NONOF - Novo Nordisk: Super Focused Pharma Company For The Long Run

2023-08-31 11:17:22 ET

Summary

- Novo Nordisk is a high-quality pharmaceutical company with a unique ownership structure, controlled by a charitable foundation.

- The company specializes in diabetes and obesity treatments, with a focus on insulin and GLP-1 analogues.

- Despite a temporary slowdown in recent years, Novo Nordisk is back on track for strong growth and has the potential for further diversification in the future.

- While I consider its current share price overvalued for a short term investment, it is an attractive long term investment with an investing horizon of 10 years or more.

Editor's note: Seeking Alpha is proud to welcome GS Value Research as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Novo Nordisk ( NVO , NONOF ) is one of the most qualitative big pharma companies globally. It specializes in a niche area of diabetes, obesity, and closely related fields. Its structure allows them to operate in their own way, ignoring common trends in pharmaceutical industry, operating with a very long-term horizon and a deeply specializing scientific knowledge. While such a setting mostly bewilders outsiders, in practice it generates superior and very stable long-term returns.

Company

Why do many regard Novo Nordisk as an unusual pharmaceutical company ? The company is based near Copenhagen, Denmark. It is controlled and partially owned by a majority shareholder Novo Holdings , which is owned by Novo Nordisk Foundation, a charitable foundation focusing on medical treatment and research. This gives Novo Nordisk a unique position among its peers, as it shields the company from potential hostile takeovers, and subsequently gives its scientists a possibility for a very long-term research horizon. This is a unique asset in the pharmaceutical environment, as scientific knowledge undisturbedly accumulates through generations of scientific work without the pressure of an instant delivery. The ownership structure also shields the company against diworsification as was demanded by consultancies in the period leading to the temporary slowdown in the years of 2017-2019. These days the trend in the pharma arena is that the main growth driver is external acquisition of competitors (M&A) and/or individual products in the form of in-licenses. In stark contrast to that, Novo Nordisk is the only big pharmaceutical company that until very recently was growing 100% organically . And despite that, Novo is not overspending on its R&D in comparison to its peers, and at the same time it is able to generate one of the highest revenues per new molecular entity of all big pharma companies.

Novo Nordisk is a 100-year-old company that until recently almost exclusively focused on diabetes treatment. As such, the company has almost no direct peers. The closest peer is Eli Lilly (LLY) which generates about half of its business from the diabetes area. Until 2019, Novo Nordisk, Eli Lilly and Sanofi (SNY) were considered as three largest global manufacturers of insulin accounting for over 90% of the market in volume and value, but as Sanofi exited research from diabetes in 2019, this gave Novo further opportunity to grow. There are other companies in the diabetes field, however they are focusing mostly on small molecules (not insulin) like Merck (MRK), J&J (JNJ), AstraZeneca (AZN), Boehringer Ingelheim, Takeda (TAK) and several other players.

Diabetes Treatment

Diabetes can be treated by several drugs. In the initial stage of Type 2 diabetes mellitus, no treatment is needed, only life adjustments as weight reduction, exercise, and dietary modification are required. First stage of Type 2 diabetes lasts 0-5 years, in which a diet plus metformin is prescribed. In the second stage of the disease (lasting 5-15 years), a combination therapy of several oral agents or the addition of incretin mimetics (also known as GLP-1) is required. In the most severe form of the disease, occurring 15 years after the onset of the disease, insulin treatment is needed.

Most oral agents for treatment of diabetes are small molecules like metformin. Those molecules face a rapid competition and value erosion by generic drugs right after their patent protection expires. The barrier to entry for those molecules is low. On the other hand, insulin and human insulin analogs are complex polypeptide hormone molecules manufactured by recombinant DNA technology in yeast and further chemical modifications, establishing a high barrier to entry. A special class of molecules are incretin mimetics also called GLP-1 analogues. Those molecules are also complex, yet a bit less than insulin and its analogues. They can be manufactured by two routes. First route is by recombinant DNA technology, which is complex but cost effective. The other possible route is manufacturing by solid-phase synthesis method, which is somehow less complicated, but also less cost-effective. The barrier to entry for those molecules is medium-high.

