SNY - Novo Nordisk: Attractive Market But Likely No Margin Of Safety

Summary

- Novo Nordisk is a market leader and the only pure-play in the diabetes and obesity care space.

- The nature of the diabetes care business makes Novo Nordisk rather recession-proof.

- The stock priced in much of the assumed future growth and I have concerns about competition, especially from Eli Lilly.

- While I think Novo Nordisk is an excellent business, I rate the stock a hold.

Author Note: Since Novo Nordisk reports in DKK (Danish crones), I will refer to financial data in DKK. For per share and valuation purposes I will add the US$ equivalents.

While looking for investment opportunities in the healthcare space, discarding many of the big pharma players early in the process, I came across Novo Nordisk ( NVO ). Since I was impressed with the overall financial metrics, I decided to add Novo Nordisk to the list of companies I needed to do a deep dive on sometime in the future. This time is now and I want to share my thoughts on Novo Nordisk in this article.

Introduction

Novo Nordisk is a healthcare company based in Denmark. It operates and reports in two segments: Diabetes/Obesity care and Rare Disease. In FY2022, the Diabetes and Obesity care segment accounted for 88% of sales while the Rare Disease segment made up the remaining 12%.

As for the structure of this article, I will start with a short peer-group comparison of some of the metrics I think are important before giving an overview of the company's operations. In the second part, I will cover the GLP-1 and the obesity care sales, because these are and will be the main growth drivers for the foreseeable future. In the last part, I will go over the financials including a short DCF valuation, go over the risks and lastly give my conclusion.

Peer Group Comparison

The problem with doing a peer group comparison in the pharmaceutical space is that all the companies have different areas of focus. Novo Nordisk for example is pretty much a pure play on diabetes care. There is no other company like Novo Nordisk.

Another problem is that assessing the quality of pharmaceutical companies can be pretty hard because we never know how many of the drugs the companies got in their pipelines will make it through the phase 3 trials, ultimately being marketed.

In my opinion, there are only two qualities to look out for:

(a) The company is doing a good job of doing acquisitions. This means that the M&A team does an outstanding job in figuring out if a potential drug will make it through all needed trials so it can be marketed. They also need to do a great job at gauging the actual sales and margin potential for those drugs. Lastly, this way of creating value for shareholders needs a really good CFO and financial management team because if the company doesn't have these, the returns on the invested capital will be mediocre at best. In my opinion, a prime example of this is the M&A and financial team at Bristol-Myers Squibb ( BMY ). The way they acquired Celgene, paying partially with their stock that was trading at a much higher valuation back then than it does now, and how they use the cash flows from the acquisition to buy back shares aggressively in the recent past is a prime example of smart financial management. Bristol-Myers' return on capital employed (ROCE) dropped to 8% in the year of the acquisition and is already back to 25% since then.

(b) The company is getting great returns on capital on self-developed drugs. This comes down to the company generating high ROCE.

I decided to use the following companies for the quick peer group comparison because they are active in the diabetes space according to this SA news article : Eli Lilly (NYSE: LLY ), Sanofi ( SNY ), Merck (NYSE: MRK ), Novartis ( NVS ), and AstraZeneca ( AZN ).

To start with, here is a chart showing the total return for the six companies over the past decade. As we can see Eli Lilly is leading the pack by quite a big margin with Novo Nordisk coming in second place.

The next chart shows the EV/EBITDA over the past decade and explains why Eli Lilly's total return is so far ahead. Eli Lilly saw the multiple expand a lot (as did AstraZeneca) while Novo Nordisk's multiple only increased a little bit. Adjusted for the multiple expansion, the fundamental performance of Novo Nordisk was probably on par if not even better than that of Eli Lilly.

The last chart shows what is the most important metric in my opinion, the ROCE. Novo Nordisk's ROCE was more than double the ROCE of the peer group over the past decade. This indicates that Novo Nordisk should probably belong to the (b) type of business I described above since such high ROCE is not possible with a pure M&A strategy.

The proof for this assumption can be seen in the following chart showing Novo Nordisk's goodwill over the past decade. I have to point out that this is a 10-year chart, you just can't see anything before FY2021 because Novo Nordisk had zero goodwill until FY2021 when it accounted for its first goodwill ever. Note that the amount is in USD.

My takeaway from this is that Novo Nordisk has a history of generating far higher ROCE than peers because they didn't engage in any kind of M&A activity. They were able to grow with high ROCE all by themselves. This leaves me to assume that Novo Nordisk has a highly innovative workforce. In the pharmaceutical sector, a highly innovative workforce is the single most valuable asset in my opinion, setting Novo Nordisk apart from the competition.

