NVZMY - Novozymes And Christian Hansen: A Danish Merger (Rating Upgrade)

2023-06-02 05:36:23 ET

Summary

- Danish companies Novozymes and Christian Hansen have announced plans to merge, creating a leading global biosolutions company.

- The merger is expected to be completed in late 2023 or early 2024, following regulatory approval.

- Despite the wide economic moat around both businesses, the stock price of Novozymes remains overvalued, making it a potentially risky investment.

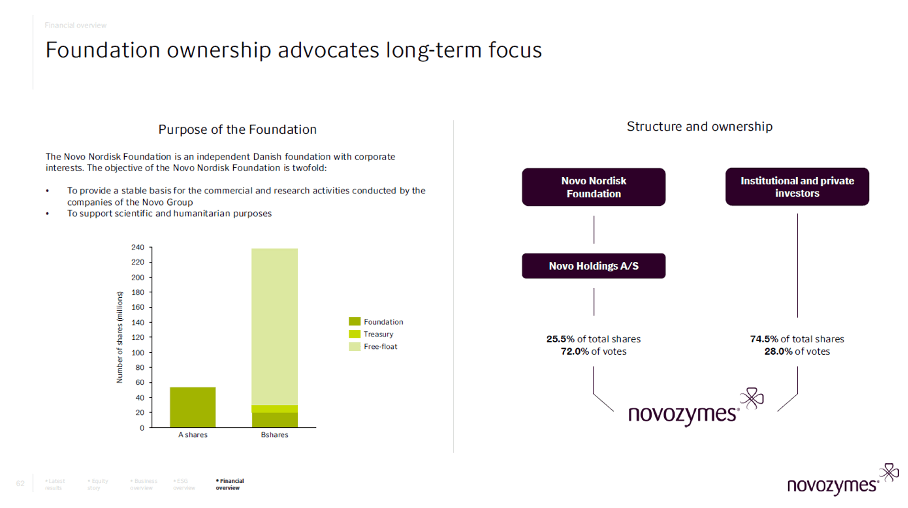

In the past, I covered several companies from Denmark quite frequently. Especially Novo Nordisk A/S ( NVO ), which is one of my biggest holdings, was covered on a regular basis (and one of my best investments in the last few years). Novo Nordisk is one of the companies controlled by Novo Holdings A/S (28.1% ownership and 76.9% voting rights according to 2022 Annual Report ) – another is Novozymes A/S ( NVZMF ) (25.6% ownership and 72.7% voting rights), which was spun off from the pharmaceutical company in 2000.

Now, Novozymes intends to merge with another major Danish company – Christian Hansen A/S ( CHYHY ). And not only did I cover Christian Hansen also in the past, Novo Holdings A/S also has a major stake in Christian Hansen (22% ownership). In the following article, we will take a closer look at the deal and try to determine if Novozymes (and/or Christian Hansen) is a good investment now.

Business Description

Before we take a closer look at the terms of the merger and try to determine an intrinsic value for the stock again, let’s start with a short description of Novozymes (which was originally published in my first article about Novozymes):

Novozymes was "founded" in 2000, when the Novo company, which was founded in 1925, was split up into three parts - another company that came to life back then is the Danish diabetes company Novo Nordisk. Since 2000, it is listed at the Nasdaq Copenhagen and has about 6,150 employees. Novozymes is the world leader for industrial enzymes and microorganisms and the company offers agriculture solutions, solutions for bioenergy or solutions for the household care industry. It also provides pharmaceutical solutions. Enzymes are enabling the transformation of products on different industries (for example, milk is becoming cheese or it gives jeans a stone-washed look). The company launches about 15 to 20 new products annually and its more than 700 different products are sold in more than 140 countries and are used in more than 30 industries.

And as we will be talking about the merger between Christian Hansen and Novozymes, let’s provide a short description of Christian Hansen as well (also taken from a previous article ):

Chr. Hansen is a global bioscience company that develops natural ingredient solutions for the food, nutritional, pharmaceutical, and agricultural industries. Chr. Hansen develops and produces cultures, enzymes, probiotics, and natural colors for a rich variety of foods, confectionery, beverages, dietary supplements, and even animal feed and plant protection. The company was founded in 1874 and is listed on the Nasdaq OMX Copenhagen since June 2010.

