DNOW - NOW Inc.: Project Additions Offset The Industry Slackness (Rating Downgrade)

2023-08-07 05:13:02 ET

Summary

- NOW Inc. focuses on technological improvement, ESG initiatives, and midstream project execution to insulate itself from energy sector volatility.

- Slower energy market activity and the recent uptrend in input cost may depress its growth and operating margin.

- DNOW's cash flows have improved significantly, and the stock appears reasonably valued, making it a good option for holding for modest gains.

DNOW Looks Stable

In my previous article , I discussed NOW Inc.'s (DNOW) strategies in detail. Since then, its approach has changed, focusing on technological improvement, ESG initiatives, and midstream project execution. It has recently acquired EcoVapor to gain grounds in the Rockies, Bakken, and Permian basins. In mid-stream, it has recently won a natural gas transmission and underground storage project. As part of diversification plans, it moves into the renewables, mining & power generation, food and beverage, recreational sports, and pharmaceutical industries. This should insulate it from the energy sector volatility.

However, the energy market lacks the encouragement required for its topline growth. Higher iron & steel pipe prices can depress its operating margin. Its cash flows improved significantly, which, along with robust liquidity, lessened the financial risks. On a relative basis, the stock appears reasonably valued. Investors might want to "hold" it for modest gains in the near-to-medium term.

Strategy And Key Drivers

DNOW has been pursuing a strategy of growth and margin expansion simultaneously. However, the recent slowdown in the energy market in North America encouraged it to tweak its strategy. It now looks to increase market share, as evidenced by onboarding a new client in Q2. The new customer addition will help it leverage technology, supply chain services solutions, and material management.

It recently acquired EcoVapor to boost technological improvement, allowing it to add oil and gas customers in the Rockies, Bakken, and Permian basins. Its ESG initiatives aim to reduce Scope 1 emissions at wellsite onshore facilities due to oxygen contamination of tank vapor gas.