From Diabetes To Obesity And Beyond

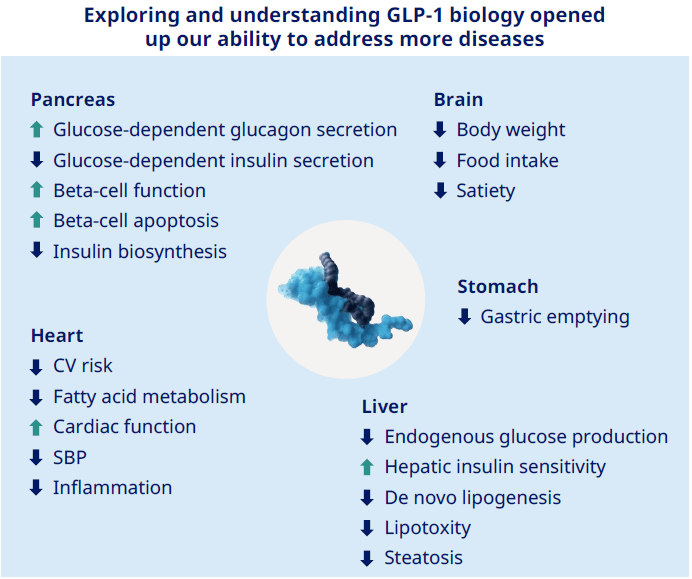

For the first 75 years of the company's existence, Novo Nordisk was growing pretty much exclusively by developing and improving insulin and insulin human analogues. In the first part of this period, focus was mostly on optimization of production and purification methods of insulin. When production and purification methods reached optimum levels and further growth in this area became difficult, focus switched to different human insulin analogues. Several types of insulin like insulin aspart, NPH insulin, insulin detemir, insulin deglutec and insulin iodec all have distinct onset speed and duration time, which is important in different diabetes management approaches. To go beyond insulin and its analogues and to find new growth drivers, about 25 years ago, Novo Nordisk started to explore a related molecule class of incretin mimetics (also called GLP-1 analogues). This led to the research of liraglutide and later to semaglutide, current flagship molecule of Novo Nordisk. During this research they noticed that laboratory mice started losing weight. While their products Ozempic and Rybelsus are registered for treating diabetes, product Wegovy is registered for treating obesity. By the very long-term in-house development orientation, Novo Nordisk was able to seamlessly diversify from diabetes to obesity treatment.

Another important breakthrough point for Novo Nordisk was the research of oral administration routes of semaglutide. It needs to be understood that while semaglutide is a complicated molecule, its classical administration route is quite simple from the scientific point of view - one prepares a solution and puts it into the injection pen. Patient then only injects the dose under the skin. No further scientific complications arise. However, a different thing is to formulate the molecule into oral formulation like tablets, not requiring injection. This comes from the chemical properties of semaglutide, which very quickly degrades in the stomach and gut, and in addition is absorbed into the bloodstream very poorly. From time to time, I have an opportunity to speak to scientists in the pharmaceutical field. I can tell you that no scientist in the world except from Novo Nordisk ever believed that it would be possible to formulate GLP-1s into oral products. I had a personal discussion with a top scientist of a top diabetes competing company as late as in 2013 and the person only waved by hand. This is amazing as only 5 years later Novo Nordisk PIONEER 1 phase 3a clinical study was successfully completed. In the area of basic biochemistry research, period of 5 years can be regarded as a blink of an eye. However, a very long-term and focused research of the company led to the product Rybelsus, first-ever oral formulation (as tablets) of a peptide molecule. Yes, the commercial name Rybelsus is spot-on - the molecule was rebelling hard against being formulated into tablets for a long time.

