DNOW - NOW Inc.: A Combination Of Pipeline And Clear Energy Projects Will Fuel Its Low Relative Valuation

Summary

- Higher demand in crude pipeline transfer, chemical injection applications, and water transfer can benefit NOW in the short-to-medium term.

- Along with the traditional MRO and PVF sales, NOW sees prospects in carbon capture and DigitalNOW projects.

- Despite negative cash flows, robust liquidity will allow shareholders' returns through share repurchase.

- I believe the stock is relatively undervalued at this level.

DNOW Is Still Attractive

I discussed NOW Inc.'s ( DNOW ) strengths and weaknesses in detail in my previous article . Despite the short-term weakness in the economy, demand is rising in crude pipeline transfer, chemical injection applications, and water transfer projects. Its performance in Canada has been impressive, given the renewed interest in oil sands, midstream valves, and artificial lift projects. It also focused on alternative energy services, including carbon capture projects in the US and the recent investment in a supercenter in the Bakken.

In Q4, however, the company's US Drilling Services revenues can decrease following the economic uncertainty and the adverse effects of seasonality in the energy market. Also, its cash flows turned negative in 9M 2022. The balance sheet remains DNOW's forte, with no debt and robust liquidity. I believe the stock is undervalued versus its peers at this level. Investors might want to buy the stock to reap better returns in the medium term.

Projects That Outline Growth

Federal Reserve Bank of St. Louis

{kind=link}

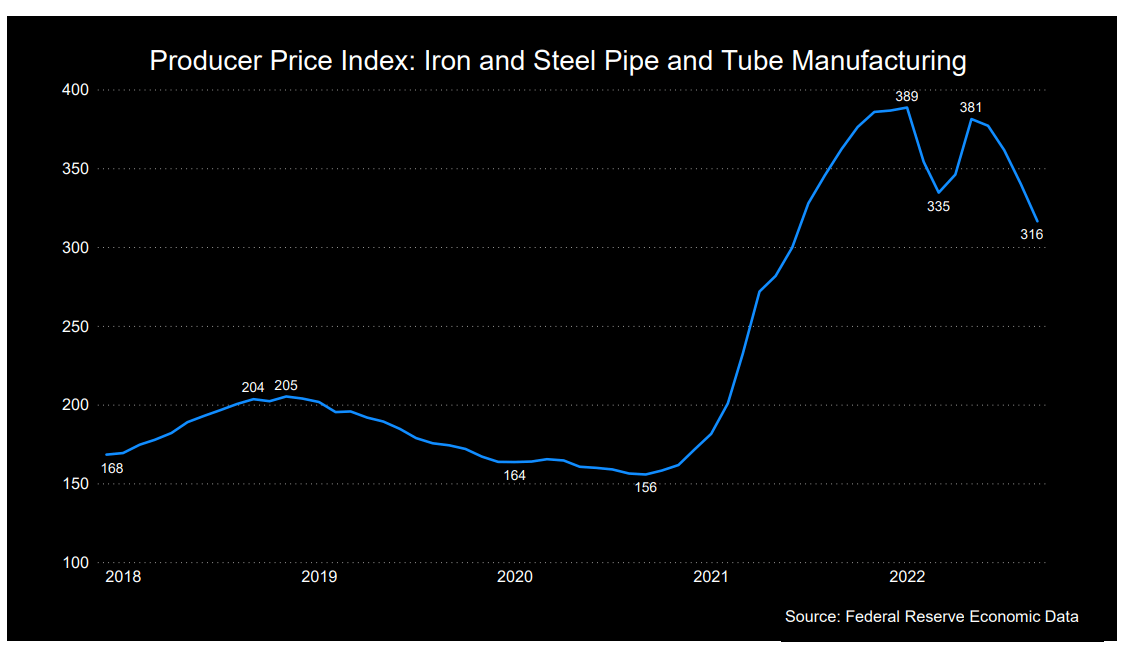

In the past year until September, the producer price index for iron and steel mills increased by 13%, indicating a rise in input cost. Since the start of 2022, however, it has fallen by 18%. Lower iron & steel prices can improve the margin. DNOW expects to see demand rising in crude pipeline transfer, chemical injection applications, and water transfer projects. As spare capacity in water transfer and water injection diminishes, the company expands the aftermarket services. Also, the horizontal rental pumps are seeing increased demand in saltwater disposal, water transfer, and frac protection activities.

