DNOW - NOW Inc.: Steady Drivers But Lacks A Punch In The Short Term

2023-11-08 03:47:01 ET

Summary

- DNOW continues to invest in supercenters and has won large project awards in various sectors, indicating potential growth opportunities.

- Near-term outlook is affected by customer budget exhaustion and fewer business days, but cash flow growth in 2023 improves financial strength.

- Iron and steel prices have decreased, which could ease DNOW's margin, but the rate of decline has slowed. Overall, the stock appears reasonably valued.

DNOW Looks Poised For Growth

I discussed NOW Inc.'s (DNOW) strategies in detail in my previous article . The company will continue to invest in supercenters in its key geographic locations. It has won large project awards in gathering projects, midstream compressor stations, and centralized tank battery builds. It also won a project to supply PVF for a plant expansion that increases carbon capture initiatives.

However, DNOW's near-term outlook suffers from customer budget exhaustion and fewer business days in the US and Canada in Q4. The cash flow growth in 2023 has made a noticeable difference to the company's financial strength. Compared to it, the stock appears reasonably valued. Although the growth potential is limited in the near term, I think the returns will accelerate in the medium-to-long term. So, investors might want to "hold" it.

Strategy And Key Drivers

DNOW continues to invest in the supercenters in the Northwest, Williston, North Dakota, and Wyoming, making it possible to expand the regional revenue bases. It has won large awards in gathering projects, midstream compressor stations, and centralized tank battery builds. In the Powder River and Uinta basins, the company sees opportunities to provide actuated valves to E&Ps and midstream companies. It has recently extended a two-year line pipe agreement with the gas utility customer.

In workover rig programs, the company's pipelines offer solutions to lower Scope 2 emissions compared to the traditional logistics companies to support well-maintenance programs. In the CCUS (carbon capture initiatives) market, which is at an early stage of a multiyear growth cycle. It recently won a project to supply PVF for a plant expansion that increases CO2 capture in an underground sandstone storage site. Such projects help grow its carbon capture revenues with the new and legacy customers.