The Merger

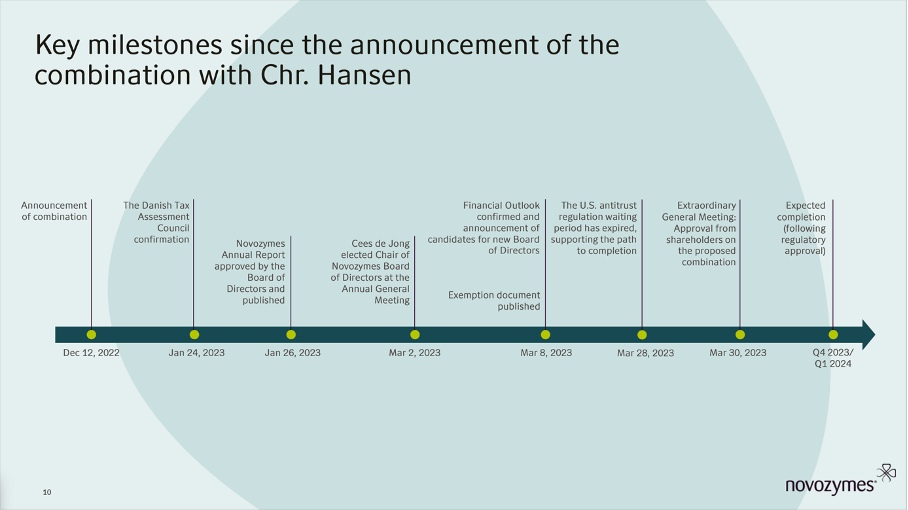

Now, that we offered a short description of the two businesses, let’s take a closer look at the merger (by the way, Christian Hansen is offering a good overview of all important documents regarding the merger). On December 12, 2022, Novozymes and Christian Hansen announced that both companies have entered an agreement to create a leading global biosolutions company.

When talking about major acquisitions we should be careful as those acquisitions are often done for the wrong reasons. It often seems to be the case that a business can’t grow organically anymore, and management is trying to increase revenue (and the bottom line) by acquiring a major competitor. These deals are often done to make the business bigger, but not better. But here we are talking about a merger, which is different, and it seems like the deal it not just done to create a bigger company. Combining the two business seems to make sense – especially as both are owned in huge parts by Novo Holdings A/S. But not only the ownership is a combining element – both companies are operating in a similar business and therefore a merger seems to make sense.

{kind=link}

When looking at the terms of the merger, Christian Hansen will receive 1.5326x Novozymes B-shares for every Christian Hansen share. This is resulting in an almost 50% premium Novozymes is paying, which raised questions among analysts. And the reaction from shareholders was a clear statement: Christian Hansen shareholder though the deal was good for them, Novozymes shareholder thought otherwise. Since the merger was announced, Christian Hansen increased 14% while Novozymes declined more than 20%.

{kind=link}

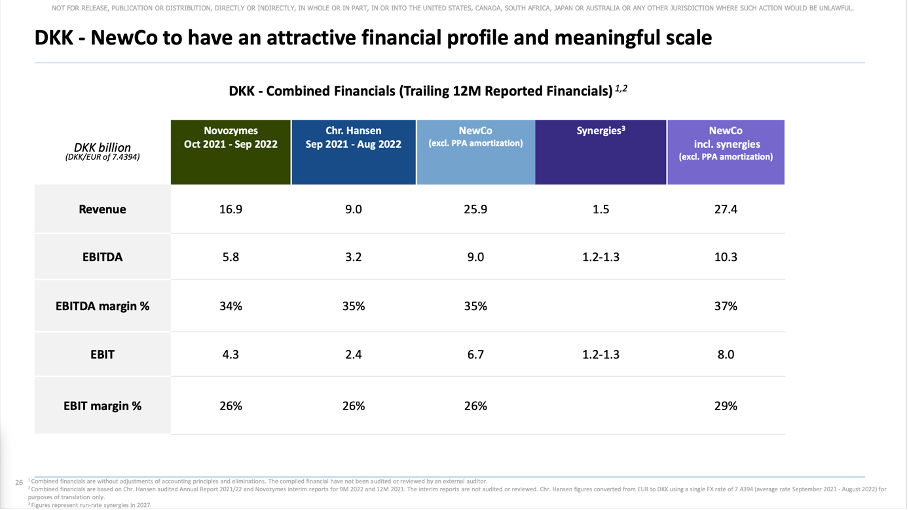

Instead of looking at the stock performance, fundamentals are much more important. When looking at the trailing twelve-month numbers, Novozymes is not only generating more revenue than Christian Hansen, but also almost twice the EBIT and one can understand why Novozymes shareholders were rather disappointed by the deal as the financial power of Novozymes does not really seem to be represented by the new shareholder structure: Novozymes shareholders will hold 44% and Christian Hansen shareholders will hold 34% of the new business. The remaining 22% will be held by Novo Holdings, but it is intending to increase its stake to 25.5% in the foreseeable future.

{kind=link}

Both companies are also expecting synergies from the deal. And another pattern we – sadly – see way too often are high expectations of synergy effects that don’t materialize. To be honest, it is beyond my circle of competence to assess the synergy effects of the two businesses, but as both companies are similar it seems realistic that synergy effects might play an important role.

