NONOF - Novo Nordisk: Enjoying The Tailwinds Of A Growing Market

2024-01-12 00:25:11 ET

Summary

- Novo Nordisk is the market leader of the fast-growing obesity care industry, which is expected to grow above 20% CAGR until 2030.

- The company raised three times its guidance during 2023, driven by a 481% growth in Wegovy's revenues.

- The company is increasing its production facilities to meet the demand and has already committed over $11.8B until 2029.

- Novo Nordisk has exceeded my expectations during the last year, but I still consider it undervalued by 18% compared to its fair price of $126 per share.

Investment Thesis In A Nutshell

Novo Nordisk ( OTCPK:NONOF ) is the market leader in an industry with strong entry barriers, pricing power, and low elasticity of demand.

The company is enjoying the long term tailwinds of an increasing population with diabetes and obesity related diseases, which has allowed for a significant reinvestment rate in organic growth, acquisitions, and production facility expansion.

Its high returns on invested capital, recurring revenues, low debt, and excellent capital allocation make it the kind of company I want to own not just when the market favors it, as has recently happened exceeding my previous article expectations, but for the long term.

Company Overview

Novo Nordisk is a pharmaceutical company with a leading positions within diabetes and obesity care. Due to the recent increase in demand for its weight-loss drug Wegovy, which has sent its earnings to record highs, it has become the most valuable business in Europe with a $460B market cap.

Novo Nordisk Q3 2023 Presentation

{kind=link}

The insulin market is highly concentrated and only three companies -Novo Nordisk, Sanofi ( SNY ), and Eli Lilly ( LLY )- control over 90 percent of the global market, allowing them to enjoy high margins, returns on capital, and pricing power.

Novo Nordisk's main products and their contribution to revenues are:

- Injectable GLP-1: Ozempic and Victoza (43.6%)

- Oral semaglutide: Rybelsus (7.7%)

- Insulin products (22.8%)

- Obesity care: Wegovy and Saxenda (18.3%)

- Rare disease (7.6%)

Although there are very few insulin products that have patent protection on the compound itself, the majority of insulin products still have patent protection on the pens and other devices that deliver the dose of insulin.

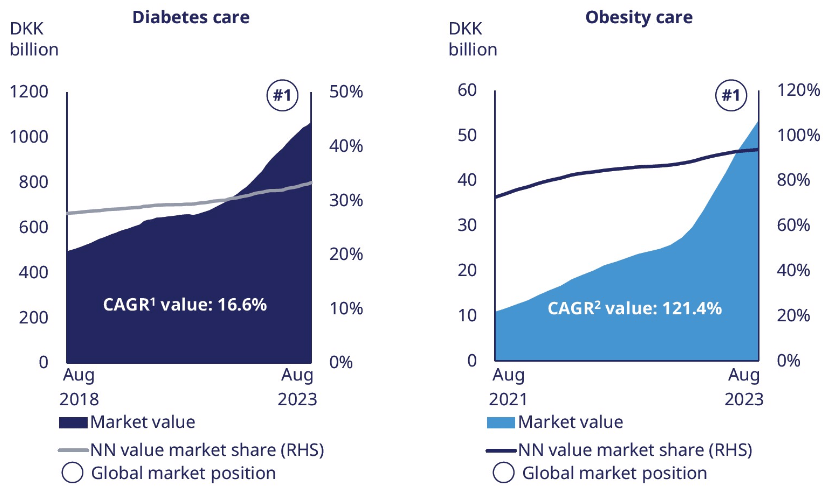

This market structure and the entry barriers has allowed Novo Nordisk to increase its revenues by 10.5% CAGR over the last 10 years. Since it supplies a first necessity product with low demand elasticity, operating margins are over 43% and returns on invested capital are at an astonishing 32%.

On the recent years, Novo Nordisk has been increasing its focus in the obesity segment, which only generated 2% of revenues in 2017 and currently makes over 18% of total revenue , exceeding investors' expectations.