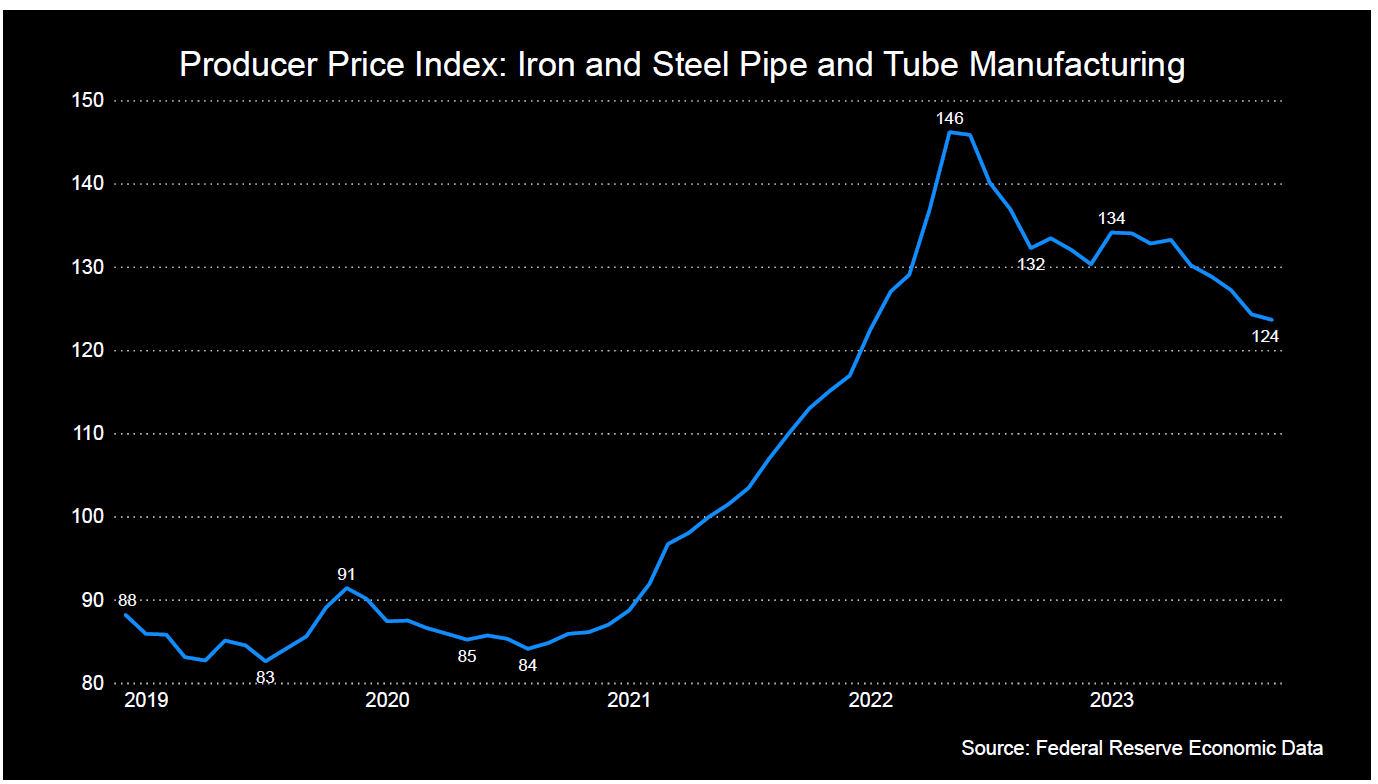

Iron & Steel Price Index

{kind=link}

The PPI for iron and steel mills decreased by 6.5% in the past year until September, indicating a fall in input cost. According to the November Pipe Logix report, pricing on line pipe has declined for 17 consecutive months. Lower iron & steel prices can ease DNOW's margin. However, the rate of decline has slowed significantly in recent times compared to a year earlier. So, to counter the possible effect of a price rise, the company will continue to manage the inflow and disposition of pipe inventory.

Outlook Explained

{kind=link}

Customer budget exhaustion and fewer business days will likely lower DNOW's revenues from the US and Canada in Q4. Since the end of 2022, nearly 150 rigs have exited the market until September. In the international market, its revenues will likely remain flat. However, because its topline and operating income are already ahead on a year-to-date basis, in FY2023, the company's revenues can exceed FY2022 by 8%, according to estimates by the company's management.

The FY2023 EBITDA can remain unchanged compared to a year earlier. The significant change, however, can occur on the cash flow side. Based on its estimates, in FY2023, DNOW can generate ~$120 million in cash from operations, translating into $100 million in free cash flow.