{kind=link}

At the end of March 2023, Christian Hansen as well as Novozymes shareholders approved the merger. The completion of the deal is expected either in the fourth quarter of 2023 or in the first quarter of 2024 – following regulatory approval.

{kind=link}

Intrinsic Value Calculation

In the past I saw both Novozymes as well as Christian Hansen as two great businesses – but clearly overvalued. Considering the merger of the two businesses (and considering the fact that my last articles about both companies were published more than a year ago), it makes sense to calculate an intrinsic value for the combined business.

First, we must determine the number of outstanding shares for Novozymes after the merger. And according to the deal structure, Novozymes will issue 157.7 million new class B shares – additionally to 276.6 million outstanding shares resulting in 434 million shares.

Second, we must calculate how much free cash flow the new company will be able to generate. When looking at the average numbers of the last few years, Christian Hansen could generate about DKK 1,500 million in free cash flow and Novozymes could generate about DKK 2,400 million in free cash flow. Combined we can assume almost DKK 4,000 million in free cash flow for Novozymes as a new company after the merger (and we should keep in mind that these are certainly not pessimistic assumptions).

Third, we must determine what growth rates might be realistic for Novozymes in the years to come. Management is excepting a revenue CAGR between 6% and 8% in the years to come (including synergies) and the company is also expecting margins to improve a little bit. In a very realistic scenario, we can assume the new business being able to grow 10% annually for the next ten years and 6% till perpetuity following that.

When calculating with these rather optimistic assumption (and assuming 10% discount rate), we get an intrinsic value of DKK 306 for Novozymes, and the share is still overvalued. But we should also calculate with lower – and maybe more realistic – growth rates. Instead of 10% growth, let’s assume only 8% growth for the next ten years which will lead to an intrinsic value of DKK 265 .

Two High-quality Businesses

Before we come to an end, let’s look once again at the main reason why we are talking about two great businesses – the economic moat around Novozymes and Christian Hansen. While the economic moat can stem from many different sources, the economic moat of Christian Hansen and Novozymes mostly stems from switching costs. In case of Christian Hansen, I wrote in a previous article:

First of all, Chr. Hansen is working with its customers and creating individualized solutions, which makes it difficult for the customers to switch to a competitor as the customers not only have to go through the process of finding an individualized solution once again. It is also uncertain if a competitor will be able to offer the same individualized solution as Chr. Hansen.

But aside from the individualization, which is leading to switching costs, another aspect is important. Christian Hansen and Novozymes are both companies selling products with a high benefit/cost ratio. I described this in an article about Novozymes:

Novozymes is providing a high benefit/cost ratio with its products and this is creating switching costs for the customers. Switching costs are extremely powerful for products that are rather cheap compared to the total costs of goods sold, but have a huge effect on the end product or outcome. Basically, when there is an extreme mismatch between the costs/input on the one side (extremely low) and the output/products on the other side (extremely high), switching costs are extremely effective. And this is the case for Novozymes' products. They are extremely important for the end product, but are only a small part of the end product's overall costs. Enzymes lead to improved performance of a product or higher yields and are therefore extremely important for Novozymes' customers.

And this is leading to high economic risks for the customers, many are not willing to take. In my article about Novozymes I also wrote:

We are especially talking about economic risk costs as the customers are also facing higher risks by switching. Maybe other companies are offering similar products as Novozymes and might offer them more cheaply, but it is difficult to tell ahead of time if the quality will be the same. And even after finding a similar product and having invested all the time and effort, the economic risk still exists because the company might only find out after some time if the product is of similar quality. And especially for such cheap products, the company has to ask if it is really worth it in the end for saving only a few cents.

And while getting bigger does not automatically result in an economic moat, it could actually help Novozymes to widen the already existing moat in the years to come.

One last aspect seem important to mention (again). Novo Holdings A/S will keep the majority of the voting rights as Novozymes will issue only B shares and as these shares have only 1/10 of the voting rights of A shares, Novo Holdings will continue to control the business.

{kind=link}

And as I have explained in an article about “family-run businesses” it is often good when one major shareholder controls the business and is interested in the long-term performance of a company.

Conclusion

The problem was (and still is) the unrealistic valuation of Novozymes – making the stock not really a good investment. Both companies – Novozymes as well as Christian Hansen – have a wide economic moat around the business and Novozymes will probably grow with a stable pace in the years to come (as it has in the last two decades).

{kind=link}

In my opinion, the stock price in the last few years was just not reflecting the fundamental reality. And at least since 2021, an investment in Novozymes would not have been a good decision. It remains to be seen if Novozymes’ stock price will decline even lower and maybe become a good investment after all.

For further details see:

Novozymes And Christian Hansen: A Danish Merger (Rating Upgrade)