Business Overview

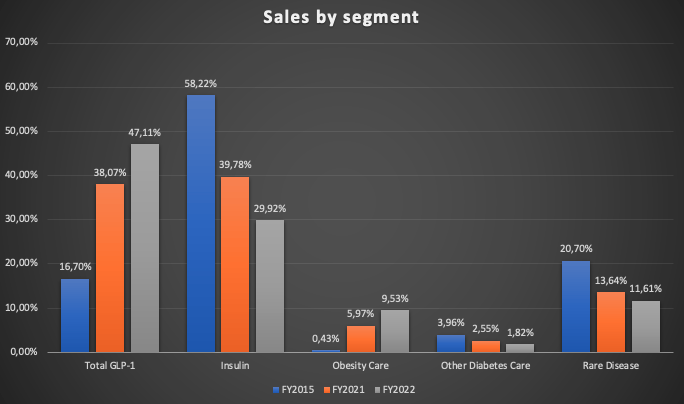

I want to start with a chart showing the development of Novo Nordisk sales by segment as a % of total sales for FY2015, FY2021 and FY2022:

Sales by segment as % of total sales - compiled by Author (Company Annual/Quarterly Reports)

{kind=link}

The contribution of GLP-1 (Glucagon-like Peptide-1) drugs to total sales nearly tripled since FY2015 while the contribution from the traditional insulin drugs dropped by close to 50%. The contribution of the obesity care segment grew by close to 22x and accounted for 9.5% of total sales in FY2022.

This chart alone doesn't tell the whole story though. Normally I would guess that the insulin drugs are losing sales while the newer drugs (GLP-1 and obesity care) are growing because they were approved much more recently. This would be the normal lifecycle in the pharmaceutical sector. Old drugs lose market share due to competition as soon as the patents run out and new drugs need to grow to make up for the lost sales.

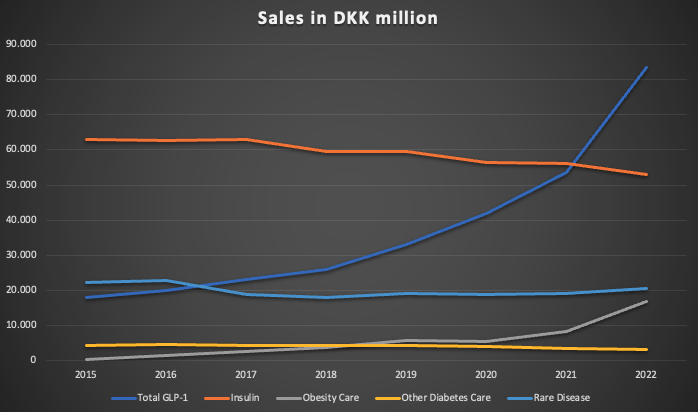

This is not the case for Novo Nordisk (at least on a segment basis), as can be seen in the following chart:

Total sales by segment from FY2015 (Company Annual/Quarterly Reports)

{kind=link}

The insulin sales only dropped from DKK 62,833 million to DKK 52,952, a drop of around 15%. Meanwhile, GLP-1 sales skyrocketed over the past few years, and obesity care sales are just starting to take off (I will come back to both of those segments later in this article). This is in line with what management presented at the capital markets day in March 2022, as can be seen in the snippet below.

Expected growth drivers towards FY2030 (Capital markets day 2022)

The GLP-1 drugs were the main growth drivers over the past few years and should drive growth in the future while the obesity care drugs are expected to materially drive growth well into FY2026.