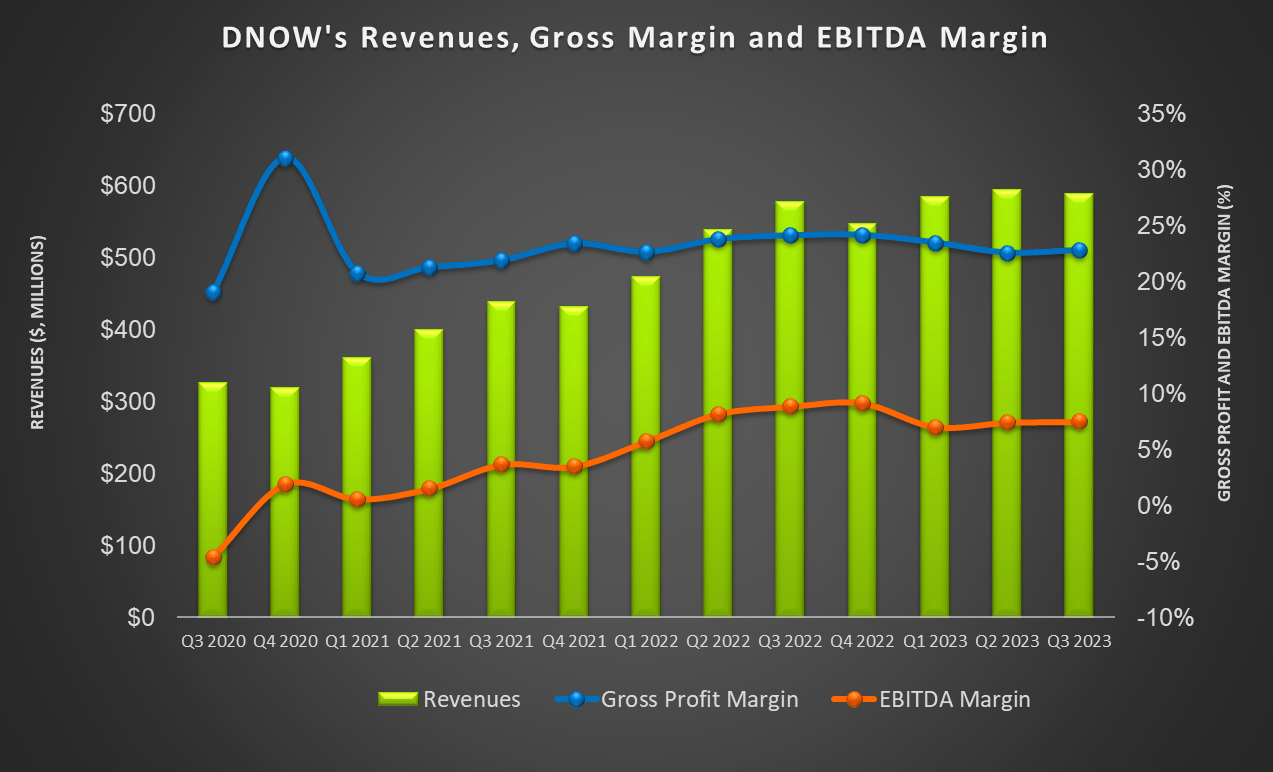

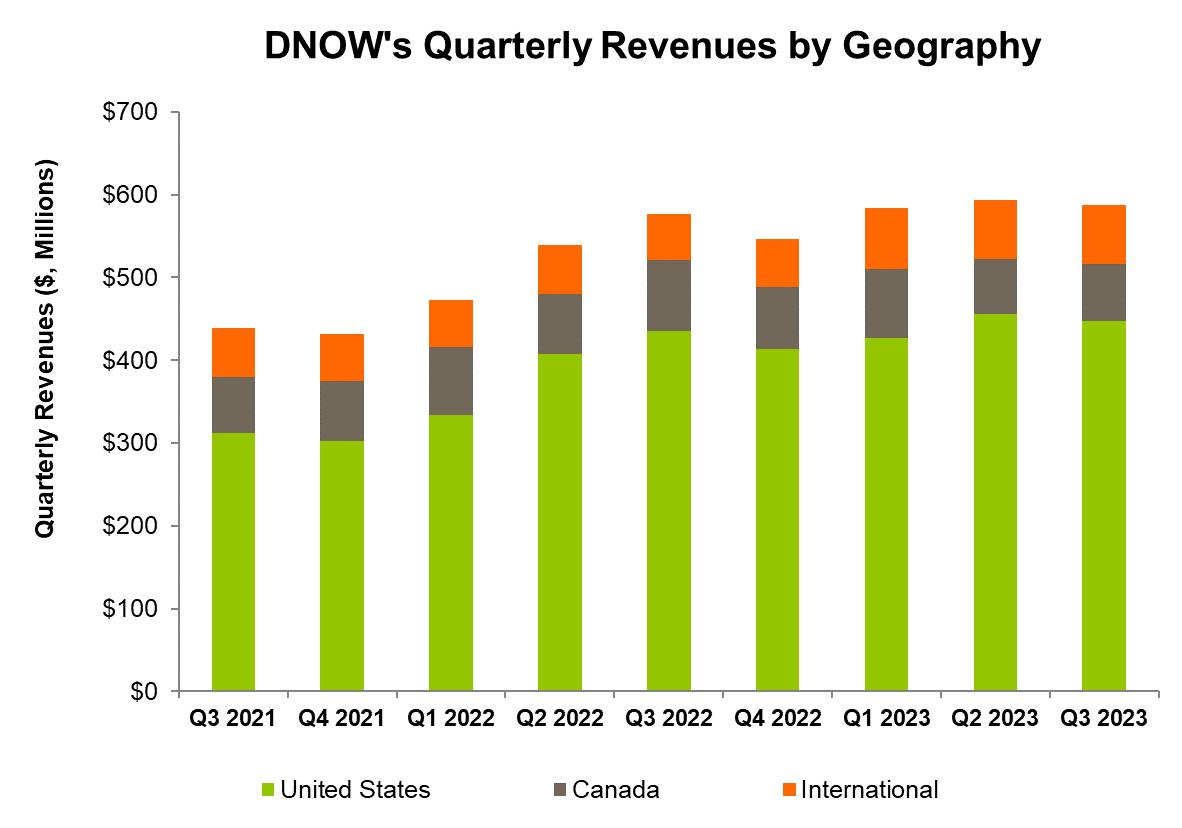

Q3 Drivers And A Geographic Break-Up

{kind=link}

DNOW generated 24% of its revenues from Canada and international regions, so we must understand the dynamics. In Canada, energy production hit a low due to a fall in takeaway capacity, the impact of wildfire outbreaks, and maintenance-related stops at oil sands mines. Lower production and the delay in drilling completion activities adversely impacted DNOW's revenues in Q3. Quarter-over-quarter, its revenues from Canada increased by 3% in Q3.

The company's Central Canada fiberglass business, on the other hand, benefited from new customer additions. I think, post-winter, the company's shipments will increase and may exceed previous expectations. In international markets, DNOW's topline remained unchanged in Q3 from a quarter ago. In the UK, Middle East, Australia, and other regions, it saw increased specific project deliveries, improving the company's sales.

The company's DigitalNOW revenue had a minor setback as its share as a percent of total SAP revenue dropped 200 basis points in Q3 from Q2. It recently went live on an e-commerce implementation with a US-based E&P operator. It also deployed a new warehouse mobility device, which helped create sales orders, packing, shipping, and receiving activities.

