NPCT - NPCT: Unsupported Yield With A High Cost Of Funds

2023-09-21 18:53:19 ET

Summary

- Nuveen Core Plus Impact Fund is a multi-asset fixed-income CEF.

- The vehicle is characterized by a very high leverage ratio of 39% and an extremely expensive cost of funds close to 6%.

- NPCT's main risk factors are interest rates and credit spreads, coupled with its floating rate liability structure.

- Despite its large discount to NAV of almost -16%, retail investors should not expect a normalization here until the Fed starts cutting rates and the fund starts posting consistent positive returns.

- The CEF's yield is unsupported, with its latest distribution showing an ROC utilization exceeding 50%.

Thesis

Nuveen Core Plus Impact Fund ( NPCT ) is a multi-asset fixed income closed end fund. The fund came to market at a very inopportune time, namely in 2021, and has been pummeled by the fastest monetary tightening cycle we have seen in decades:

Change in Fed Funds (Federal Reserve)

The CEF has a multi-asset portfolio with leverage on top, so it is not a surprise the name has been down in the past two years. Its horrendous performance has now opened a very large discount to NAV of -16%.

We have covered this name last year, but the Fed has raised rates much further than expected, and the fund has failed to assume a more conservative stance via its leverage since our prior article 12 months ago, prompting a rating review. Our prior article outlined the collateral build, fund performance since inception given risk/reward metrics and expectations for a better performance in 2023 on the back of a recovery in risk assets. The fund delivered a modest total return since the rating in 2022:

Performance (Seeking Alpha)

The weak spot for this name resides in its high leverage combined with a floating cost of funds. The CEF has an effective leverage percent of 39%, which comes with an average cost of 5.97%. In this article we are going to examine the fund's discount, its leverage and implications, the collateral pool and the fund's unsupported yield.

NPCT's discount to NAV and its genesis

CEFs are short for closed end management companies, and thus represent a finite amount of issued shares, where the company is not an operating one, but one which holds assets. If investors do not like the outlook or performance of those assets, then they vote by selling the held shares. This structural feature can create significant distortions, with CEFs being able to trade at high premiums or discounts to NAV.

For NPCT, investors have chosen to open up a large discount to the net asset value of the fund due to its lack of performance. As discussed above, the timing of the CEF's IPO was horrendous, so it is not surprising the name is trading at a discount:

The CEF is trading very close to historic wide levels in terms of discount to NAV, and more importantly, we can see the tight correlation between fund performance and discount to NAV via this graph. As the CEF lost money in 2022 the discount to NAV kept widening.

We are not going to see the above discount tighten until the CEF starts posting healthy annual total returns. As we will see below, this fund has a very high floating rate cost of funds that is eating into its returns, and per our estimation the CEF will not start a consistent positive performance until the Fed starts lowering rates.

Fund risk factors - what is next?

NPCT's main risk factors are rates and credit spreads. We are currently witnessing the peak in rates for this cycle, with the Fed having chosen to pause at their September 20th meeting. Credit spreads are on the higher side, but not at stressed levels. This risk factor can still negatively affect the CEF, especially in the instance where we get a protracted recession.