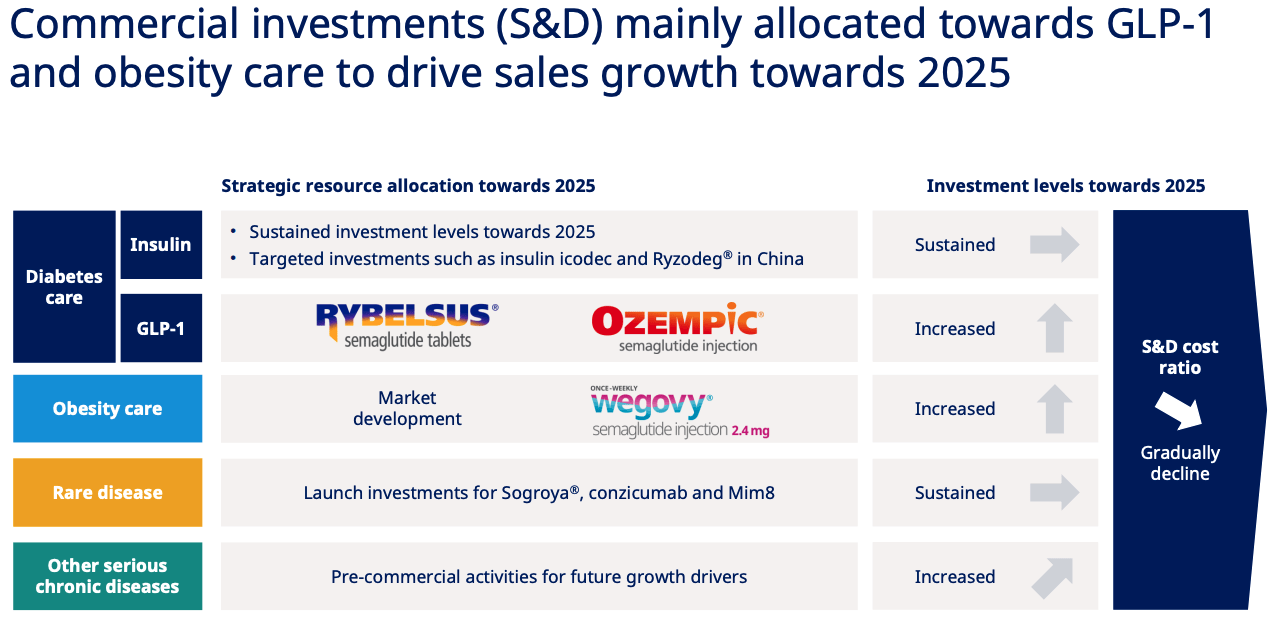

Accordingly, Novo Nordisk is planning to invest mainly in those two segments for the next few years, as can be seen in the next snippet from the capital markets presentation.

Planned investments (Capital markets day 2022)

{kind=link}

Now I want to give a superficial overview of how the best-selling drugs for the insulin and the GLP-1 segment work.

The top-selling drug for the insulin segment as of FY2022 is NovoRapid. According to the European Medicines Agency , NovoRapid is used for the treatment of diabetes mellitus in adults, adolescents and children aged 1 year and above. It can be used to treat type-1 and type-2 diabetes as it contains insulin aspart.

The top-selling drug for the GLP-1 segment as of FY2022 is Ozempic. Ozempic is used for the treatment of adults with insufficiently controlled type 2 diabetes mellitus as an adjunct to diet and exercise.

Type-1 diabetes is a form of diabetes where the body lost the ability to produce insulin and needs injections like NovoRapid. Type-1 is much more rare than type-2 diabetes. The German ministry of health states that in Germany, 90-95% of patients suffer from type-2 diabetes while the rest suffers from type-1 diabetes.

In the case of type-2 diabetes, the body is still able to produce insulin, but the amount it can produce is not enough. Besides genetic reasons, the main reasons for type-2 diabetes are being overweight and lack of physical activity. In case of a failed treatment (weight loss, nutrition, exercise), the last resort for type-2 diabetes patients is to either use GLP-1 (normally one injection per week) or inject insulin directly like type-1 diabetes patients.

Now from an investor's perspective, the fact that the insulin drugs and the GLP-1 drugs (in cases where type-2 diabetes can't get "cured") are a subscription kind of business is quite interesting (even if it may be morally wrong to think about it this way). This should make Novo Nordisk resilient to economic downturns because patients can't just stop taking their medicine.

To end this chapter I want to quote from Philip A. Fisher's book "Common Stocks And Uncommon Profits" and connect the quote to what we are seeing at Novo Nordisk right now:

The investor usually obtains the best results in companies whose engineering or research is to a considerable extent devoted to products having some business relationship to those already within the scope of company activities. This does not mean that a desirable company may not have a number of divisions, some of which have product lines quite different from others. It does mean that a company with research centered around each of these divisions, like a cluster of trees each growing additional branches from its own trunk, will usually do much better than a company working on a number of unrelated new products which, if successful, will land it in several new industries unrelated to its existing business.

Philip A. Fisher - Common Stocks And Uncommon Profits

Novo Nordisk has been a pure-play, market-leading company in the diabetes care space for a long time. The main focus in the past was the insulin business which is used to treat type-1 and type-2 diabetes. From the deep expertise in this area, Novo Nordisk was able to develop the GLP-1 part of the business which focuses on type-2 diabetes patients so that they don't have to inject insulin on a regular (daily) basis but can rather just inject the GLP-1 drug once a week.

The next step is using the knowledge obtained from prior activities to tackle the cause of type-2 diabetes, which is overweight/obesity, by developing drugs specifically targeting this problem. This could lead to rapid expansion in sales for the drugs coming from the obesity care segment. The interesting point is that the sales of the obesity care drugs won't necessarily affect the sales of the GLP-1 drugs. If an obese patient using a drug for weight loss achieves getting to a healthy body weight, this doesn't automatically mean that he/she won't suffer from type-2 diabetes anymore. Besides that, the possibility that he/she will fall back to their former weight is pretty high when the weight loss was only attributable to the temporary use of a weight loss drug.