Exceeding Expectations

In my first Novo Nordisk article, I was expecting 25% growth in revenues for 2023 and 15% in 2024. The company has been exceeding my expectations and the stock has already reached the previous fair price ($186 per share, $93 after the 2:1 split).

After rising the guidance three times during the year (April, August and October), revenue growth is expected to be at 29% for the full 2023 (34% at CER) and net income margins above 36% (compared to 31.4% in 2022).

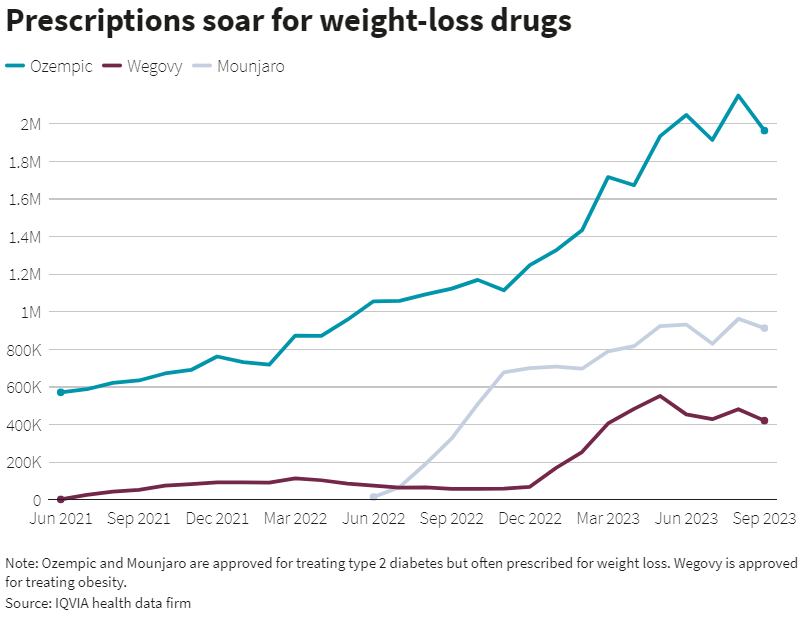

The impressive results the company has been able to deliver during the year has been primarily due to a higher than expected revenues in injectable GLP-1, with Ozempic revenues growing by 53% during the first 9 months, and the obesity care segment growing by 167% during the same period, mainly driven by a 481% growth in Wegovy's revenues.

Ozempic generates almost 40% of total revenues, so an increase of demand has a significant impact on the overall results. While Wegovy revenues represented a small percentage during last year due to supply issues (2.9%), the company has been expanding its production facilities, and it can currently supply the full U.S. demand for the 2.4mg dose (still experiencing issues to meet the 1.7mg demand), increasing the contribution to 13% of total revenues during 2023.

From a geographic perspective, GLP-1 diabetes products grew at faster rates outside the U.S., mainly driven by the demand in China (80% revenue growth), while the growth on obesity products was mainly driven by the U.S., which is the main market for this segment (79% of obesity revenues) and where the company has put more efforts on meeting the increasing demand.

In Europe, the company has only launched Wegovy in Germany, the U.K., Denmark, Norway, and Iceland, so there is still significant growth ahead.

Source: Reuters (Data from IQVIA)

{kind=link}

On top of reaching during 2023 the sales expected for 2025 on the obesity segment ($3.7B), the company released its results from the SELECT cardiovascular trial with a statistically significant result and a 20% reduction in major adverse cardiovascular events compared to placebo, which opens a new market for Novo Nordisk.

These results come at a perfect time given the recent approval by the FDA for Eli Lilly's Zepbound injection for obesity treatment, which has shown better results than Wegovy (although the latter can be prescribed to treating pediatric patients).

The full SELECT results were presented at the American Heart Association Congress in November, and a label indication expansion for Wegovy has been filed. The FDA gave a priority review and the expansion could be approved by May 2024.

While it is hard to estimate an accurate total addressable market given the significant overlap between diabetes, obesity, and cardiovascular diseases, the label expansion could strengthen Novo Nordisk's leading market position and put pressure on insurance companies to cover Wegovy.

