FSNUF - Novo Nordisk: Denmark's Coca-Cola

2023-07-25 06:22:00 ET

Summary

- Denmark's Novo Nordisk is 100 years old this year, with fundamentals as strong as ever facing a population with record rates of obesity and diabetes.

- I almost wish NVO stock would decline by 50% due to a collapse in the demand for insulin, but that seems unlikely to happen.

- That said, this stock is very expensive at over 30x forward earnings and a yield of less than 1.5%, so I don't have appetite to buy more here.

- Rather, I'd look at buying longer-term call spreads, perhaps financed by writing out of the money puts.

One theme I'm especially keen on maintaining a "permanent" allocation to, at least until I see a major change in global trends, are companies that serve a global population that continues to get older, fatter, and more diabetic. More of my focus in this area over the past year has been on dialysis machines and dialysis clinics, especially those run by Germany's Fresenius SE & Co. ( FSNUY ), because that company meets my criteria of yield and growth well enough for me to keep buying more. This time though, I wanted to review a smaller position I've long held as a "wonderful but expensive" business just north of Germany's border, Denmark's Novo Nordisk A/S ( NVO ), which celebrates its 100th anniversary this year . In this article, I will briefly review NVO's stellar historical performance, why I keep owning the stock despite wishing it would fall, and perhaps more importantly, what I am doing now that I consider it too expensive to buy more.

NVO's Stellar Historical Returns

The performance chart of NVO, going as far back as YCharts has data, is about as close to perfection as any long term stock investor could dream of. As the chart below shows, $10,000 invested in this company back in 1981, after a lost decade in the 1980s, would have still averaged a compound annual growth rate of 17.4%, turning that $10,000 into $8.9 million over that 42 year period. While even I often hate these "if you bought X this many years ago..." examples, what makes it hard for me to put this chart down is how steadily NVO managed to sustain these returns decade after decade through the 1990s, 2000s, and 2010s, and still seems to be on track in the 2020s. In other words, this seems like a stock that has been so consistently good that investors could have bought it almost anytime over the past 42 years and still be very happy a decade or two later. The $17.8 million question for NVO investors today, though, is how well positioned these shares are to continue this phenomenal compound rate of return, which at 17.44% per year, means doubling an NVO shareholder's investment again in another 4-5 years.

In the title of this article, I called NVO "Denmark's Coca-Cola" because of this exceptional record of compounding a high rate of return to investors over many decades. On the same thread, I might also say, only half-jokingly, that Coca-Cola's (KO) decades of returns came from selling something addictive that can give its customers diabetes, so it makes sense that another company would just as profitably provide treatments to all those Coca-Cola drinkers a few decades later.

I last wrote about Coca-Cola in January 2022 , where I focused on how even this wonderful business can run into a "lost decade" for investors, so my key concern today is assessing how likely it is that NVO might have its first "lost decade" since the 1980s from today's valuations.