GLP-1

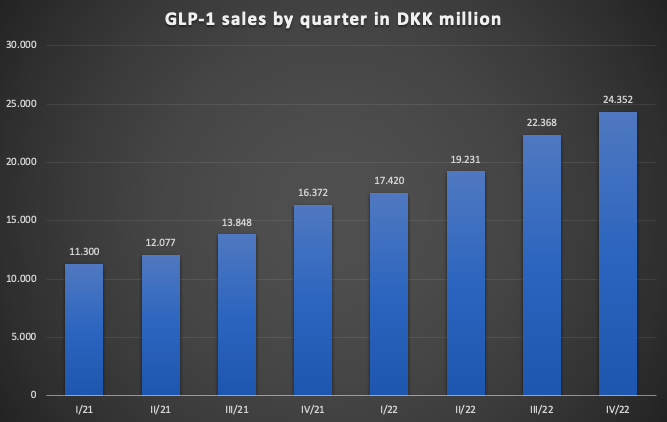

GLP-1 is used for type-2 diabetes patients. According to the EMA , Ozempic is used once weekly. In the case of Ozempic, the contained semaglutide helps the body to produce more insulin instead of having to inject insulin directly. To start, here is a chart showing the quarterly sales for the GLP-1 segment over the past 8 quarters:

GLP-1 sales per quarter (Company Annual/Quarterly Reports)

{kind=link}

The quarterly sales more than doubled from the first quarter of FY2021 to the recent fourth quarter of FY2022.

As for the market dynamics, newer products seem to be mainly focusing on the dosage form. While Ozempic is an injection pen, the newer GLP-1 drug Rybelsus comes in the form of tablets. This is more comfortable for patients because instead of injecting a pen (Ozempic) they can just opt to take a tablet daily. Rybelsus sales were DKK 50 million in FY2019, DKK 1,873 million in FY2020, DKK 4,838 million in FY2021 and DKK 11,299 million in FY2022, an astounding growth rate.

Now there are two questions to be made:

(1) How long can this rate of growth continue?

(2) Will Novo Nordisk lose market share in the future?

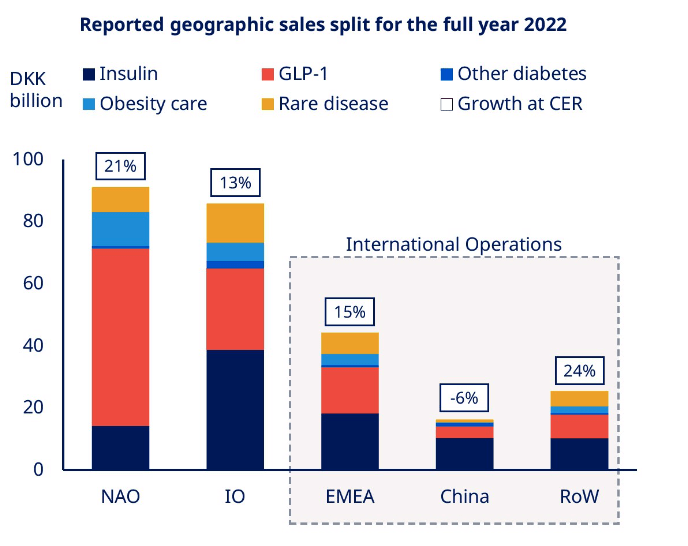

I will start with the first question and want to start with a chart from the recent 4th quarter earnings presentation :

Geographic sales split FY2022 (Company 4th quarter presentation)

{kind=link}

The main takeaway here is that the % of GLP-1 sales in North America ((NAO)) is way higher than in the rest of the world (IO=International Operations). I assume that North America is leading the charge and the international operations will follow with declining insulin sales and increasing GLP-1 sales. This might sound like a mediocre deal because one segment's sales would be swapped out with the other. This is not the case though as can be seen in the following chart from the capital markets day:

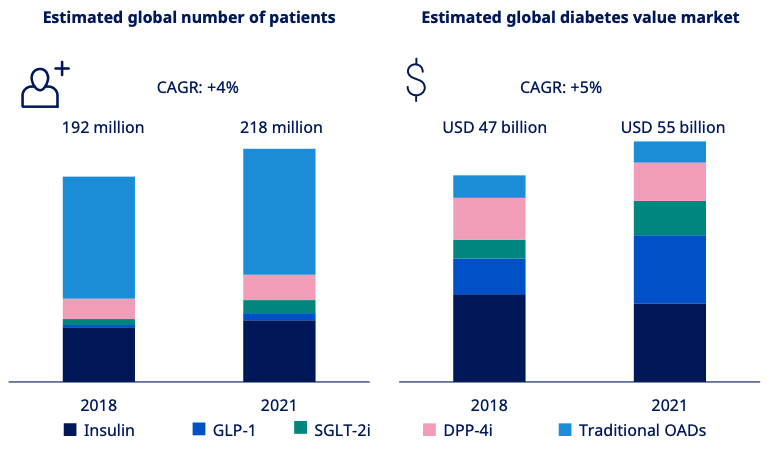

No. of patients vs. market value (Capital markets day 2022)

{kind=link}

The number of patients for GLP-1 is tiny compared to the estimated market value for the GLP-1 market. This leaves me to assume that there is much more runway for growth ahead of Novo Nordisk in the GLP-1 market.