{kind=link}

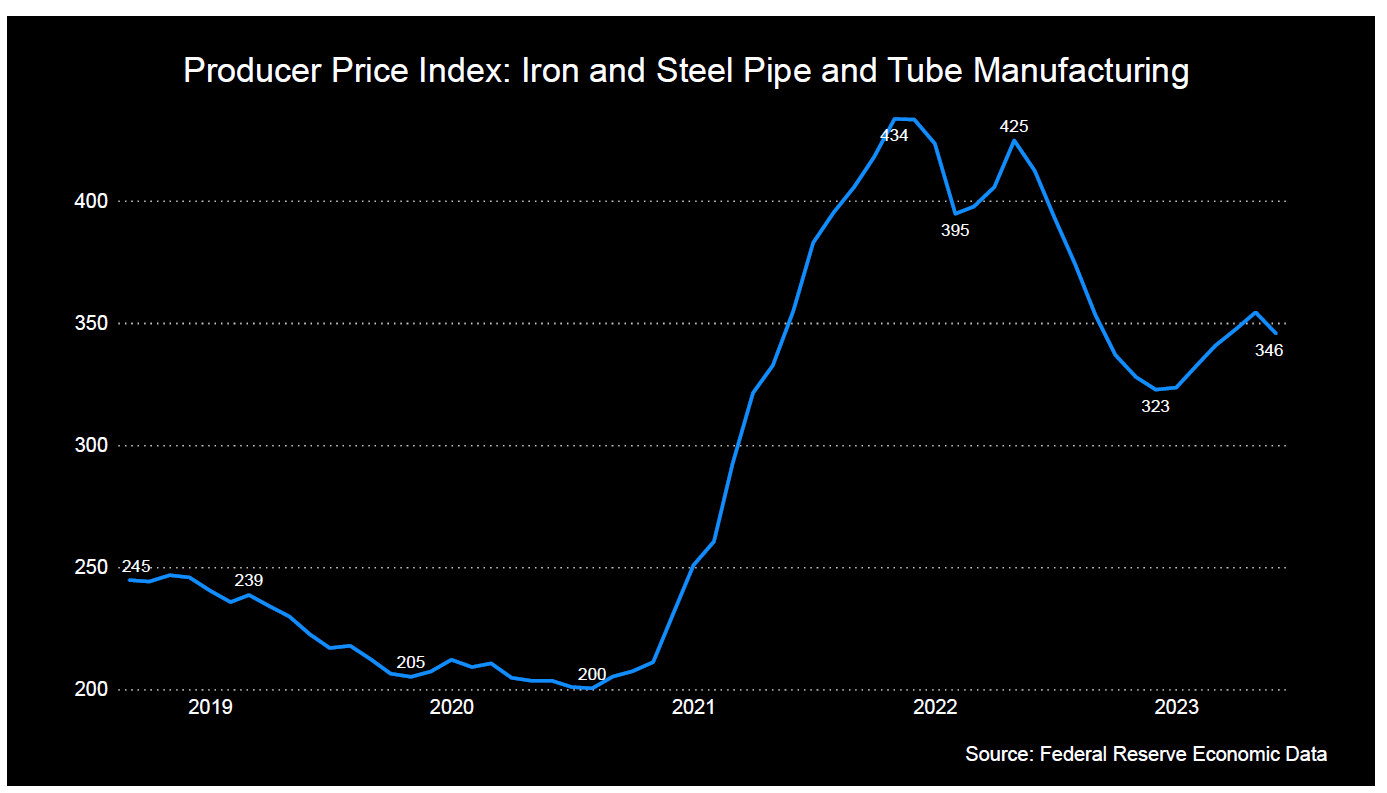

The PPI for iron and steel mills decreased by 16% in the past year until June, indicating a fall in input cost. Year-to-date, however, it has gained some ground. Higher iron & steel prices can put pressure on DNOW's margin.

DNOW continues to gain from sequential revenue rise in its U.S. Process Solutions business. The business distributes OEM equipment such as pumps, air compressors, dryers, blowers, and valves. It also provides aftermarket services.

Midstream And Renewable Energy Projects

{kind=link}

DNOW has started providing large bore valves and actuation packages for the Gulf Coast LNG markets. It serves various large integrated midstream companies and has expanded its market in the private midstream space. The supply of valves has extended to a midstream energy infrastructure company. It recently won a natural gas transmission and underground storage project to supply high-yield line pipe and weld fittings.

In renewable, it has commissioned renewable natural gas (e.g., biogas) units and expects activities to strengthen in 2H 2023. As part of diversification plans, it has started catering to the mining and power generation, food and beverage, recreational sports, and pharmaceutical industries. In wastewater applications in fracking, it has recently supplied water pump skids to a Permian operator.

Market Challenges

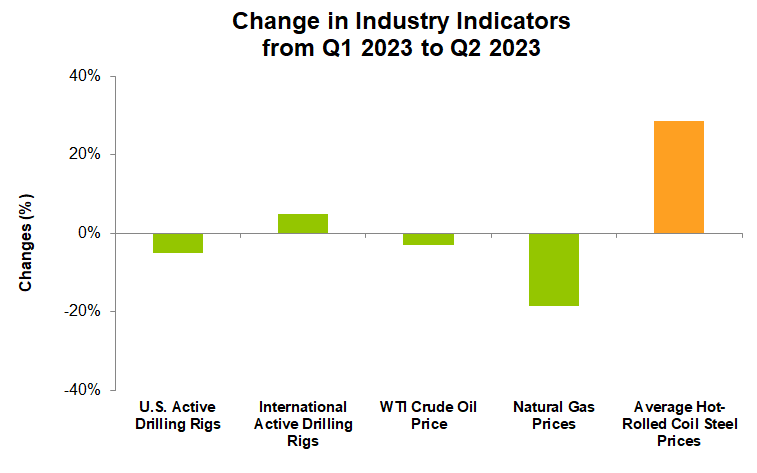

The US rig count dipped more sharply in Q2 than in Q1. While Q1 saw a 2% US rig reduction, it steepened to 5% in Q2. On top of the lower US onshore activity, the Canadian wildfires also harmed its Q2 performance. The WTI crude oil price was relatively resilient, while the natural gas price fell by 19%. The falling rig count contracted the total market. So, DNOW emphasizes deepening its ties with key customers to maintain its market share.

Analyzing The Outlook

DNOW should benefit from the material management program with an IOC. Revenues from this deal include PVF and automated valves for an LNG gathering infrastructure. The company expects revenues from this project to inflate in 2H 2023. In Canada's Saskatchewan, adding a natural gas utilities customer expanded its market share in the utility sector. Plus, it consolidates its operations following the relocation of a new supercenter.