Cash Flows And Balance Sheet

In 9M 2023, DNOW's cash flow from operations (or CFO) turned significantly positive compared to a negative CFO a year ago, due primarily to higher revenues and favorable changes in net working capital. Its free cash flow also turned positive during this period.

DNOW's liquidity was $672 million as of September 30, 2023. It has a robust balance sheet with zero debt. During Q2, it repurchased $5 million worth of shares at an average price of $10.65, similar to its current stock price.

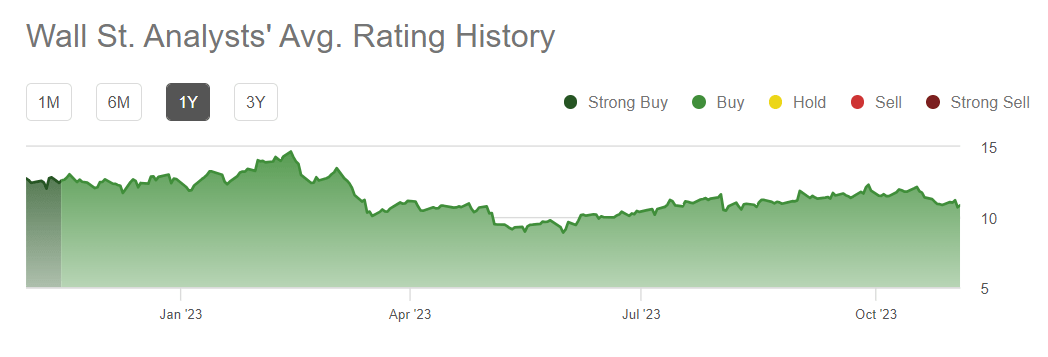

Analyst Rating

{kind=link}

Two sell-side analysts rated DNOW a "buy" ("Strong Buy") in the past three months. One analyst rated it a "hold," while none rated it a "sell." The consensus target price is $13.7, suggesting a 30% upside at the current price.

Relative Valuation

{kind=link}

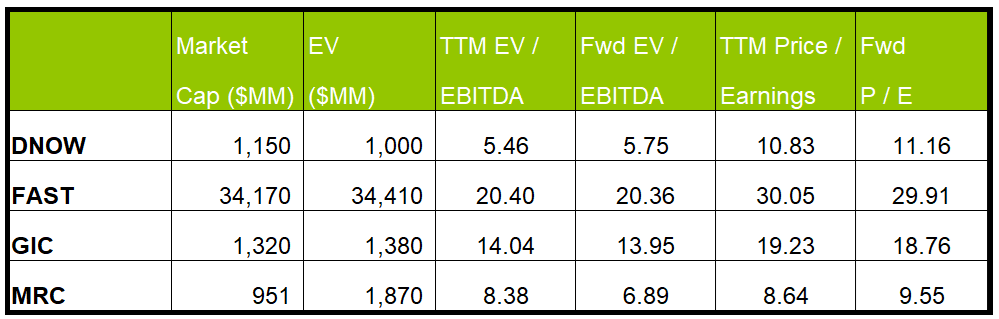

DNOW's current EV/EBITDA is expected to expand versus the forward EV/EBITDA multiple. This is in contrast to some of its peers, which indicates DNOWS's adjusted EBITDA can fall compared to a rise in EBITDA for its peers. This typically results in a much lower EV/EBITDA multiple. The company's EV/EBITDA multiple (5.5x) is much lower than its peers' (FAST, GIC, and MRC) average (14.3x). So, the stock appears to be reasonably valued compared to its peers.