The overall diabetes market value is estimated at $55 billion for FY2021. According to this SA news article , the type-2 diabetes market alone is expected to reach $136.2 billion by 2029. This would be a CAGR of 12% from the assumed 2021 levels. It is safe to say that there is much more room to grow in the future.

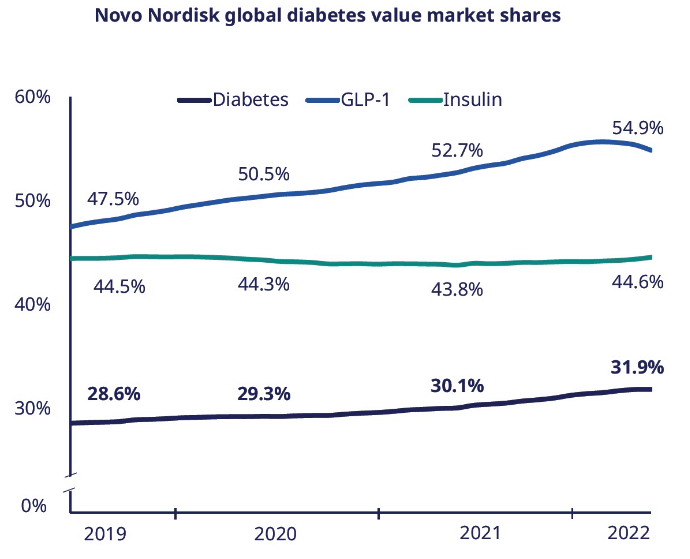

As for the second question regarding market share, Novo Nordisk stated in their capital markets day presentation (slide 8) that the diabetes market share grew from 27.5% in FY2017 to 30.3% in FY2021 and that they are aiming for one-third market share. In the recent 4th quarter FY2022 presentation, they stated that their market share came in at 31.9%, as can be seen in this snippet from the presentation:

Novo Nordisk market share (Company 4th quarter presentation)

{kind=link}

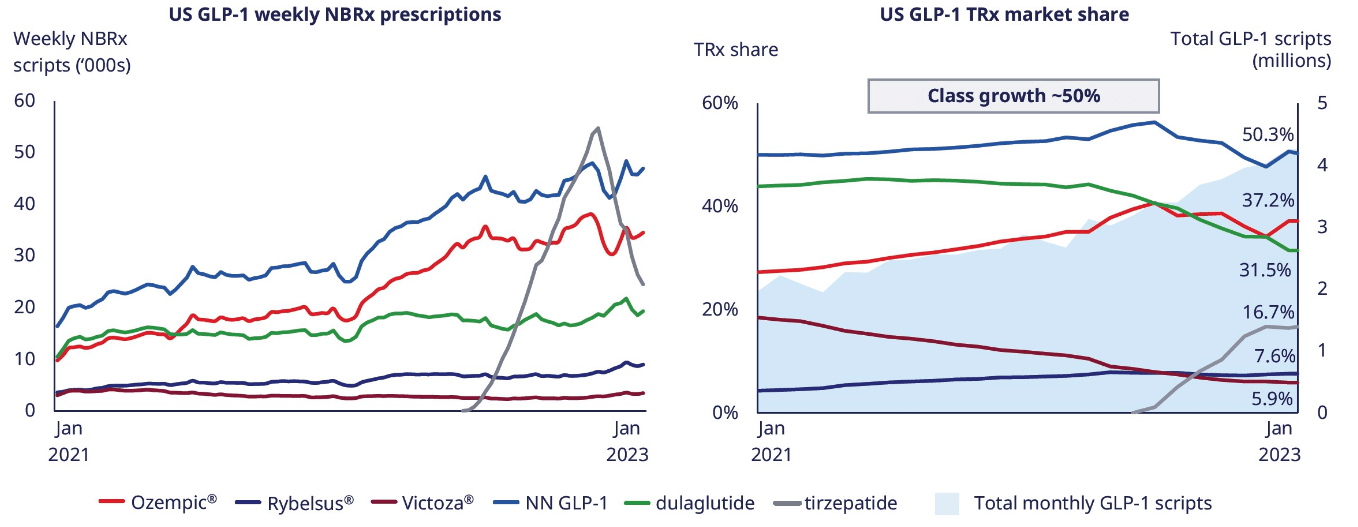

There is however one thing that concerns me which can be seen in the following chart showing GLP-1 prescriptions in the US from January 2021 to January 2023:

US GLP-1 weekly prescriptions (Company 4th quarter presentation)

{kind=link}

Dulaglutide and tirzepatide are GLP-1 drugs developed and marketed by Eli Lilly. Prescriptions for tirzepatide skyrocketed as soon as it was approved in the US. The positive is that this didn't have a big effect on the number of prescriptions for Novo Nordisk's top GLP-1 drugs Ozempic and Rybelsus but the negative is that it had an impact on the market share as can also be seen in the market share chart above. Prescriptions for tirzepatide have started to decline since November. However, this is something that has to be monitored in the future.