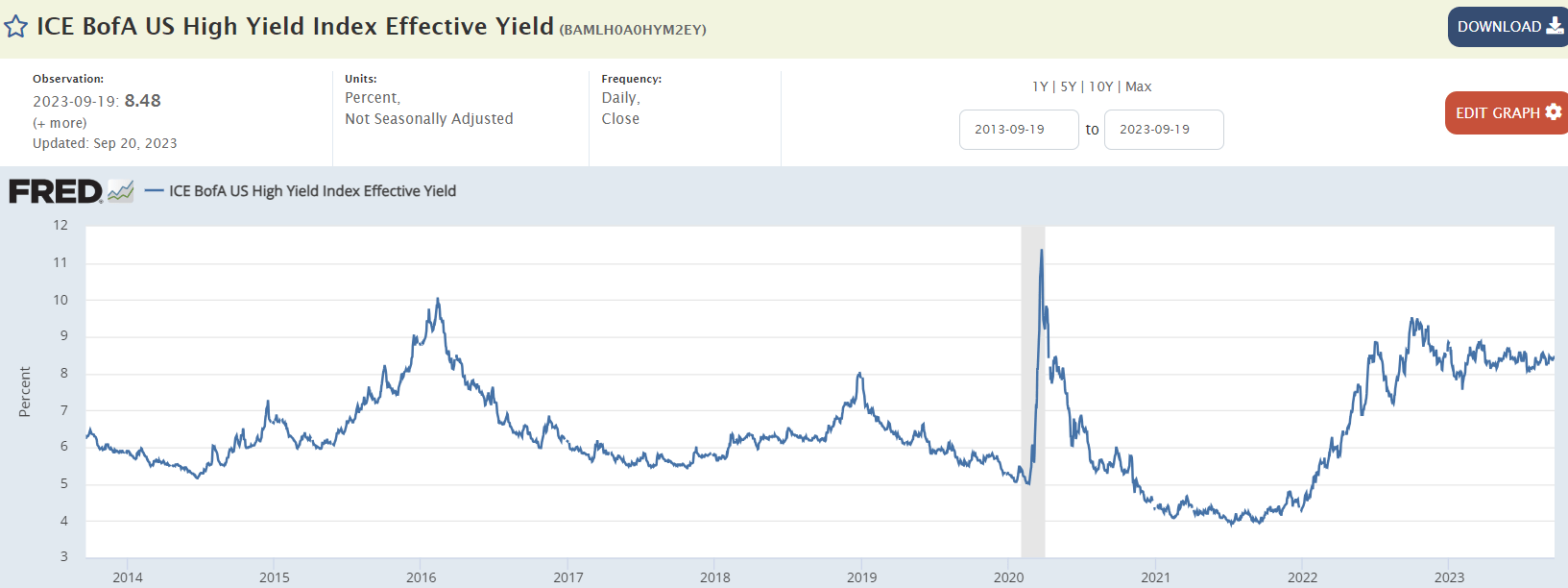

However, a retail investor needs to keep in mind that all-in yields are close to historic high levels:

{kind=link}

As measured by the ICE BofA US High Yield Index, the current effective yield is 8.48%, close to the upper range of the above 10-year graph. This is due to the current high level of risk free rates, levels which we have not seen for over a decade.

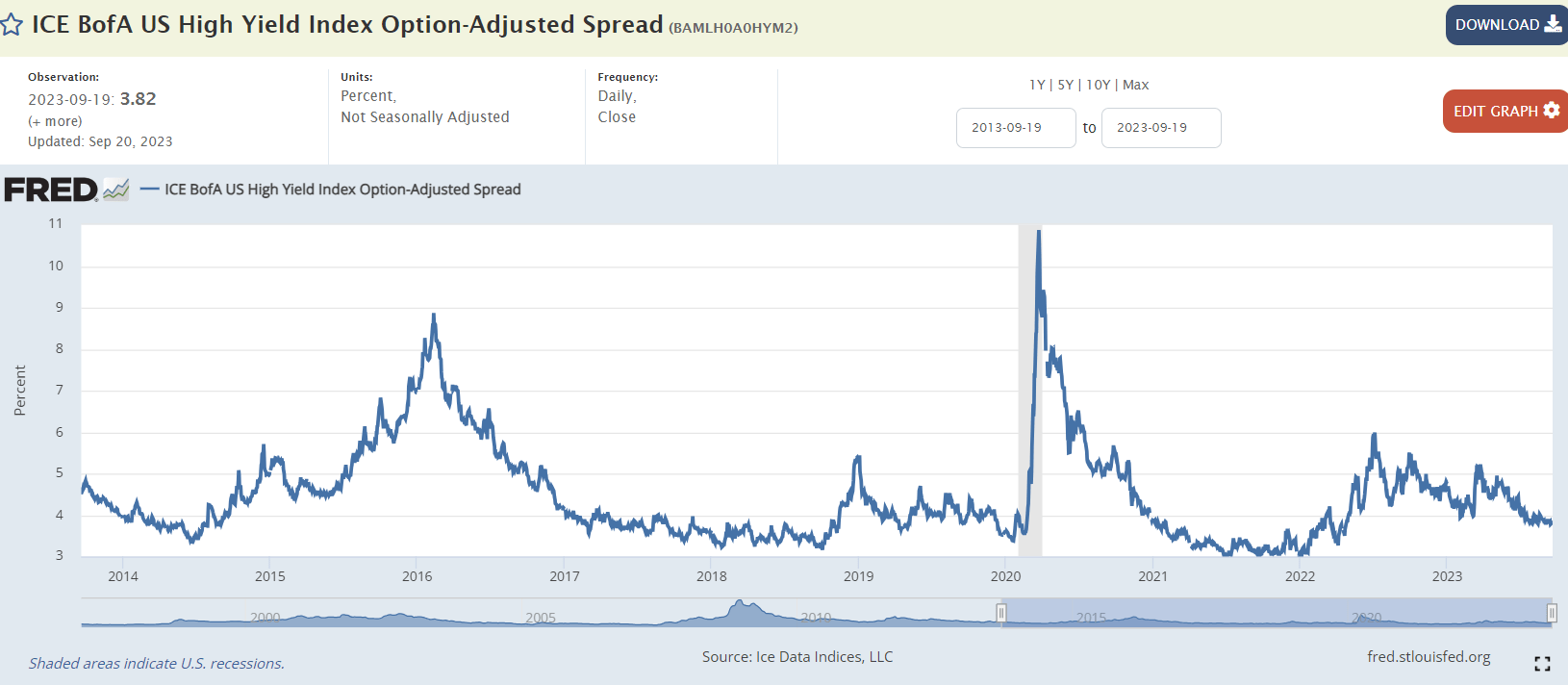

Credit spreads on the other hand have come down significantly, and could experience a substantial spike higher if a recession were to materialize:

{kind=link}

The ICE BofA US High Yield OAS is now trading at 382 bps, substantially lower than the 600 bps seen in October 2022. We are yet to see any credit event associated with pricing a potential recession here.

