DNOW - NOW Inc.: Growing Revenue Stream And Undervaluation Provide An Opening (Rating Upgrade)

2023-05-17 05:00:52 ET

Summary

- Following the acquisitions, DNOW has enhanced revenue opportunities.

- With integrated supply chain services, it lowered its operating expenses and improved inventory levels.

- However, the revenue growth faces near-term obstacles from project non-recurrence and the spring break up in Canada.

- DNOW stock is relatively undervalued compared to its peers.

Opportunities Coming At DNOW's Ways

You can read NOW Inc.'s ( DNOW ) strengths and weaknesses in my previous article . The company's 2022 acquisitions bolstered its revenue generation capabilities and grew its market share after implementing a new commitment with an IOC (integrated oil company) in the Permian. It has deployed several mobile horizontal pumping units to Canada for a new LNG pipeline. Demand for oxygen removal systems for oil and gas tank batteries, which came through the EcoVapor acquisition, has also risen.

However, I see revenue headwinds from project non-recurrence. Plus, in Canada, the adverse effect of seasonality can lower the topline growth. The company's free cash flow remained negative in Q1 after upgrading key facilities' utility and expanding its rental fleet. Nonetheless, it plans to generate robust cash flow from operations in 2023. The remaining balance in its share repurchase program can perk up the share value. The stock is relatively undervalued compared to its peers. Investors would do well to "buy" the stock, expecting higher returns in the medium term.

Strategies In Different Geographies

DNOW has recently acquired two US Process Solutions businesses, expanding its manufacturer territorial exclusivities and providing enhanced revenue opportunities. The Odessa Pumps and Stealth Pump and Supply in the Permian position DNOW a large pump service organization in the Permian. In addition, it would deepen its offerings into the downstream, refining, and industrial markets. The company did not only renew its agreements with IOCs and gas utility and refinery customers but also grew its market share after implementing a commitment with IOC in the Permian. With integrated supply chain services, it lowered its lease operating expenses and improved inventory levels to maintain construction and project time limits. As demand for renewable diesel products increased, the company's PBF products for biodiesel conversion at the refineries increased.

In other initiatives, the company deployed several mobile horizontal pumping units to Canada for a new LNG pipeline under construction. It may also find opportunities to meet higher demand for natural gas emission reduction products. Demand for recently acquired EcoVapor oxygen removal systems for oil and gas tank batteries has also risen. The recent acquisitions and increased demand for lapped units and pump booster packages in the midstream activity. Outside oil and gas, the industrial manufacturing and food and beverage business require higher pump packages, air compressors, and aftermarket service capabilities.

The Q2 Outlook And Forecast

{kind=link}

DNOW's filings

With all these acquisitions and market share gains, DNOW's management expects revenue synergies to result in "mid-single-digit" revenue growth in Q2 compared to Q1 in the US. However, internationally, its revenue can decline in Q2 following a $4 million project non-recurrence. In Canada, it expects the adverse effect of seasonality to drive revenue lower in Q2. Due to the cold weather thaw and muddy breakup period in energy activity, heavy equipment movement is restricted in Q2.

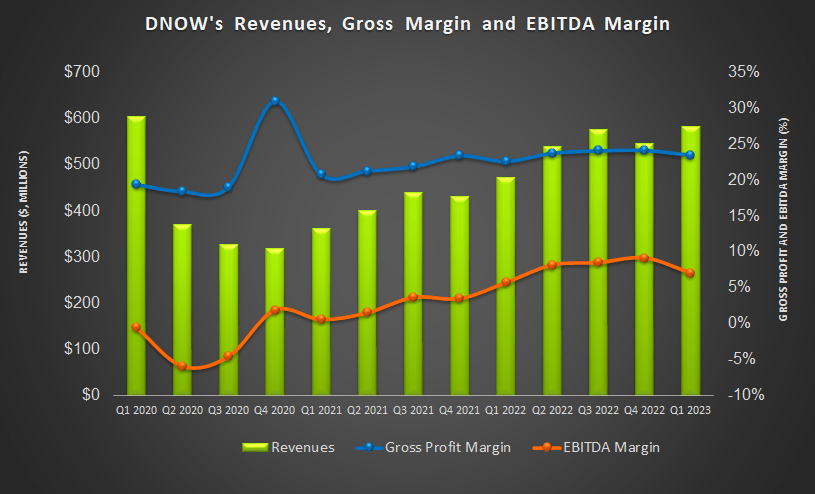

Overall, the company expects DNOW's revenues to increase in the "low single-digit percentage" range from Q1 to Q2. It expects Q2 EBITDA to remain unchanged compared to 1Q 2023. In FY2023, its revenues can increase by 8%-12% compared to FY2022. Its FY2023 EBITDA target is 8% of the annual revenue.