Obesity care

What is obesity? According to the World Health Organization (WHO) , a body mass index ((BMI)) over 25 is considered overweight and over 30 is obese. The WHO also states that from 1975 to 2016, the prevalence of overweight or obese children and adolescents aged 5–19 years increased more than four-fold from 4% to 18% globally. This SA news article doesn't paint a better picture for the future, estimating that diabetes rates in children could increase by up to 675% until 2060. The snippet from the capital markets day 2022 below shows the obesity prevalence for different regions all around the world:

Obesity prevalence in % for different regions (Capital markets day 2022)

The US and the Middle East are the regions with an obesity prevalence of over 30%, followed by many other developed countries like Europe, Russia, Australia and South America. In Asia and Africa, obesity seems to be no problem (at least for now).

According to Novo Nordisk, there are more than 650 million people with obesity. Only 2% of those (13 million) are treated with medication. This can have several reasons. People could just be happy with their bodies or decide to try losing weight on their own by focusing on nutrition and exercising. Some may just be ashamed and don't want to seek help from a professional. Creating awareness that obesity is treatable will be important to drive broader adoption by patients and physicians.

A plus is that obesity has a clear link to Novo Nordisk's existing business (remember the Philip A. Fisher quote earlier) because type-2 diabetes is, besides genetics, caused by obesity and inactivity. Physicians already prescribing GLP-1 to patients with type-2 diabetes might opt to introduce their patients to obesity care drugs, boosting sales and awareness in the process.

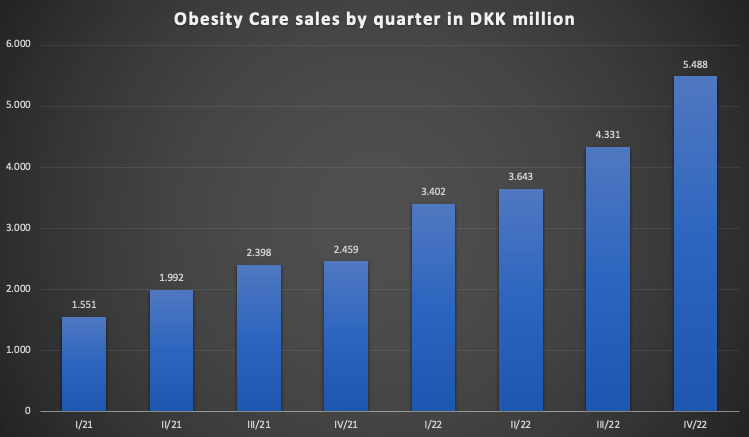

The chart below shows the quarterly obesity care sales over the past 8 quarters:

Obesity care sales by quarter (Company Annual/Quarterly Reports)