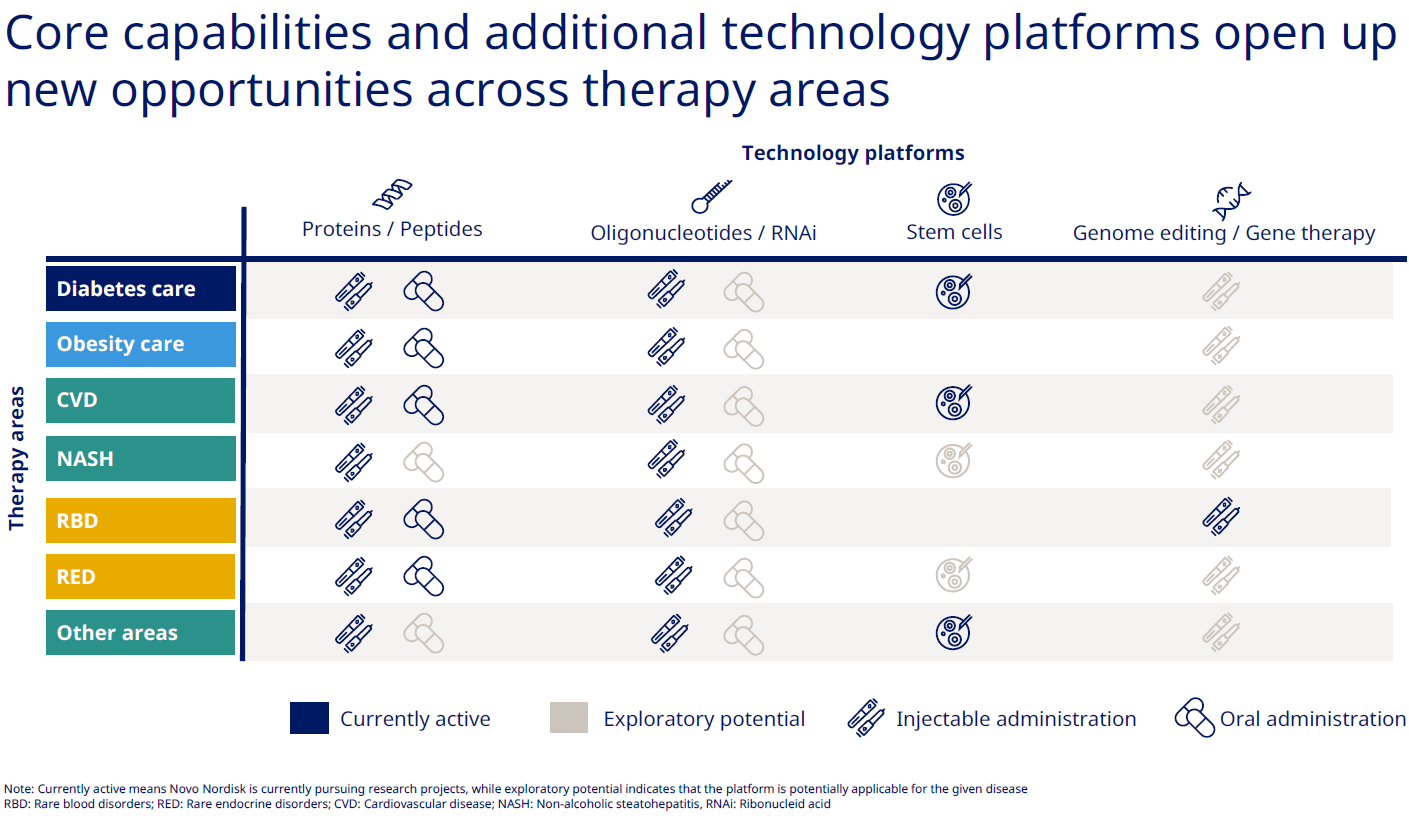

The research connected to the exploration of tablet formulation of peptide molecules had one particularly important additional implication for Novo. By exploring the biology of GLP-1s and oral absorption routes thereof, Novo Nordisk scientists learned a lot about related diseases and absorption mechanisms from stomach and gut. One needs to understand that diabetes and obesity are closely related to several cardiovascular ((CVD)) and liver diseases (like NASH), and the know-how of proteins/peptides can further be applicable to rare blood and endocrine disorders and further. In addition, oral administration formulations for proteins/peptides and chemically similar oligonucleotides in general do not exist (except for Rybelsus). So, Novo Nordisk is organically diversifying (and not diworsifying) by continuous build-up and expansion of core competencies that can be measured in generations.

Current and near-future growth drivers. (Novo Nordisk IR)

{kind=link}

{kind=link}

{kind=link}

Business Operations

I have available annual report data over the 22-year time span, from 2000 to 2022. In this time period, the company operations metrics are as:

Author's own calculations

These ratios are phenomenal. They are better than, for example, the same ratios from Merck, J&J, Sanofi, AbbVie (ABBV), BMS, Amgen (AMGN), and, as a reference, Microsoft (MSFT). Moreover, what is impressive is the consistency of Novo Nordisk business operations. Within the last 10 years, minimum Net Profit Margin was 30% in the years 2013 and 2014, and after that it climbed only higher. The only weakness in those numbers is the fact that a slow increase in debt ratio is observed. While Total-Debt-to-Total-Assets Ratio stood at 39% in the year 2013, it climbed slowly to the level of 65% in 2022. In the