In LNG operations, the company supplied line pipe in an LNG processing facility in Q3. In Q4, it plans to open a PBF plus supercenter in Williston to provide its customers with technical sales and product application support. Also included in the facility are downhole pump sales and power service stocking and service offerings. The company's Williston supercenter will also house US energy and US processes businesses, providing opportunities to generate synergies through revenue capture from cross-selling products and services.

Outlook And Forecast

{kind=link}

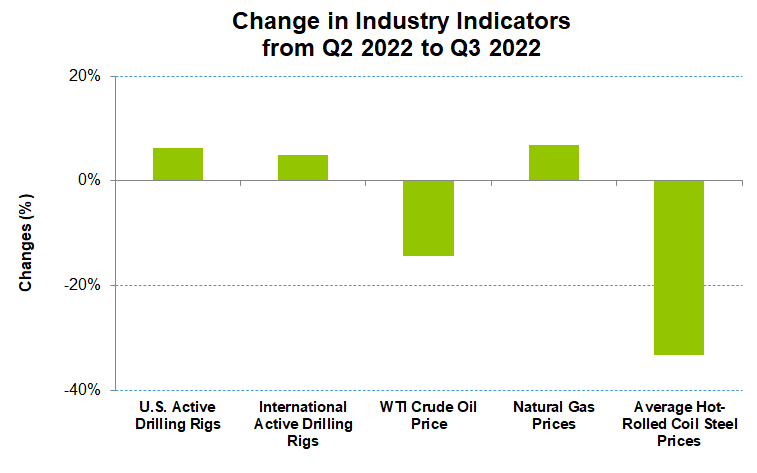

The energy indicators started to weaken at the close of the year. Over the past year, the crude oil price declined by 14%, while the rig count registered a modest 6% growth. The US completion activity, however, maintained its strength, increasing by 23% in the past year. The volatility has adversely affected the company's US Drilling Services outlook.

In Q4 2022, DNOW expects its US revenues to decrease by " mid to high single-digit" percentage points. Despite that, the annual revenues in FY2022 will likely increase compared to a year ago. In FY2022, EBITDA can expand significantly (by at least 3x) compared to FY2021 due to a more robust business model, revenue growth, and stronger gross margins.

Digitization And Clean Energy Projects

DNOW recently provided a pipeline project that collects and transfers CO2. The carbon capture project aims to enhance oil recovery operations in the Northern U.S. It also offers multistage pumps used in the green hydrogen project.

The company's DigitalNOW initiatives took another step forward. Digital revenue as a percentage of SAP revenue improved to 42% in Q3. Plus, it received another project commitment to provide its AccessNOW security, monitoring, and inventory management solution.

Q3 Drivers And A Geographic Break-Up

{kind=link}

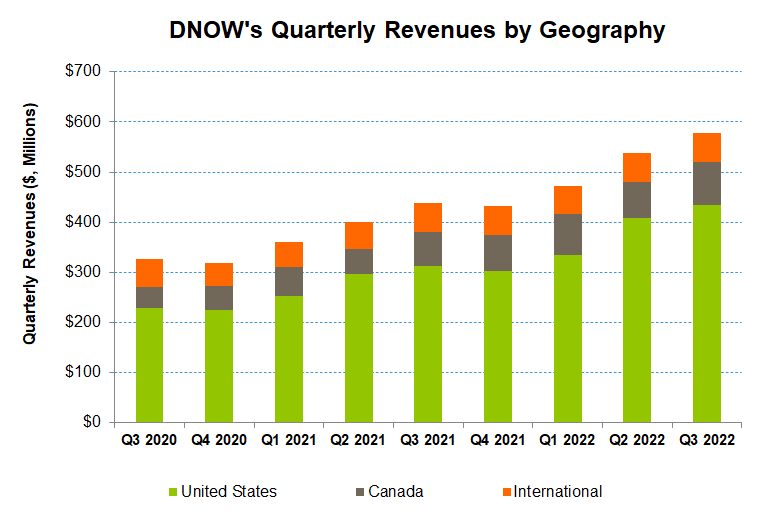

The company's US revenues increased by 7% in Q3 2022 compared to Q2. The US energy centers contributed ~75% of total US revenues. In the steel line pipe products, the margin declined while the operating margin expanded in the non-pipe products, resulting in mild topline improvement. Inventory charges also reduced during Q3.

Excluding Canada, its revenues from international markets decreased (5% down) quarter-over-quarter in Q3. Revenues from Canada increased the most (19% up sequentially) because various projects in oil sands, midstream valve, and artificial lift pushed the revenue up in Q3. The situation in the UK remains fluid, with rapid and frequent policy changes in the past few months. Besides that region, the energy market was upbeat in Europe, and activities in the company's joint contractors increased. EPC activity picked up as several projects were initiated. In the Middle East, a few projects also started to reactivate and develop.