{kind=link}

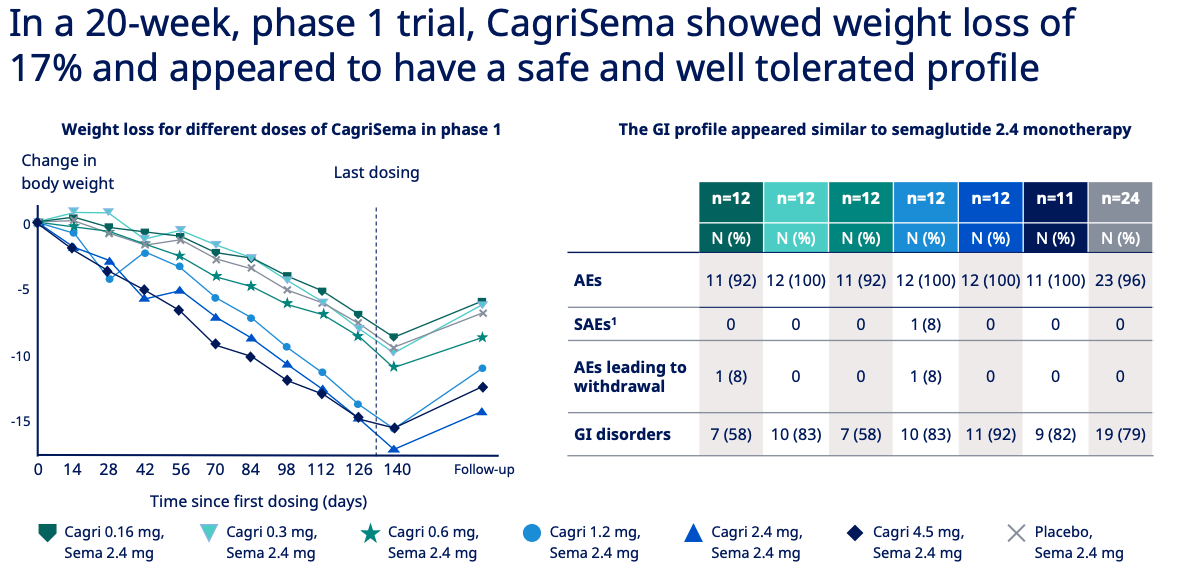

The quarterly sales nearly quadrupled from the first quarter of FY2021 to the recent fourth quarter of FY2022. Novo Nordisk has two marketed obesity care drugs at the moment, Saxenda and Wegovy. In clinical trials, Saxenda was able to achieve 5-10% weight loss while Wegovy achieved 15%. CagriSema, the drug that is in the pipeline right now, is supposed to achieve a weight loss of 20% or above. In a 20-week phase 1 trial, CagriSema showed weight loss of 17% at the high end, as can be seen in the slide from the capital markets day below:

CagriSema phase 1 trial overview (Capital markets day 2022)

{kind=link}

Another important point to keep in mind is that drug makers like Novo Nordisk and Eli Lilly need to convince insurance providers that covering the costs of a weight loss drug is (a) important for the health of the patient and (b) makes economic sense for the insurance provider. I think both of these points should not be problematic because regarding (a) most patients will probably suffer from type-2 diabetes and any chance of curing this should be taken and (b) the costs that are coming with type-2 diabetes and/or other after-effects of obesity will most likely be higher than the costs for a weight loss drug (assuming it helps to end the obesity for good).

My remaining concern is the same as the one for the GLP-1 segment: competition. Eli Lilly's tirzepatide achieved up to 22.5% weight loss over 72 weeks. Wegovy only achieved 15% weight loss over 68 weeks. While I think that the market size is big enough for two players, I am not sure why physicians should prescribe Wegovy instead of tirzepatide. The number of prescriptions for weight loss drugs will be an important metric to watch out for in the upcoming quarters.

Financials

I want to start this chapter by looking at the balance sheet. The first thing I always look at is the net debt/net cash. As of the end of FY2022, net debt stood at DKK 2.21 billion ($318 million). Novo Nordisk usually has a history of carrying a net cash position on the balance sheet. The financial position is still very healthy since net debt represents only around 4% of FY2022 Free Cash Flow ((FCF)).

One thing that caught my attention is the increase in intangible assets over the recent past years, as can be seen in the chart below (amount is in USD):

I already stated in the beginning that Novo Nordisk didn't carry any goodwill on the balance sheet in the past. According to the annual reports, the increase in intangible assets came from acquisitions. I am not sure if this might (at least partially) be goodwill which was accounted for as intangible assets. However, it doesn't matter because ROCE is still high.

My numbers for the ROCE are a bit different than the ones from Y-Charts. I guess this is a result of me subtracting net cash from the capital employed (if there is any net cash). My reasoning for doing this is that those net cash businesses could just pay out the cash as a dividend and would still operate on a zero-debt basis. Here are my numbers for the past few years:

| FY |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| ROCE |

| 156,8% |

| 163,4% |

| 128,38% |

| 113,9% |

| 94,33% |

| 74,92% |

| 61,74% |

| 62.18% |

Such a high ROCE indicates that Novo Nordisk is a business with a wide moat. Another indicator of this is the high EBIT margin of around 40% over the past decade, as can be seen in the following chart.

What concerns me a bit is the drop in ROCE over the past few years as a result of the aforementioned acquisitions. On the other hand, it is plausible that ROCE above 100% due to no M&A activity at all could hardly be sustained as the business grew bigger, so this is not that big of a problem as of now. Future M&A activity should be monitored closely though.

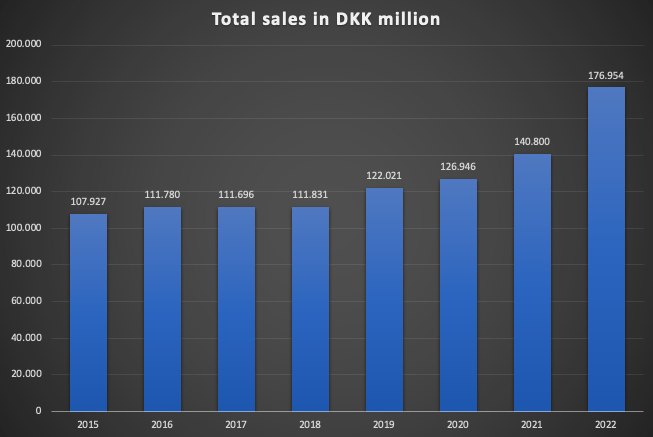

Looking at total sales growth over the last few years (chart below), we can see that sales were pretty much flat from FY2015 to FY2018 and only started to climb from FY2019 onwards.