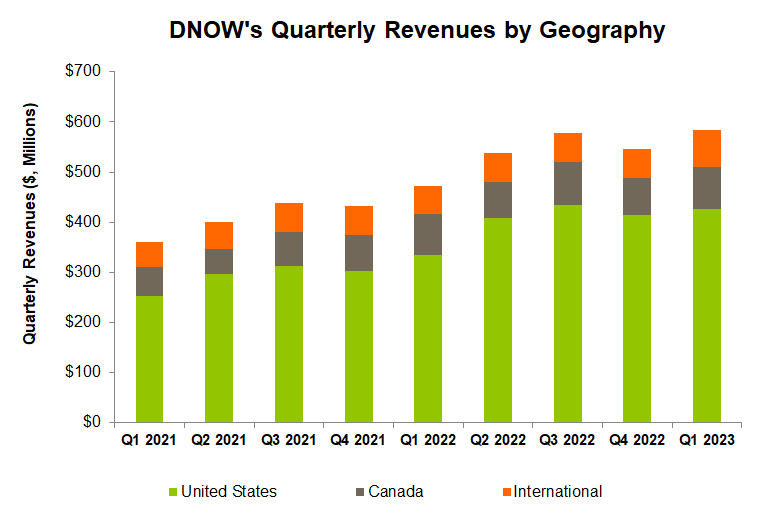

Q1 Drivers And A Geographic Breakup

{kind=link}

Seeking Alpha

The company's US revenues increased by 3% in Q1 2023 compared to Q4, primarily to higher demand for production, process, and pump packaged equipment. Sales of its seamless and ERW steel pipe increased due to increased drilling and completion activity. But lower rig count in the US and adverse weather effects partially offset the growth. Much of the rig count decline in Q1 was due to lower demand for natural gas, which pulled down the price of natural gas.

The company's revenues from international markets increased sharply (28% up) quarter-over-quarter in Q1 after it won competitive bidding in the long cycle projects. Revenues from Canada also increased handsomely (11% up sequentially). Strong demand for its valve and actuation solutions, higher MRO demand, and increased demand for pipe fittings and flanges resulted in the topline growth in international markets.

One of the critical challenges in Q1 was the revenue decline in digital revenue (as a percent of SAP revenue). A change in customer and project billing mix caused the weakness in the digital business. However, the company's management sees revenue efficiency coming from procurement simplicity and driving efficiencies. It has also rolled out a new field service app to help in the training process.

Cash Flows And Balance Sheet

In Q1 2023, DNOW'S cash flow from operations was negative, although it improved compared to a year ago. Higher revenues over the past year led to the improvement. In Q1, it invested in upgrading the utility of key facilities and expanded its rental fleet for the Flex Flow and EcoVapor businesses. So, its free cash flow remained negative in Q1. The company plans to generate $100 million in cash from operations in 2023.

DNOW's liquidity (cash & equivalents and available borrowing capacity) was $629 million as of March 31, 2023. It has a zero-debt balance sheet, which is more robust than many peers (FAST, MSM, and MRC). Of its $80 million share repurchase program, it repurchased $36 million until March 31. So, it has already consumed 53% of the authorized repurchase program.

Analyst Rating And Relative Valuation

{kind=link}

Seeking Alpha

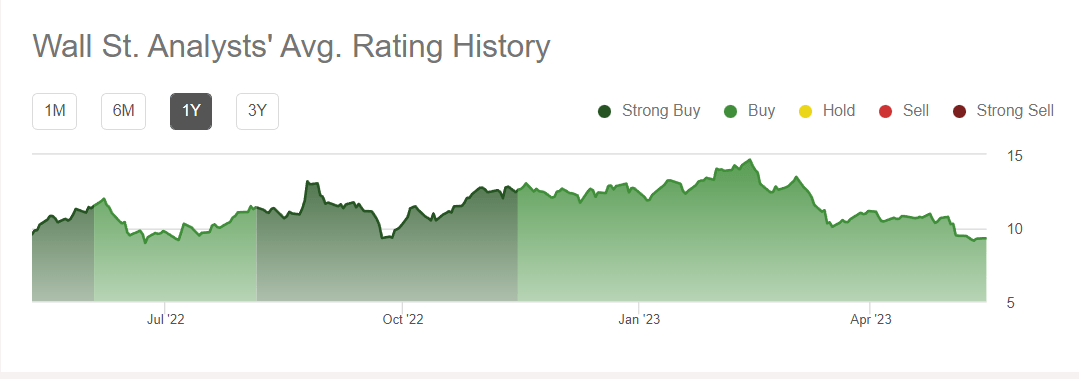

According to data provided by Seeking Alpha, two sell-side analysts rated DNOW a "buy" in the past three months (including "Strong Buy"), while one analyst rated it a "hold." None of the analysts rated it a "sell." The consensus target price is $13.5, suggesting a 46% upside at the current price.

