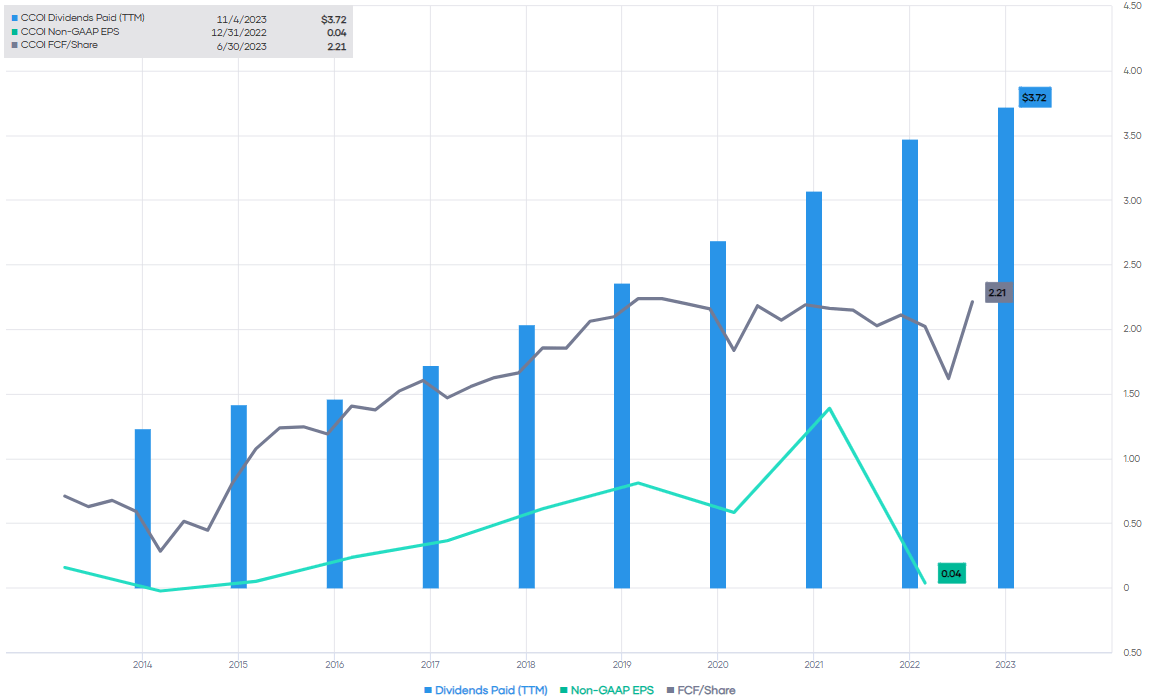

That's for good reason, too, as the company isn't covering its payout with regular earnings. This presents why I've been hesitant to add, though it has meant I've missed out on some opportunities as the share price still moved higher through 2023. Sometimes, my worst moves are those when I don't make a move fast enough, but that's investing. That said, here's a look at the FCF and EPS relative to their dividend payout.

CCOI EPS and FCF vs. Dividends Paid (Portfolio Insight)

{kind=link}

Their last quarter showed an EPS of $23.84, but this has to do with acquiring Sprint assets from T-Mobile ( TMUS ). That's causing all sorts of noise in their earnings and will do so in the following years; analysts are now projecting negative earnings going forward before climbing again.

CCOI Earnings History (Portfolio Insight)

{kind=link}

Of course, on the revenue side, that is expected to climb significantly as they acquire all these new connections.

CCOI Earnings Estimates (Seeking Alpha)

{kind=link}

That's precisely what their last earnings report showed, too, that revenue was up 61.5%. EBITDA, on the other hand, declined year-over-year by 7.5% for the quarter. On an EV/EBITDA basis, the stock price seems exceedingly expensive relative to its ~16x area.

CCOI EV/EBITDA (Seeking Alpha)

{kind=link}

Operating cash flow did surge higher, though, which is a positive as that gets them to a level where they can at least cover their dividend after it slipped lower.

Ycharts

In a scenario where cash flows aren't covering the dividend, any growth can really only come from taking on debt or issuing shares. Along with raising the dividend every quarter, they also issue shares nearly every quarter. With a net leverage ratio of 4.56x and rising, they carry some significant debt levels. Though, as they operate a utility-like business with fairly predictable cash flow, this might not be a problem for some investors.

Ycharts

This puts added pressure on the dividend in the future when more and more needs to be paid out. Hopefully, with the Sprint assets, cash flow growth can be reinvigorated or at least buy the company some time with added flexibility on the next moves. So, it is positive to see once again that operating cash flows can cover the dividend after having slipped and stagnated, but watching to see which way the trend goes from here will still be important.

With so much noise in their earnings, I'm willing to continue to sit on the sidelines and wait despite the resiliency of its share price, which seems only to want to go higher along with its dividend.

For further details see:

November's 5 Dividend Growth Stocks With 5.57%+ Yields