Why I Wish NVO Would Fall By 50% or More

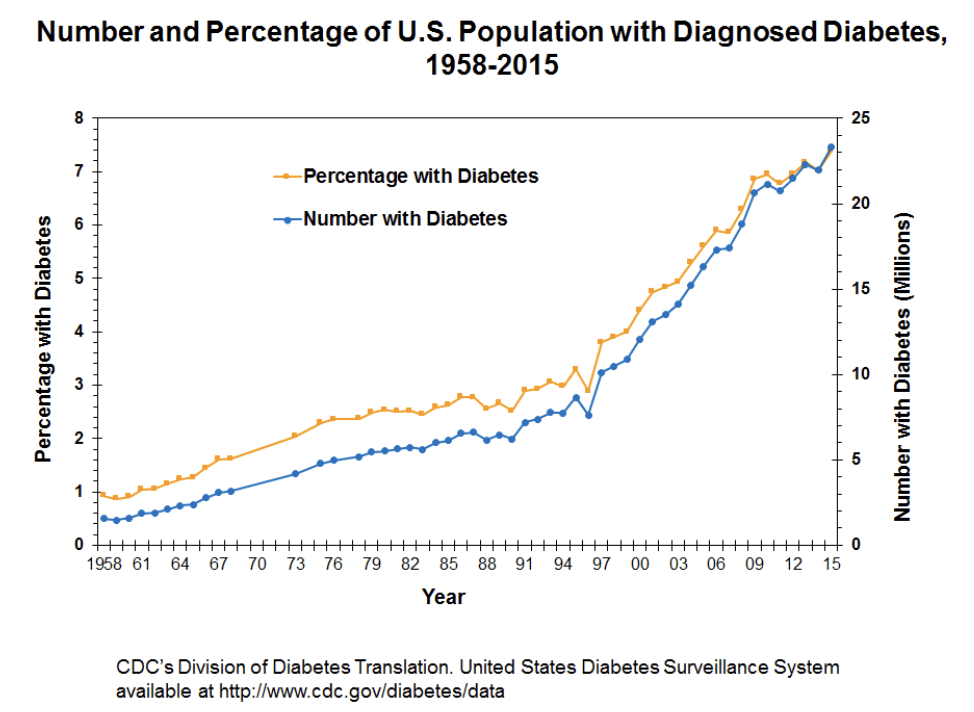

One reason it might make sense to pay up for a business like NVO's is that it has done well, and is likely to continue doing well, because of a dismal global trend: the world population is getting older, and more of those people are ageing with diabetes. The demographic trend of the 20th century could broadly be summarised as the world's greatest boom, where birth rates remained high as mortality rates plummeted and life expectancy increased. The 21st century, on the other hand, starts with birth rates that are low and still declining, with two-thirds of the world living in a region where birth rates aren't even high enough to replace today's population . While it is extremely good news that we are far less likely than a century ago to die as children or youth from tuberculosis, diarrhea, small pox, we are now far more likely to live into our 70s when other diseases like cancer or diabetes are bigger concerns. It is also good news that many more people are also ageing with more money, so will likely be ready to spend more of that money on medical treatment. The below chart is from the US CDC , and shows the rise in both diabetes numbers and prevalence rates in the US population, but I naturally extrapolate this to populations like India's, to get an idea of what the total addressable market for diabetes treatments is likely to be over the next decade.

{kind=link}

When I say that I wish my investments in dialysis clinics and NVO would fall by at least 50%, I am imagining a scenario where these diabetes rates have levelled off, and the current generation of 40-60 year olds stops eating sugar and exercises enough to significantly reduce the rates of diabetes. While I am in the age range that I focus much of my own diet and exercise decision making on trying to avoid ever having to need NVO's diabetes care products, I simply see it as too unlikely that global demand for these products will slow anytime in my lifetime.

Rather, I see two other main "cataclysmic risk" scenarios for NVO, namely:

- Governments see diabetes care as so critical to their national welfare that they either further cap prices or try and nationalise NVO, or

- A competitor comes up with much cheaper or longer-lasting treatments that replace NVO's.

Given these trends and risk scenarios, in the next section I want to quickly run some numbers on what it would take for NVO to double again in another 4-5 years.

Model: NVO's Future Expected Rate of Return

Since NVO pays a steady dividend which it has steadily increased year by year, I prefer to estimate its future rate of return using a purely dividend-based model. This model combines three components:

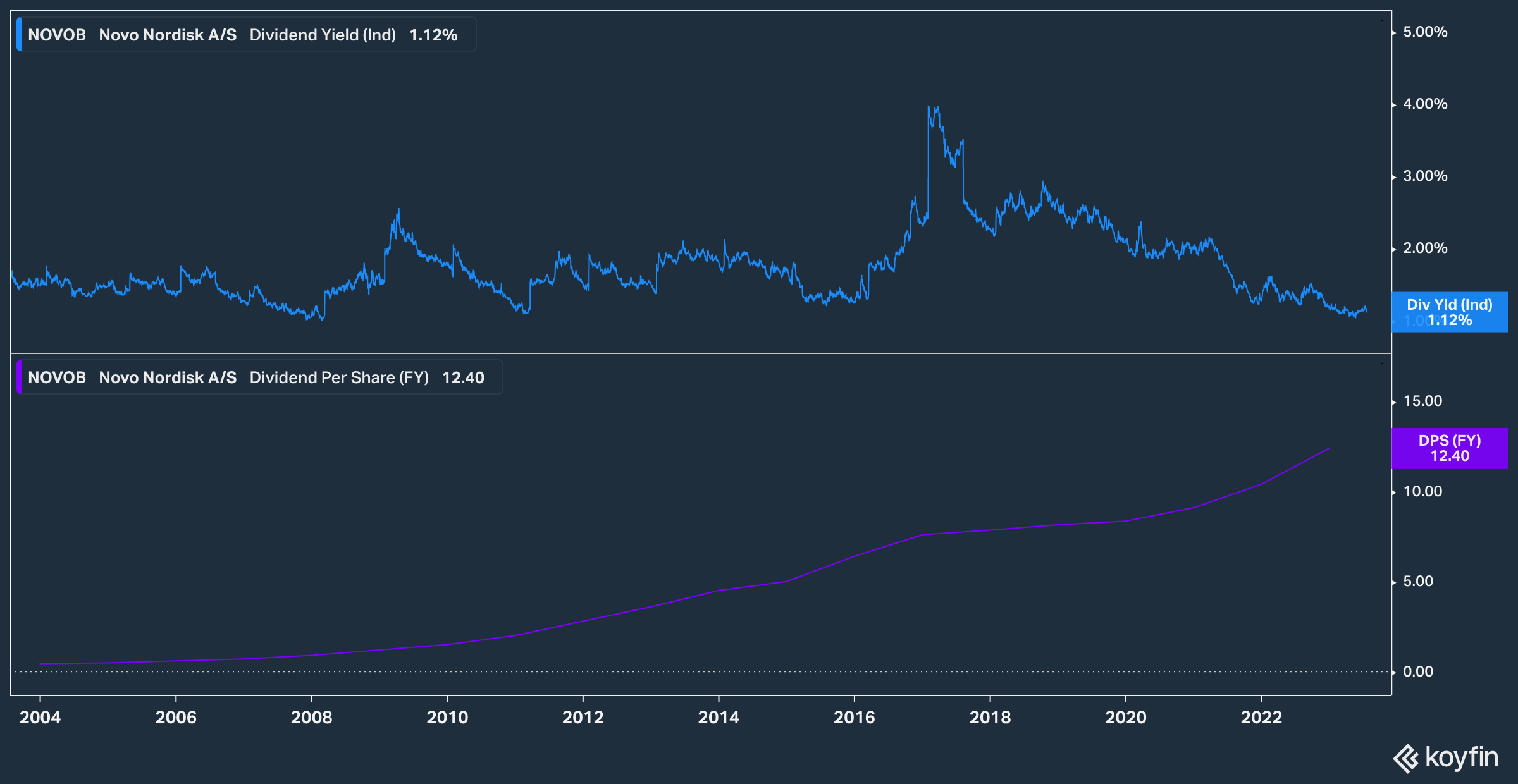

- Dividend yield, which is currently only around 1.1% (based on the DKK 8.15/share dividend paid in March, plus an estimate that the August interim dividend will be DKK 4.25/share like last year, divided by the last price of DKK 1,109.20/share), plus

- Dividend growth, which as a baseline we can assume to be around the 13% per year rate seen from the DKK 3.60 paid in March 2013 to the DKK 12.40/share paid in the 12 months ending March 2023, plus

- Revaluation due to change in yield, also known as "speculative return".

The low initial yield of just 1.1% means that NVO shares could decline by 50% simply by the market yield rising to 2.2% with no change in the dividend, and the MAIN reason I'm not rating NVO a buy is because its current yield is too far on the low end of its historical range. While the below chart shows that NVO's yield has only risen much above 2% in the 2017-2019 period, which in hindsight was the last best time to buy, but from these levels, it seems more likely the yield may rise back up to around 1.5% than it is to fall to 0.5%, around the current yield of Apple (AAPL).

{kind=link}

If we make the conservative assumption that NVO's dividend yield will be back around 2% 10 years from now, and that the dividend kept growing at 13% per year to be around DKK 42.7 per share by 2033, that implies a share price of around DKK 2,000/share, or about 6% per year appreciation from current levels. That plus the 1.1% initial dividend yield implies an expected rate of return around 7% per year based on these assumptions.

That leaves a critical variable in this rate of return assumption being how likely it is that NVO can sustain that 13% annual dividend growth rate for the next decade. Here, we look to NVO's impressive rates of growth on its Seeking Alpha Growth Ratings Page , which shows impressive 20%+ growth rates, but also temper this with a more conservative growth estimate based on the ~6-9% revenue growth rates seen in some of its slower decades in the past. Even with these more conservative growth estimates, we should also note that in each of the past several years, as seen through the dividend link above, NVO has been spending about as much on share repurchases as on dividends. This means that even a lower growth rate will likely be shared by an annually shrinking number of shares, making it easier to support high returns as we've seen in the case of McDonald's (MCD). Note that at the most conservative end of this range, which assumes only a 6% annual growth rate, which would raise the dividend to DKK 22.20 by 2033, would mean that a rise in the dividend yield to 2% would put the price of NVO shares right where they are today, implying a lost decade with a growth rate of 6% or lower.

Conclusion: Option Trades I'm Considering

Perhaps even more than with Apple, I see a high likelihood that NVO can continue compounding at a double-digit growth rate, and keep its yield below 1.5% so that this stock is better holding than selling, though I find it way too expensive to buy more at these levels. For accounts which haven't bought NVO yet, but for which I'd like to add some risk managed exposure to its next 20% upside, I would instead consider the following option trade: buying the January 2025 180-200 call spread, which I would aim to buy at a price of 8 points or lower. This trade would more than double my $800 per spread with a $2000 payoff if NVO finishes above $200/share 18 months from now, with my downside risk limited to the $800 premium, whether NVO stays where it is now or falls by 50%. 200 is a little more than 22% above its current share price, meaning this would capture a ~15% annual rate of return if NVO manages to sustain that over the next 18 months, but I would still lose my premium even if NVO rises only to the 180 lower strike. In theory, I should also consider buying some protective puts on my existing shares, but I do want to remain a shareholder even on my small position, and use this option trade to limit my risk to any additional exposure I'm adding. For investors with appetite for some downside risk on NVO, who'd rather not have an $800 premium waste away if the share price stays below $180, it may be possible to cover the cost of this spread by selling the January 2025 130 or 135 strike put, which allows a significant buffer from the current share price above 160.

For further details see:

Novo Nordisk: Denmark's Coca-Cola