{kind=link}

Author created and Seeking Alpha

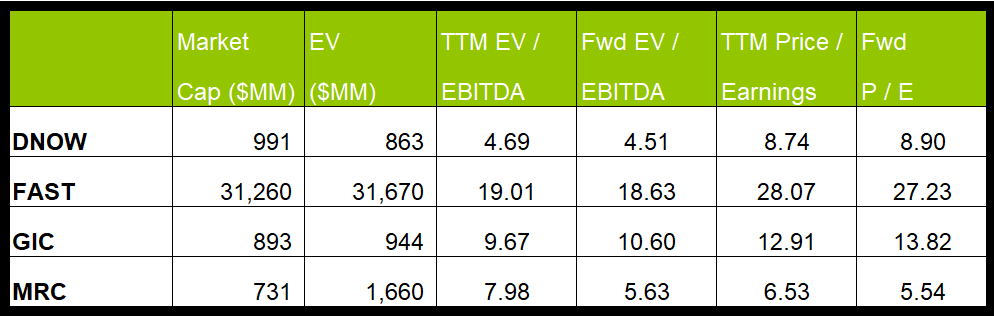

DNOW's forward EV/EBITDA multiple contraction is similar to its peers. This typically results in an at-par EV/EBITDA multiple. However, the company's EV/EBITDA multiple (4.7x) is significantly lower than its peers' (FAST, MSM, and MRC) average (12.2x). So, the stock appears to be relatively undervalued.

Why Do I Change My Call?

In my previous article, I went slightly conservative about DNOW's prospect based on the demand softness for PBF and consumable deliveries from the refining and chemical customers. So, I anticipated gross margin headwinds ahead, although I expected the international activities to come to the rescue, at least partially in the near term. I wrote :

The company is working on improving its product lines and locations in the current environment and focuses on higher-margin manufacturers. In 2023, demand will likely improve, products moving in tank battery construction, meter skids, launcher receivers and water transfer units in midstream, and air compressor packages and vertical turbine pumps in mining.

The acquisitions in 2022 have greatly improved DNOW's position as a large pump service organization in the Permian. It has also grown market share in that region. Outside oil and gas, industrial manufacturing, and food and beverage demand will require higher pump packages, air compressors, and aftermarket service capabilities. Its relative valuation multiples have also gone under. So, I think it's apt to upgrade the stock to a "buy."

What's The Take On DNOW?

{kind=link}

Seeking Alpha

At the start of Q2, DNOW strengthened its manufacturer territorial exclusivities, which enhanced its revenue opportunities. At the same time, the 2022 acquisitions bolstered its revenue generation capabilities in the Permian. Revenue synergies from the Odessa Pumps and Stealth Pump and Supply can generate revenue growth in Q2. The company's PBF products at the refineries also increased in recent times.

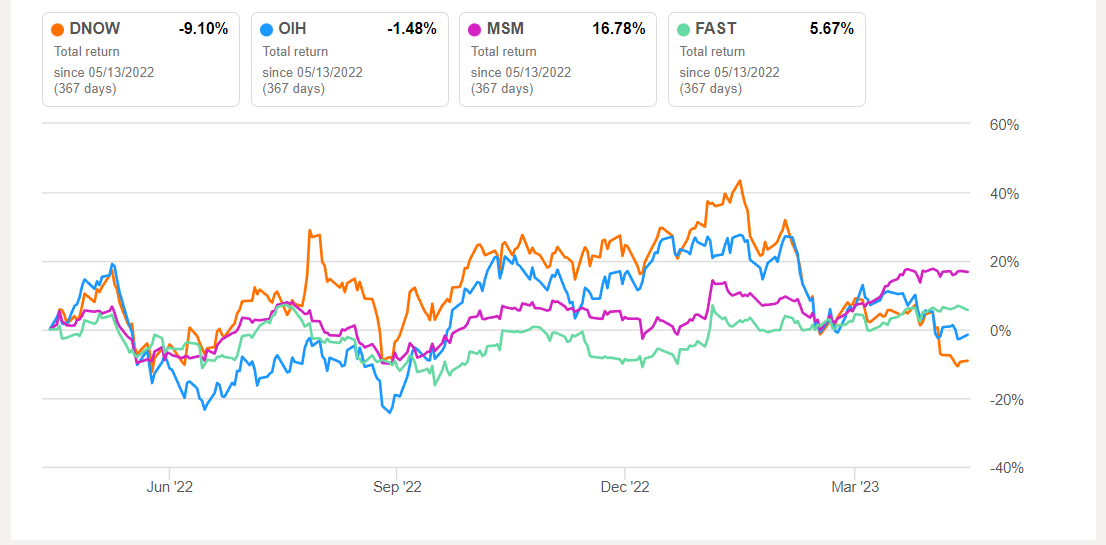

However, I see revenue headwinds from project non-recurrence, while in Canada, the adverse effect of seasonality can lower the topline growth. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. Despite negative FCF, it plans to generate $100 million in cash flow from operations in 2023. It has a zero-debt balance sheet, which has an advantage when interest rates are rising. Given the low valuation multiples, investors can expect returns to move higher in the medium term.

For further details see:

NOW Inc.: Growing Revenue Stream And Undervaluation Provide An Opening (Rating Upgrade)