Source: Novo Nordisk Q3 2023 Investor Presentation

Production Expansion

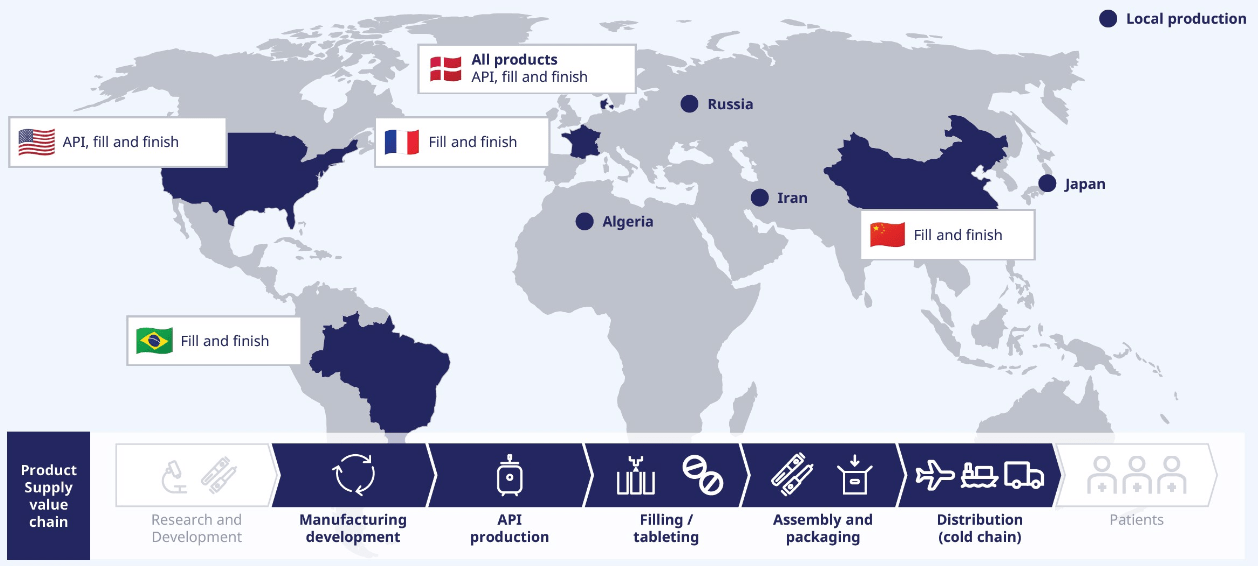

One of the main issues the company has faced over the last years has been the disruption in the supply chain, which combined with a meteoric increase in demand has caused a shortage of certain products ( mainly Wegovy and Ozempic).

To solve this issue, Novo Nordisk started last year a restructuring of the supply chain and has been gradually investing in expanding its production capacity.

Source: Novo Nordisk Q3 2023 Investor Presentation

{kind=link}

As shown in the image above, Novo Nordisk has some local production facilities to supply the local markets (Algeria, Russia, Iran, Japan), and the biggest production sites for export are located in Denmark, the U.S., Brazil, France, and China.

While the company has spent $1.1B per year on average in Capex during the last decade, of which half has been growth capex, during the first nine months of 2023 the growth capex has increased to $1.48B and is expected to reach $2.3B for the full year.

Source: Author

To achieve higher production levels, the company has already announced a series of expansions and acquisitions that will go through 2029.

In 2022, Novo Nordisk announced the expansion of the clinical manufacturing facilities in Denmark for $800M, which will be completed in 2024.

In June 2023 , the company started the construction of a new manufacturing plant in Hillerød (Denmark) to expand the existing Active Pharmaceutical Ingredient ((API)) production by early 2029, which will cost $2.35B.

Recently, the company has announced it will acquire Alkermes's development and manufacturing facility in Ireland for $92.5M by mid-2024, and the expansion of the French manufacturing site, which will be finalized between 2026 and 2028 for a total investment of $2.35B and will double the production capacity of the site.