The company's gross margin expanded by 40 basis points in Q3. The company's high-grading strategy, lower inventory charges, and healthy project margin yielded positive results. The company believes its warehousing, selling, and administrative expense is critical to better operating performance. EBITDA margin expanded marginally in Q3 compared to Q2.

Cash Flows And Balance Sheet

In 9M 2022, although the company's revenues grew versus the previous year, investment in inventory in a new supercenter in the Bakken and added employees used cash flow from operations (or CFO). So, CFO turned negative in 9M 2022 from a healthy positive balance a year ago. However, capex declined sharply in the past year. So, free cash flow remained negative but improved considerably during this period.

DNOW's liquidity was $756 million as of September 30, 2022. Its debt-free balance sheet has a definitive advantage over its peers (FAST, MSM, and MRC). The company's $80 million share repurchase program, initiated during Q2, will continue through 2024. Keeping shareholders' returns in mind, the company will prioritize acquisitions and organic growth in its capital decisions.

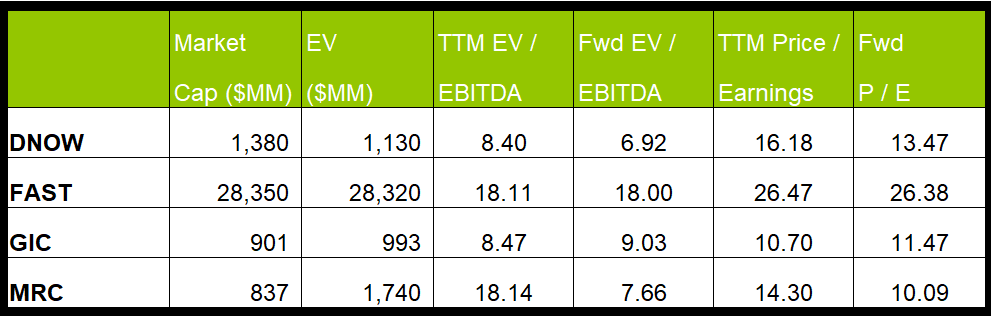

Analyst Rating And Relative Valuation

{kind=link}

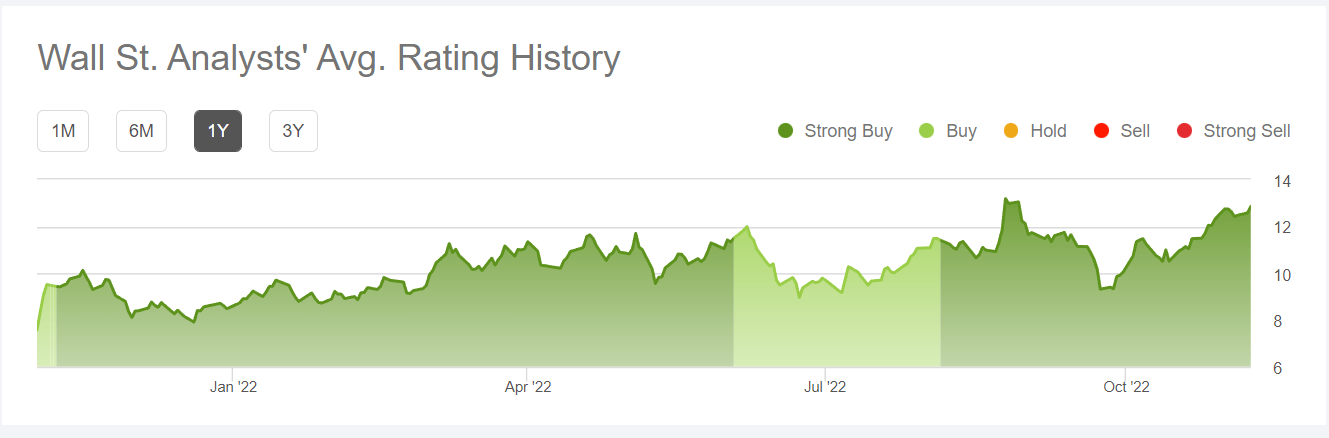

According to data provided by Seeking Alpha, three sell-side analysts rated DNOW a "buy" in the past 90 days (including "Strong Buy"), while one analyst rated it a "hold." None of the analysts rated it a "sell." The consensus target price is $14.5, suggesting a 17% upside at the current price.