Total sales FY2015-FY2022 (Company Annual/Quarterly Reports)

{kind=link}

As we can see in the next chart showing the PE ratio over the past decade, the valuation started to skyrocket from the moment sales started to grow again.

Valuation

As I am writing this, Novo Nordisk shares are trading at DKK 994 ($143.20). At the end of the recent 4th quarter of FY2022, there were 2,261,400,000 shares outstanding, resulting in a market capitalization of DKK 2,248 billion ($323.8 billion).

For FY2022, Novo Nordisk reported a net income of DKK 55,525 million ($7.999 billion), resulting in a current PE ratio of around 40. Cash conversion for Novo Nordisk has been around 92% over the past few years so the normalized free cash flow yield stands at around 2.27%. Both valuation metrics are very high.

DCF-valuation

Since I am not confident to lay out assumed growth rates for pharmaceutical companies, I will use a reverse DCF approach to gauge at what kind of rates Novo Nordisk would need to grow in the future to justify the current valuation. Because the high ROCE indicates a wide moat, I will assume 6% growth into perpetuity. The discount rate is 10% and the starting free cash flow per share (FY2022 basis) would be 2.27% x DKK 994 = DKK 22.59 ($3.25). Here are the results:

DCF valuation (moneychimp.com)

Novo Nordisk would need to grow 12.4% per year over the next decade and 6% into perpetuity thereafter. Now one might argue that we need to value it on a forward-looking basis, but even then the valuation is way too high in my opinion. Assuming the diabetes market would grow with 11% CAGR as I mentioned earlier in this article while factoring in that Novo Nordisk might lose some market share I would see it fairly valued at around DKK 800.00 ($115.25). Even assuming a growth CAGR of 11% for the next decade (in line with the assumed growth of the diabetes market), I get a value of DKK 893.00 ($128.65) per share.

When we look at the earlier PE chart we can see that Novo Nordisk was valued at between 20 and 30 times earnings in the past. With cash conversion at around 92%, this would come in line with what I would consider fair value. I would even consider paying a premium (closer to a PE of 30) because (a) Novo Nordisk looks like a high-quality company and (b) the PE multiples of the past few years were paid at a time when Novo Nordisk struggled to grow sales. The problem is that even when I am willing to pay a premium PE of 30 on a forward-looking basis, I am still only a buyer in the range around DKK 800.00 ($115.25).

Risks

I already laid out the main risk throughout this article: the competition from Eli Lilly's tirzepatide in the GLP-1 and the obesity care sector. These segments are supposed to drive Novo Nordisk's growth well into 2026. Prescriptions for tirzepatide in the GLP-1 space skyrocketed since it has been approved last year. This could cause market share losses for Novo Nordisk in the GLP-1 space. As for the obesity care segment, clinical trials showed that Eli Lilly's weight loss drug tirzepatide achieved better results than Wegovy (Novo Nordisk's main weight loss drug at the moment) in a similar timeframe. Future prescription development for Wegovy compared to competition drugs should be closely monitored. If the market gets any signals that Wegovy can't match Eli Lilly's tirzepatide regarding prescriptions there is a high possibility of the stock price rerating to the downside.

The other main risk of investing in Novo Nordisk is the high valuation and the general risk of multiple compression coming along with it. The stock has much of the supposed growth already priced in, leaving no margin of safety. According to my reverse DCF valuation, Novo Nordisk would need to grow 12.4% per year over the next decade, which is a higher growth rate than the supposed growth of the diabetes care market, and 6% into perpetuity thereafter. Such growth would only be possible by either (a) gaining market share or (b) entering new medication areas. I am not confident enough for (a) and have no idea how (b) could play out.

Conclusion

Novo Nordisk is a high-quality company and a market leader in the diabetes and obesity care space. The diabetes and obesity care market is expected to grow at a high rate in the future. The fact that Novo Nordisk is operating at ROCE of consistently above 60% and the high EBIT margins of around 40% show the wide moat of the business. Furthermore, the diabetes care business is pretty recession-proof, since patients can't just stop taking their medication.

Nevertheless, I rate Novo Nordisk a hold because the valuation seems high and leaves no margin of safety. Another reason for my hold rating is that I see a possible threat from the competition, specifically Eli Lilly.

For further details see:

Novo Nordisk: Attractive Market But Likely No Margin Of Safety