Distribution coverage - extremely weak with an unsupported yield

ROC stands for return of capital, and this is a structural feature that you will find in CEFs only. In essence, a fund can give you back your own money via ROC distributions. Funds with unsupported yields have high ROC distributions. NPCT falls in this category:

Distribution Coverage (Section 19a)

{kind=link}

If a fund has a ROC distribution above 40%, a retail investor should stay away. As stated above, ROC stands for return of capital. You are getting your money back when ROC is high. It is our proprietary view that sometimes as retail investors we should give portfolio managers some breathing room regarding the utilization of ROC, but a consistent high utilization of this feature puts into question the entire CEF structural feature. We should not pay high management fees just to get our cash back. The 40% is our 'house view' and it will vary as per each investor professional.

NPCT has a 10.4% distribution yield, but it is highly unsupported, as we have seen from the above Section 19a statement. The reason behind this status quo is the high cost of leverage incurred by the CEF:

Cost of Leverage (Fund Fact Sheet)

The fund has repurchase agreements in place which are floating rate based, which has translated into the fund paying higher and higher funding costs as rates have moved up:

{kind=link}

Furthermore, the CEF's leverage ratio is extremely high at 40%, meaning the vehicle has a significant cash outlay on its debt.

A high leverage ratio equates a high beta fund

Leverage magnifies returns, both on the upside and on the downside. In general, we have seen many CEFs in today's high interest rate environment reduce their leverage in order to become less volatile and more conservative. Not here. NPCT has a very high leverage of 39%, which has provided for a very volatile performance:

We have chosen a pure U.S. HY fund here in the PIMCO Corporate & Income Opportunity Fund ( PTY ) and a pure U.S. investment grade corporate fund in BlackRock Credit Allocation Income Trust ( BTZ ). They have both significantly outperformed NPCT in the past year.

2023 has been a surprising year, with receding credit spreads and a buoyant equity market, despite the anticipated headwinds. Good, robust CEFs such as PTY or BTZ have managed to post good positive total returns, while constrained names such as NPCT are still in the red on a 1-year total return basis.

Fund Holdings

The CEF has a multi-asset mandate, and may invest up to 50% of its assets in below investment-grade investments. There is a 10% cap on the CCC credits here. The current allocation to BB names is 33%, while the CCC allocation stands below 7%:

Rating Matrix (Fund Fact Sheet)

The CEF holds roughly 46% of its collateral in investment grade bonds, which provides for a nice balance against the junk portfolio. To note that the chosen fixed income securities mainly straddle the middle of the ratings grid, namely BBB/BB names.

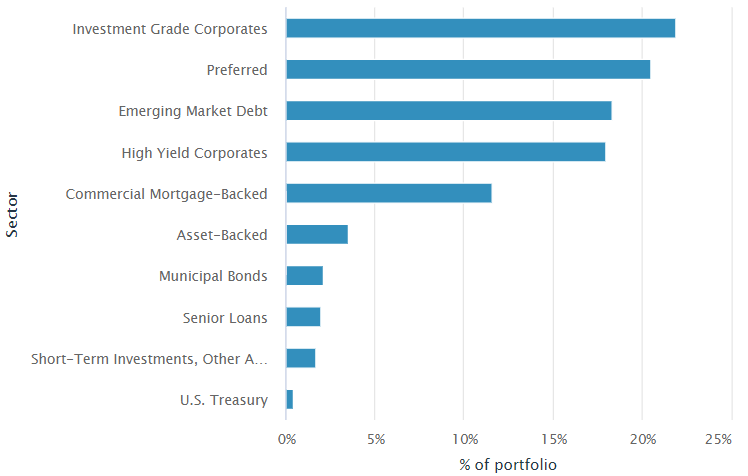

The fund holds a mix of assets:

{kind=link}

The largest allocation is to investment grade corporate bonds, followed by preferred securities and EM debt.

Its top holdings are as follows:

{kind=link}

Conclusion

NPCT is a multi-asset CEF. The vehicle invests in a mix of investment grade and junk bonds, and comes with a very high leverage of 39%. The fund's liabilities are floating rate, and the current weighted average cost of funds sits at a very high 5.97%.

The fund's structure and IPO timing have led to a significant underperformance in the past two years, the CEF being down roughly -40% since its issuance in 2021. Its main risk factors are rates and credit spreads, coupled with its high cost of funds. The floating rate liability feature has resulted in a significant income reduction for the CEF, which currently sports an unsupported 10.4% yield. With a return of capital figure of roughly 63%, NPCT's true yield is somewhere close to 5%. That is less than what a retail investor can make on treasuries currently.

This CEF will not generate robust results until the Fed starts cutting rates and its cost of funds decreases, together with a rally in fixed income. We are still not there yet, with the market now pricing the first-rate cut in mid 2024. There is no benefit to be had in allocating capital to NPCT at the moment, with a potential significant sell-off in the cards for this high beta fund. We are a Sell here for the name, with the intent to revisit the fund once the Fed starts cutting rates.

For further details see:

NPCT: Unsupported Yield With A High Cost Of Funds