{kind=link}

DNOW's forward EV/EBITDA multiple contraction is in line with its peers' EV/EBITDA contraction, which typically results in a higher EV/EBITDA multiple. The company's EV/EBITDA multiple (8.4x) is significantly lower than its peers' (FAST, MSM, and MRC) average (14.9x). So, the stock is relatively undervalued.

Why Do I Remain Bullish?

In my previous article, I was bullish on DNOW based on its position to produce innovative inventory management, cost control, and margin expansion. I wrote :

I expect its operating profit to increase significantly because of increased demand for the core service of supplying packaged units in MRO products, PVF, and safety services. On top of that, it will benefit from increased demand for fiberglass solutions in turnkey solutions. Currently, it focuses on optimizing inventory and cost control. Recently, it made an acquisition that strengthened its pump strategy and expanded the flex-flow horizontal rental pumps solution.

As the year-end approaches, its position has become bolder as demand for pipeline and water transfer increases in the US. In international operations, the energy market was upbeat in Europe, and EPC activity picked up. In the Middle East, a few projects started, while in Canada, various projects in oil sands, midstream valves, and artificial lift pushed the revenue up. So, I am maintaining the "buy" rating for the stock.

What's The Take On DNOW?

{kind=link}

As the year 2022 draws to an end, the volatility in the economy and seasonality in the energy market adversely affects DNOW's US Drilling Services outlook. Nonetheless, it focuses on carbon capture projects in the US and the recent DigitalNOW initiatives. In international operations, new projects in Europe and the Middle East will help boost revenues in the medium to long term.

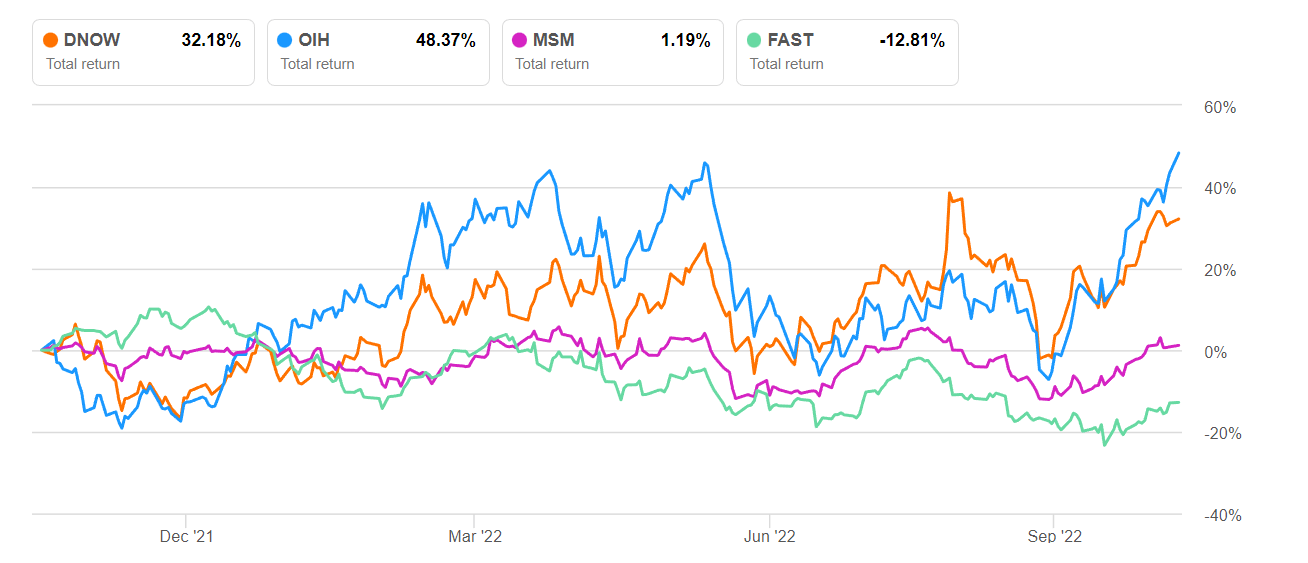

However, CFO turned negative in 9M 2022 after its investment in inventory in a new supercenter in the Bakken while it added workforce. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. DNOW has no debt and robust liquidity. The company's share repurchase program through 2024 will keep the stock price momentum upwards. I think investors would want to buy the stock at this level.

For further details see:

NOW Inc.: A Combination Of Pipeline And Clear Energy Projects Will Fuel Its Low Relative Valuation