Given the uncertainty in the energy sector, I do not see the stock improving sharply in the short term. However, if it trades at the past average, it can climb 175% from the current level. I think the energy sector has undergone structural changes over the past few years, and I do not believe it will return to its past high. Therefore, DNOW trading at the past average is unlikely. But with higher operating margin and free cash flow generation, it can yield materially higher positive returns (about 50%) in the medium term.

Why Do I Keep My Call Unchanged?

In my previous article, I discussed that ESG initiatives and midstream project execution were DNOW's concurrent strategy. During Q2, Its higher crude oil price and NGL production activity improved performance in the US. However, its activities in Canada declined. So, I thought the stock was apt for a "hold." I wrote :

DNOW should gain from a project with an IOC by supplying PVF and automated valves for an LNG gathering infrastructure. Although it faces headwinds in Canada, adding a natural gas utilities customer in that region expanded its market share in the utility sector. The company's recent acquisition of EcoVar will help it proliferate in the Rockies, Bakken, and Permian basins.

After Q3, DNOW's strategy revolved around workover rig programs and the growing importance of decarbonization initiatives. Its relative valuation multiples do not show much room for stock price appreciation. The pipeline price index, which signals the pressure on its operating margin, has been fluctuating. Better inventory management, however, will help improve its cash flows in the coming quarters. Given the relative valuation, I am keeping my rating unchanged at a "hold."

What's The Take On DNOW?

{kind=link}

DNOW focused on expanding its revenue bases after it won large awards in gathering projects, midstream compressor stations, and centralized tank battery builds. It caters to the rising tide in workover rig programs and decarbonization projects. Lower iron and steel mills compared to a year ago should improve its operating margin.

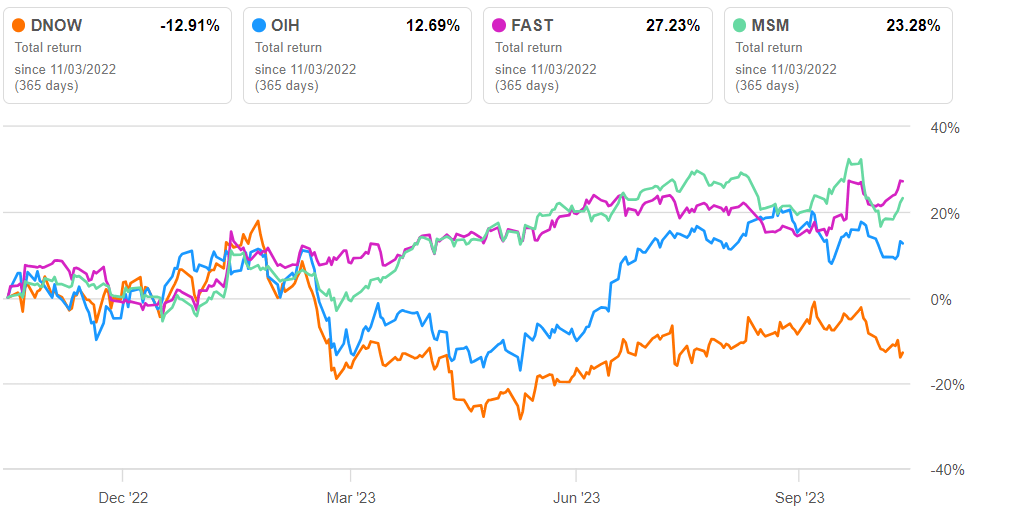

However, I see a lack of growth drivers in its international operations while the US energy market goes through an uncertain period. There is also no clear indication of movement in the iron & steel prices. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. With ample liquidity and no debt, the stock remains a "hold" at this price level.

For further details see:

NOW Inc.: Steady Drivers But Lacks A Punch In The Short Term