Q2 Drivers And A Geographic Break-Up

{kind=link}

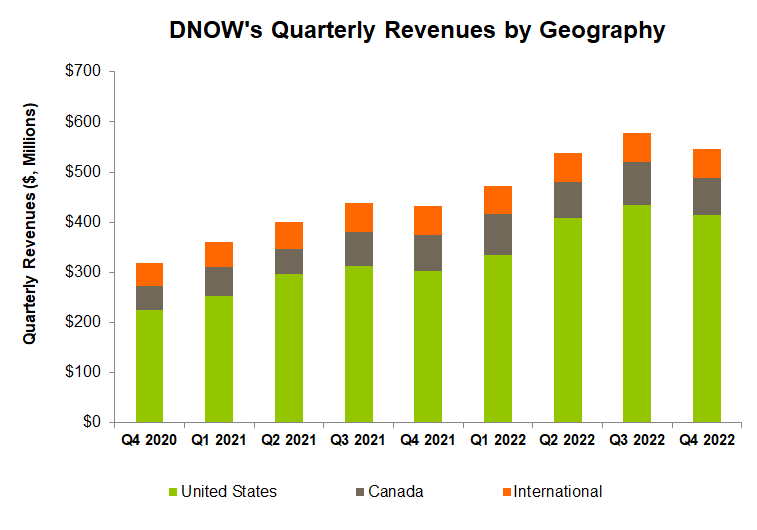

DNOW's US revenues increased by 7% in Q2 2023 compared to Q1 due to higher sales in the process, production, and pump-packaged equipment. Demand from customers in the oil and NGL production activity increased sharply, while private and public E&Ps focusing on natural has-heavy operations softened in Q2.

Quarter-over-quarter revenues from Canada decreased sharply (20% down). Following the wildfires in Alberta and British Columbia, the company idled three branches as energy companies curtailed drilling and construction activities. This reduced revenues in this region in Q2.

The company's gross and operating margins were resilient in Q2 compared to Q1. However, lower product margin in the OCTG tubing pipe sales from the workover rig programs put pressure on the margin, despite higher revenues in Q2.

Cash Flows And Balance Sheet

In 1H 2023, DNOW's cash flow from operations (or CFO) turned positive compared to a negative CFO a year ago, due primarily to higher revenues. Its free cash flow also turned positive during this period. In FY2023, it increased its CFO generation target to $120 million from $100 million earlier. It also aims to raise $100 million in FCF in FY2023.

DNOW's liquidity was $694 million as of June 30, 2023. It has a robust balance sheet with zero debt. During Q2, it repurchased $8 million worth of shares at an average price of $10.31, similar to its current stock price.

Analyst Rating And Relative Valuation

{kind=link}

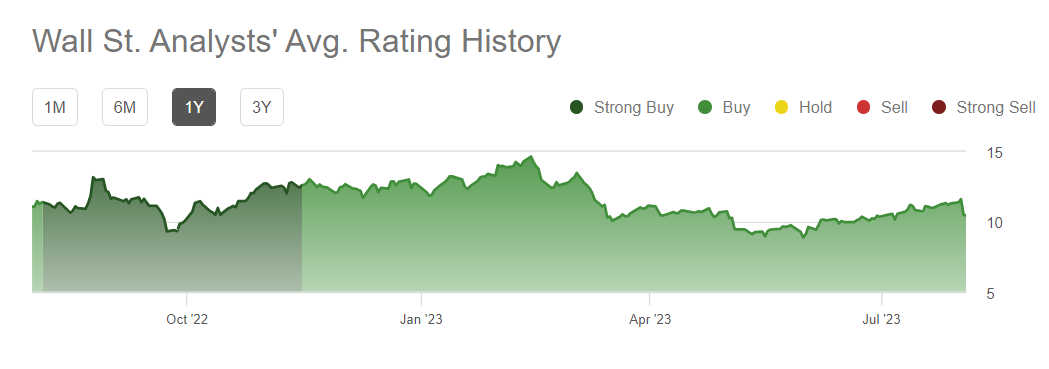

In the past 90 days, two sell-side analysts rated DNOW a "buy." This includes "Strong Buy." One analyst rated it a "hold," while none rated it a "sell." The consensus target price is $11.7, suggesting a 12% upside at the current price.