years prior to 2013, this ratio was stable in the range around 35%. On the other hand, in the same period the Net Profit Margin was about half as it is currently. So, one can conclude that in the period of the last 22 years, Novo Nordisk doubled its debt ratio, and at the same time it also approximately doubled profit margin, so the end effect is positive.

One more aspect needs to be understood regarding the increasing debt level in the last couple of years or so. As mentioned earlier, manufacture of semaglutide via recombinant DNA technology is complex. But in the first place, Novo first needed to invest into a manufacturing plant of solid dosage forms (tablets) for oral semaglutide (Rybelsus) in 2019 to be able to manufacture tablets at all. We need to remember that until Rybelsus, Novo did not have any solid dosage form product, so they did not have any manufacturing assets of this kind. Next, when semaglutide molecule was first launched in 2018 (as an injectable pen, products Ozempic and Wegovy), Novo Nordisk itself failed to anticipate such a strong demand. And as the demand greatly exceeded supply of all forms of semaglutide, Novo needed to invest heavily into manufacturing capacity in 2021. And it continues to do so, but currently not in semaglutide manufacturing anymore, but into manufacturing capacity of its future pipeline molecules . So, if Novo increases its debt to increase manufacturing capacity, which in effect satisfies the demand, we should not be critical of increasing its debt level.

Company Growth

In analyzing company growth, I am using a year-to-year top line, bottom line, and cash flow data, and to smooth out year-to-year spikes (especially of net profit and operating cash flow), I am also using corresponding 5-year growth rates. With Novo Nordisk, we can see some very decent numbers:

Author's own calculations

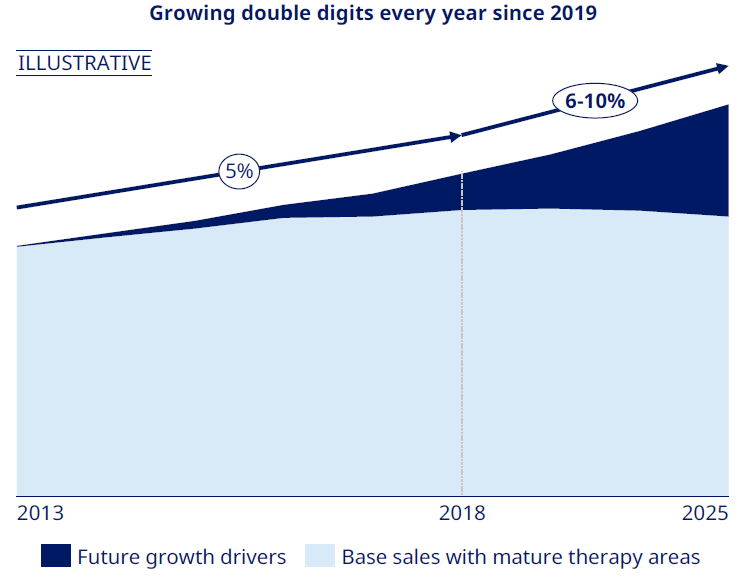

Looking into details, we can notice one important peculiarity in the data: prior to 2016, the company grew rapidly. Then, in 2017 to 2019, the company experienced its first slowdown in at least 16 years, as revenues, net profit and cash flow were stagnant. Then, from 2020 onwards, the company is reverting back to its standard growth rates. This trend is even more accelerating in the H1 of 2023 . So what happened in the years 2017 - 2019?

Right until 2017, as mentioned, Novo Nordisk was a pure-play insulin maker. And in 2017, due to a bipartisan push in the U.S., U.S. insulin net prices started to drop. However, at about the same time, Novo diversified into a new diabetes treatment of GLP-1 molecule class and a new therapy area of obesity. So, by the new diabetes and obesity treatment portfolio (Victoza, Ozempic, Rybelsus and Wegovy), the company is well able to offset the decline in insulin net prices. In fact, the demand for the new therapies is so overwhelming that the company needs to throttle starter doses of semaglutide in the U.S. and pause marketing, even though the company is ramping up the manufacturing capabilities. But even despite that, net profit is expected to grow for about 43% in the year 2023.

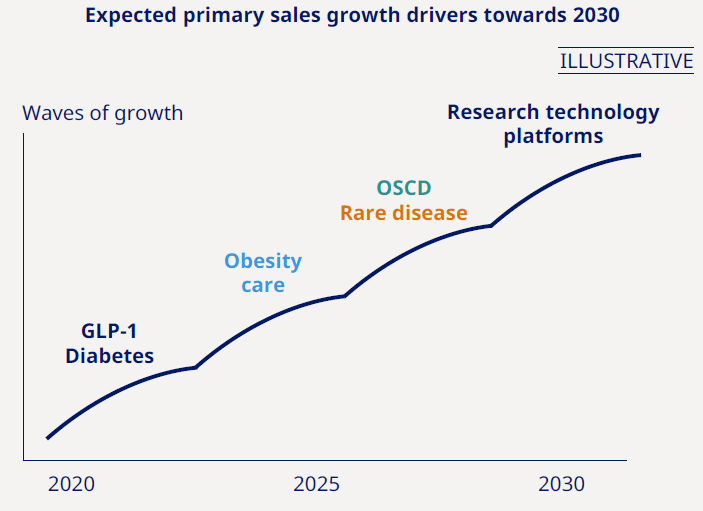

What can we expect will happen after the current demand for GLP-1 molecules for diabetes and obesity care will be satisfied? As mentioned earlier, the company is well geared to organically diversify into further new therapeutic areas and research platforms, so we can expect that at least for several years in the future the company will sustain its normal double digit growth rates.

Evolution of U.S. insulin net prices (Novo Nordisk IR)

Substitution of base (insulin) products with new growth drivers (Novo Nordisk IR)

{kind=link}

{kind=link}

Dividend And Dividend Coverage

I need to mention that I invest globally and am based in Europe. Wherever possible, I also invest on the native exchange where the company is present. I only buy ADRs in case when I do not have access to the native exchange. To have the same metric for all my investments, I use the following approach for evaluating the dividends and share prices. First, I use raw data in the currency in which the company releases its yearly figures. In the next step, I convert the data into the common base currency, which in my case is Euro. In my analyses, when referring to the current value of dividends and share prices I am referring to its native currency, but otherwise when I am referring to growth rates and ratios over a longer time, I am also including the currency effect into the analysis.