But the biggest announcement has been the $6.2B that will be invested in expanding one of Novo Nordisk's largest facilities (Kalundborg, Denmark), which will be gradually finalized between 2025 and 2029, adding 800 new jobs to the current 4,400 employees that work at the location.

Acquisitions

On top of the organic growth, the ~0.85% dividend yield, and the almost 2% annual share buyback (average last 10 years), Novo Nordisk started strategically acquiring smaller companies and molecules in 2021.

While it deployed $2.8B in acquisitions during 2021, and $1.01B in 2022, during 2023 the company has acquired two companies and the ocedurenone molecule from KBP Biosciences.

The acquisition of ocedurenone for the treatment of cardiovascular and kidney disease supports the aspiration of establishing a presence in other serious chronic diseases.

The molecule has been acquired for $1.3B, is currently in phase 3 trial for patients with hypertension and advanced kidney disease, and will also be included in Novo Nordisk's pipeline since it will complement some of its current programs.

The two companies acquired during 2023 have been Inversago Pharma ($1.07B), which has developed receptor-based therapies for the treatment of obesity, diabetes, and metabolic disorders, and Biocorp ($168M), a small French medical device manufacturer with $12.8M in revenues during 2022.

The Biocorp acquisition was mainly driven by the sensor developed by the French company that can be attached to insulin injection pens to keep precise real-time track of the doses injected.

The capital deployed into acquisitions during 2023 has been at $2.54B, and as long as the company is not overpaying, I believe this is an outstanding capital allocation given the R&D costs could be higher, it strengthens Novo Nordisk's competitive position, brings synergies to the existing businesses, and opens new market opportunities.

Valuation

While it is easy to see that the company has been exceeding expectations and has taken the right steps to continue gaining market share in the diabetes segment, the main question is if the market hasn't priced yet the future growth.

{kind=link}

Taking into account that there are many countries where Wegovy has not been released yet, and its competitors will not be able to deliver similar results to the SELECT trial at least until 2027, I expect revenues to continue growing above 20% in 2024.

For the upcoming years, in a base case scenario, I expect a slight decline in revenue growth since I am not accounting for a positive result in Cagrisema trial that is expected to be completed by 2025-2026 (although phase 2 showed an average of 15.6% bodyweight reduction), or the OASIS trial for oral semaglutide.

In a base case scenario, I expect a decrease in market share for the obesity segment in favor of Eli Lilly and its Zepbound drug.

{kind=link}

I expect an increase in capital expenditures given the already committed production facilities expansion. The relatively low discount rate is based on the fact that Novo Nordisk's average interest rate paid on debt is under 1% and its low beta (0.20x).

Readers will note that the net debt I indicated is significantly higher than the one provided by most financial data sources, this is because I don't consider it to be fair to include the increase in cash and short-term investments, but not include the increase in rebates since they are related. I use a conservative assumption and account for the pending rebates (generally settled after 150 days) as debt.

From a 3% growth in perpetuity based on inflation plus population increase (arguably I could use a higher rate given the faster increase in population with diabetes and obesity), and a 28x last twelve months free cash flow multiple, my average fair price is $126 per share, assuming a 2% annual decrease in share count.

Risks

From a financial perspective, I don't see any significant short-term risk for Novo Nordisk, since it has a low debt compared to its strong cash flows from operations.

The major risk I see for the short term would be the FDA or the European Medicines Agency (EMEA) not approving the label expansion for Wegovy to include cardiovascular diseases. If Novo Nordisk is not able to continue improving its obesity products, its market share will drop over the next years, given the 5% to 6% better results in weight loss for Zepbound compared to Wegovy.

Although Novo Nordisk could see its market share in the obesity segment reduced as competition increases, the overall market is expected to grow at a fast pace, reaching between $44B (Bloomberg projections ) to $100B (Goldman Sachs (GS) projections ) by 2030 and growing above 20% CAGR.