Author Created and Seeking Alpha

{kind=link}

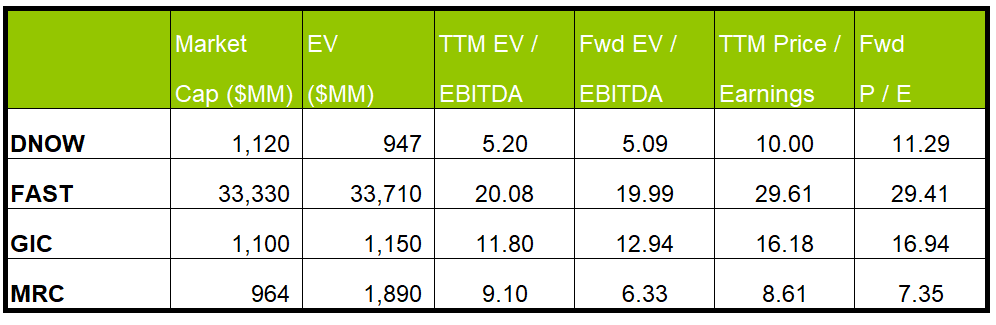

DNOW's current EV/EBITDA is expected to contract versus the forward EV/EBITDA multiple. The rate of contraction, however, is less steep than some of its peers. This typically results in a lower EV/EBITDA multiple. The company's EV/EBITDA multiple (5.2x) is much lower than its peers' (FAST, MSM, and MRC) average (13.6x). So, the stock appears to be slightly undervalued compared to its peers.

Why Do I Change My Call?

In my previous article, I discussed that an improved international market, especially from the IOCs and NOCs worldwide, would push the company's sales. Its margin growth was likely to stagnate as PBF and consumable deliveries softened following a slowdown in the downstream sector. It set plans to generate robust cash flow from operations in 2023. Given the relative undervaluation, I thought the stock was apt for a "buy." I wrote :

The 2022 acquisitions bolstered its revenue generation capabilities in the Permian. Revenue synergies from the Odessa Pumps and Stealth Pump and Supply can generate revenue growth in Q2. The company's PBF products at the refineries also increased in recent times.

After Q2, DNOW's strategy revolved around technological improvement, ESG initiatives, and midstream project execution. Its performance in the US improved following higher oil and NGL production activity. However, its activities in Canada have been curtailed significantly. Its relative valuation multiples do not show much room for stock price appreciation. So, I am downgrading it to a "hold."

What's The Take On DNOW?

{kind=link}

DNOW should gain from a project with an IOC by supplying PVF and automated valves for an LNG gathering infrastructure. Although it faces headwinds in Canada, adding a natural gas utilities customer in that region expanded its market share in the utility sector. The company's recent acquisition of EcoVar will help it proliferate in the Rockies, Bakken, and Permian basins.

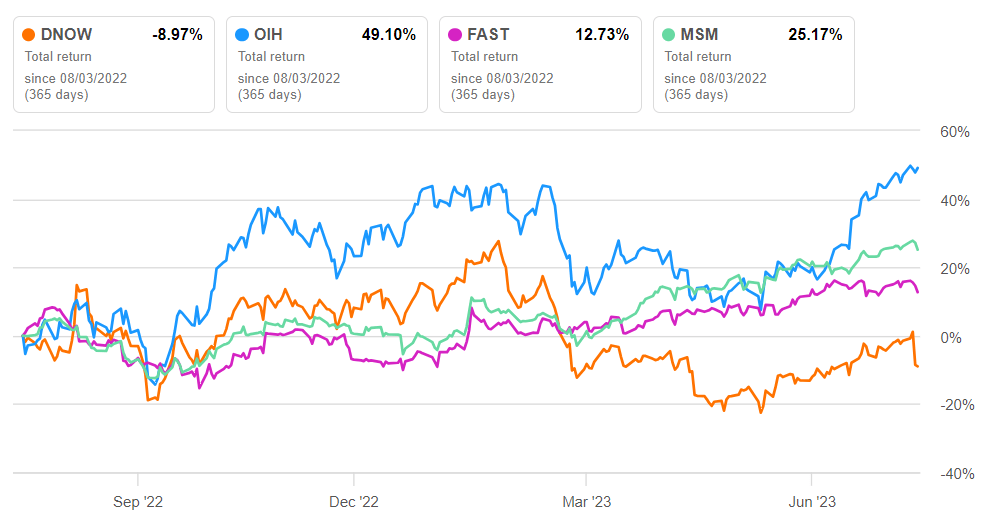

In 1H 2023, the industry indicators needed to be more conducive to energy activity growth in the near term. Higher iron & steel prices can also pressure DNOW's margin. So, the stock underperformed in line with the VanEck Vectors Oil Services ETF ( OIH ) in the past year. Not only did its FCF turn positive in 1H 2023, but DNOW also increased its FCF guidance for FY2023. It has ample liquidity. I think the stock is apt for a "hold" at this price level.

For further details see:

NOW Inc.: Project Additions Offset The Industry Slackness (Rating Downgrade)