Novo Nordisk is a global dividend aristocrat with 25+ years of consecutive dividend increases. While Novo pays a meager current dividend yielding 1.1%, the dividend is rising rapidly. We saw the last rise at 19%, which is in-line with its average historical growth rate of about 20%. In the last 10 years the average dividend payout ratio has stabilized at 50% of its Net Profit and at 43% of its Cash flow from Operations, which is a safe level.

Author's own calculations

Valuation

For valuation purposes I use several parameters, which are current PE and P/CF ratios and its corresponding 5-year Cyclically Adjusted values to smooth out spikes. On top of that, I am keeping long term historical values, so I can observe long-term trends. While the drawback of this approach is that it relies on the past values, I prefer to use an assumption-free and parameter-free approach. For a reference opinion, I also compare my values with the values provided by Refinitiv.

By no doubt, current valuation of Novo Nordisk (1080 DKK or 157 USD) is high by all parameters from a historical perspective. If we compare the latest values of PE, CAPE 5, P/CF and CAPCF 5 from Q2 2023 with its corresponding long-term average values, we may conclude that the current share price is overvalued for about 31% to 41% (depending on which parameter you use). This implies mean historically fair value for share price of about 700 DKK (102 USD). However, Refinitiv values Novo Nordisk somehow higher than is the value of current share price. Why is that so?

Author's own calculations

As mentioned above, the company just recently went through a temporary slow-down due to price pressures of its insulin treatment. However, Novo Nordisk successfully returned to its long-term growth rate by new diabetes and obesity treatments in GLP-1 molecules. Current Novo Nordisk revenues stand at $26 billion, which is still drawn predominantly from the diabetes market. However, the obesity market alone is expected to be worth at least $30 billion in 2030, with most estimates in the $50 billion range ( here and here ), while some optimistic estimates are as high as $100 billion . And this market is divided among only a few companies: Novo Nordisk breaking the ground in obesity treatment, Eli Lilly following with its own GLP-1 molecule and after that some further followers. Moreover, Novo has a significant advantage over its main competitor: while it's obesity therapy Wegovy is comparable to the Lilly's GLP-1 molecule, as mentioned, Novo Nordisk is the only company in the world that succeeded to prepare a tablet formulation of it, replacing the need of an injectable pen. While Novo's product Rybelsus is indicated for treatment of diabetes, the company is running the late-stage clinical programme for using the same technology platform for the obesity market as well.

In general, the very long-term and stable performance of the company translates into the very stable long-term share price increases that correspond well with the long-term Net profit and Cash Flow growth rates. We can see that in no moving 10-year period, share price growth was less than 6% (selling in 1995 and buying 10 years prior), and in no moving 15-year period, share price growth was less than 15% (selling in 2000 and buying 15 years prior).

Author's own calculations

Risks

Main risk in investing in Novo Nordisk is its currently high valuation. Other risks are typical of all other pharmaceutical companies: potential side effects of their products and newer therapies which could prove to be better than the current ones. One example of the latter is a small molecule version of GLP-1 molecules (a so-called molecular class of -gliprons). However, up to now this has not been the case, and semaglutide, a flagship product of Novo Nordisk seems safe.

Verdict

The best time to buy Novo Nordisk shares was in the period 2017-2019 when the PE and P/CF ratios were on low levels. Currently, given the high valuation, it is probable that in the next one or two years, the share price will not make miracles. From that perspective I give the company a "Hold". On the other hand, if one is investing with an investment horizon of 10 years or more, current high valuation is probably not so relevant anymore, so from this perspective I give a company a "Buy". Moreover, with the long term investment horizon, one will collect a significant amount of dividends which are rising fast.

For further details see:

Novo Nordisk: Super Focused Pharma Company For The Long Run