So we are only scratching the surface of the obesity market. The biggest challenge we have is not competition, it's actually awareness of obesity as a chronic disease, the need for medical intervention, the value it has on your health system. So I welcome competition in actually driving and unlocking that market.

Source: Lars Jorgensen ((CEO)), J.P. Morgan 42nd Annual Healthcare Conference, January 2024.

In terms of the supply chain and the ability to meet the demand, which has been the main issue over the last few years, I don't see it as a major short-term risk, since the company has taken the right steps to improve in that area.

Looking from a long-term perspective, the primary risks are:

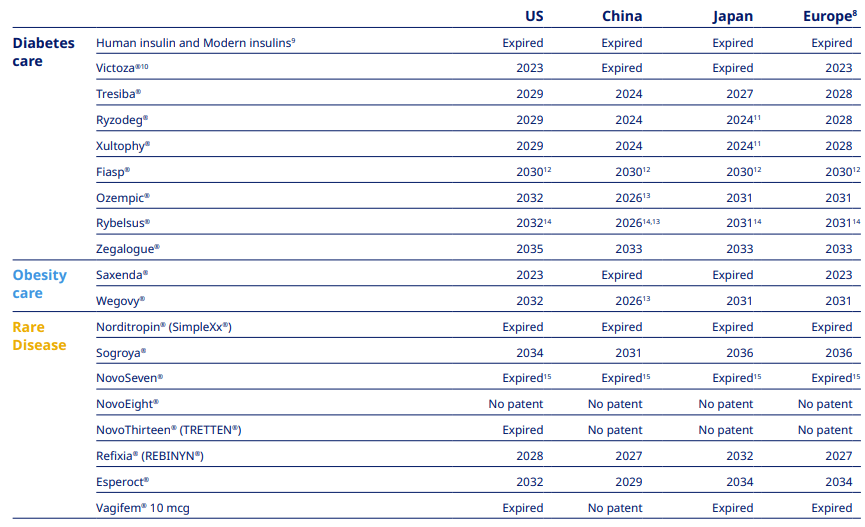

- Lack of innovation and product development: this is heavily dependent on the amount spent on R&D and its effectiveness. The size of the company creates economies of scale that make it difficult for smaller companies to compete against Novo Nordisk's R&D budget, but it is crucial the company uses its resources efficiently and continues developing new products.

Source: Novo Nordisk Q3 2023 Investor Presentation

{kind=link}

- Regulatory and legislation risks: the pharma industry operates under significant regulatory scrutiny, with controls on testing, manufacturing, distribution, and drug approvals by government agencies. On one side it makes it difficult for new competitors to enter the market, but also poses a significant risk if Novo Nordisk fails to comply with any regulation or procedure.

- Unknown side effects: Some of the drugs on the market have been approved recently, and although they have been tested, some unknown side effects could be discovered. For instance, obesity drugs are being scrutinized by U.S. and European regulators due to potential links to suicidal thoughts, which if confirmed, would have a negative effect on revenues and reputation.

- Market overestimating the addressable market: Given the recent growth in revenues for the obesity segment, I don't believe the market is overestimating the potential addressable market and I agree with Bloomberg's projections for the upcoming years. However, if the growth rates were to decline, the average fair price for Novo Nordisk would be significantly affected and the current valuation wouldn't be justified.

Conclusion

Novo Nordisk is enjoying the tailwinds from a fast-growing market and holds a privileged position as the market leader. While I anticipated the company to sustain its long-term performance, it has exceeded my expectations significantly during the last year.

The major problem the company is facing is having too much demand, which is the dream of every business, and the right steps have been taken towards increasing production.

Notably, its reinvestment rate in organic growth has increased, is paying less than 1% for its debt, and is returning the excess capital to shareholders through share buybacks and dividends.

Despite the 51% growth in the share price over the last year, I view the stock as undervalue, increasing my fair price to $126 per share and rating it as a buy.

For further details see:

Novo Nordisk: Enjoying The Tailwinds Of A Growing Market